After MSTR, a leading Bitcoin concept stock, first indicated it might "sell its cryptocurrency," its stock price plummeted by as much as 12% during trading.

- 核心观点:MicroStrategy首次暗示可能出售比特币。

- 关键要素:

- 设立14.4亿美元储备金应对市场波动。

- 若mNAV指标跌破1且融资无门,将出售BTC。

- 此举打破其长期“只买不卖”的持有策略。

- 市场影响:引发市场对其商业模式及抛售BTC的担忧。

- 时效性标注:短期影响。

Original author: Long Yue

Original source: Wall Street News

MicroStrategy, the publicly traded company holding the most Bitcoin globally, announced on Monday, December 1, that it had raised $1.44 billion in "dollar reserves" through a stock sale.

This move aims to address the extreme volatility in the cryptocurrency market and provide security for dividend and debt interest payments. Previously, the price of Bitcoin had fallen from a high of over $126,000 in early October to approximately $85,000 in just over a month.

Company executives stated that if its metric "mNAV," which measures the relationship between corporate value and cryptocurrency holdings, falls below 1, and the company is unable to raise funds through other means, it will sell Bitcoin to replenish its dollar reserves. This statement is seen as a major turning point in the company's strategy, breaking with the "buy and hold" philosophy long advocated by its founder, Michael Saylor.

Shares of the company plunged as much as 12.2% on Monday after it first hinted at the possibility of selling Bitcoin, eventually closing down 3.3%. The sell-off reflects deep concerns among investors about the sustainability of its business model during the “Bitcoin winter.”

US Dollar Reserves: Insurance Against the "Bitcoin Winter"

Facing headwinds in the crypto market, MicroStrategy is taking steps to bolster its financial position. According to reports from the Financial Times and other media outlets, the $1.44 billion reserve is funded by proceeds from the sale of shares. The company aims to maintain sufficient dollar reserves to pay "at least 12 months of dividends" and eventually expand them to cover "24 months or longer."

The funds were reportedly raised through the issuance of 8.2 million shares last week, enough to cover the company's total interest expenses for the next 21 months. Currently, MicroStrategy's annual interest and preferred stock dividend expenses are approximately $800 million. This move aims to ensure that the company will not be forced to sell Bitcoin in the short term, even if capital markets lose interest in its stocks and bonds.

In a recent podcast, "What Bitcoin Did," CEO Phong Le admitted that the move was in preparation for a "Bitcoin winter." Founder Michael Saylor stated that the reserve would "allow us to better navigate short-term market volatility."

Has the myth of "never selling" been shattered?

The most significant change in this strategic adjustment is that MicroStrategy has for the first time acknowledged the possibility of selling Bitcoin. This potential sale condition is linked to the company's proprietary "mNAV" metric, which compares the company's enterprise value (market capitalization plus debt minus cash) with the value of its cryptocurrency assets.

CEO Phong Le stated explicitly, "I hope our mNAV won't fall below 1. But if we do reach that point and there are no other funding channels, we will sell Bitcoin."

This statement is significant. Michael Saylor has long presented himself as a staunch evangelist for Bitcoin, transforming MicroStrategy from a small software company into the world's largest corporate Bitcoin holder, with his core strategy being to continuously buy and hold for the long term.

Currently, the company holds approximately 650,000 bitcoins, worth about $56 billion, representing 3.1% of the total global bitcoin supply. Its enterprise value is approximately $67 billion. If mNAV falls below 1, it means that the company's market valuation (excluding debt) is lower than the value of its bitcoin holdings, which would severely undermine the foundation of its business model.

Imminent debt pressure

Behind the establishment of dollar reserves lies the enormous debt pressure MicroStrategy faces. The company has financed its Bitcoin purchases through various means, including issuing stocks, convertible bonds, and preferred stock, and currently carries $8.2 billion in convertible bonds.

If the company's stock price remains depressed, bondholders will likely demand that the company repay the principal in cash rather than convert it into stock, putting significant pressure on the company's cash flow. When S&P Global assigned MicroStrategy a "B-" credit rating on October 27, it specifically highlighted the "liquidity risk" posed by its convertible bonds.

S&P warned: "We believe there is a risk that the company's convertible bonds could mature at the same time as Bitcoin prices face severe pressure, which could lead the company to liquidate its Bitcoin holdings during a period of low prices or to undertake a debt restructuring that we may consider a default."

