BitMart VIP 인사이트 | 5월 암호화폐 시장 리뷰 및 핫 이슈 분석

- 핵심 의견: 2025년 5월, 거시적 차원에서는 '고인플레이션 + 매파적 성향' 구도가 심화되며 암호화폐 시장은 '상승 후 하락'하는 흐름을 보였습니다. 주요 핫 이슈는 CLARITY 법안 추진을 통한 규제 합법화와 Uniswap V4가 주도하는 온체인 금융 인프라 업그레이드에 집중되었으며, 기관 자금은 BTC로 뚜렷이 쏠린 반면 ETH와 SOL은 상대적으로 부진한 성과를 기록했습니다.

- 핵심 요소:

- 거시적 압력이 시장 심리를 지배: 미국 4월 CPI가 전년 동월 대비 3.8% 상승했으며, 연준 의사록은 1992년 이후 최대 내부 의견 차이를 보여 올해 금리 인하 기대감이 거의 사라져 위험 자산의 변동성을 확대했습니다.

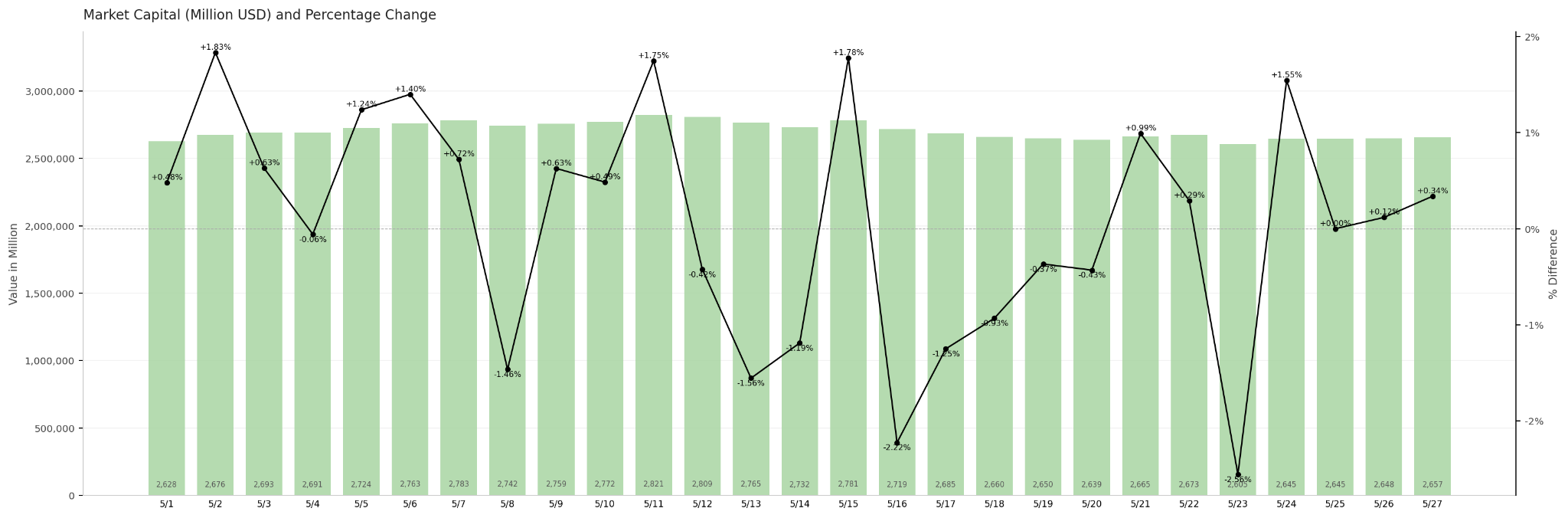

- 암호화폐 시가총액 선행 후행: 전체 시장 시가총액은 월 초 2.821조 달러로 월간 고점을 기록했으나, 매파적 신호의 영향으로 급락하며 월말 2.657조 달러에 마감, 월간 상승분을 대부분 반납했습니다.

- 핵심 자산별 성과 차별화: BTC는 8만 달러를 돌파한 후 조정을 겪었으나 여전히 기관 중심의 '하방 경직성' 특성을 보였습니다. ETH는 기관 선호도 하락의 영향을 받아 월 약 11% 하락했습니다. SOL은 생태계 유동성 회복이 더딘 탓에 BTC보다 부진한 성과를 보였습니다.

