The UAE leaves OPEC: What’s the impact?

- Core View: The market’s real reaction to the UAE leaving OPEC is not a surge in oil prices, but rather a deep contango in the futures curve, indicating that near-term panic stems from geopolitical noise and headline risks. Far-dated futures prices have barely moved, suggesting the market views this move as neutral for medium-term oil prices, but it weakens OPEC’s ability to act as a price stability anchor.

- Key Elements:

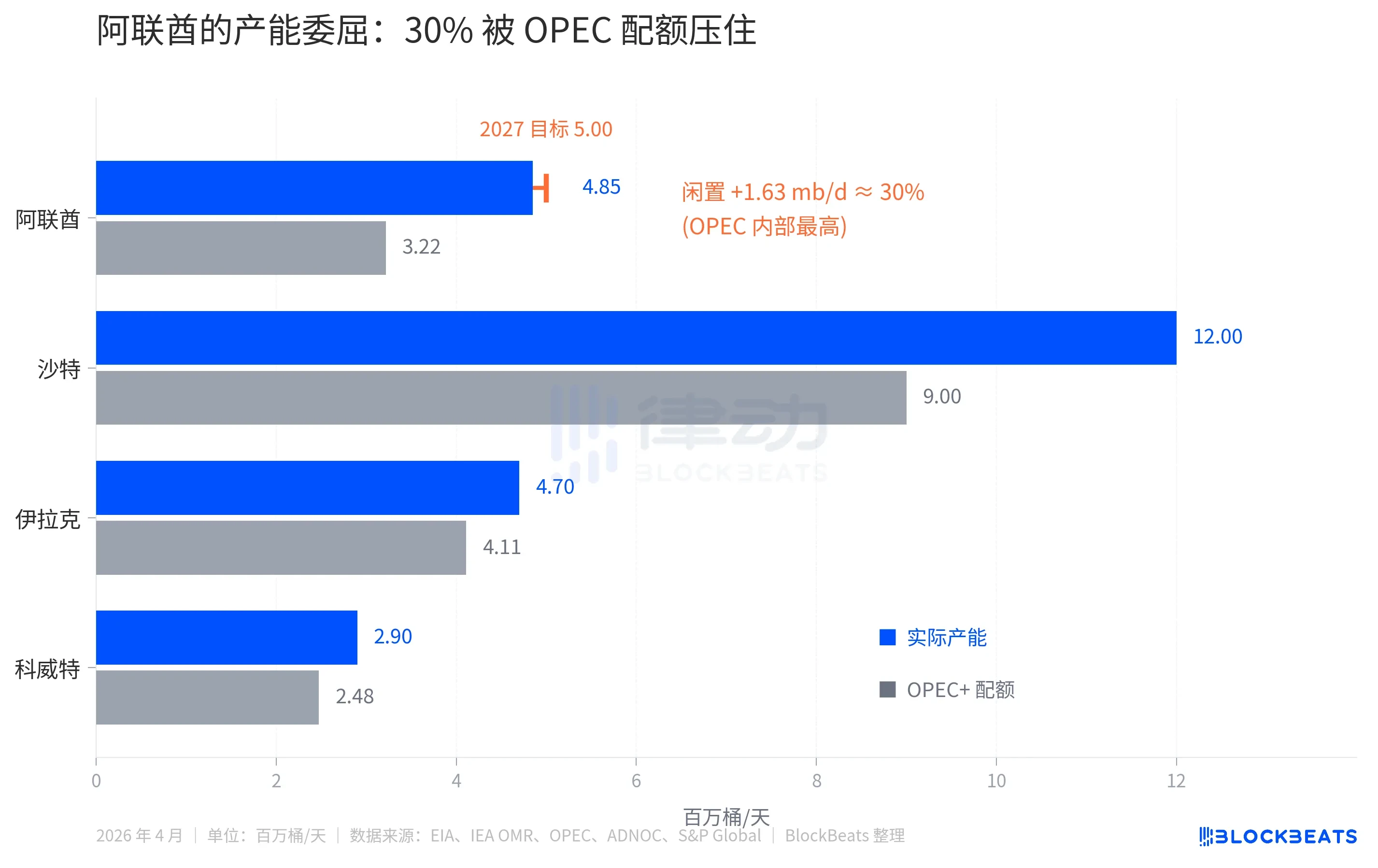

- The UAE’s exit is mainly due to its production capacity (4.85 mb/d) being suppressed for a long time by OPEC+ quotas (3.22 mb/d) by about 30%, resulting in billions in lost daily revenue. ADNOC also plans to increase capacity to 5.0 mb/d by 2027.

