From AMMs to CLOBs: The Race to Bring Nasdaq to the $7 Trillion Chain

- 核心观点:链上CLOB是DeFi吸引机构资本的关键。

- 关键要素:

- CLOB提供机构熟悉的交易框架。

- AMM存在滑点与资本效率问题。

- L2与专用链实现低延迟交易。

- 市场影响:推动传统金融资产上链交易。

- 时效性标注:中期影响

Original author: A1 Research

Original translation: AididiaoJP, Foreight News

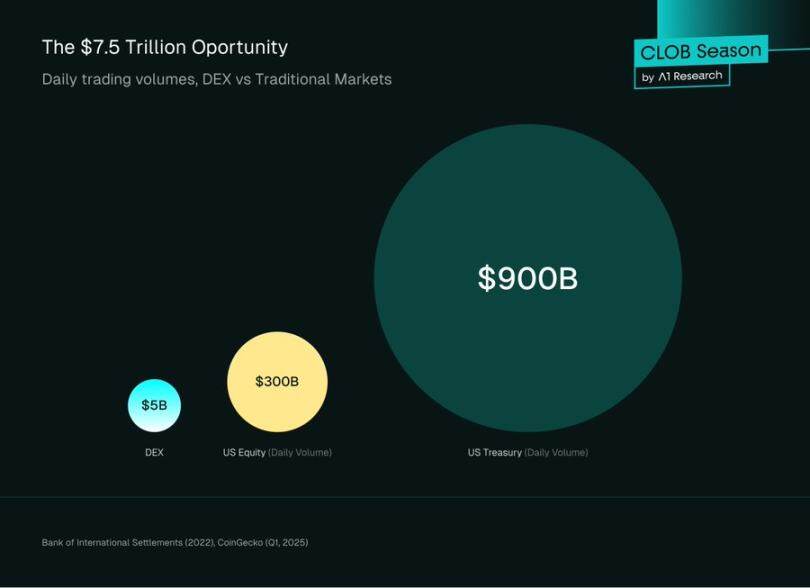

From AMMs to CLOBs: The $7 Trillion Race to Bring Nasdaq On-Chain. According to a 2022 report from the Bank for International Settlements, the global exchange market processes over $7.5 trillion in daily trading volume. Cryptocurrency accounts for less than 2% of this. In the first quarter of 2025, the average daily trading volume of cryptocurrencies plummeted to $14.6 billion. Spot DEXs only process approximately $5 billion in daily trading volume, a negligible error in global finance.

If the financial world is destined to move on-chain, the primary question isn't when, but whether the infrastructure will be robust enough. Consider the scale: the US stock market trades approximately $300 billion daily, while the US Treasury market sees nearly $900 billion in daily volume. For decades, professional traders, market makers, and institutions have built their algorithms, risk models, and entire operational stacks around a single standard: the central limit order book (CLOB).

Now compare this to DeFi. DeFi requires them to abandon this framework and embrace automated market makers (AMMs): trading against mathematical curves rather than order books. From the perspective of institutions managing billions of dollars, this is inefficient and unfamiliar.

So what’s the upshot? Much of the capital entering the crypto space has ended up on centralized exchanges like Binance and Coinbase, which have infrastructure familiar to traditional financial institutions. DeFi’s promise of transparent, self-custodial markets is compelling, but its current operations are a stark departure from Wall Street.

The good news is that this is changing. The emergence of on-chain CLOBs represents a coming-of-age moment for DeFi, a moment when blockchain infrastructure finally matches the sophistication of traditional markets.

When Citadel Securities processed ~35% of US listed retail trading volume through its platform, and when Jane Street generated $20.5B in net trading revenue in 2024, they weren't using AMMs, they were using CLOBs. And now, with platforms like @HyperliquidX processing 200,000 orders per second, and with Ethereum L2 and Solana scaling to millisecond latency, the infrastructure is ready to handle $7.5T in daily trading volume.

