Trivia: The first DApp on Ethereum was a prediction market

- 核心观点:Augur作为以太坊首个ICO项目重启。

- 关键要素:

- 2015年完成以太坊首次ICO。

- 曾因体验差、费用高导致用户流失。

- 新团队将预言机与预测市场分离。

- 市场影响:推动去中心化预测市场发展。

- 时效性标注:中期影响

Original author: Eric, Foresight News

While sorting through Web3 prediction markets recently, I suddenly came across Augur. After some research, I discovered that Augur announced a relaunch in March of this year, but I have no idea when it ceased operations.

This sentiment stems from the fact that Augur was the subject of the first article I translated after entering the industry. The article was published on March 19, 2019. I particularly remember the requirement to add my own interpretation to the translation. I also remember using the poster from the movie "The Butterfly Effect" as the cover for the article published on my WeChat official account, as I personally believe that prediction markets have the power to change the future.

I don’t know if the opinion that suddenly emerged more than six years ago can be regarded as a prophecy, but my view on the reason why the current leading Web3 prediction market is valued at nearly $10 billion remains unchanged: when an event is bound to have a certain outcome in the future, and the game on this outcome is mixed with economic interests, the game itself will have the ability and motivation to change the final outcome.

Ethereum’s first DApp and first ICO

Augur is unrivaled in its early days. Because Ethereum is a permissionless network, it's difficult to verify whether Augur was truly the first DApp on Ethereum. However, some things are certain: development began on the Ethereum testnet while it was still in its infancy. Furthermore, Augur was the first to truly capture the attention of the broader industry, which at the time wasn't even called "Web3," leading to the emergence of numerous ecosystem projects. While Augur officially launched in 2018, it's not an exaggeration to call it "Ethereum's first DApp."

As for Augur being the first successful ICO on Ethereum, this is verifiable. The Economist's 2018 article, "Blockchains could breathe new life into prediction markets," also mentioned the Augur ICO as taking place in 2015, specifically in August 2015.

This timing is somewhat absurdly early: Ethereum's genesis block was born on July 30, 2015, and the ERC-20 standard was not officially proposed until November 2015. That is to say, when Augur initially sold REP tokens, REP did not comply with the ERC-20 standard.

I’ve seen many different versions of which institutional investors participated in Augur’s legendary ICO, including well-known institutions such as Founders Fund, Pantera Capital, Blockchain Capital, 1confirmation, and Multicoin Capital, but I haven’t found an authoritative source of information.

Augur's ICO successfully raised over $5 million. Bitcoin's price in 2015 was only between $300 and $400, and Ethereum's price plummeted to around $0.40 the same month as the Augur ICO. Over eight years ago, in a Reddit discussion titled "What was the first ICO/ERC20 token to run on an Ethereum smart contract?", a user nicknamed x_ETHeREAL_x stated that Ethereum didn't have a wallet or GUI at the time, requiring "transfers" to be made via the command line using the Geth client. This was quickly corrected by a user nicknamed adrianclv, who stated that the Geth client didn't exist at the time, and that the client used was the CPP Ethereum client developed by Gavin Wood, co-founder of Ethereum and later founder of Polkadot.

An application that continues to develop but offers a poor user experience

Nearly three years after the ICO, Augur was officially launched in July 2018.

When Augur officially launched, it offered both a desktop app and a web app. The reason for launching a desktop app was that the number of Ethereum nodes was relatively small at the time, and using the built-in full node application directly would be more efficient. At the time, the Augur ecosystem project Guesser's team described the design of the desktop app:

The Augur App is a lightweight Electron application that bundles the Augur UI and Augur Node, deployed locally on your computer. The Augur UI is a reference client (similar to Geth for Ethereum) for interacting with the core Augur protocol smart contracts on the Ethereum blockchain. The Augur Node is a locally running program that scans the Ethereum blockchain for Augur-related event logs, stores them in a database, and provides the corresponding data to the Augur UI.

While other NFT projects, such as Crypto Kitties and the pure gambling app Fomo3D, emerged during the same period, Augur remained the industry's "hottest kid." Besides implementing a prediction market on-chain, Augur also developed its own decentralized oracle to provide results. This self-developed oracle was officially launched nearly a year before Chainlink's.

According to DappRadar data, Augur's daily active users peaked at 265 upon launch, but by August 8th, this number had dropped to 37, and by the end of the year, it had fewer than 30 daily active users. As of December 11, 2018, Augur had created 1,635 markets, 11,825 orders, and 6,331 completed orders. During the US midterm elections at the end of 2018, the platform saw over 200 orders completed in a single day. These numbers, while seemingly insignificant now, were considered impressive at the time.