- 규제 입법의 이정표: CLARITY 법안이 상원 은행위원회 표결에서 15:9로 통과되어 디지털 자산의 상품/증권 이원 분류 기준을 명확히 했으며, 이는 미국 암호화폐 규제 체계의 중요한 전환점으로 평가됩니다.

- 온체인 금융 인프라 업그레이드: Uniswap V4 Hook 생태계가 폭발적으로 성장하며 DeFi가 '프로그래밍 가능한 유동성' 시대로 진입했습니다. Hyperliquid는 ETF 및 파생상품 확장에 힘입어 사상 최고치를 경신하며 고성장 온체인 금융 플랫폼으로 주목받고 있습니다.

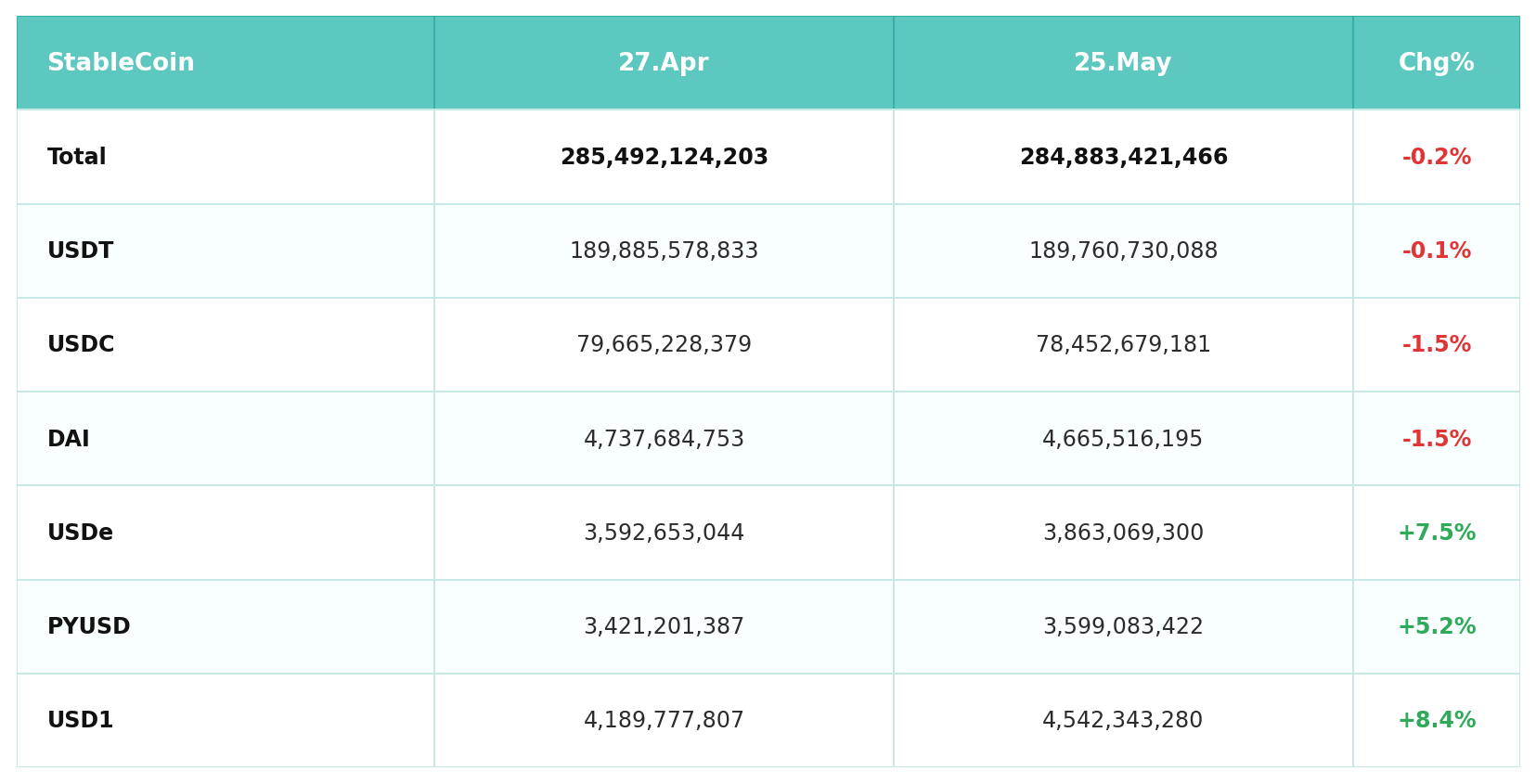

- 자금 구조 전환 및 신흥 스테이블코인의 부상: 스테이블코인 총 규모는 거의 변동이 없었으나 USDT, USDC는 소폭 감소한 반면, USD1, USDe 등 신흥 규제 준수형 스테이블코인은 역성장하며 자금이 수익형 및 규제 준수형 자산으로 전환되고 있음을 반영했습니다.