This isn’t about replacing AMMs, which will continue to play a vital role in on-chain price discovery, especially for long-tail digital assets. It’s about building a bridge that brings Wall Street on-chain, enabling BlackRock to trade mainstream stocks and bonds directly on DeFi rails, making “decentralized finance” more than just a vision for retail traders, and ultimately unlocking the full potential of programmable, composable, on-chain DeFi primitives.

The path from AMMs to on-chain CLOBs is not just a technological evolution; it's the story of DeFi's growth. When blockchains first enabled trading, limited block space and slow transactions made traditional order books impossible. AMMs offered an elegant solution: trading against mathematical curves rather than waiting for counterparties. They made DeFi possible. But now, as the infrastructure matures and institutional demand becomes paramount, markets are returning to the method that has always operated at scale: the order book.

This article explores the technical mechanics of both systems, their fundamental trade-offs, and why the most sophisticated trading applications are leading the charge back towards CLOBs, not as a rejection of DeFi innovation but rather as its natural evolution towards institutional readiness.

Automated Market Makers: DeFi Innovation from Zero to One

Ethereum has significant limitations: low throughput (approximately 15 transactions per second) and high and volatile gas fees. Replicating a traditional high-frequency CLOB, which requires constant order submission, cancellation, and modification, is computationally and economically infeasible. AMMs offer a brilliant solution to this problem.

Instead of matching individual buyers and sellers, AMMs allow users to trade against a pool of assets, called a liquidity pool. Prices are determined not by an order book but by a deterministic algorithm.

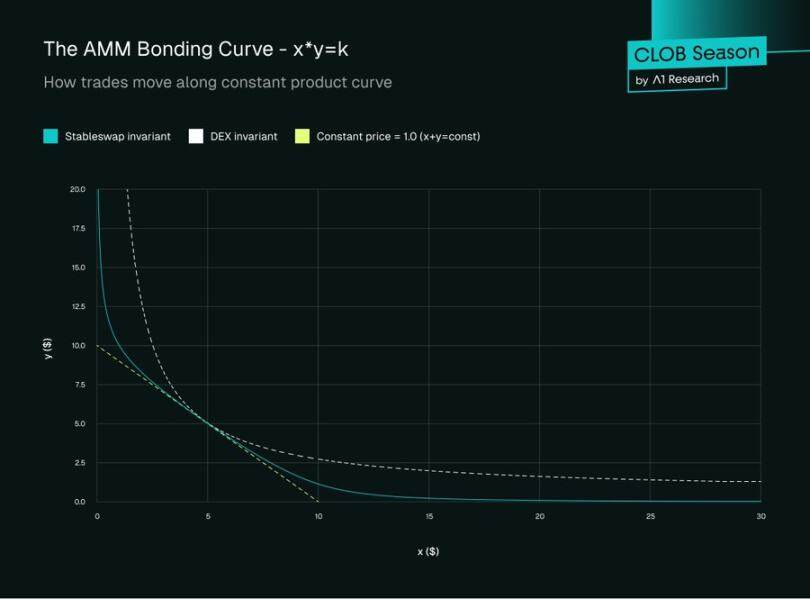

Constant Product Market Maker (CPMM)

The most basic and popular type of AMM is the Constant Product Market Maker, implemented by Uniswap. Its mechanism is governed by a simple yet powerful formula:

x × y = k

in:

- x is the amount of asset A in the liquidity pool.

- y is the amount of asset B in the liquidity pool.

- k is a constant product. This value must remain constant during a transaction (ignoring fees).

In CPMM, the price of an asset is simply a ratio of reserves, price of asset A = y / x.

Transaction Examples

Let’s look at a concrete example to understand how trades are executed in CPMM and why slippage is a key consideration.

Initial liquidity pool status

Consider an ETH/USDC pool with the following reserves:

- x = 1,000 ETH

- y = 4,500,000 USDC

- k = 1,000 × 4,500,000 = 4,500,000,000

The spot price before the transaction is the reserve ratio:

Price = y / x = 4,500,000 / 1,000 = 4,500 USDC per ETH

Execute a trade

Scenario: A trader wants to exchange USDC for 10 ETH.