In addition, if you understand the implementation mechanism of Augur, you will find it a miracle that there are still dozens of people playing and thousands of orders can be completed.

The Augur experience was deemed terrible not only because the user experience of platforms like MetaMask was inherently poor at the time, but also because Augur's design itself was fatally flawed. First, unlike Polymarket, Augur didn't automatically balance probabilities with an arbitrage mechanism. Instead, it required a one-to-one correspondence between positive and negative trades. In an era without market makers, you had to find someone who shared the exact opposite view.

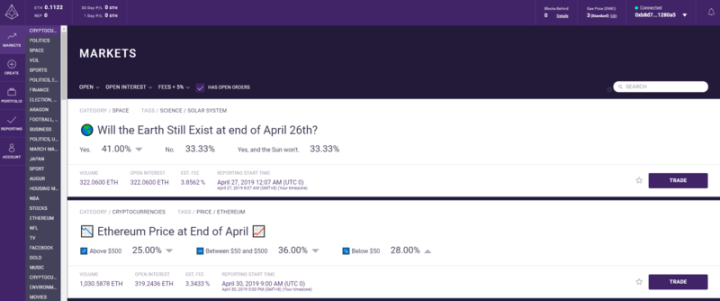

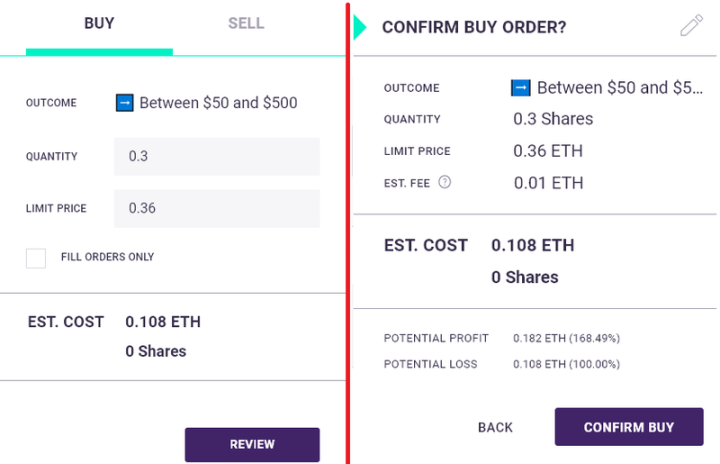

For example, the second market in the trading market interface above is betting on the price of ETH before the end of April (2019). The three options are less than $50; between $50 and $500; and greater than $500. If we choose the second option to place a bet, you will see a page like this:

Users select a stake and a price (probability). The number in the image represents a 0.3 stake bet with a 36% probability of the final price falling between $50 and $500, costing a total of 0.108 ETH. Like Polymarket, Augur also has an order book, but the two are completely different.

The chart shows the lowest sell price of 0.3605. This doesn't mean someone believes there's a 36.05% chance the price won't fall within the $50-$500 range, but rather a 63.95% chance it won't. Therefore, when placing a bet against the price, you need to calculate the probability yourself; otherwise, your order will likely not be matched. The bet just placed requires a user who believes, or is willing to believe, there's a 74% chance the price won't fall within this range. For both parties to be matched, and for the final result to be announced, they can profit from the other party's chips.

This is where the problem arises. Augur only has one option for each option: "yes". Users have to choose to go long (yes) or short (yes).

Augur's permissionless nature leads to the creation of many invalid markets. For example, the expiration date of the aforementioned market may have been set in mid-April, and the results provided by the oracle network were subject to multiple challenges. This resulted in a market on Augur that was supposed to settle in the near term being delayed for nearly five months, consuming numerous disputes before being shut down. This market environment, coupled with the requirement to find evenly matched opponents, resulted in only 6,331 orders out of 11,825 being filled.

Finally, the cost of using Augur is surprisingly high. Besides gas fees and the fees for early users who don’t have a wallet, users also have to pay fees to both the oracle network’s report providers and market creators, as both parties must stake a certain amount of REP.

While market creators and reporters charge low fees (1-2%), users must pay layers of fees to use the platform, which can add up significantly. On Augur, these fees, from lowest to highest, include a reporting fee (0.01%), a market creator fee (1-2%), Ethereum gas fees (depending on order size), and a fiat-to-ETH conversion fee (4% for debit card payments on Coinbase and 1.5% for ACH payments). As a result, total fees for trading on Augur range from 3.5% to 9% or even higher.

