Stop valuing ETH based on fees; ‘Treasury logic’ is the future?

- 核心观点:以太坊不应被视为靠手续费创收的企业,而是一个保护约2500亿美元加密资产的“金库”。ETH是保护此金库的“锁”,其价值直接决定了金库的安全等级。当前ETH市值被严重低估,合理价格应远高于市场价。

- 关键要素:

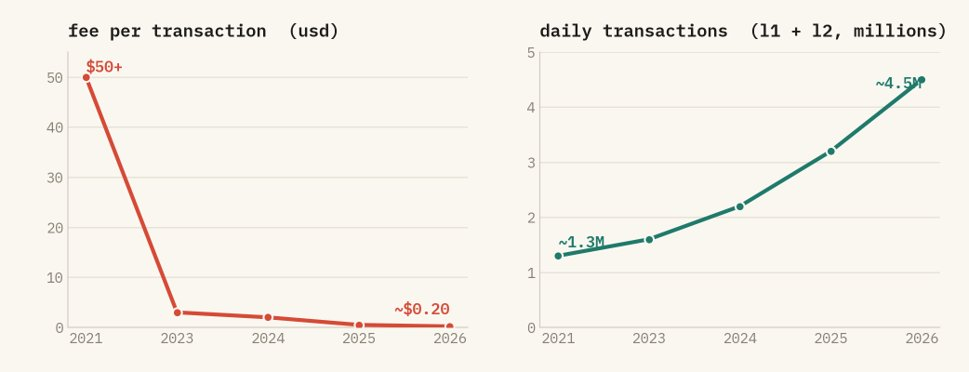

- 手续费是网络摩擦而非收入。以太坊单笔手续费从50多美元降至0.2美元,但交易量翻三倍,成功网络的标志是将费用降至零。

- 转为权益证明后,攻击成本与ETH价值绑定。控制33%和66%的质押ETH可分别瘫痪或篡改网络,作恶成本使用ETH计算且作恶即销毁。

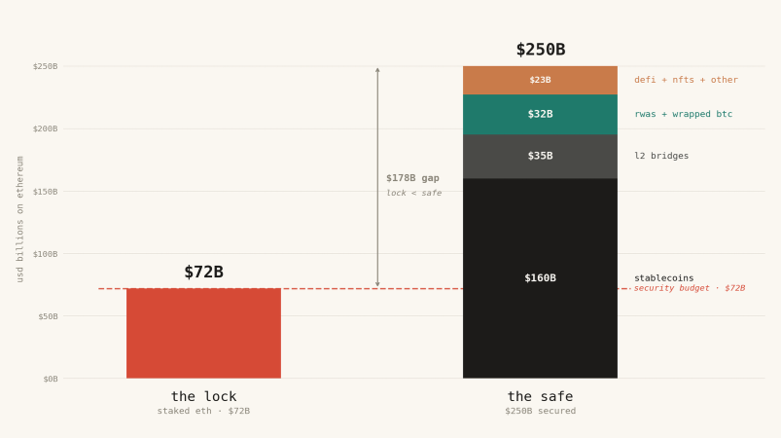

- 以太坊链上资产约2500亿美元,但保护资产的质押ETH价值仅720亿美元。安全比(锁:保险箱)严重失衡,如同用破锁保护金条。

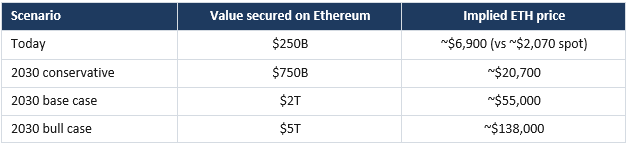

- 根据模型,为保护现有资产,ETH合理价格应为6900美元(当前约2070美元)。随着链上资产增至数万亿,ETH需涨至数万美元。

- 以太坊的安全性自负盈亏,与依赖外部法律或社区担保的Linux或DTCC截然不同。ETH不能价值为零,否则链无安全保障。

Original author: Tom Dunleavy, Venture Partner at Varys Capital

Compiled by: Yuliya, PANews

Editor's Note: The market currently views Ethereum as a traditional enterprise, calculating its P/E ratio based on the fees it generates, and concluding it is overvalued. However, Tom Dunleavy proposes a completely different framework: fees are not revenue, but network friction; Ethereum is not a company, but a "vault" protecting hundreds of billions of dollars in assets, and ETH itself is the lock. Below is a translation of the original text:

TLDR

- Stop valuing Ethereum based on fees. Fees are actually a hindrance; a successful network will inevitably strive to reduce them to zero. Today, ETH fees have dropped from over $50 at their peak in 2021 to around $0.20, yet transaction volume has more than tripled. The plunge in fees indicates the network's great success, not its decline.