TL, DR

- The U.S. macro environment in May was generally characterized by "high inflation + hawkish expectations." The FOMC minutes revealed significantly intensified internal policy分歧, rapidly cooling market expectations for rate cuts this year. Meanwhile, the April CPI rose to 3.8% year-on-year, further reinforcing market pricing for higher rates for longer. Concurrently, U.S. stocks remained strong, driven by AI capital expenditure expansion and better-than-expected tech earnings, but experienced a pullback late in the month due to inflation and hawkish signals, significantly increasing volatility in risk assets.

- The May crypto market exhibited a "surge then plunge" trend. Early in the month, trading volume and total market capitalization strengthened alongside improving risk appetite and a BTC rally. However, hawkish signals from the Fed in mid-to-late May led to clear volume-price divergence and capital outflows. Total market cap quickly retreated after hitting a monthly high, with gains largely erased by month-end, indicating macro pressures continued to dominate market sentiment. For newly listed projects, GENIUS and BILL represent two major narratives – on-chain trading infrastructure and AI identity verification – reflecting current capital preference for projects with strong narratives related to AI, compliance, and infrastructure.

- May ETF flows showed a pattern of "BTC relatively resilient, ETH under sustained pressure." Although BTC ETFs saw periodic net outflows, cumulative inflows remained at historical highs, suggesting institutional long-term allocation logic hasn't fundamentally changed. In contrast, ETH ETFs experienced more pronounced outflows and liquidity pressures, reflecting a clear institutional risk appetite bias towards BTC. The stablecoin market remained largely stable in total size, with USDT and USDC contracting slightly, while emerging stablecoins like USD1, USDe, and PYUSD grew against the trend, indicating a capital shift from traditional trading stablecoins towards yield-generating and compliant stablecoins.

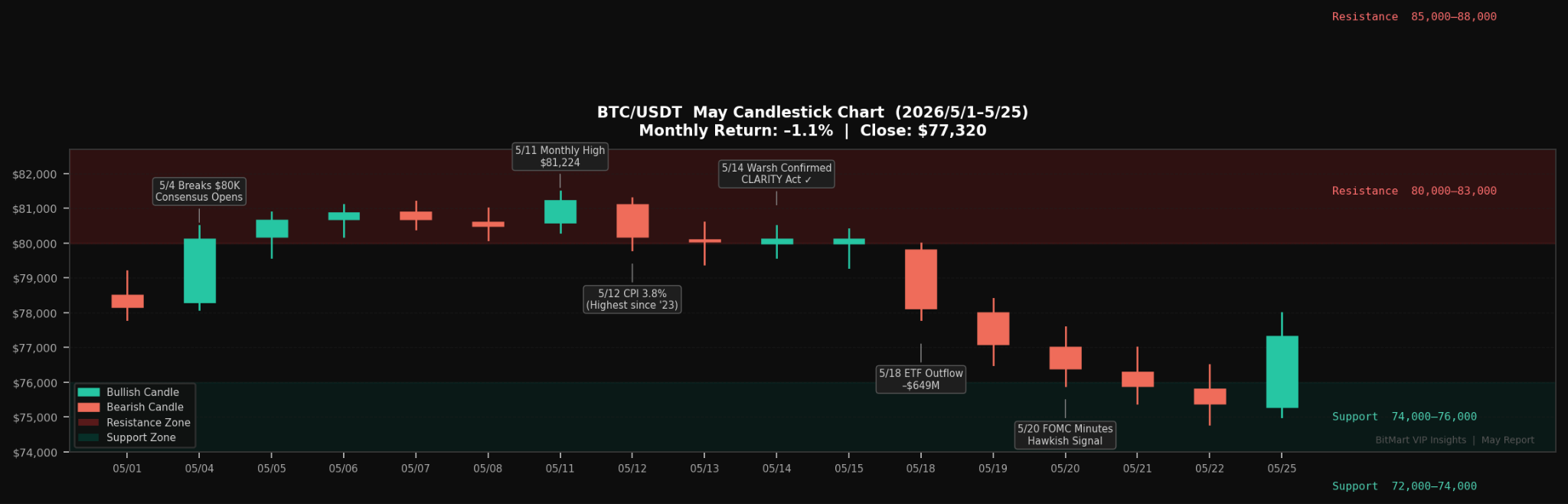

- In May, BTC showed a "post-breakout pullback" pattern, briefly surpassing the $80,000 mark to hit a new phase high, but subsequently retreating due to above-expected inflation, hawkish Fed rhetoric, and ETF outflows, significantly cooling market sentiment. In comparison, ETH and SOL lagged BTC. ETH continued to suffer from declining institutional preference, while SOL was impacted by slow DeFi ecosystem liquidity recovery, indicating market capital is mainly concentrated in core assets like BTC.

