10 Truths About Prediction Markets: Only 3.14% of Polymarket's 1.72 Million Addresses Are "True Winners"

- Core Insight: The "wisdom of the crowd" narrative surrounding prediction markets (such as Polymarket) has been challenged: Only about 3.14% of "skill-based winner" accounts determine the effectiveness of price discovery, while over 67% of participants are in a losing position, essentially subsidizing a minority with an information advantage.

- Key Findings:

- A Minority Drives Prices: Only 3.14% of accounts (approximately 54,000) are identified as "skill-based winners." They are the primary drivers of price discovery and steering events toward their final outcomes.

- The Majority Loses Money: Over 67% of participants (both lucky losers and unskilled losers) bear all the losses. Their trading activity is non-contributory to price discovery, effectively making them "philanthropists."

- High Effectiveness of Skill: The identification effectiveness of skilled players in prediction markets (44%) far exceeds that of traditional fund managers (10%), indicating a clear divergence between experts and "amateurs" in this market.

- Limited Impact of Insider Trading: An estimated 1,950 suspected insider trading accounts show high accuracy for specific event predictions, but their overall contribution to market-wide price discovery is not significant.

- Extremely Uneven Trading Distribution: The median active account trading volume on Polymarket is just $72, while the top 1% of accounts have an average trading volume of $74,000 – a disparity of over 1,000 times.

Source: Prediction Market Accuracy: Crowd Wisdom or Informed Minority?

Compiled by: Odaily (@OdailyChina)

Translator: Wenser (@wenser2010)

Editor's Note: For a long time, prediction market platforms like Polymarket and Kalshi have defined themselves as "the embodiment of collective wisdom" to distinguish themselves from gambling platforms and boost their valuations through this narrative. However, a recent paper from the London Business School and Yale University, analyzing Polymarket's on-chain data, found that less than 4% of addresses drive price changes and achieve significant profits, while the remaining ~97% of addresses are mostly "also-rans," with over 67% incurring losses. Considering that Polymarket's user addresses now exceed 2.43 million, the research data may have some lag, but the underlying phenomenon it reveals is still worth pondering.

Below is a summary of the core content of this paper, compiled by Odaily.

Truth 1: Prediction Market Accuracy Has Nothing to Do with "Crowd Wisdom," But Is Determined by 3.14% of the Minority

This is the most central conclusion of the entire paper and a direct challenge to the industry narrative.