- After transitioning to Proof of Stake (PoS), ETH became the lock protecting the asset vault. To attack Ethereum, you must control the staked ETH. Controlling one-third can halt the network; controlling two-thirds can alter the record. In either case, the cost of malicious action is denominated in ETH, and any ETH used for such actions is destroyed by the system. This inextricably links the value of ETH to the network's security. No network operated this way before the advent of staking.

- Currently, approximately $250 billion in assets (including stablecoins, tokenized assets, L2 cross-chain funds, etc.) are held on the Ethereum chain, but the staked ETH protecting these assets is only worth about $72 billion. It's like using a cheap, flimsy lock to secure a vault full of gold bars. Logically, a fair price for ETH should be around $6,900 (it is currently $2,070). If on-chain assets grow to trillions in the future, ETH's price must rise to tens of thousands of dollars to justify its security role.

- Arguments like "Ethereum is like a free Linux system" or "like the DTCC" are incorrect. The security of Linux and the DTCC is external (e.g., open-source community goodwill or legal guarantees from governments and banks). But Ethereum's security is self-funded, using its own token, ETH. Therefore, ETH must have value, whereas Linux does not.

- If ETH fails, Crypto will likely fail too.

Fees Are Not Revenue, They Are Friction

Last week, Bankless founder David Hoffman caused a stir in the crypto space when he announced he had sold all his ETH. While I respect David's decision, I believe the way people evaluate ETH and other PoS public chains is outdated. I've discussed my new framework with many people on shows, but it seems it didn't quite sink in (maybe my fault for not explaining well), so today I'm laying it all out clearly.

New things require new perspectives. Let me introduce a brand new ETH valuation model.

Many people treat Ethereum as a company and the fees it collects as revenue. When they see fees declining, they think the "company" is failing and the token is overpriced. This completely puts the cart before the horse. Once you truly understand this, you'll never see it that way again.

In reality, fees are like taxes. The higher they are, the less people want to use the network. Lowering fees encourages more participation, attracting more applications and capital to the chain. The data doesn't lie: single transaction fees have dropped from over $50 in 2021 to around $0.20 today, yet transaction volume has hit all-time highs, more than tripling the 2021 level, with L2s now handling approximately 85% of transactions. It's cheaper to use, so more people use it. A successful settlement network should naturally drive its transaction costs down to zero.

Ethereum's fees have plummeted while transaction volume hits new highs. It has become cheaper and more widely used. L2s now carry about 85% of the throughput.

So, if fees are the wrong metric, what is the right one?

Ethereum is a Giant Vault, ETH is the Lock

Stop thinking of Ethereum as a company. Think of it as a giant vault. This vault holds approximately $160 billion in stablecoins, $20 billion in RWAs (like US Treasuries, money market funds, and private credit), $35 billion in L2 cross-chain assets (with L2 networks inheriting Ethereum's consensus by design). Additionally, there are about $12 billion in wrapped Bitcoin, and roughly $20 billion distributed across DeFi positions, NFTs, and on-chain treasuries. In total, on-chain assets are approximately $250 billion and growing every quarter.

The security of a vault depends entirely on its lock. And the value of this lock is precisely what people are miscalculating. On Ethereum, this lock is made of ETH.

Under the old Proof of Work (PoW) system, you secured the network with mining hardware. The lock was bought externally; its cost wasn't tied to the token's value. But now it's Proof of Stake (PoS), and everything has changed. To attack Ethereum now, you can only buy and control the staked ETH. The lock is made of the token itself. This means the security level of the vault and the market price of the token have become one and the same. You cannot separate them.

The Current State: Lock Cheaper than the Safe

This is what the market is overlooking. Today, the total value of all staked ETH protecting Ethereum is only $72 billion. But it protects assets worth $250 billion. The money inside the safe is more than double the cost of the lock protecting it.