- The core hotspots in the May crypto market revolved around two main themes: "regulatory compliance" and "on-chain financial infrastructure upgrades." The advancement of the CLARITY Act is seen as a pivotal turning point for the U.S. crypto regulatory framework, while the SEC's proposed "innovation exemption" for tokenized stocks further strengthened the long-term narrative for RWA and on-chain securities markets. Meanwhile, Hyperliquid hit all-time highs driven by ETFs and on-chain derivatives expansion, reflecting market capital refocusing on high-growth on-chain financial platforms. In DeFi, the explosive growth of the Uniswap V4 Hook ecosystem propelled "programmable liquidity" as a new narrative.

- In June, the market will focus on the first FOMC meeting chaired by Warsh and the latest dot plot. The Fed's stance on inflation and the rate path will directly impact U.S. bond yields, BTC trends, and overall risk appetite. On the regulatory front, the CLARITY Act enters a full Senate vote. If successful, it will further clarify the digital asset regulatory framework and accelerate institutional inflows, ETF growth, and compliant stablecoin development. Meanwhile, Hong Kong's stablecoin HKDAP completed Ethereum mainnet testing and plans a formal issuance by the end of Q2, suggesting that the competition for Asian compliant stablecoins and on-chain payment/RWA ecosystem development may intensify in June.

1. Macro Perspective

Policy Direction

May marked the most significant leadership transition of this cycle for the Fed's policy framework. The minutes of the April 28–29 FOMC meeting (the last under Chair Powell), released on May 20, revealed policy分歧 at its highest level since 1992, with 4 dissenting votes. Governor Stephen Milan favored a 25bp cut, while members Hammack, Kashkari, and Logan opposed maintaining easing bias language in the statement, effectively calling for a stronger stance. The minutes also showed that most officials explicitly stated that if inflation remained persistently above 2%, rate hikes would become an "appropriate option." Market pricing adjusted sharply, with expectations for a 2025 rate cut nearly eliminated and the implied probability of a rate hike by late 2026/early 2027 rising significantly.

On the personnel front, the Senate confirmed Kevin Warsh as the 16th Fed Chair on May 13 with a 54-45 vote, the closest margin in modern history, largely along party lines, with only Senator Fetterman (D-PA) crossing party lines to support. Powell's term officially ended on May 15. Warsh's first FOMC meeting as Chair is scheduled for June 16–17, where the latest dot plot and Summary of Economic Projections (SEP) will be released, with the market scrutinizing every word.

U.S. Equity Market Trends

The U.S. stock market broadly continued its strength in May. The S&P 500 recorded positive returns for 8 consecutive weeks, its longest winning streak since December 2023. The Nasdaq posted gains in 7 out of 8 weeks. The Dow Jones Industrial Average closed near 50,580 on May 22, hitting a new phase high during the month. The main driver was a better-than-expected Q1 earnings season, with major tech companies generally beating estimates and continued expansion in AI capital expenditure boosting sentiment. Progress in U.S.-Iran ceasefire talks also provided external support for risk assets. In late May, the April CPI jump to 3.8% and hawkish signals from the FOMC minutes triggered a brief pullback, but overall equity market resilience remained robust.

Inflation Data

The Bureau of Labor Statistics released April CPI data on May 12. CPI grew 3.8% year-over-year, the highest since May 2023, with a monthly increase of 0.6% (down from March's 0.9% but still significantly above expectations). Core CPI (excluding food and energy) was +2.8% YoY and +0.4% MoM, both exceeding forecasts. By component, energy prices rose another 3.8% month-over-month in April, a continued pass-through from the March oil price shock. The shelter index increased 0.6% month-over-month, remaining stubborn. Food prices rose 0.5% MoM, with food at home up 0.7%. Overall, above-expected inflation dashed hopes for a natural cooldown following the energy shock. The core reading of 2.8% YoY makes it difficult for the Fed to shift back to accommodation anytime soon.