When a trader withdraws 10 ETH from the pool, the constant product formula states:

New ETH balance: x = 1,000 - 10 = 990 ETH

USDC balance must be adjusted so that: 990 × y' = 4,500,000,000

Therefore: y = 4,500,000,000 ÷ 990 = 4,545,454.55 USDC

Traders must deposit:

Required USDC = 4,545,454.55 - 4,500,000 = 45,454.55 USDC

Effective payment price = 45,454.55 ÷ 10 = 4,545.45 USDC per ETH

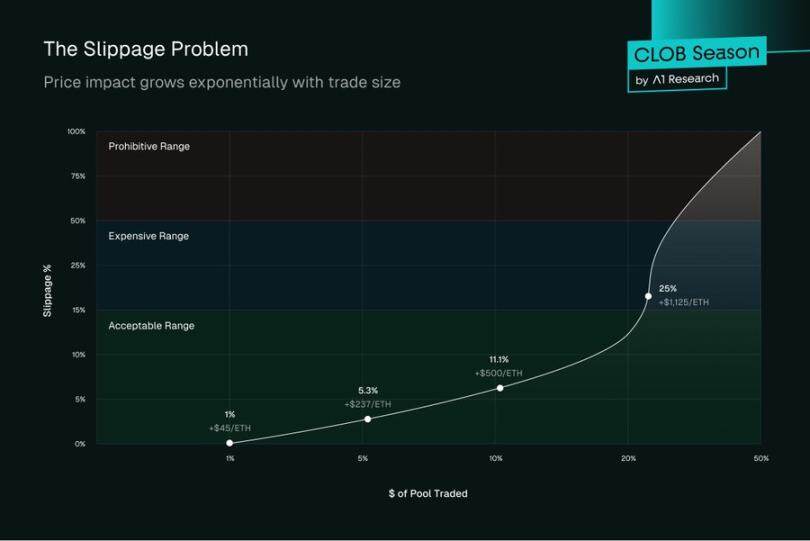

Note that the trader paid 4,545.45 USDC per ETH, rather than the initial spot price of 4,500. This difference is known as price impact.

Understanding Slippage

Slippage represents the percentage difference between the expected price (spot price) and the actual execution price. In our example:

Slippage = (4,545.45 - 4,500) ÷ 4,500 × 100% = 1.01%

This 1.01% slippage might seem acceptable, but as the trade size increases, the constant product formula leads to exponentially worse prices:

For a 50 ETH transaction:

- New ETH balance: 950

- New USDC balance: 4,500,000,000 ÷ 950 = 4,736,842.11

- USDC required: 236,842.11

- Price per ETH: 4,736.84

- Slippage: 5.26%

For a 100 ETH transaction:

- New ETH balance: 900

- New USDC balance: 4,500,000,000 ÷ 900 = 5,000,000

- USDC Required: 500,000

- Price per ETH: 5,000

- Slippage: 11.11%

Price Impact Curve

The relationship between trade size and price impact follows a hyperbolic curve. As you trade closer to a larger percentage of the pool’s liquidity:

- 1% of pool liquidity → approximately 1% slippage

- 5% of pool liquidity → approximately 5.3% slippage

- 10% of pool liquidity → approximately 11.1% slippage

Key AMM Concepts and Challenges

Liquidity Provider: Anyone can provide assets to a pool (e.g., deposit 1 ETH and 2,000 USDC) to become a liquidity provider. In return, they earn a portion of the trading fees generated by the pool.