This is dangerous. If what you are protecting is worth more than the cost of breaking in, your vault is inadequate. For Ethereum to securely safeguard this $250 billion, the defensive staked capital must exceed $250 billion, not be less than one-third of it.

Currently, only about 30% of ETH is staked. So, simply for this 30% staked amount to match on-chain assets, ETH's total market cap needs to be more than three times (1 / 0.30) the value of on-chain assets. Currently, ETH's market cap is roughly equal to the assets it protects (about 1x). But according to my logic, it should be over 3x. Based on the current $250 billion, a fair price for ETH would be around $6,900, not the current $2,070. That means, even without any new capital influx, based solely on the assets it now protects, ETH's price should more than triple. This aligns with the directional model proposed by BitMine Chairman Tom Lee.

"But Circle can freeze USDC, so it doesn't need ETH's protection."

Every time I say this, someone brings up this point, but it's profoundly wrong. Here's why:

People think that if Ethereum is attacked, Circle, the issuer of USDC, could simply freeze the attacker's address and reissue the coins. So, those hundreds of billions shouldn't be counted in Ethereum's security responsibility.

But think about it: Circle's freeze mechanism operates via a smart contract. It executes on Ethereum and relies on Ethereum's ledger. If Ethereum's consensus is compromised, there is no single honest chain that everyone agrees on, and the freeze mechanism cannot function.

Furthermore, Circle could have chosen a private database instead of Ethereum. They chose Ethereum for its neutrality, deep liquidity, and composability with other projects. Having enjoyed these benefits, the consequence is this: USDC's very existence is tied to Ethereum's security. You can't have the benefits without assuming the dependency risk.

Moreover, the common assumption is that attackers want to steal USDC. That's not the point. If Ethereum collapses, that $150+ billion isn't stolen; it becomes trapped on a chain with no consensus, unable to be redeemed, throwing all loans and transactions relying on that chain into chaos. The value of these assets isn't appropriated by the thief; it is destroyed. And this destroyed value is a critical factor for security considerations.

An attacker doesn't even need to steal money to profit. They could short ETH, short the entire ecosystem, or simply be a hostile entity that profits from crippling the network. The more value held on-chain, the greater their incentive to attack. So, our security budget must scale with the total assets on the chain, not just the easily stealable portion.

If you place your money on Ethereum, you are consuming its security, whether you have a "freeze" button or not. All money counts.

"Ethereum is just Linux" or "Ethereum is the DTCC."

Another common rebuttal from smart people.

- The first analogy: Ethereum is like Linux. It's foundational infrastructure powering the internet (or web3), but worthless as an asset. Open-source infrastructure is a free public good. Value is captured by applications built on top, not the base protocol. Therefore, ETH will be the same – extremely important but fundamentally valueless.

- The second analogy: Ethereum is like the DTCC (Depository Trust & Clearing Corporation), the infrastructure behind nearly all US securities transactions. The DTCC processed $3,700 trillion in transactions in 2024, earning ~$2.5 billion in revenue, but less than $500 million in profit. It is critical, regulated, but its value is a tiny fraction of the transaction volume. Infrastructure is cheap. Even if Ethereum processes trillions, it will only capture a sliver of utility profit, and that's it.

Both analogies fail for the same reason.

Linux and the DTCC borrow their security from external sources. Linux relies on the open-source community, reputation, and decades of code review. The DTCC relies on US law, federal regulators, and the backing of big banks with dollars and treasuries. Their security guarantees are outside the system. This is precisely why the DTCC can settle vast fortunes while capturing almost no value. It is a member-owned utility designed to run at cost. It doesn't need a valuable token because trust is provided by governments and banks.

Ethereum lacks these external safeguards. No government enforces it. No member banks back it. No law can reverse a fraudulent settlement. The only barrier between Ethereum and an attacker is the market value of the staked ETH securing it. Ethereum must purchase security for every single block, on the open market, using its own asset.

This is the fundamental difference. Linux is software; no one is required to possess a scarce asset to run it. The DTCC provides collateral in dollars, external to itself. Ethereum's collateral is ETH, internal to itself. You cannot commoditize it to zero because security isn't a line of code; it's an amount of value that must be locked and placed at risk. Strip away ETH's value, and you don't create a leaner Linux. You create an uncollateralized chain that no one would trust with a single dollar.