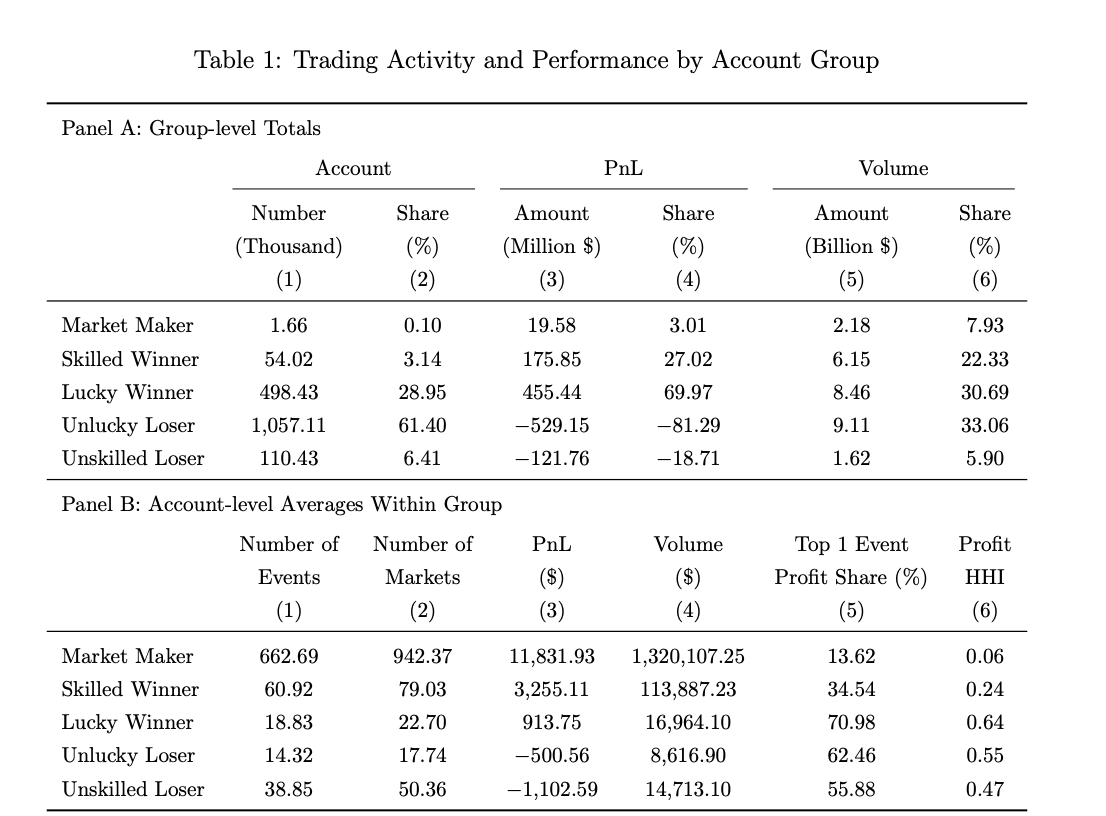

Previously, several prominent industry figures took pride in this. Kalshi CEO Tarek Mansour said prediction markets "harness the wisdom of crowds," Polymarket CEO Shayne Coplan repeatedly claimed that "financial stakes can aggregate information more effectively than experts," and Robinhood CEO Vlad Tenev called it "capitalism's pursuit of truth." But the research data tells us: out of 1.72 million Polymarket accounts, only about 54,000 accounts (3.14%) were identified as "skilled winners" (Odaily Note: In the paper, this group is defined as professional players who can both predict and absorb information on average and react efficiently when news emerges).

The primary driver of price discovery in prediction markets is this minority, not the masses often hidden behind the veil of "crowd wisdom."

Truth 2: Making or Losing Money Can Be a Matter of Luck; 67% of Participants Are Essentially "Charitable Donors"

In this paper, Roberto Gómez-Cram and others used a sign-randomization statistical method to classify all traders' accounts into four categories: Skilled Winners (3.14%), Lucky Winners (29.0%), Lucky Losers (61.4%), and Unskilled Losers (6.4%).

The most counterintuitive number is that Lucky Winners account for nearly 30% of the users. They made money, but their trades contributed nothing to price discovery, statistically indistinguishable from flipping a coin.

In other words, making money in a prediction market is different from being "good at predicting the future." The ~67% of losers bear all the losses, effectively subsidizing the informational advantage of a few.

Truth 3: Among Top Profit Leaders, 88% Make Money Through Luck

Of the top 54,000 traders on Polymarket ranked by actual profit, only 12% were simultaneously identified as "skilled winners" by the statistical method.

This means that the vast majority of the big winners on the leaderboards achieved their large profits through luck, landing one or two big gambles.