Impermanent Loss: The most misunderstood risk for LPs is that AMM pools are isolated markets. Prices therein aren’t set by external sources, but rather by a constant product formula. Every time an asset’s market price moves—like ETH doubling on Coinbase—arbitrageurs step in to trade against the pool until its price matches the global market. This rebalancing process extracts value from LPs: they end up holding more of the asset that’s depreciating and less of the asset that’s appreciating. This loss is called “impermanent” because it disappears if prices revert to their original ratio, but in volatile markets, it often materializes into a very real opportunity cost compared to simply holding on.

Capital Inefficiency: In a standard CPMM model, liquidity is distributed across the entire price curve from zero to infinity. This means that at any given time, the vast majority of the capital in the pool is idle, as trading occurs only at the current market price. For a stablecoin pair like USDC/DAI that fluctuates in a narrow range around $1.00, providing liquidity at prices of $0.10 or $10.00 is extremely inefficient.

Evolution: Centralized Liquidity (Uniswap v 3)

To address the problem of capital inefficiency, Uniswap v3 introduced pooled liquidity. Instead of providing liquidity across the entire price range, LPs can choose to provide liquidity within a specific price range.

For example, an LP could provide liquidity only for the ETH/USDC pair in the $4,400-$4,800 range. This concentrates their capital where most trading actually occurs, allowing them to earn significantly more fees with the same amount of capital. Functionally, this creates a deeper series of liquidity positions that begin to resemble the "limit orders" of an order book, marking the first major conceptual bridge between AMMs and CLOBs.

Remaining challenges facing centralized liquidity:

Impermanent loss amplification

Concentrated positions experience amplified impermanent loss when prices move outside their range. LPs face a harsh dilemma: narrower ranges earn more fees but suffer greater losses when prices drift. A position concentrated within a 1% range could lose 100% of an asset if the price moves just 1% in either direction.

Actively manage burden

Unlike V2's "set and forget" approach, V3 requires constant monitoring and rebalancing. When ETH moves from $4,500 to $4,600, positions centered around $4,500 become inactive, earning zero fees until manually adjusted. This incurs operational overhead comparable to traditional market making.

Gas cost complexity

Managing concentrated positions requires frequent transactions for rebalancing, position adjustments, and fee collection. During periods of high volatility, gas costs can exceed fee income, especially for smaller positions. This creates a barrier to entry for retail LPs.

MEV vulnerability persists

Instant liquidity attacks have become more sophisticated. MEV bots can clamp down on concentrated positions with surgical precision, extracting value instantly before a large trade and removing liquidity immediately afterwards, leaving losses to regular LPs.

Price discovery still fails

The x*y=k formula, even in centralized scenarios, doesn't reflect true market dynamics. There's no concept of market sentiment, order flow, or price-time priority. Every trade moves price, regardless of size or intent, creating artificial volatility.

Liquidity fragmentation

The different ranges chosen by LPs created a fragmented liquidity landscape. A trader might face good liquidity at $4,500 but terrible slippage at $4,550, leading to unpredictable execution quality across price levels.

No native limit orders

While concentrated positions are similar to limit orders, they are not true limit orders. They continue to provide liquidity in both directions, may be partially filled multiple times, and are not guaranteed to be executed at a specific price.

The success of spot trading and the problems of perpetual contracts

Thus, while AMMs have revolutionized spot trading (Uniswap alone facilitates over $2 trillion in cumulative trading volume), their success has not translated to the perpetual futures market. This divergence reveals a fundamental truth about market structure: different tools require different infrastructure.

What does this mean? Spot markets are forgiving. Traders exchanging ETH for USDC accept slippage as the price of instant execution. Trades are settled instantly, with no ongoing obligations. AMMs excel here because their simplicity aligns with the straightforward nature of spot trading.

Perpetual futures, on the other hand, require precise entry and exit prices, continuous funding rate calculations, a real-time liquidation engine, and leverage management. @GMX_IO and other AMM-based perpetual platforms struggle with these requirements. Their reliance on oracle pricing creates toxic order flow opportunities, where traders can exploit price discrepancies between oracle feeds and actual market conditions. The lack of true price discovery means positions are often mispriced, exposing liquidity providers to asymmetric risk. AMM-based perpetual platforms implement stop-loss and limit orders through assisted position systems, but these systems lack the sophistication, reliability, and price discovery advantages of true order book markets.