So, stop comparing Ethereum to Linux or the DTCC. Instead, compare it to the dollars and treasuries backing the DTCC. No one values the US dollar based on the fees charged by the DTCC. You would evaluate the clearinghouse's fees separately and assess the dollars and treasuries serving as the system's collateral as a monetary base worth trillions. ETH is not the clearinghouse. ETH is the collateral that builds the clearinghouse. That is the asset you are buying.

Linux never needed a treasury. Ethereum's security budget is a treasury, and it is denominated in ETH.

Looking Ahead and Market Dynamics

Let's follow this logic further. This model completely ignores fees or market hype. It focuses on one core question: How much money will be settled on Ethereum in the future? And to protect that money, how much must ETH be worth?

Stablecoins are on track to break $1 trillion in the coming years. RWA tokenization is projected to reach trillions by 2030. Combined with various on-chain applications, the assets Ethereum must protect will surge from today's $250 billion to trillions. Maintaining that "greater than 3x" security multiplier, you can calculate how high ETH's price must rise as more money flows in.

Even if you are pessimistic and adjust the security multiplier down, the principle holds. On-chain capital is growing (the variable), and the security multiplier (the leverage). No matter how you calculate it, the long-term direction points upwards.

"This is blindly optimistic. The market will never price this in."

This is the most valid criticism. I am discussing what ETH *should* be worth, not what the market will *immediately* price it at. There is no forced arbitrage mechanism to close this gap. Furthermore, my "ETH should go up" logic has clearly been wrong on price action over the past few years. Let me address this.

- On what closes the gap: Ethereum is not arbitrage; it is demand for the systemic pricing asset. As value settles on Ethereum, ETH is used as collateral, a paired trading asset, and is staked to earn the network's base yield. This demand grows with the activity it supports. Reserve assets aren't priced by their cash flow; they are priced by how urgently the surrounding system needs to hold them. Gold is worth over $18 trillion and generates no cash flow. ETH is the reserve asset for on-chain finance, and this framework merely measures how large that reserve must be.

- On the staking multiplier: My mental model treats the staking multiplier as a range, not a fixed target. At current staking rates, parity (staked ETH equals protected value) occurs around a 3.3x market cap multiple. A reasonable range spans from a loose end of ~1.7x to a strict end of ~5x, where the cost to attack via a two-thirds staking share must equal the total protected value. The price tracks the protected value times some multiplier within this range. Fixing it to one specific number sacrifices rigor, and this is where reasonable people can disagree without breaking the model.

- On reflexivity: The model does have multiple equilibria, and nothing deterministically selects the highest one. Today, Ethereum is secure enough with coverage below the floor because acquiring a one-third staking share has poor liquidity, slashing is brutally punitive, and the social layer can fork out an attacker. These are real, but they determine if an attack *succeeds*, not if the coverage is *adequate* as risk grows. Thin coverage might be tolerable protecting $250 billion. When dealing with two or five trillion in regulated institutional capital, coverage is no longer an academic question. The gradient to close the gap increases monotonically with adoption.

Finally, the most painful counterpoint is ETH's price action over the last 5 years. Logically it should go up; in reality, it has been declining. I believe the main reason is: in the past, there wasn't enough money on-chain for security to be a major concern. No one cared when there was only $50 billion on-chain; people started feeling uneasy when it hit $175 billion; when it reaches $1 trillion, the first question large institutions will ask before entering will be: "Is this chain secure?" The answer to this question relies entirely on ETH's price. My model can't predict *when* this will happen, but it tells you that the force for upward price pressure increases relentlessly as on-chain capital grows, a fact that even bears cannot deny.

Some counter with Bitcoin, saying its security budget is tiny relative to its market cap. But Bitcoin primarily protects itself. Ethereum protects other people's dollars and assets – a much heavier responsibility! And the trends are already visible: more ETH is being staked, compliant products are continuously buying ETH, and the burning mechanism destroys ETH with on-chain activity. All these confirm the demand growth I am describing.

Those fixated on fees and cash flow will continue to claim ETH is overvalued. They have completely reversed cause and effect. On-chain activity comes first, and it creates the need for security. ETH *must* be valuable to secure the entire ecosystem. Fees are a friction you should strive to eliminate, not a metric to value ETH.