The poor wallet experience, one-to-one matching mechanism, logical vulnerabilities and high fees have made it difficult for Augur to expand in scale. However, this does not affect Augur's influence as a "pioneer" in the development of Ethereum and DApp. Some of the teams that developed Augur have now become the backbone of the industry.

Internal conflict within the team, the eliminated players demand 150 million yuan in compensation

Augur was launched by the Forecast Foundation. Public information shows that the organization includes co-founder and Augur core developer Jack Peterson, co-founder and Augur chief architect Joey Krug, early marketing and community director Jeremy Gardner, full-stack engineer responsible for front-end and contract integration Stephen Sprinkle, and researcher Austin Williams, who wrote the game theory proof in the appendix of the Augur white paper.

Among them, Joey Krug has served as Co-Chief Investment Officer of Pantera Capital since June 2017 and is currently a partner at Founders Fund. Stephen Sprinkle left Augur in 2019 to join ConsenSys as a product manager, and then joined BlockFi as Director of Engineering. After BlockFi's restructuring in 2022, he moved to Coinbase to continue to lead institutional products.

But in fact, according to a lawsuit filed by Matt Liston in 2018, a story before the birth of Augur was revealed.

According to a 2018 report by Blockchain.com, Matt Liston initially registered a company called Dyffy in Delaware and hired Jack Peterson. At the time, Liston proposed the idea of developing a prediction market on the blockchain, but Peterson initially disagreed.

Later, Liston read the Truthcoin white paper, authored by Yale University economist Paul Sztorc, and saw the potential for developing a prediction market and issuing a token based on it. Liston successfully persuaded Joseph Ball Costello to invest, and through Paul Sztorc, he also convinced Peterson to support the idea of on-chain development. With this foundation, Liston hired Joey Krug and Jeremy Gardner, the latter of whom proposed naming the project Augur.

In the months that followed, the team debated the technology and business strategy, ultimately leading to the dismissal of Matt Liston, the man who orchestrated it all, in October 2014. Krug replaced Liston as a director, and Peterson became CEO. In December of that year, the Forecast Foundation, a nonprofit organization in Oregon, was established.

Matt Liston stated that Costello, perhaps hoping to completely separate himself from Dyffy, repeatedly pressured Liston to agree not to pursue legal action against Dyffy, acknowledge the acquisition, and exchange his equity for cash or REP tokens. Under continued pressure, Liston was forced to sign the agreement and, due to allegedly being "concealed from the specific ICO distribution plan," relinquished his 5% stake in REP and opted for $65,000 in cash. Based on Augur's market capitalization at the time of the lawsuit, these relinquished tokens are now worth over $20 million.

Matt Liston filed a lawsuit for $38 million in general damages and $114 million in punitive damages against Augur, which had a market capitalization of over $450 million at the time. This totaled $152 million, exceeding one-third of Augur's market capitalization and becoming the "highest claim in cryptocurrency history" lawsuit at the time.

Several of Augur's defendants were surprised that Liston suddenly reneged on his agreement three years after signing it. Furthermore, both Jack Peterson and Joey Krug maintain that Liston is not the founder of Augur. Krug stated, "Liston has made no contributions to the GitHub open source code repository or other Augur repositories. He cannot be considered an Augur founder." Reports indicate that doubts about Liston's true identity have left him struggling with unemployment, and his LinkedIn profile shows no new employment since resigning as Chief Strategy Officer at Gnosis in 2017.

The report, citing sources familiar with the matter, stated that the main cause of the internal conflict was Liston's advocacy for developing Augur on Ethereum, while the team insisted on developing it on Bitcoin. Interestingly, Augur was ultimately launched on Ethereum and became the first successful ICO after the Ethereum mainnet launch. It's worth noting that no further public information regarding the case has been released since then. Given that Augur survived until the end of 2021, the matter was ultimately resolved peacefully or withheld.

After three and a half years of silence, we set out again

In March of this year, Augur suddenly announced its return on X, and the last time this account tweeted was on November 18, 2021.

In 2020, Augur launched an updated version, v2, which included adjustments to the user experience and other aspects. In July of that year, Forbes published an article calling it "a major leap forward in decentralized applications." In the article "Ethereum's First ICO Blazes Trail To A World Without Bosses," Forbes reporter Michael del Castillo stated, "It functions similarly to the internet, but without the need for a trusted third party. If successful, this profound upgrade will go beyond simply enabling horse racing betting without bookmakers; it could mark a turning point for the next generation of the internet."