The result is predictable: professional traders remain on centralized exchanges. While Uniswap has captured significant spot market share from Coinbase, GMX and its peers have barely managed to shake Binance's dominance in the perpetual swaps space. Perpetual futures trading volume, 3-5 times that of the spot market, remains firmly in the hands of CeFi.

This isn't a failure of execution, but an architectural mismatch. Perpetual futures evolved from traditional futures markets, which have always relied on order books for price discovery and risk management. Trying to force them into an AMM model is like asking a Formula 1 car to run on square wheels—technically possible, but fundamentally inefficient.

The market is ready for solutions, and Hyperliquid and a new generation of on-chain CLOBs are now providing them, recognizing a simple truth: to capture institutional perpetual swaps flow, you need institutional-grade infrastructure. Not an approximation, not a workaround, but the real thing: an on-chain order book with performance rivaling that of centralized venues.

Central Limit Order Book (CLOB): Precision and Efficiency

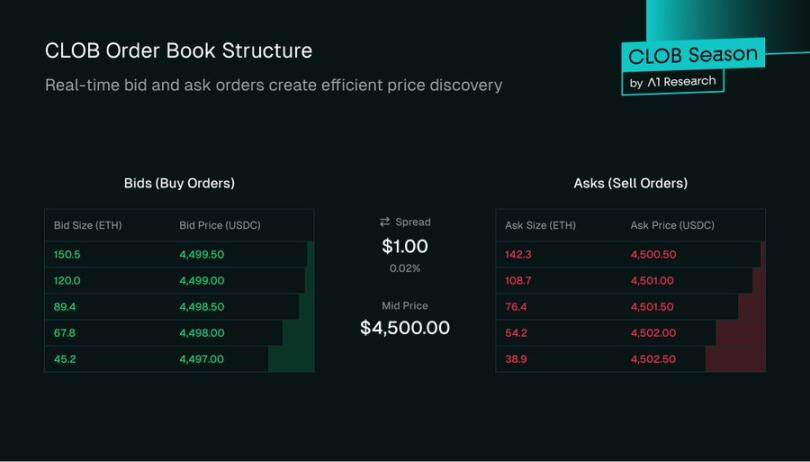

The CLOB is a cornerstone of traditional finance, powering everything from the New York Stock Exchange to Coinbase. It is a transparent and efficient system for matching buyers and sellers.

Core Mechanics

A CLOB is essentially a list of two orders for a specific asset pair:

- Buy side: A list of buy orders, sorted by price from highest to lowest.

- Sell Side: A list of sell orders, sorted by price from low to high.

The difference between the highest bid price (the highest price someone is willing to pay) and the lowest ask price (the lowest price someone is willing to accept) is called the bid-ask spread. In addition to the spread, the depth of each price level also impacts execution quality. For example, a CLOB with 100 ETH available at $4,500 provides better execution for large trades than a CLOB with only 10 ETH available at that level, as deeper liquidity reduces slippage.

Order Types and Matching Engine

Users can interact with CLOBs using a variety of order types:

Limit order: An order to buy or sell at a specific price or better. For example, a limit order to buy ETH at $4,495 will only execute if the ask price reaches $4,495 or lower. If it can't be filled immediately, it stays on the order book, increasing market depth. This is how market makers provide liquidity.

Market Order: An order to buy or sell immediately at the best available market price. A market buy order will "walk through the order book," consuming the lowest available sell orders one by one until the entire order is filled. This provides certainty of execution, but does not guarantee price.

Stop-loss orders: These are activated only when a specified trigger price is reached. For example, a sell stop order at $4,400 would execute if ETH falls to that level, helping traders manage downside risk.

