Has the Global Central Bank "Gold Hoarding Era" Ended?

- Core View: A UBS report suggests the likelihood of a structural shift and large-scale gold selling by global central banks is extremely low. Official sectors are expected to maintain a net buying stance, albeit with a moderate slowdown in the pace of purchases. While gold prices face short-term volatility due to geopolitical and traditional macroeconomic factors, the medium-term logic still points to new highs.

- Key Elements:

- UBS forecasts global central bank gold purchases in 2026 to be around 800-850 tons, slightly lower than 2025 levels, representing a "slowing down" rather than a trend reversal.

- The report clarifies that the case of Turkey "selling 50 tons" involved data confusion (including commercial bank positions and swap operations) and should not be simplistically equated with central bank selling.

- Central bank gold holdings are characterized by long-term and strategic behavior, with approximately 62% of institutions adopting a buy-and-hold strategy, and only about 4.5% engaging in short-term tactical adjustments.

- Gold prices are suppressed in the short term by traditional frameworks such as a stronger US dollar and rising US real interest rates, while also experiencing volatility due to geopolitical news.

- UBS has lowered its 2026 average annual gold price forecast to $5,000 but maintains its year-end target price of $5,600, viewing any pullback as a strategic accumulation window.

Original Author: Zhao Ying

Original Source: Wall Street News

The hottest question in the market recently is: Are global central banks selling gold? Has this 15-year-long official "gold accumulation wave" come to an end?

According to the Wind Trading Desk, UBS strategist Joni Teves gave a clear judgment in the latest precious metals research report released on April 2: The possibility of a structural shift by central banks leading to large-scale gold sales is extremely low. Official institutions will maintain a net buying stance, but the pace of purchases will moderately slow down—it is estimated that total gold purchases for 2026 will be about 800 to 850 tons, slightly lower than the approximately 860 tons in 2025.

The report targets the most glaring recent example—the news that Turkey "sold about 50 tons of gold within weeks." Teves believes that Turkey's official gold data is mixed with commercial bank positions, swaps, and other operational traces. Relying solely on headlines to infer that "central banks are starting to sell" carries high risks; one should wait for more detailed breakdown data before making a judgment.

Regarding price levels, UBS defines the short term as having "a lot of noise": the news cycle surrounding geopolitical situations will keep gold prices volatile and consolidating. However, the medium-term logic still points to new highs. UBS has lowered its 2026 average annual gold price forecast to $5,000 (previously $5,200, mainly a book adjustment for Q1) while maintaining its year-end target price of $5,600 (set at the end of January).

Evidence for "Central Bank Gold Sales" as the Main Cause of This Round of Pullback is Not Solid; 800-850 Tons is More Like "Slowing Down"

The scenario the market fears is specific: If the Middle East conflict becomes protracted, oil prices push up inflation, growth weakens, and local currencies depreciate, some central banks might be forced to sell gold to cope with the pressure. The report does not deny that "individual central bank selling" might occur, but it emphasizes that this does not equate to a reversal of the official sector's trend.

A key reminder from the report is: During the past 15 years of continuous gold accumulation by the official sector, single-month "selling" was not uncommon. The reasons could also be practical—central banks that bought cheaply earlier might take some tactical profit-taking outside their core positions; sharp gold price increases trigger rebalancing; "natural inflows" from gold-producing countries turn into outflows at certain points. In other words, selling can be an action, not necessarily a stance.

The baseline judgment is that net buying continues, but at a slower pace. The detail here lies in the trading habits of the official sector: They are more like "physical buyers," often providing support during pullbacks, helping the market stabilize faster at a higher plateau. Conversely, the official sector typically does not chase rallies, preferring to intervene when prices are more suitable and volatility has subsided.

This also explains why when volatility rises, the market suddenly feels "central banks are absent." The observation mentioned in the research is that recently, the official sector and other longer-term holders have been more inclined to wait and see rather than immediately replenish positions on every dip.

The Narrative of Turkey Selling "50 Tons" is Overstated; Short-Term Gold Prices are More Influenced by the Dollar and Real Interest Rates

The Turkish case is sensitive because it appears to fit the narrative of "central banks starting to sell gold." However, Turkey has certain particularities: Some changes might be swaps rather than direct sales; more importantly, the Turkish central bank has long used gold as a policy tool to support liquidity management within the domestic banking system.