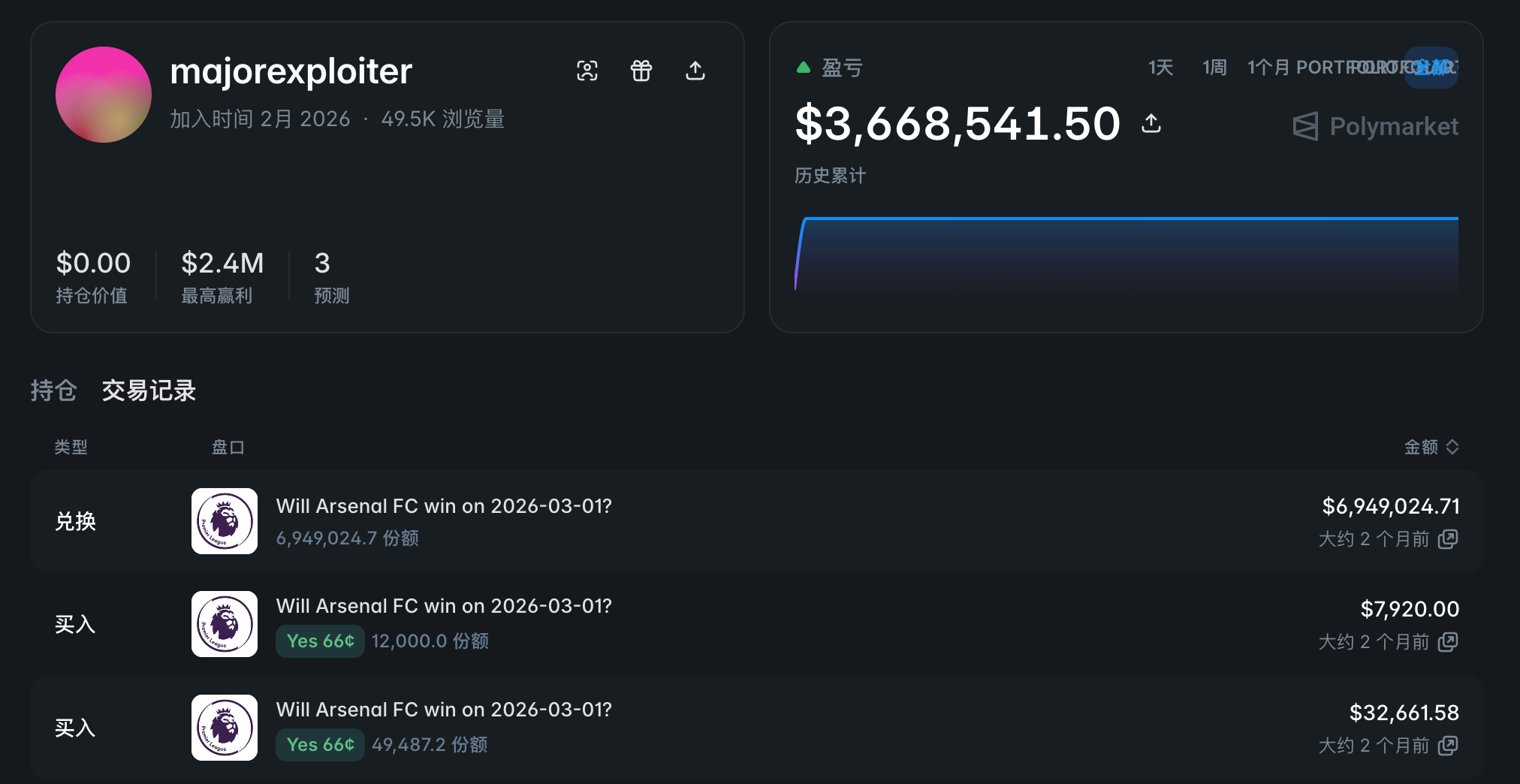

A typical case is the account @majorexploiter – over a weekend in early 2026, the account invested $4.5 million in three sports events, earning over $3.6 million in profit.

The returns from such concentrated bets are highly unsustainable; 60% of "lucky winners" became losers in out-of-sample validation.