The matching engine is the core algorithm that enforces these rules, generally following a price-time priority principle. Orders at higher price levels are matched first. If multiple orders exist at the same price, the first order placed is matched first. This first-in-first-out (FIFO) approach at each price level ensures fairness and prevents queue jumping, unlike in AMMs, where larger trades can extract more value.

The Engine of the Order Book: Professional Market Makers

The order book is simply a list of interests until liquidity is available. Unlike AMMs, where liquidity is passively provided by a diverse pool of limited partners (LPs), CLOBs rely on a specialized class of participants to operate effectively: market makers. These are complex entities, typically professional trading firms or dedicated liquidity funds, whose primary business is providing liquidity.

What do market makers actually do?

The core function of a market maker is to be ready to both buy and sell an asset at any given time. They do this by placing a buy order and a sell order on the order book simultaneously. This action achieves two key goals:

- Ensured Liquidity: Market makers guarantee that there are always orders available for retail traders to trade. Traders who want to sell an asset can immediately hit the market maker’s bid price, and traders who want to buy can immediately get their ask price.

- Tighter spreads: Competition among multiple market makers forces the difference between the highest bid and lowest ask prices to be as small as possible. A narrow spread is a sign of a healthy, liquid market and results in better prices for traders.

Market makers primarily profit from capturing the bid-ask spread. For example, if they have a buy order for ETH at $1,999.50 and a sell order at $2,000.00, their goal is to buy from the seller at the lower price and sell to the buyer at the higher price, earning a $0.50 spread on each round trip. Their total profit is essentially (spread) x (trading volume).

This is not a risk-free activity. Market makers face significant inventory risk.

If the overall market price of ETH suddenly drops, the market maker’s buy order will be filled, and the accumulated ETH inventory is now worth less than the price they paid. If a market maker accumulated 100 ETH at $4,500 and the price drops to $4,400, they face an unrealized inventory loss of $10,000.

Conversely, if the price of ETH rises dramatically, their sell order will be filled, selling their inventory below the new, higher market price.

To manage this, market makers use complex algorithms to continuously adjust their quotes based on market volatility, trading volume, and their current inventory levels. Professional market makers typically use perpetual futures or options on centralized exchanges to hedge inventory risk and maintain a delta-neutral position. This is a highly proactive and data-driven process, in stark contrast to the passive "deposit and forget" nature of limited partners in standard AMMs.

On-chain liquidity fund landscape

The transition to on-chain CLOBs has attracted professional liquidity funds and trading firms that honed their skills in traditional finance and centralized crypto markets. Firms like @wintermute_t, @jump_, and @GSR_io are now major players in DeFi, providing deep liquidity to on-chain order books.

These companies don’t trade manually. They connect to DEX protocols via APIs and run high-frequency, automated strategies. To attract these key players, on-chain CLOBs have developed a strong incentive structure:

Maker rebates: Many order books offer a maker-taker fee model. Takers pay the fee, while makers receive a small rebate. For high-volume market makers, these rebates can be a significant source of revenue.

Liquidity mining programs: Protocols often reward market makers directly with their native governance tokens. These programs typically require market makers to meet specific key performance indicators, such as maintaining a certain order book depth, a maximum spread, and an uptime exceeding 90% on a given trading pair. This is a highly effective strategy for protocols to bootstrap liquidity for new markets.

Operating on a blockchain presents unique challenges not found in traditional finance:

- Gas Costs: Every order placement, cancellation, and update is an on-chain transaction that consumes gas. This creates ongoing operational costs that market makers must factor into their profit models. The low fees of L2 and the high throughput of L1 are crucial to achieving this.

- Latency and MEV: Blockchain block times introduce latency. For example, with Ethereum’s block time of approximately 12 seconds, a market maker’s order could be “in transit” and unmodifiable for up to 12 seconds, whereas traditional finance can achieve microsecond updates.

During this time, the market can move against them. Further complicating matters, orders are visible in the public mempool before they are confirmed, exposing them to maximum-value-extractable strategies like front-running. To mitigate this, market makers employ techniques such as splitting orders, routing through private mempools, or leveraging off-chain execution.