Employment Data

The Labor Department released the April jobs report on May 8. Non-farm payrolls increased by 115,000, a significant slowdown from the revised March figure of 185,000, but still slightly above the average expectation influenced by post-truce risk-on sentiment. The unemployment rate held steady at 4.3%, and the labor force participation rate ticked up slightly. Average hourly earnings rose 3.6% YoY and 0.2% MoM to $37.41, indicating contained wage inflation pressures. Job gains were mainly in healthcare (+37,000), transportation and warehousing (+30,000), and retail (+22,000). Federal government employment continued to decline, while information and manufacturing saw small decreases. Overall, the April data showed a "moderate deceleration" rather than a sharp deterioration. In the current high-inflation environment, this neither triggers a rate cut nor provides urgency for a hike, further narrowing the policy window.

Political Factors

The U.S.-Iran ceasefire was the core geopolitical variable throughout May. After the initial round of talks on April 8, a new two-week temporary ceasefire was reached in early May through Pakistani mediation. The U.S. also advanced "Operation Freedom" to ensure commercial shipping through the Strait of Hormuz. Brent crude fell significantly from its peak to around $94.80/barrel, and WTI dropped near $95.75. However, the fragility of the ceasefire remained evident, as Iran's Supreme National Security Council continued to reject the full reopening of the Strait, leading oil prices to rebound to around $108 for Brent. The temporary respite from the ceasefire provided breathing room for global risk assets and was a key macro catalyst for BTC's break above $80,000.

On the crypto regulatory legislative front, the full text of the "CLARITY Act of 2025" was released by the Senate Banking Committee on May 11. It passed the committee markup by a 15-9 vote on May 14, advancing to the full Senate for consideration. This is substantive progress following the end of the comment period in late April. Polymarket odds for its passage within the year subsequently rose above 85%.

Outlook for Next Month

Looking ahead to June, Warsh's first FOMC meeting (June 16–17) is the most critical macro event. The updated dot plot will be released simultaneously, and the market will be highly sensitive to his weighting of inflation versus employment. If April's 3.8% headline and 2.8% core CPI readings persist, Warsh will face immense pressure. A clearly hawkish tone could test Bitcoin's ability to hold above $75,000. The May CPI data, released on June 10, will be the last key inflation input before the dot plot. On the legislative front, the outcome of the full Senate vote on the CLARITY Act will be the most important regulatory signal of this cycle.

