Will the Fed Still Cut Rates? Tonight's Data Is Crucial

- Core View: Against the backdrop of geopolitical conflicts and rebounding inflation, market views on the Fed's rate cut path diverge significantly. Citi believes the geopolitical shock is temporary and the direction for cuts remains unchanged; while Deutsche Bank argues policy has reached neutrality, and the Fed may maintain high rates indefinitely. The upcoming March retail sales "control group" data is a key validation point.

- Key Elements:

- Citi believes the impact of the Strait of Hormuz situation on oil supply is temporary, and oil prices have retreated from highs, creating conditions for the Fed to return to a rate-cutting path.

- Citi emphasizes that the "control group" (excluding gas stations, etc.) within the March retail sales data is key. If this data weakens, it will prove that high oil prices are eroding other consumer demand, thereby supporting the logic for rate cuts.

- Deutsche Bank points out that the process of US inflation reduction has stalled, and tracking Fed officials' speeches reveals that figures like Waller have turned hawkish, with most officials believing the current policy stance is "very appropriate."

- Deutsche Bank data shows a dramatic shift in market pricing, which now expects "zero rate cuts" for the entirety of 2026. Under the baseline scenario, rates could remain at 3.63% throughout 2026-2028.

- The Fed's March meeting minutes show that most officials believe the process of inflation returning to the 2% target will be delayed, with some officials even discussing adding "two-way risk" language to the statement hinting at the possibility of rate hikes.

Original Author: Dong Jing

Original Source: Wall Street News

Amid the dual pressures of geopolitical conflict and rebounding inflation, market expectations for Federal Reserve interest rate cuts are experiencing intense volatility. The core of the current market debate is: will elevated energy prices trigger persistent inflation, or will they backfire on consumer demand, thereby forcing the Fed to cut rates?

On April 21st, according to Zhui Feng Trading Desk, Citi provided clear bullish reasoning for rate cuts in its latest research report, arguing that oil supply disruptions are merely temporary disturbances, and the path to rate cuts, though bumpy, has a clear direction. Meanwhile, Deutsche Bank poured cold water on this optimism, warning that Fed policy is already in a neutral position and is expected to maintain current rates indefinitely.

As these two major investment banks clash in their views, the upcoming March retail sales data will become the key litmus test to break the deadlock. This data will not only reveal the true destructive power of high oil prices on core consumption but will also directly determine the Fed's near-term policy path.

Citi: Geopolitical Disturbances Are Temporary, the Broad Direction for Rate Cuts Remains Unchanged

Despite the market's continued influence by geopolitical developments, Citi firmly believes that a path towards lower interest rates and a more dovish Fed policy still exists.

The core logic of this judgment lies in: the impact of the Strait of Hormuz situation on oil supply is increasingly likely to be temporary, not a persistent source of inflation. On April 18th, news emerged that the Strait of Hormuz would reopen; although this was later questioned, both Treasury yields and oil prices have retreated from their Thursday highs and remained at lower levels—this in itself is the market pricing in a "short-lived shock" scenario.

The report points out that Citi's logic chain is clear: geopolitical conflict is temporary → oil price shock is not persistent → inflationary pressure does not spread → the Fed has the conditions to return to a rate-cutting track.

Furthermore, a series of underlying economic data tracked by Citi shows subtle changes in the macro-financial environment:

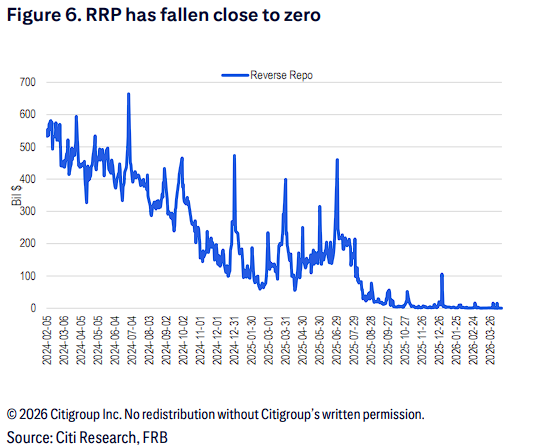

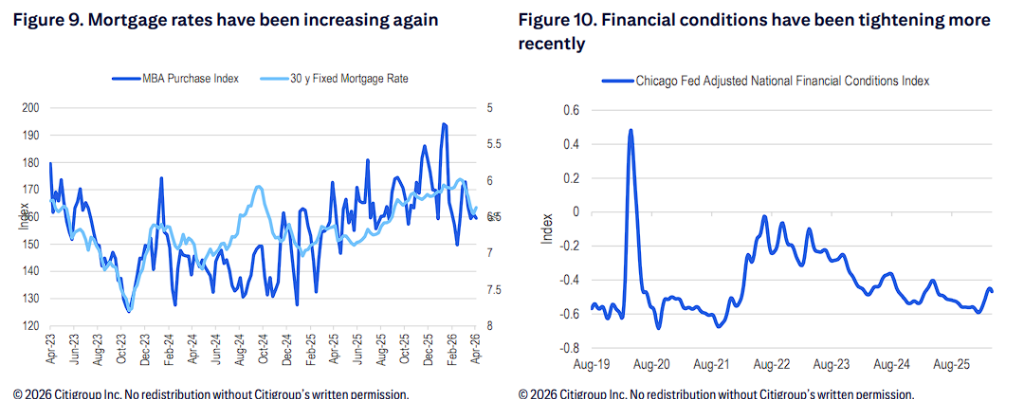

Liquidity and Financial Conditions: The Fed's Reverse Repo (RRP) balance has dropped significantly to near-zero levels; meanwhile, recent financial conditions have been tightening, and mortgage rates are trending upwards again.

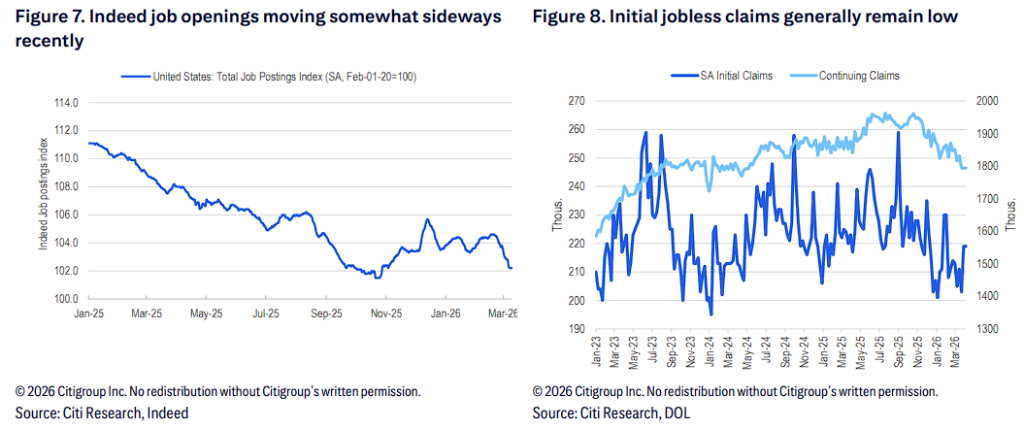

Labor Market: Indeed job vacancy data has recently shown a sideways consolidation trend, although initial jobless claims overall remain at low levels.

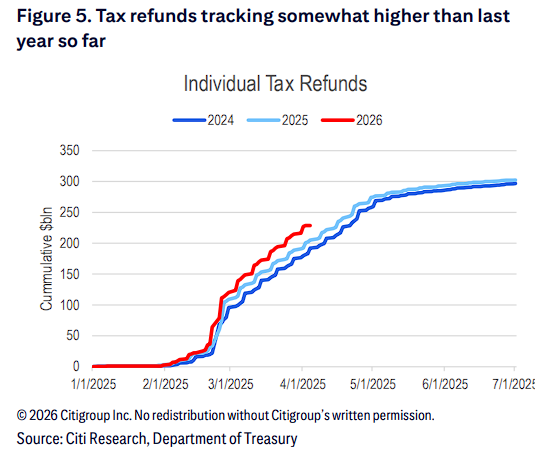

Capital Flows: So far this year, personal tax refunds (cumulative scale in billions of dollars) are overall slightly higher than the same period last year.

Tonight's Litmus Test: Why is the March "Control Group" Retail Sales Data Critical?

As rate cut expectations waver, the upcoming March retail sales data will provide investors with first-hand clues, revealing the extent to which high gasoline prices have cut into consumer spending on other goods categories.

Citi emphasizes that investors must "look beyond the surface" when interpreting this data. Due to rising gasoline prices, nominal retail sales for March are bound to show a sharp increase. However, what truly determines the Fed's policy direction is the "Control group" sales data.

The report points out that this data excludes sales from gas stations and certain specific categories, providing a more genuine and accurate reflection of whether high oil prices have led to weak consumer spending in other areas. If the "Control group" data unexpectedly weakens, it will strongly confirm that high inflation is backfiring on demand, thereby providing crucial data support for the Fed's rate-cutting logic.

Deutsche Bank's Cold Water: Policy Already Neutral, Fed May Stay on Hold Indefinitely

In stark contrast to Citi's optimistic expectations, Deutsche Bank offers an extremely cautious judgment on the rate cut outlook. Deutsche Bank clearly states in its report: the Fed is expected to maintain current interest rates indefinitely because current policy is already in a neutral position.

Deutsche Bank's pessimistic outlook is primarily based on the following key points:

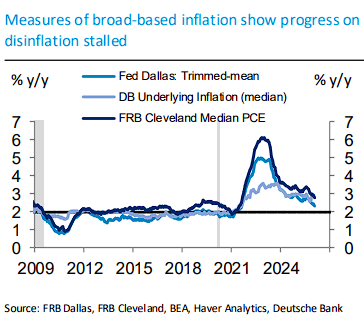

Disinflation Stalling: Broad inflation indicators show that US progress in fighting inflation has stalled.