Although Augur saw over $10 million in participation in a single market during the 2020 US presidential election, the glare of DeFi ultimately led to its collapse at the peak of the 2021 bull market. Perhaps it was the rise of Polymarket that brought prediction markets back into the spotlight after nearly a decade, leading the new team behind Augur to relaunch this year.

Augur's relaunch will be led by two teams: the Lituus Foundation, which will oversee the token, operational matters, and oracle development, and the Dark Florists, which will implement the prediction market. The Lituus Foundation claims to be composed of long-time Augur community members, but no information about its members is currently available.

The Dark Florists are a prominent Ethereum development team. Among their key members, Killari cracked an implementation of indistinguishable obfuscation (a cryptographic scheme designed to transform programs into "black boxes" that can be freely shared and executed but whose internal workings remain completely hidden) developed by the Ethereum Foundation, Phantom.zone, and 0xPARC at Devcon 2024, earning him a $10,000 bounty. Micah Zoltu, known for discovering a major MakerDAO vulnerability in 2019, is also the developer of EIP-3074 and EIP-2718.

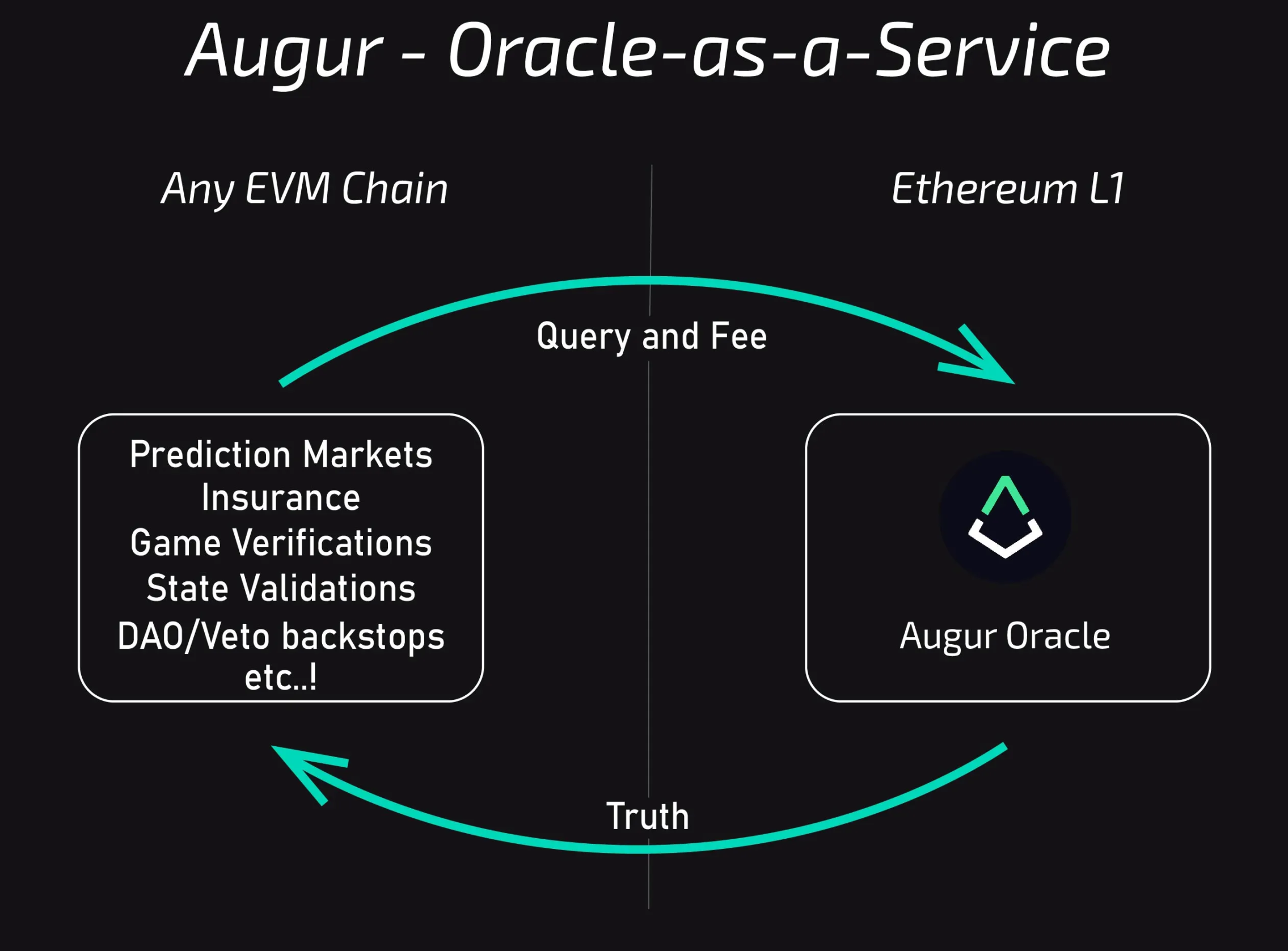

The "new Augur" that this team hopes to launch isn't a purely commercial platform, but rather, as the Lituus Foundation puts it, a cross-chain decentralized truth machine. The Lituus Foundation aims to separate and modularize the oracle from Augur's prediction markets, making it accessible to all applications.

Augur was originally designed as a purely decentralized application, without relying on multi-signatures, managed keys, or fallback mechanisms. Even its token economics incorporates original game theory to leverage the power of the platform (this aspect was not previously discussed; interested readers can refer to the original Augur whitepaper and v2 update ). The new Augur will maintain this spirit. The only information we have available so far is that the new oracle will likely be deployed on Layer 2 and that the initial prediction market will be based on an AMM.

To date, the Litius Foundation has released two progress reports. In the first quarter following the announcement, Litius increased its REP holdings from 250,000 to 550,000, deployed $100,000 in liquidity on Uniswap v3, and planned to launch a CEX. In the second quarter, there were four key developments:

- Launch the website ;

- Oracle research will develop along two complementary lines, one focusing on consumer prediction markets and the other on enterprise oracle use cases;

- Micah Zoltu initiated a crowdloan to intentionally drive a fork of the REP algorithm to test the Augur core security model;

- The foundation's repurchase scale has been expanded to 1 million REP.

The algorithm bifurcation is a very interesting design. The details are quite complicated, so I will give a simple explanation here:

In Augur's design, there's no fixed answer to the "outcome." Augur allows disputes to be initiated by voting on the outcome through staked REP. When the dispute reaches a threshold (2.5% of the total REP staked), the system splits into two parallel universes, one for each outcome. REP holders must choose the universe they agree with and migrate their REP to it. After a dispute begins, if staked REP doesn't reach the threshold within a given timeframe, participants who supported the initial outcome will receive a reward.

Micah Zoltu initiated the crowdloan to raise funds to invest in the disputed, clearly erroneous results, thereby sacrificing some REP to test the feasibility of the mechanism. However, due to this test, the plan to list on the CEX was forced to be suspended and will need to be discussed again after the dispute is fully resolved.

Conclusion

"Feng Tang grows old easily, but Li Guang is hard to be promoted."

In his article "From Prediction Markets to Info Finance" published last November, Ethereum co-founder Vitalik Buterin mentioned that he was a loyal user and supporter of Augur. As Ethereum's first ICO, Augur's design seems far ahead of its time even today.

This advancement does not come entirely from the mechanism, but the premise of its realization is too utopian. What was our discussion about the prediction market at that time?

- Farmers can open a prediction market for harvest season weather as a hedge against the potential impact of climate on yields;

- Use prediction markets to build bug bounties and smart contract insurance;

- Implementing incentivized polling markets and introducing conditional markets to guide policy making (see the Ethereum Foundation’s 2014 article for details);

- Create a trading pair on Uniswap between RealT (real estate token) tokens and tokenized positions betting on falling house prices in the prediction market to allow hedged positions to earn trading fees;

…

The current prediction market is rife with trading and arbitrage, which is one approach, and it seems to be the only correct one at the moment. We've often complained about the lack of innovation in Web3 in recent years, but looking back at the thinking of the original developers a decade ago, do we really have no room for innovation?

Web3 is a giant Polymarket. We were once busy opening new markets, never tired of it. Suddenly, we began making markets in the order book, using bots to find opportunities where the sum of probabilities was different than 1 within milliseconds, and taking arbitrage opportunities by placing stop-loss and take-profit orders before the market closed. It seemed as if everyone had suddenly lost the courage to open a new market and gamble on a bigger future.

An article I translated six years ago mentioned the "3P Theory": predicting the future (Predict), hedging the future (Prepare), and incentivizing the future (Persuade). At the time, I wrote a passage I've since forgotten: Decentralized prediction markets present all possible parallel universes to you. Everyone has the right to choose the future they wish to enter. The more people participate, the greater the potential for guiding time further into the future.