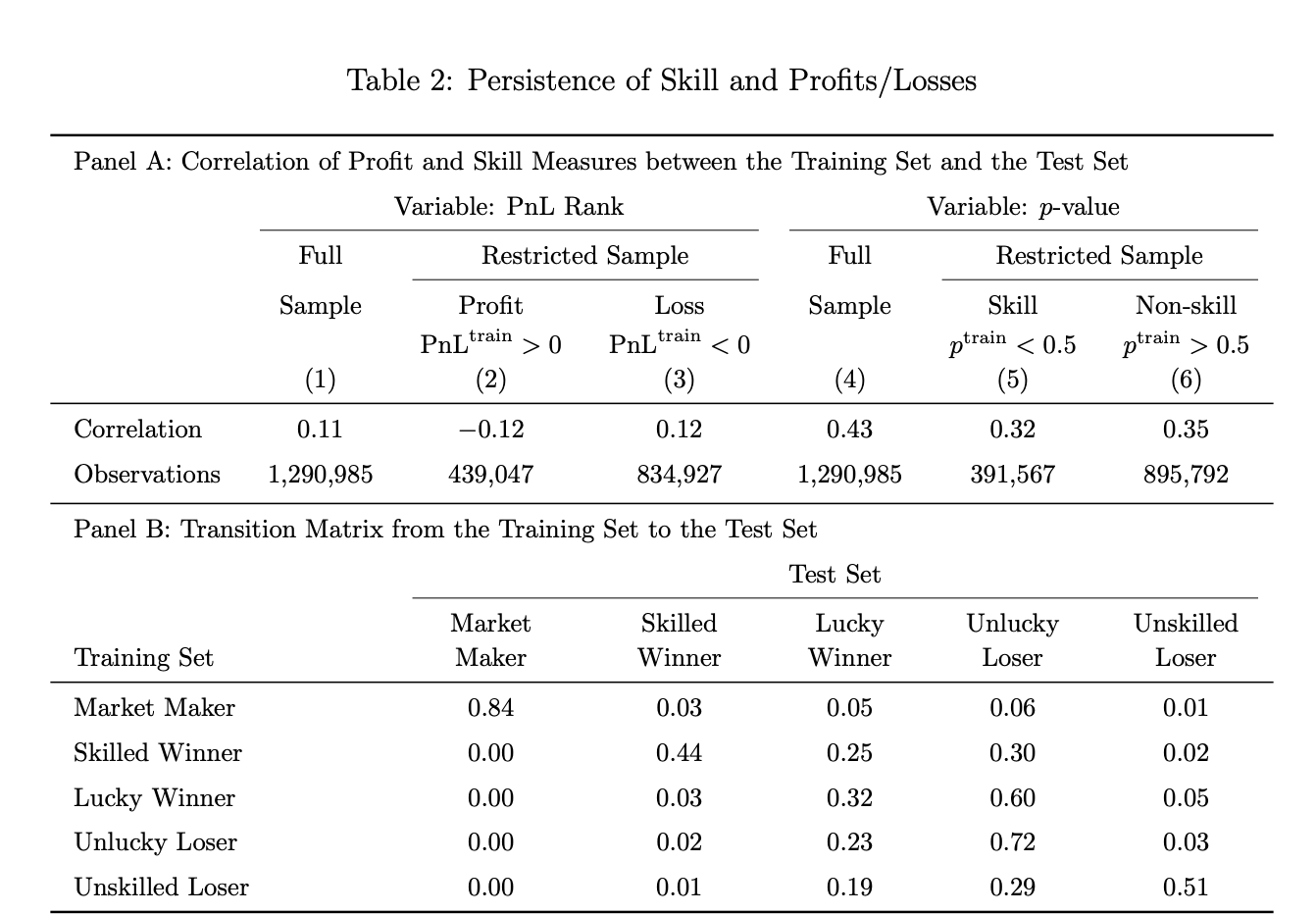

Truth 4: Skill Persistence in Prediction Markets Far Exceeds That in the Traditional Fund Industry

The researchers randomly divided betting events into training and test sets for out-of-sample validation.

Results showed that 44% of accounts identified as "skilled players" in the training set were still identified as "skilled users" in the test set. In comparison, when the same test was applied to actively managed mutual funds in the US, skill persistence was only 10%.

Conversely, "anti-skill" (consistent losses) also showed high persistence: 51% of "unskilled losers" in the training set remained losers in the test set, compared to 20% for US mutual funds.

The final conclusion is that in prediction markets, the true experts are genuine experts, and the "lemmings" are genuine lemmings.