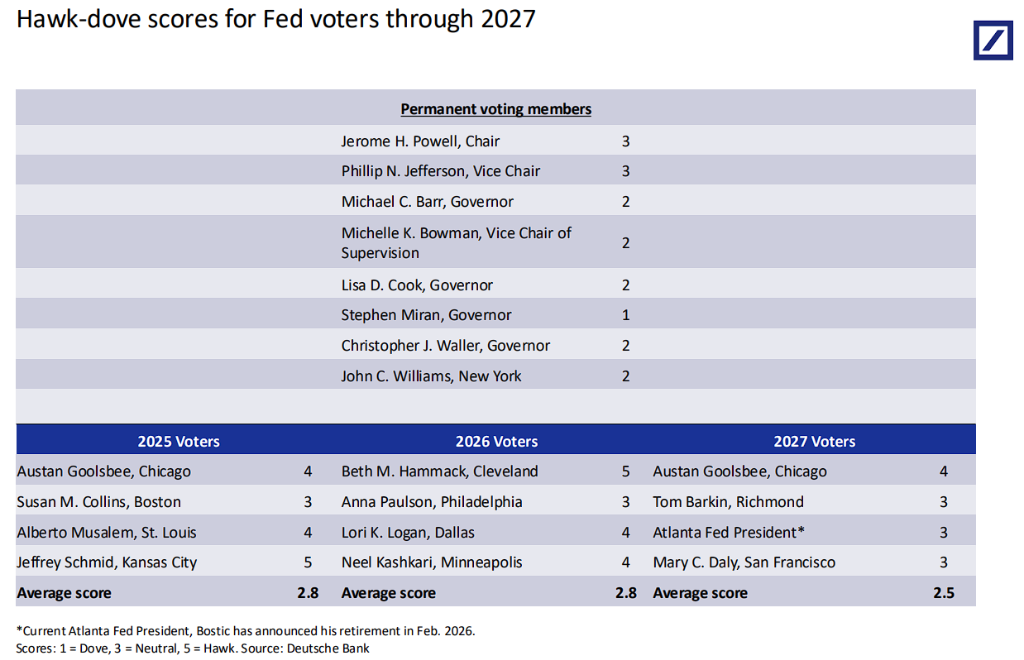

Officials Turning Hawkish: Deutsche Bank's tracking of Fed officials' speeches shows that officials like Waller and Miran have adopted a more hawkish tone, while most others continue to believe the current policy stance is "very appropriate" (well positioned). Details are as follows:

- Waller: Leaning hawkish. He noted that a prolonged Middle East conflict would block the path to rate cuts; a series of shocks (tariffs layered with oil prices) could trigger more persistent inflation increases; he also emphasized that core inflation excluding tariff effects is close to 2%, and the labor market has vulnerabilities;

- Miran: Currently the most dovish voice, supporting 3 or even 4 rate cuts this year, believing the war hasn't changed the inflation outlook 12-18 months out, and the oil price shock is temporary;

- Williams: Believes policy is "exactly where it needs to be," raised 2026 inflation forecast to about 2.75%, lowered 2026 GDP growth forecast to 2%-2.5%;

- Hammack: Clearly stated rates will "remain unchanged for quite some time";

- Goolsbee: Warned that if oil prices persist at $90 per barrel, it could spill over to other prices; further rate cuts in 2026 are unlikely, cuts may need to wait until 2027;

- Daly: Believes current policy is in a "very good place," if the oil price shock lasts until year-end, a market shift to pricing "zero cuts" would not be surprising.

The Fed's March meeting minutes also showed that the vast majority of officials believe the process of returning inflation to the 2% target will be delayed; some officials even discussed the necessity of adding "two-way risk" language to the meeting statement, hinting that the possibility of rate hikes is not entirely off the table.

Deutsche Bank's hawk-dove scoring for Fed officials shows the 2026 voting committee has an average score of 2.8 (1 being most dovish, 5 being most hawkish), overall leaning neutral-slightly dovish, but dovish voices are clearly in the minority.

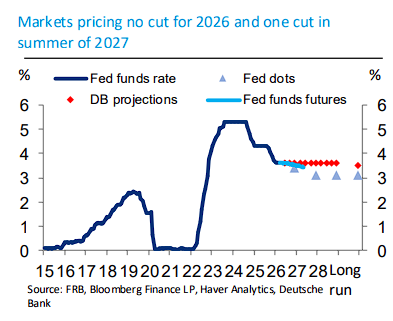

Market Pricing Completely Reversed: Faced with persistent inflation pressure and strong economic resilience, market expectations have undergone a dramatic shift. According to Deutsche Bank data, current market pricing expects "zero cuts" for the entirety of 2026, with the first cut not until the summer of 2027.

Deutsche Bank expects that under the baseline scenario, the federal funds rate will remain at 3.63% throughout 2026-2028, with no rate cuts for the entire year.