Part of the total gold disclosed by the Turkish central bank corresponds to commercial bank positions. Coupled with policies since 2017 that allow banks and other entities to use gold more within the financial system, "changes in total data" do not equal "central banks selling in the market." The report's advice is clear: Wait for more detailed data that can break down the metrics before discussing trends.

The trading environment in March had "dual uncertainties": On one hand, when Iran-related news developed, gold prices were already seeking a new stable range after sharp rises and falls in January-February. On the other hand, the impact of the Middle East conflict on macroeconomics and asset pricing is nonlinear, making long-term capital reluctant to place bets easily.

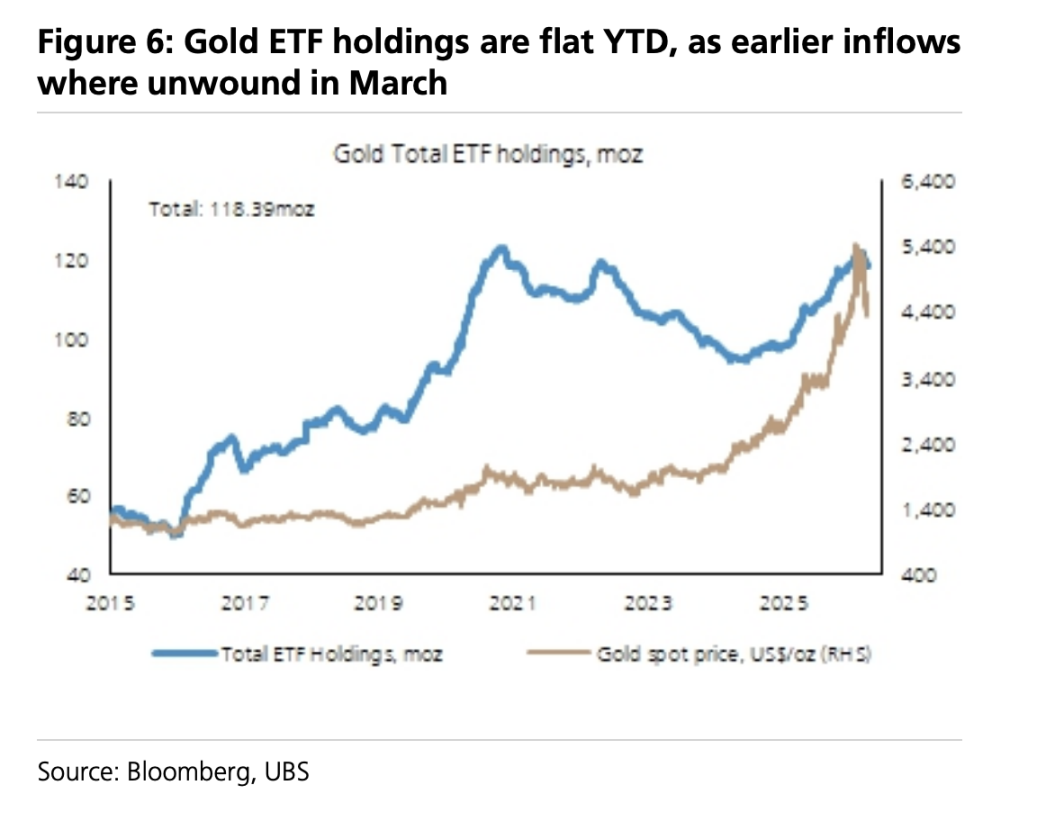

When strategic funds that "buy the dip" are absent, short-term gold prices are more likely to revert to the traditional framework: A stronger US dollar and rising US real interest rates put pressure on gold prices; long positions are further squeezed out, and even some short-selling forces emerge. Additionally, Chinese demand provided support during this phase of decline. After stabilizing around $4,500, gold prices fluctuated near the $4,700 level.

The Underlying Logic of Central Bank Gold Holdings: Buy and Don't Sell

The World Bank's "Fifth Biennial Reserve Management Survey Report (2025)" explains a more fundamental question: How do central banks actually think about gold? The survey covers holdings up to December 2024, with participation from 136 institutions being the highest ever, and includes a dedicated gold chapter for the first time.