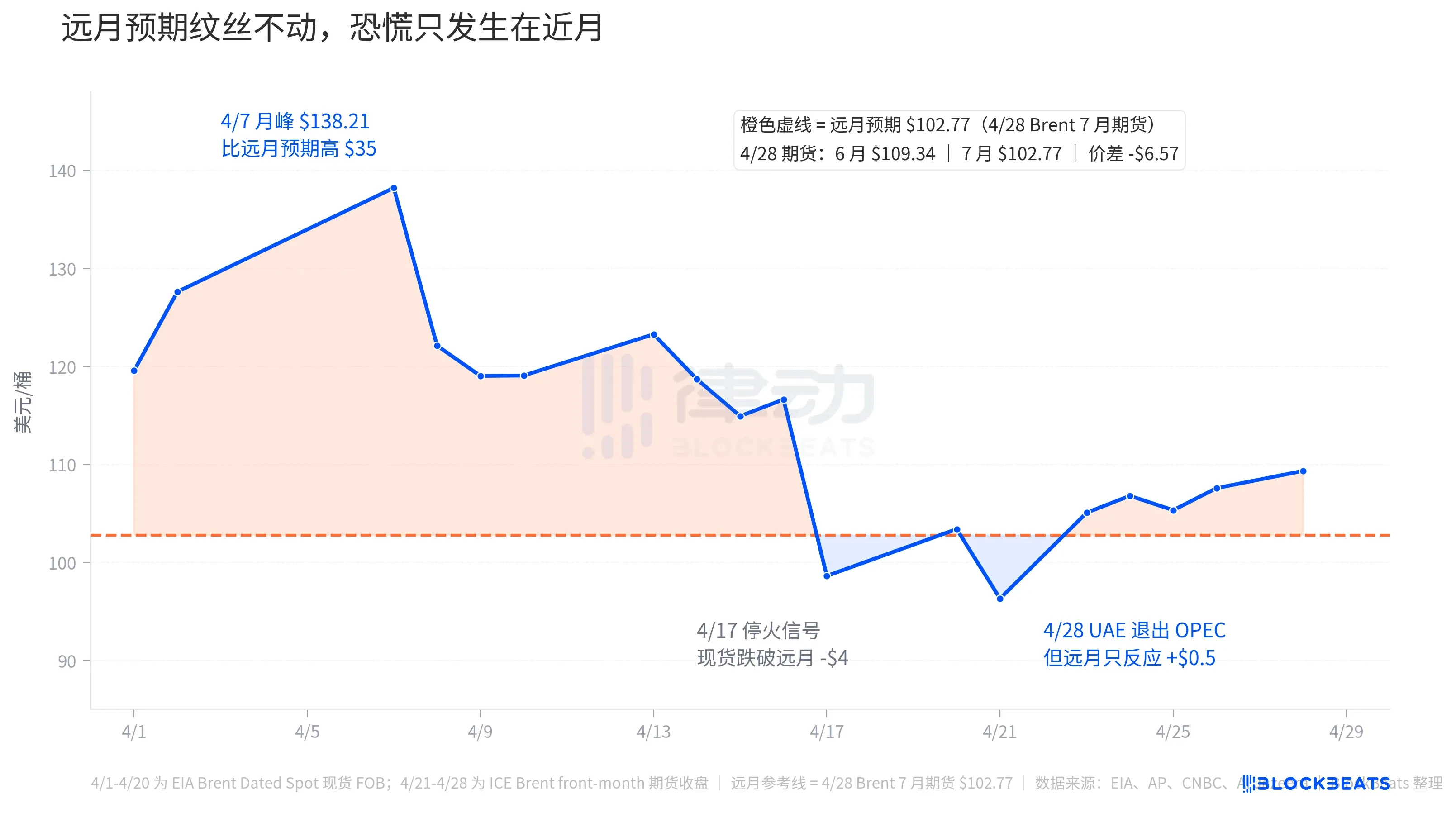

- On April 28, Brent June futures surged to $109.34, but July futures only rose to $102.77, a spread of $6.57. Far-dated futures remained almost unchanged throughout April.

- At the height of the Hormuz crisis in early April, Brent spot prices were $35 higher than far-dated futures (panic premium). After the UAE’s exit, the spread was only about $6.57, indicating a far smaller panic reaction than during the geopolitical crisis.