2. Crypto Market Overview

Token Data Analysis

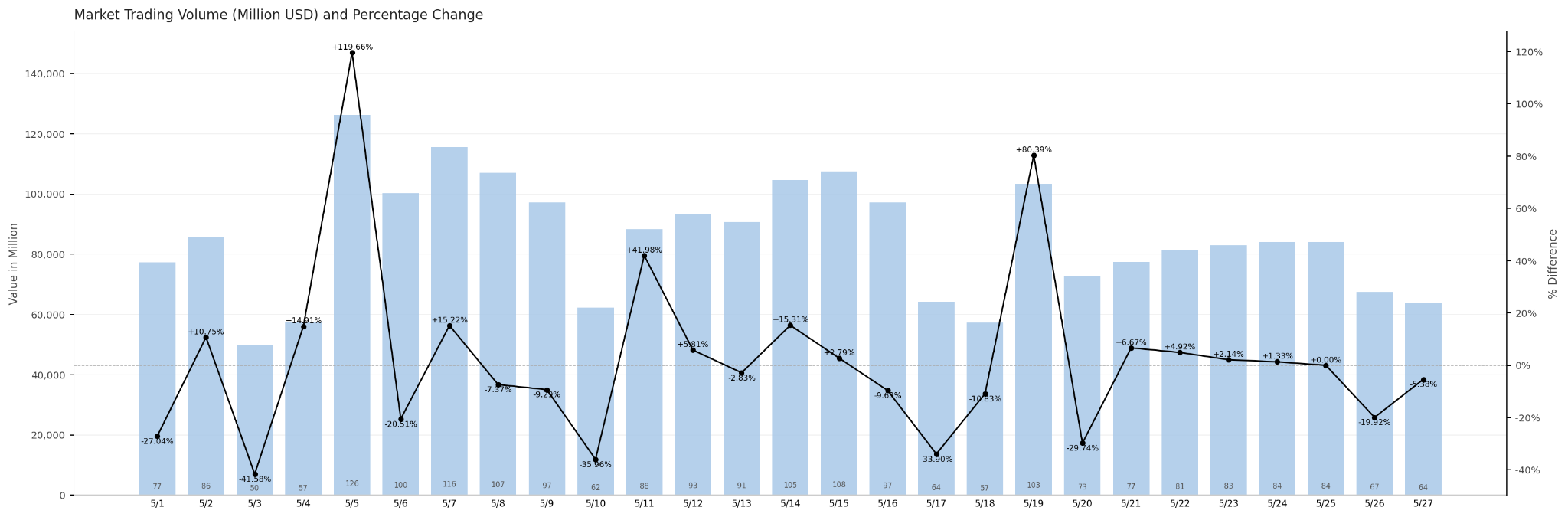

Trading Volume & Daily Growth Rate

Market trading volume remained active in May, but the structure showed clear "volume-price divergence" signals. Volume concentrated in two phases: First, from May 5–7, daily turnover reached $126.2B, $100.3B, and $115.6B respectively, the month's highest. Market cap rose concurrently during this period, a classic volume-price increase trending rally. Second, around May 14–15 and May 19, volume surged back to the ~$100B level, but market cap declined simultaneously. This bearish divergence of rising volume and falling prices suggested dominant short-side pressure and concentrated selling. Late in the month (May 26–27), volume contracted to $67.4B and $63.7B, the lowest range of the month, indicating cautious short-term sentiment and increased wait-and-see behavior. Overall, the May volume structure reveals a complete sentiment evolution cycle from "chasing highs" to "stop-loss exodus" to "hibernation."

Total Market Cap & Daily Change

Total crypto market capitalization in May followed a "rise then fall, stabilizing at month-end" pattern. Starting from the end of April's $2.615T base, the market cap climbed steadily alongside improving risk appetite and BTC's break above $80,000, reaching a monthly high of $2.821T on May 11, up 7.8% from the start. However, sentiment reversed sharply following the hawkish signals from the May 20 FOMC minutes. The market cap quickly fell from its peak to a monthly low of $2.605T on May 23, a decline of about 7.7% from the high. It rebounded slightly to $2.657T by month-end, roughly flat (+1.6%) compared to the end of April, with almost all monthly gains erased. Overall, the "surge and plunge" pattern of total market cap in May clearly reflects the suppressing effect of macro disturbances on crypto market sentiment – short-term catalyst-driven rallies struggle against systemic risk aversion.