Why CLOBs are back: Technology enablers

The initial hurdles faced by on-chain CLOBs are computational

High-throughput L1s: Chains like @solana, @SeiNetwork, @monad, @Aptos, and @SuiNetwork are built for high throughput and low latency, making on-chain order books feasible. These are general-purpose L1s designed to host many applications. In contrast, specialized L1s like Hyperliquid's HyperCore are tailored for trading, with matching engines optimized for speed and performance.

Rollups: High-performance rollups like @megaeth_labs, @fuel_network, and @rise_chain aim to enable real-time, low-latency transactions on Ethereum by leveraging parallel transaction processing. In addition to general-purpose rollups, we're also seeing specialized L2 application chains. For example, @hibachi_xyz, based on @celestia, or Solana network extensions like @bulletxyz_ are purpose-built to host on-chain matching engines.

Crucially, these designs rely on scalable data availability layers like @eigen_da and Celestia, which achieve the throughput required for order book-style trading. Meanwhile, advances in ZK infrastructure make it possible to run verifiable off-chain CLOBs, combining performance with Ethereum-level security.

Projects like Hyperliquid, Bullet, @dYdX are excellent examples of DEXs based on the CLOB model.

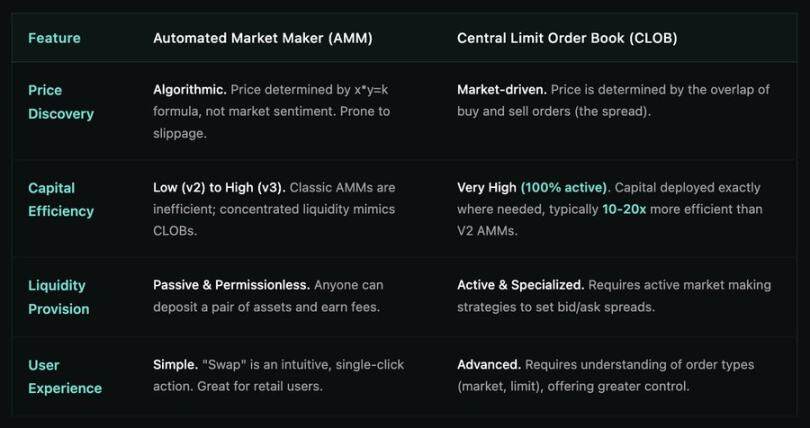

Part 3: Head-to-Head Comparison: AMM vs. CLOB

What this means for users

The transition from AMM to CLOB is not just a technical upgrade, it directly reshapes the user experience:

Retail traders: Get better prices and lower slippage, with a trading interface that will be familiar to anyone used to using centralized exchanges.

Institutions: Now have access to professional-grade tools, advanced order types, risk management, and deep liquidity on a transparent, decentralized rail.

DeFi protocols: Unlocking more composable liquidity, capital is efficiently allocated and seamlessly integrated across the ecosystem.

As blockchain approaches traditional finance-level performance, the gap between centralized and decentralized trading experiences will narrow, making on-chain markets not just an alternative but a competitive arena for global finance.

Conclusion: The maturity of DeFi transactions

AMMs are a groundbreaking innovation in DeFi, solving the cold start problem that made on-chain transactions possible when blockchains were slow and expensive. They democratize market making and provide a simple, unstoppable way to trade on-chain.

However, as DeFi matures from a niche market for early adopters into a parallel financial system seeking to attract institutional capital and professional traders, its infrastructure must also mature. Central limit order books provide market makers with unparalleled capital efficiency, precise price control, and the granular control required for complex trading strategies.

While AMMs will always have a place for long-tail assets and simple exchanges, the future of high-volume, professional-grade decentralized trading belongs to CLOBs. The CLOB movement is not about replacing AMMs, but about building the next layer of complex financial infrastructure on-chain.