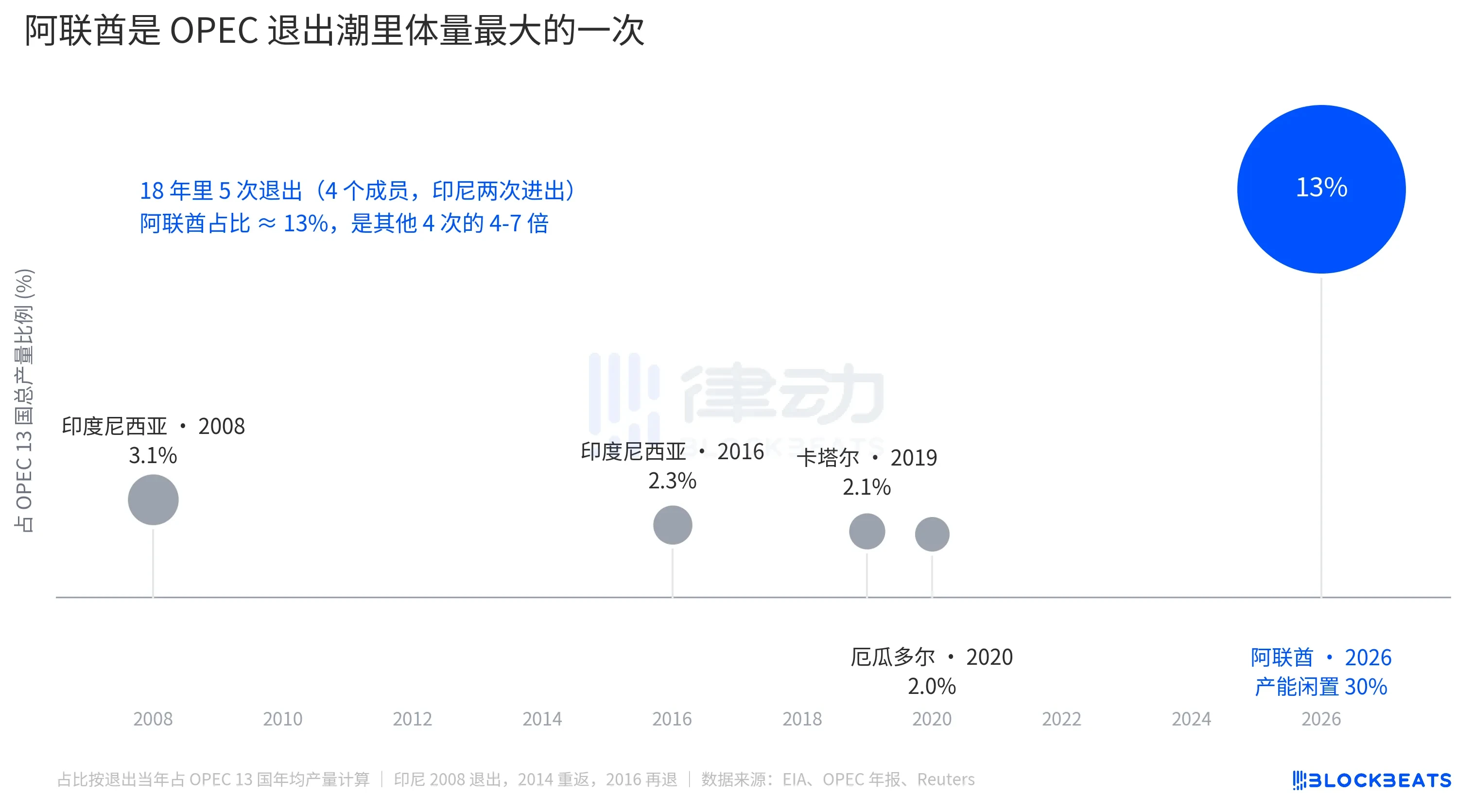

- The UAE accounts for about 13% of OPEC’s total output, more than 1.5 times the cumulative volume of all member countries that left in the past 18 years. However, Saudi Arabia still has 25% idle capacity to offset the impact.

- After the UAE’s exit, OPEC’s 13 members’ idle capacity will shrink to about 1 mb/d, covering only 1% of global demand. This raises fears that its price-adjustment capability will be further weakened.

On April 28, the United Arab Emirates announced its withdrawal from OPEC and OPEC+, effective May 1, ending nearly 60 years of membership. On the same day, Brent crude futures for June jumped $1.11 to $109.34 per barrel. This is the story being told across financial media. But Brent futures for July rose only $1.08 to $102.77, $6.57 cheaper than the June contract. Placed side by side, these two numbers tell a different story.

The UAE is OPEC's third-largest oil producer, behind only Saudi Arabia and Iraq. Its position within OPEC has always been awkward, with its capacity expansion outpacing quota updates. In 2023, dissatisfied with what it considered excessively low quotas, it dragged out the entire OPEC+ production agreement for months. This time, walking away is widely interpreted by media as the biggest challenge yet to Saudi Arabia's leadership.

Following the UAE's announcement, market judgment on oil prices split into two tracks: spot prices jumped, while far-month futures barely moved. The gap between these two pricing tracks is the market's true response to the UAE's withdrawal.