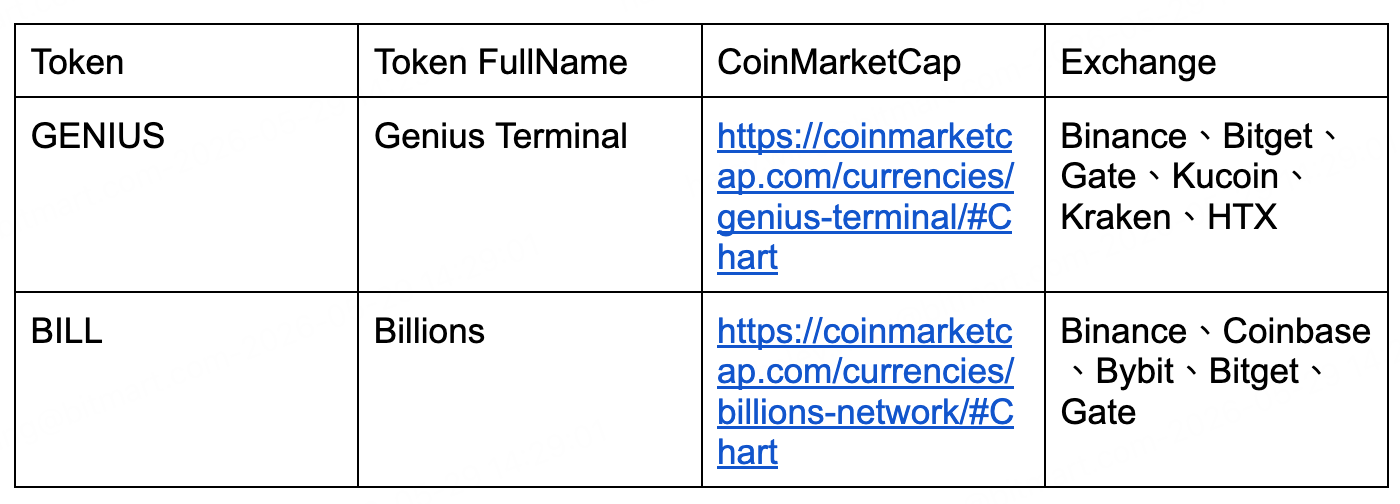

Hot Tokens in May

Among tokens newly listed in May, GENIUS and BILL represent the two main narrative lines currently favored by capital: on-chain trading infrastructure and AI identity verification. GENIUS, incubated by YZi Labs, is positioned as an all-in-one on-chain trading operating system, surpassing $2 billion in trading volume in its first week on Binance. BILL, leveraging a ZK-proof-driven decentralized human identity protocol, saw its price surge over 10x from its TGE price, backed by Coinbase Ventures and Polychain. Their common characteristics are strong backer support, simultaneous listing on major exchanges, and clear product narratives, confirming that projects resonating with macro themes like AI and compliant infrastructure still command a significant liquidity premium in the current market environment.

Among tokens newly listed in May, GENIUS and BILL represent the two main narrative lines currently favored by capital: on-chain trading infrastructure and AI identity verification. GENIUS, incubated by YZi Labs, is positioned as an all-in-one on-chain trading operating system, surpassing $2 billion in trading volume in its first week on Binance. BILL, leveraging a ZK-proof-driven decentralized human identity protocol, saw its price surge over 10x from its TGE price, backed by Coinbase Ventures and Polychain. Their common characteristics are strong backer support, simultaneous listing on major exchanges, and clear product narratives, confirming that projects resonating with macro themes like AI and compliant infrastructure still command a significant liquidity premium in the current market environment.