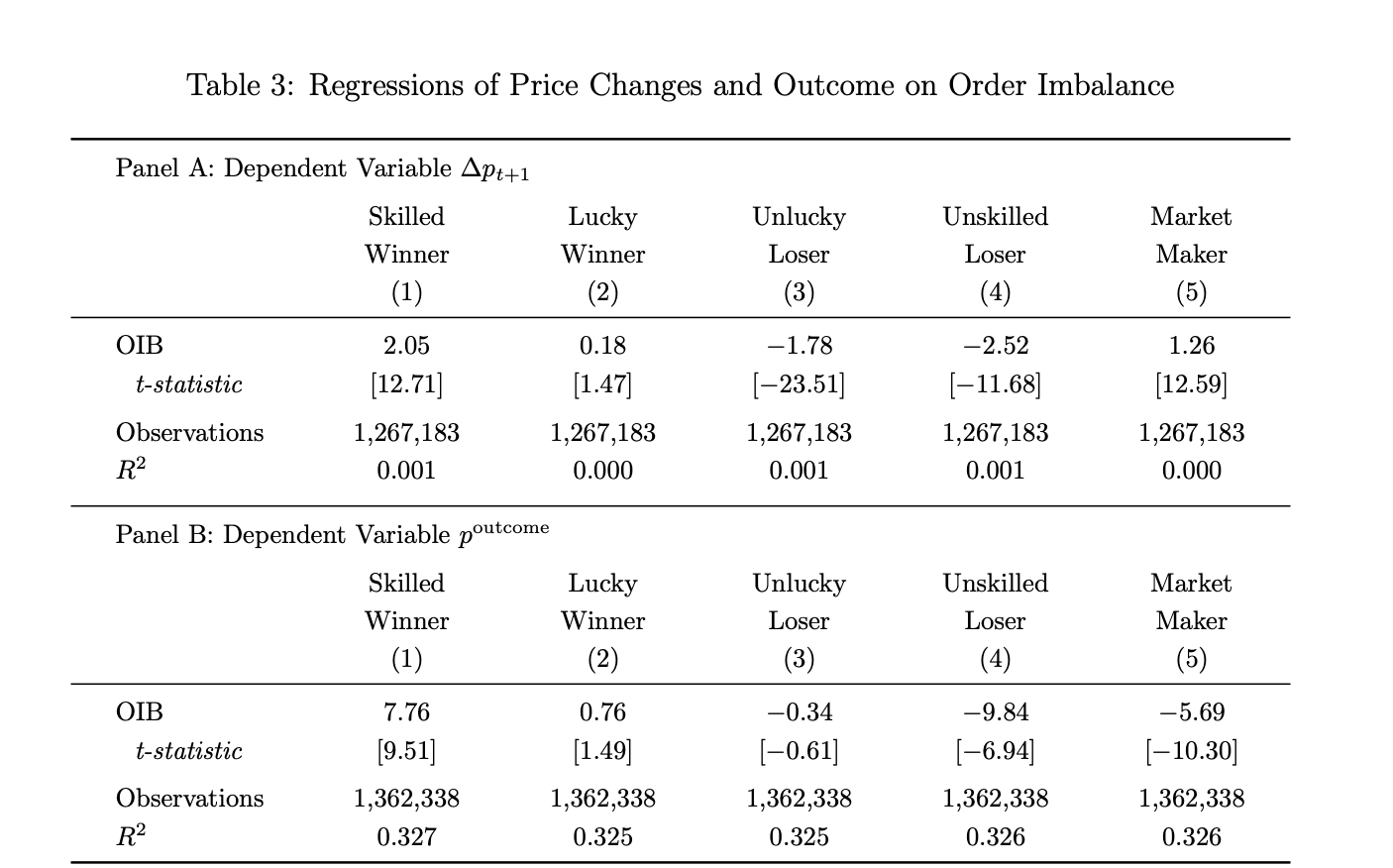

Truth 5: Skilled Winners' Orders Are Highly Correlated with Final Outcomes

Using a constructed order imbalance formula, researchers found that for skilled winners, a 1% increase in their net buying indicator (OIB) was associated with the next period's price rising by about 2 basis points and the final event occurrence probability increasing by about 8 basis points, with very high statistical significance (t-statistics of 12.71 and 9.51, respectively).

In contrast, the order flow of lucky winners was insignificant for both measures (t-statistics of only 1.47 and 1.49).

In other words, although lucky winners have positive profits, their trading operations contain no informational content – this conclusion is very robust from a data perspective.

The study shows that in markets that resolved to "Yes," skilled winners were net buyers; in markets resolving to "No," they were net sellers. They consistently build positions in the direction of the final outcome. Market makers were mostly net sellers in "Yes" markets and net buyers in "No" markets, consistent with their role of accommodating directional order flow and earning bid-ask spreads rather than building positions based on inside information.