Actual Capacity is 1.5 Times the OPEC Quota

According to EIA data, the UAE's current actual production capacity is 4.85 mb/d (million barrels per day), but the OPEC+ quota for 2025 has recently been pinned at around 3.22 mb/d. The difference of 1.63 mb/d means roughly 30% of its capacity is artificially idled.

The same gap for Saudi Arabia is about 25% (actual capacity of 12 mb/d against a quota of 9 mb/d), and for Iraq and Kuwait, it's only 10-15%. Among OPEC's 13 members, the UAE is the most constrained.

There is another layer to the frustration. The UAE's national oil company, ADNOC, is accelerating its investments. According to ADNOC announcements, its capital expenditure budget for 2023-2027 is $150 billion, and the 5.0 mb/d capacity target has been brought forward from 2030 to 2027. On one hand, it's spending money to expand capacity; on the other, OPEC quotas prevent it from selling more. The daily revenue lost on paper is counted in the millions of barrels.

This is the financial rationale behind the UAE's necessary departure. But looking at this rationale alone, basic economics suggests that a member state with 30% idle capacity, freed from quota constraints, would produce more oil. More oil production means increased supply. Increased supply is bearish for oil prices.

Backwardation in Crude Oil Futures

On April 28, mainstream headlines read "Brent Jumps." But only the near-month contract jumped. The orange dotted line representing far-month expectations remained almost motionless throughout April.