3. On-Chain Data Analysis

Analysis of BTC and ETH ETF Inflows/Outflows

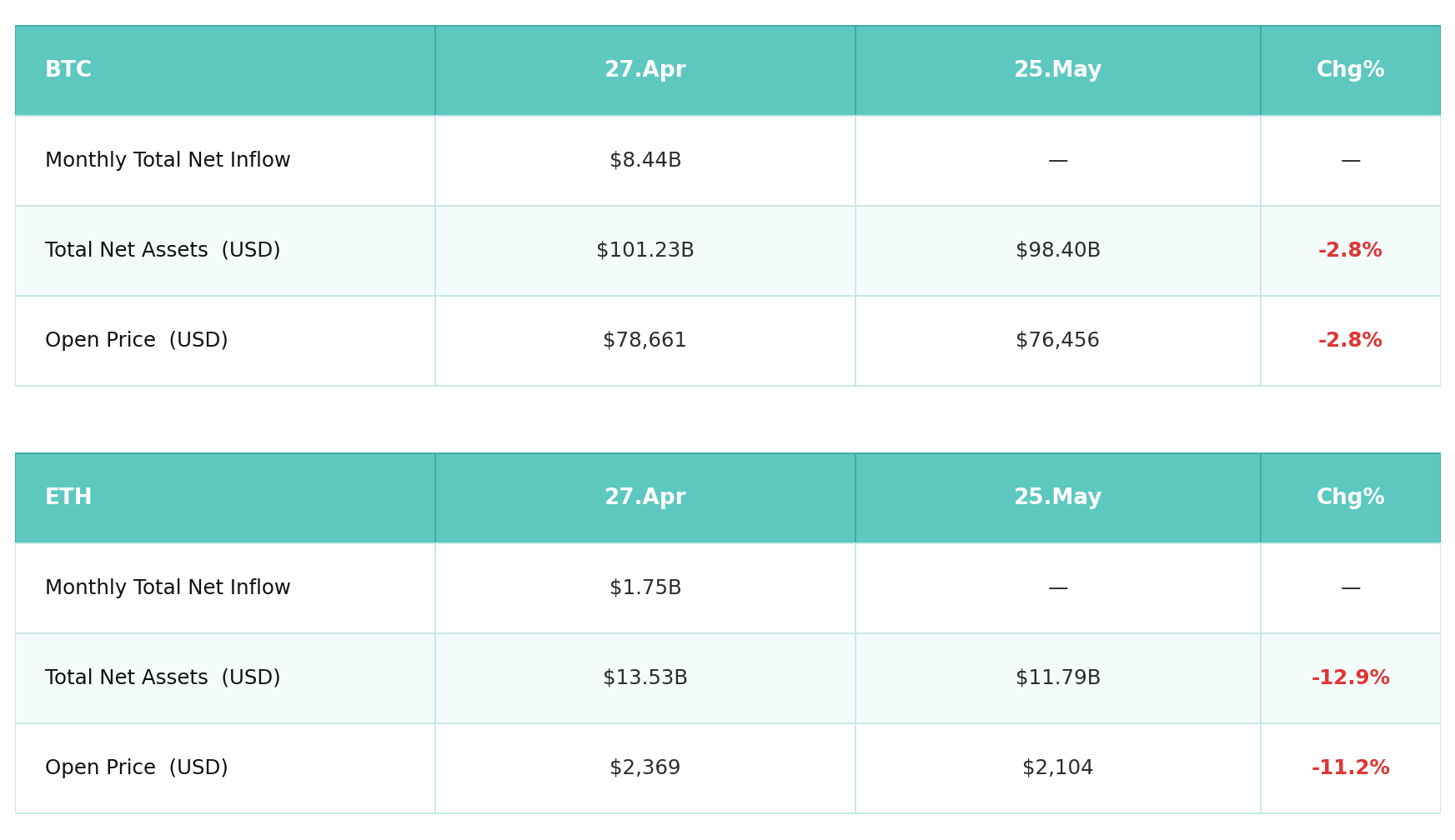

Bitcoin spot ETFs faced overall pressure in May. Net asset value (NAV) fell from $101.23B at end-April to $98.40B (-2.8%), roughly matching the concurrent decline in BTC price, suggesting relatively stable holdings with the NAV decrease primarily driven by price rather than large-scale redemptions. As of May 26, BTC ETFs saw a single-day net outflow of $334M, but cumulative net inflows remained at a historic high of $56.75B, indicating that the institutional long-term allocation logic hasn't wavered. Ethereum ETFs faced more pronounced pressure: NAV declined from $13.53B to $11.79B (-12.9%). ETH price fell 11.2% month-to-date, which, combined with marginal net outflows, created a dual drag. On May 26, ETH ETFs recorded a net outflow of $35.04M, with daily volume of only $614M, significantly lagging BTC's $4.4B volume. This indicates that institutional willingness to allocate to ETH remains markedly weaker than BTC. Overall, May ETF data showed a "BTC resilient, ETH under pressure" pattern, consistent with a phase of contracting risk appetite. However, the massive cumulative holdings base also suggests that institutional capital hasn't entered a systemic retreat mode.

Analysis of Stablecoin Inflows/Outflows

The stablecoin market size was broadly stable in May, with total circulating supply contracting slightly from $285.49B on April 27 to $284.88B on May 25 (-0.2%), indicating no systemic capital exodus from the venue. The structural divergence is more noteworthy. The two major stablecoins, USDT (-0.1%) and USDC (-1.5%), saw mild contraction, possibly related to institutions marginally reducing on-chain exposure amid rising macro uncertainty (Moody's downgrade of U.S. sovereign rating, hawkish FOMC). Conversely, emerging stablecoins expanded against the trend: USD1 grew 8.4%, USDe 7.5%, and PYUSD 5.2%. The rapid volume increase in USD1 was particularly prominent, highly resonant with improved regulatory expectations driven by the CLARITY Act legislative progress. Overall, the stabilization of total stablecoin supply means ample "ammunition" in the market, while the structural shift towards new varieties reflects capital pre-positioning in the regulated compliance track.

4. Price Analysis of Major Currencies

Bitcoin (BTC) Price Analysis

In May, Bitcoin completed its most notable technical breakout of the year so far, followed by a significant pullback. The full-month trajectory showed a three-phase structure: "high-volume breakout – institutional profit-taking – ETF fund exodus."

BTC started May around $78,661 from the end of April, opening at $78,178 on May 1. Benefiting from the geopolitical ceasefire, the tug-of-war intensified around the $80,000 level. On May 4, BTC closed above $80,000 for the first time since January 2026, triggering approximately $300 million in short squeezes and creating a brief mechanical acceleration. BTC hit a monthly high of $81,224 on May 11, the highest price so far in May. Sentiment then cooled rapidly following the release of the April CPI data on May 12 (YoY 3.8%, significantly above expectations) and the FOMC minutes (May 20) revealing that most officials leaned towards a hawkish stance favoring rate hikes. Starting May 18, U.S. spot BTC ETFs recorded net outflows for 6 consecutive trading days, totaling approximately $1.256 billion. BTC fell to a monthly low of $75,195 on May 23. By May 25, the price had somewhat recovered to around $77,320.

The key resistance zone above is $80,000–$83,000; a firm hold above this is needed to open the path towards $85,000–$88,000. The primary support below is the $74,000–$76,000 range; a loss of this level could lead to a test of the $72,000 area