The specific pressures are already looming. Data shows that bondholders of a $1.01 billion bond can demand repayment of principal from the company on September 15, 2027. In addition, over $5.6 billion in "out-of-the-money" convertible bonds may need to be redeemed in cash in 2028, posing a threat to the company's long-term financial stability.

Traders' interpretation: Is this cautious risk aversion or a "prelude to a sell-off"?

While MicroStrategy's CEO emphasized that Bitcoin would only be sold under extreme conditions, traders have clearly begun to "over-interpret" his remarks in a sensitive market environment.

Despite the company's insistence that its long-term accumulation strategy remains unchanged, traders worried that the latest comments had introduced a potential sell-off path. This concern quickly translated into action, leading to a surge in risk aversion.

The market reaction to CEO Phong Le's statement that "selling Bitcoin is mathematically justifiable when the stock price is below the value of the underlying asset and financing is limited" has been polarized:

Pessimists read an underlying message: many cryptocurrency traders speculate that these seemingly understated comments might be a signal that the world's largest corporate holder is preparing to sell some of its Bitcoin. One user sarcastically commented on social media platform X, "Can't wait to see them dump at the bottom." Another commenter remarked, "Sounds like typical corporate PR rhetoric, but they better not sell at the wrong time."

Rationalists see this as an inevitable move; others argue that CEO Phong Le is simply acknowledging the constraints any publicly traded company faces when its market capitalization falls below its asset value. One investor noted, "The point isn't whether they might sell, but how committed they are to the option before it becomes a reality."

To reassure the market, MicroStrategy subsequently stated on its X platform that even if the price of Bitcoin fell back to the average purchase price of around $74,000, its assets would still cover its outstanding convertible debt several times over; it even claimed that even if the price dropped to $25,000, its asset coverage ratio would still be more than twice its liabilities. Founder Michael Saylor continued to demonstrate confidence, announcing on Monday that the company had purchased another 130 BTC for $11.7 million.

Market reaction and earnings warning

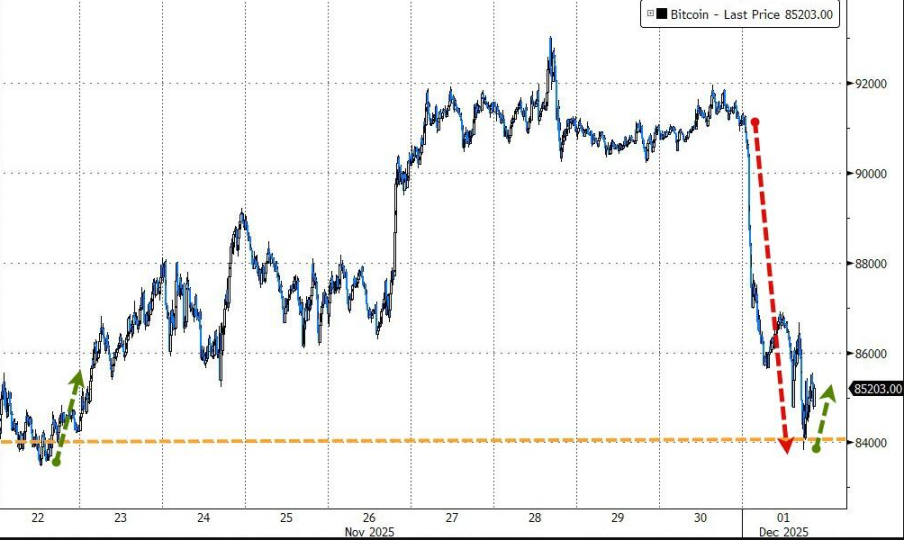

MicroStrategy's latest developments and the resulting concerns about a strategic shift quickly triggered a negative market reaction. On Monday, its stock price hit a low of $156 during the session, and although it recovered somewhat by the close, it was still down 64% from its 52-week high in mid-July. Year-to-date, the stock has fallen nearly 41%. Meanwhile, Bitcoin's price also suffered, falling over 4% to approximately $86,370.