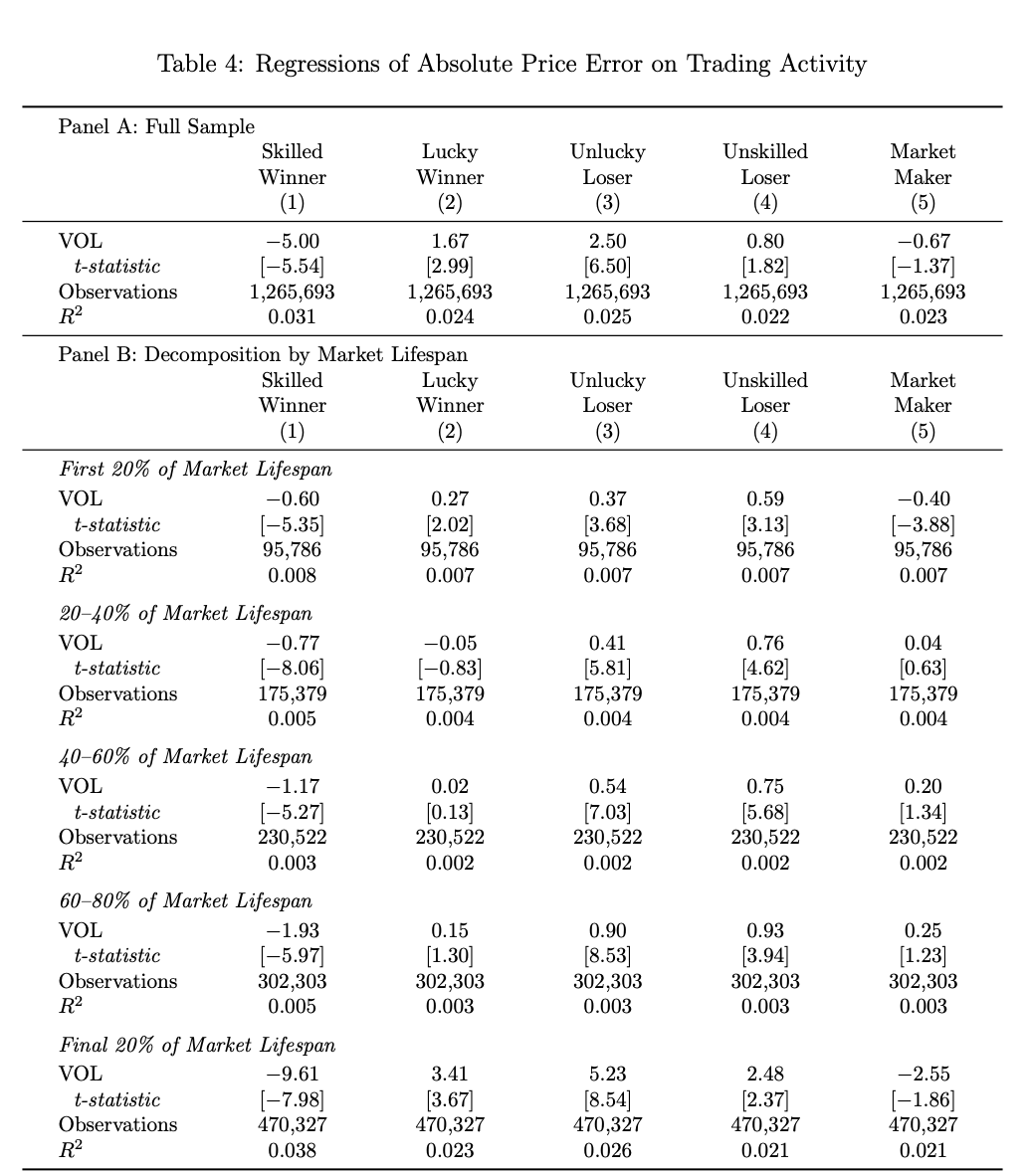

Truth 6: Skilled Traders Are the Only Group That Makes Prices More Accurate

Based on the premise that some trades actually push prices towards the final outcome, the researchers constructed a "price discovery contribution metric" to measure whether the price moved closer to or further from the final outcome accuracy within each time window.

The results showed that only when the trading volume share of skilled winners increased could the pricing error for that betting event be significantly reduced (coefficient -5.00, t-statistic -5.54).

Conversely, trades by the other three groups – lucky winners, lucky losers, and unskilled losers – actually pushed prices away from the final outcome. In effect, most people just create noise at the trading level, and this impact grows as the market nears its resolution. In the last 20% of a betting event's lifecycle, the contribution coefficient for skilled winners expanded to -9.61.