A few numbers can clarify the behavioral boundaries of central banks: About 47% of central banks determine their gold holdings based on "historical legacy," about 26% based on qualitative judgment; only about a quarter incorporate gold into a formal strategic asset allocation framework.

More crucially, only about 4.5% make short-term tactical adjustments to gold reserves, and the dominant investment style for gold is buy-and-hold (about 62%). This profile means that even if the buying pace slows, the official sector does not resemble a group of traders driven by news headlines and frequently flipping positions.

Regarding reasons for increasing holdings, over half cited "diversification" as the primary reason; local gold purchase programs accounted for about 35%, geopolitical risks about 32%; only about 6% cited "liquidity needs" as a reason. The official sector's rationale for holding gold has not been invalidated by recent volatility.

Short-Term Volatility is Inevitable, but "Unfinished New Highs" Remains the Main Theme

Returning to the trading level, gold's path is not a straight line upward: The next few weeks may continue to see consolidation and bumpy movements as the market constantly reassesses geopolitical risks. However, the report believes that the two long-term drivers pushing capital allocation to gold—the combined risks of growth and inflation, and the persistence of geopolitical tensions—are turning "diversification into gold" into a more common portfolio action.

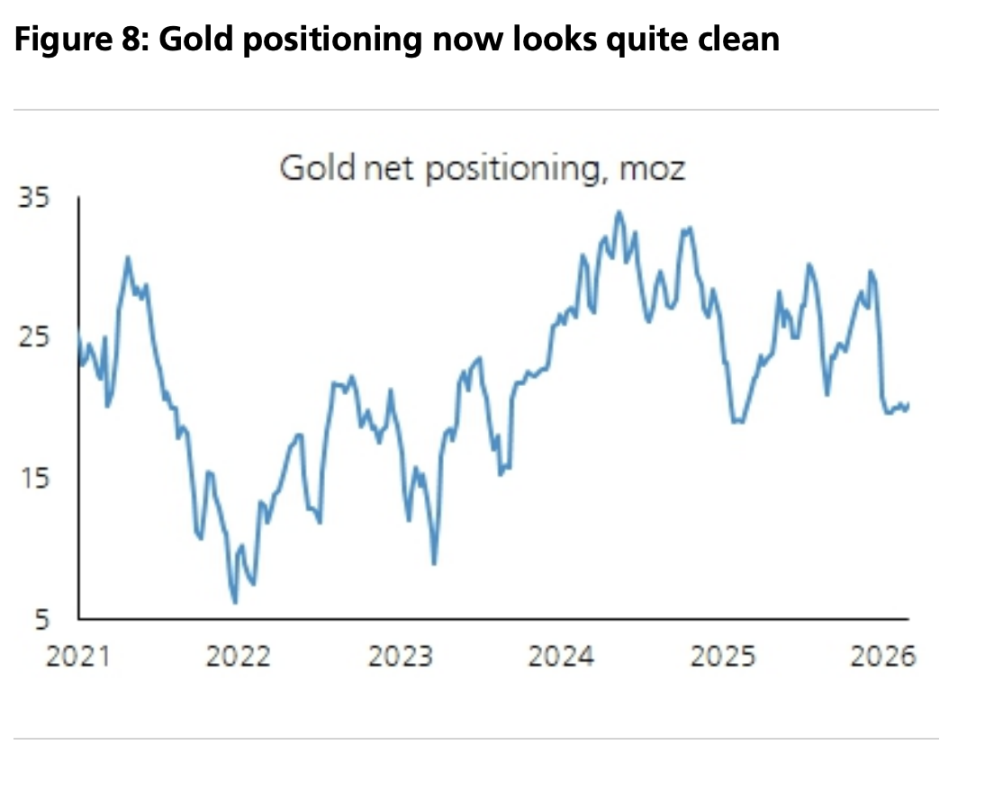

Within this framework, the pricing anchors provided by the report are: an average annual gold price of $5,000 for 2026 and a year-end target of $5,600. It also mentions that speculative positioning is already "cleaner," while long-term participants remain underweight; if another pullback occurs, it would be closer to a "strategic accumulation window" rather than a signal of a trend reversal.