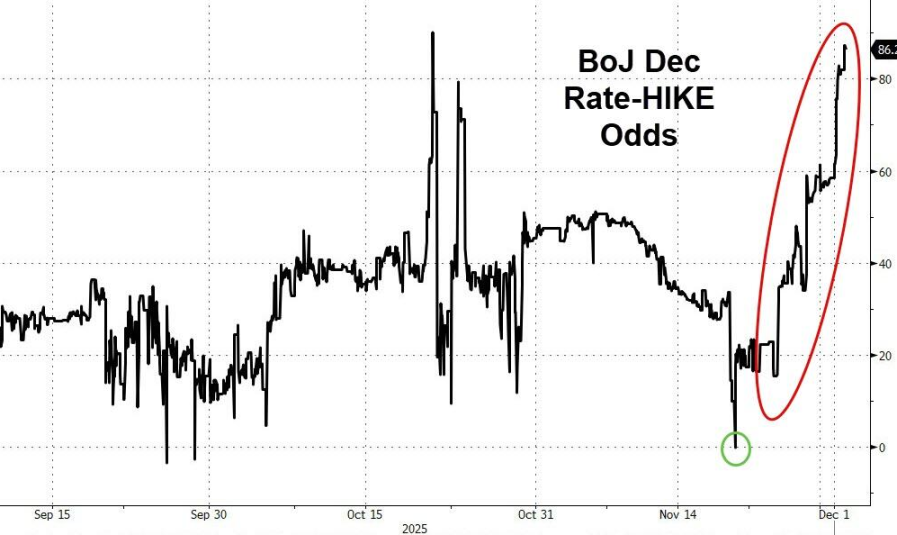

Besides the company's own strategic adjustments, the sharp fluctuations in the macro market also became the "last straw" that broke the camel's back. Monday's market showed a clear risk-averse tone, partly due to the yen funding squeeze caused by the Bank of Japan's hawkish stance, and partly due to the turmoil in the cryptocurrency sector itself.

The relevant charts and data illustrate the current extreme sentiment in the market:

Bitcoin's purchasing power has shrunk: A year ago, one Bitcoin could buy 3,500 ounces of silver; now, the same unit of Bitcoin can only buy 1,450 ounces of silver, the lowest point since October 2023. This sharp drop in the ratio directly reflects the weakness of crypto assets relative to traditional safe-haven assets such as silver.

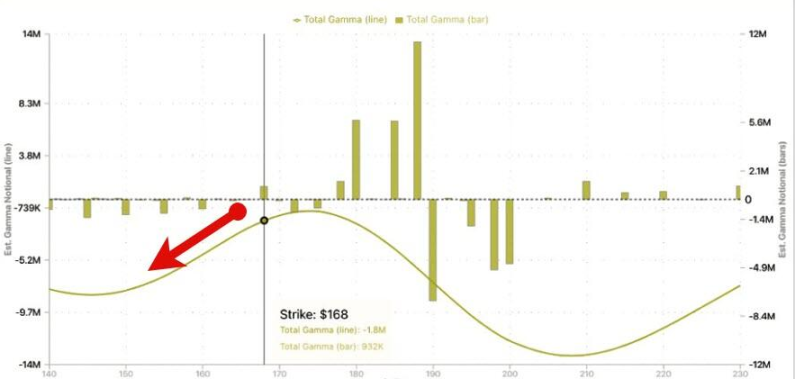

Options Market Sniping: SpotGamma data indicates that MicroStrategy (MSTR) is facing a classic "over-leveraged target under attack" scenario. A large number of long puts are clustered below $170. This negative Gamma effect means that if Bitcoin prices fall further, market makers' hedging activities could accelerate the decline of crypto stocks like MSTR and Coinbase, and even drag down major stock indices.

Macroeconomic headwinds: With rising expectations of a Bank of Japan interest rate hike, carry trades are facing liquidation pressure, and cryptocurrencies, as the most speculative asset class, are bearing the brunt. Bitcoin briefly sought support around $84,000 during the day, experiencing its worst single-day performance since March 3; Ethereum even fell below the $3,000 mark.

In addition to the pressure on its stock price, the company's earnings forecast is also flashing red. MicroStrategy predicts that if the price of Bitcoin closes between $85,000 and $110,000 by the end of this year, the company's full-year results could range from a net loss of $5.5 billion to a net profit of $6.3 billion. This contrasts sharply with the company's forecast of $24 billion in net profit by 2025 in its earnings report released on October 30.