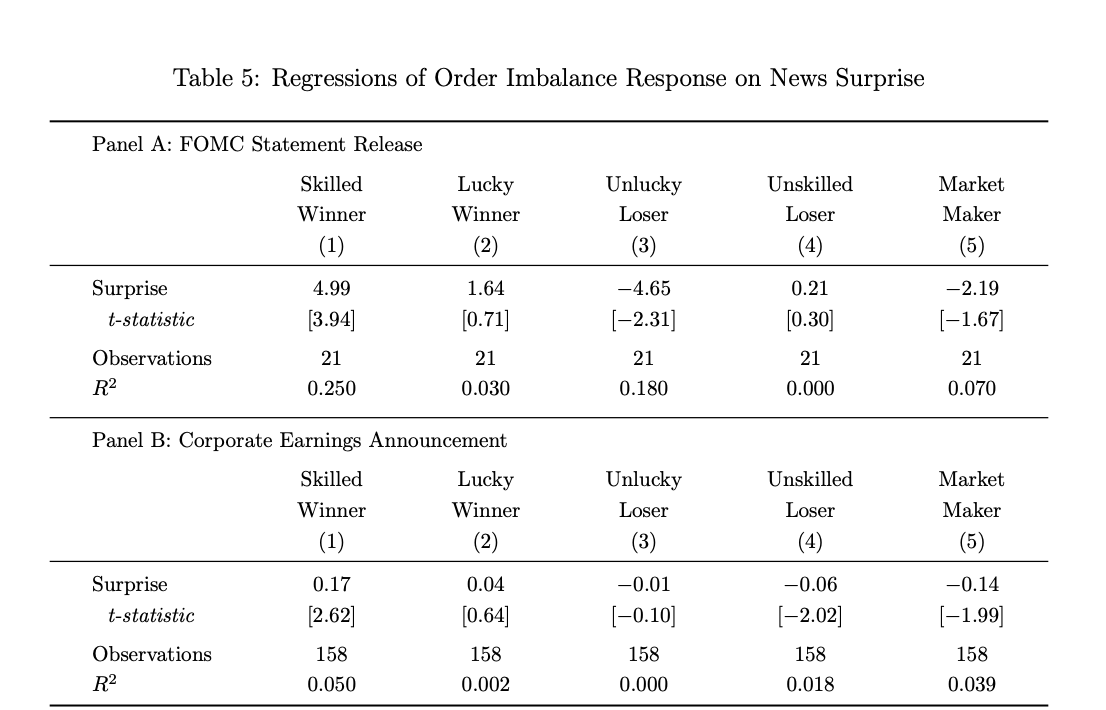

Truth 7: Skilled Winners Are the Only "News Trading" Players

To minimize errors from news transmission time, the researchers selected events with clearly defined information release times, such as FOMC interest rate decisions and corporate earnings announcements (Odaily Note: The former is core for monetary policy expectations; the latter is core for understanding company fundamentals).

The research data shows that only the order flow of skilled winners significantly shifted in the "unexpected direction" during the short-term window following the news release.

For FOMC betting events, a 1% increase in the unexpected component was associated with an approximate 5% increase in the net buying volume of skilled winners (t=3.94). For earnings announcements, a 1% increase in the unexpected component was associated with an approximate 17-basis-point increase in their net buying volume (t=2.62). In contrast, all other groups showed no coherent reaction to the news, and some even traded in the opposite direction.

Truth 8: Market Maker Profits Come from Liquidity Spreads, Not Information Asymmetry

The research data shows that market makers on Polymarket account for only 0.1% of total accounts (about 1,660), but they participate in an average of 942 betting markets, with each account averaging a profit of $11,832.

Furthermore, their order flow can predict price movements in the short term (as they are continuously "taking the other side"), but their predictive impact on the final event outcome is negative (Figure 3 data: coefficient -5.69, t=-10.30).

This means that while they take the sell orders of insider traders in the short term, over the long term, they get "outpaced" by insiders, primarily earning through bid-ask spreads rather than directional bets.

Truth 9: Insider Trading Only Impacts the Outcome of a Minority of Events

Acknowledging the near-inevitability of insider trading in prediction markets, the study also conducted data analysis on its impact on price discovery (Odaily Note: The study used two main criteria to flag suspicious trades. First, timing: accounts opened shortly before specific events, e.g., 7 days, and stopped trading after the event settlement. Second, conviction: accounts concentrated activity on single event contracts and held unusually large positions, with trading volume at least $1,000 and profit at least $1,000. Accounts meeting both conditions were classified as potential insider traders).

The paper identified approximately 1,950 potential insider trading accounts using the dimensions of "account time characteristics + position concentration." These addresses earned an average profit of $15,000 per person.

Notably, the orders from these accounts showed extremely high predictive accuracy for the prices and outcomes of some events (final outcome prediction coefficient 94.63, which is 12 times that of skilled winners). However, this activity was concentrated on a few events and did not significantly contribute to overall price discovery in the prediction market.

Interestingly, the study detailed the case of the "US Raid on Maduro" prediction market: three accounts placed bets in the days before the operation, heavily buying an event with only a 10% probability, ultimately pocketing over $630,000 in combined profits. One of these account holders was later charged by the CFTC as an active-duty US military member. For more details, read "Over 4 months, Polymarket helped Trump catch the military operation leaker, but the price