At the close on April 28, Brent futures saw the June contract (front-month, essentially the price for "immediate oil") at $109.34, while the July contract was at $102.77, a spread of $6.57. The futures curve exhibits deep backwardation, with near-term prices pushed higher and far-term prices relatively cheaper.

The futures curve is not speculation; it's the price of real contracts backed by real money. It tells you that the market is willing to pay more for oil now and less for oil in a few months. The underlying logic is simple: the market expects the Hormuz crisis to be resolved, OPEC's supply coordination to loosen, and the UAE's 30% idle capacity to enter the market.

Reconstructing this story across the entire month of April makes it clearer. According to EIA Brent Dated spot data, the spot price surged to $138.21/barrel on April 7, the monthly peak, a full $35 higher than the April 28 far-month expectation of $102.77. This $35 is the panic premium the market is willing to pay for "getting oil immediately." At that time, the US-Iran conflict had entered its ninth week, the Strait of Hormuz passage was nearly completely blocked, and the daily transport of roughly 20 million barrels of Middle Eastern crude was crushed to near zero.

Then, on April 17, ceasefire signals emerged. Brent spot fell to $98.63 that day, dropping about $4 below far-month expectations. The market briefly believed the conflict would end, so "future oil prices" became more expensive than "current oil prices." This anomalous state lasted only a few days. On April 21, Brent hit a monthly low of $96.32, before rebounding on April 23.

On April 28, the UAE announced its withdrawal. Brent for June rose another $1.11 to $109.34, returning to $6.57 above far-month expectations. But this is merely a fraction of the panic premium seen in early April. In other words, the market's panicked reaction to the "UAE withdrawal" was far smaller than its reaction to the Hormuz crisis.

The far-month line speaks more directly. On the day of the UAE's announcement, the July futures contract rose only $1.08 to $102.77, almost identical to the June contract's increase. This implies the market sees the UAE's withdrawal as having a near-zero impact on medium-term oil prices—neither bullish nor bearish. The short-term jump is headline noise layered on top of Hormuz psychology.

The Largest Exit in the Wave of OPEC Departures

Indonesia left for the first time in 2008 (returned in 2014, left again in 2016), Qatar exited in 2019 to focus on LNG, and Ecuador left in 2020 due to fiscal pressure. In these four previous exits, the departing members each accounted for 2-3.1% of total OPEC production. Each was interpreted as an isolated event, and each time, OPEC's market share was not significantly damaged.

The UAE's share is 13%. A single exit here is more than 1.5 times the cumulative share of all exits over the past 18 years.

But for oil price determination, a large size doesn't necessarily mean a large impact. The 13% figure needs to be absorbed within the framework of OPEC discipline led by Saudi Arabia. Saudi Arabia still has about 25% idle capacity to release as a counterbalance, and the production quotas of other OPEC+ members can also be adjusted. The market has not translated "OPEC losing 13% of its volume" into "significant future oil price increases."

The real structural impact lies on another level: OPEC's function as a "price regulator" is further weakened. According to IEA estimates, the total idle capacity of OPEC+ at the beginning of 2026 was about 4-5 mb/d, with the UAE contributing roughly 0.85 mb/d. After the UAE leaves, the idle capacity of the remaining 13 OPEC members will shrink to around 1 mb/d. This is the "ammunition" the market can draw upon when facing future supply shocks—1 mb/d is only enough to cover about 1% of global demand.

So, far-month futures rose by $1. Not because the UAE pumping a few more barrels will cause oil prices to fall, but because OPEC's ability to act as a price stability anchor has been further eroded.

Mainstream reports layer the UAE's exit into the Hormuz rally, making it appear as though OPEC's disintegration is pushing oil prices higher. The futures curve separates the two events. In early April, Brent spot was once $35 more expensive than far-month futures—that was the Hormuz panic premium. On April 28, the near-far month spread was only $6.57 — this is the combined effect of the UAE withdrawal and headline noise. The market's true pricing of the UAE event lies hidden in that nearly unmoved far-month line.