Will Bitcoin be "incorporated" into the U.S. mortgage system? The private market has tested the waters with $65 million

Original author: BitpushNews

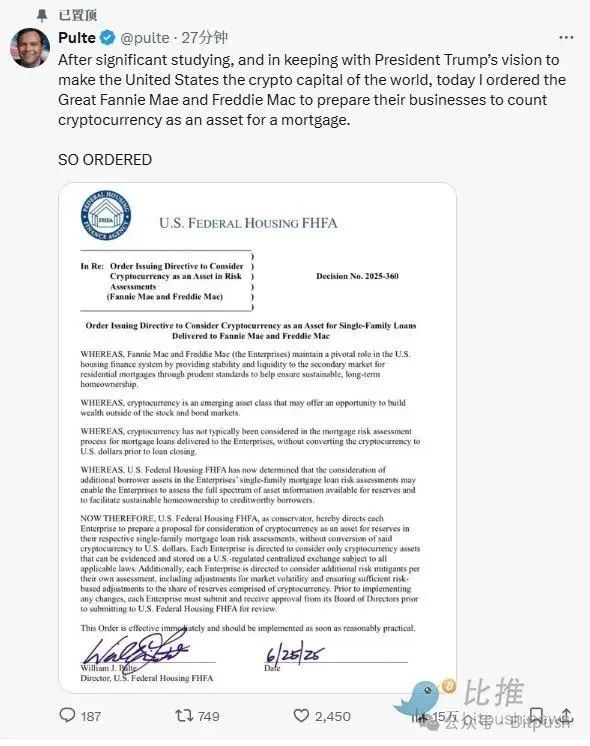

On June 25th local time, Bill Pulte, director of the U.S. Federal Housing Finance Agency (FHFA), suddenly issued a statement saying that he had asked Fannie Mae and Freddie Mac - the two "invisible giants" that control more than half of U.S. mortgage loans - to study the inclusion of cryptocurrencies such as Bitcoin in the mortgage assessment system!

As the news came out, Bitcoin soared by 2.2%, reaching $107,000, and its market share soared to 66%.

It is worth noting that Bill Pulte is the grandson of William J. Pulte, the founder of Pulte Homes, one of the largest home builders in the United States. He was appointed director in March 2025 during Trump's second term.

Unlike his predecessor, Bill Pulte has been publicly supportive of cryptocurrencies since 2019, using his social media influence to promote the adoption of digital assets and encourage policy openness.

Financial disclosures show that he personally holds between $500,000 and $1 million worth of Bitcoin and a similarly sized position in Solana. He also holds a stake in Marathon Digital Holdings, a U.S. Bitcoin mining company, and has invested in speculative stocks such as GameStop.

What does Fannie Mae/Freddie Mac do?

Fannie Mae (Federal National Mortgage Association, FNMA) and Freddie Mac (Federal Home Loan Mortgage Corporation, FHLMC) are two government-sponsored enterprises (GSEs) in the United States.

They are not banks that provide mortgages directly to homebuyers, but they play a vital role in the secondary mortgage market. By acting as market makers (i.e., continuous buyers), they ensure liquidity in the loan market.

This role can be roughly compared to a combination of China's "housing provident fund management center" + "state-owned bank" + "secondary market securitization platform", but the operating model is more market-oriented.

According to the National Association of Realtors, Fannie Mae and Freddie Mac back about 70% of the mortgage market through 2025. That means most conventional loans made by private lenders are ultimately backed or purchased by one of these two entities.

The FHFA was established after the collapse of the US housing market in 2008 to strengthen supervision and maintain the safety and liquidity of the mortgage financial system. Any policy changes it announces will have a profound impact on potential homebuyers and the entire financial industry.

While FHFA’s review of crypto assets in mortgage underwriting remains in the early and exploratory stages, its consideration itself reflects a shift in the relevance of crypto assets and leadership priorities.

How might crypto assets be valued?

In the U.S., borrowers who currently want to use digital assets in the mortgage process must first convert them into U.S. dollars and deposit the funds in a regulated U.S. bank account. To comply with Fannie Mae and Freddie Mac’s down payment or reserve fund guidelines, the funds must also be “matured,” meaning they must remain in the account for at least 60 days.

The FHFA review is expected to examine whether those rules need to be updated. One possible area of focus is asset valuation. Because of the volatility of crypto assets like Bitcoin, lenders may be reluctant to accept the full market value when assessing a borrower's assets. A common approach in traditional finance is to apply a "haircut," which deducts a portion from the stated value to account for potential price fluctuations. Whether cryptocurrencies will adopt similar adjustments is uncertain.

Holding history may also be scrutinized. Lenders generally favor assets that have been held for a long time over those that have been held for a short time. Assets with clear documentation, consistent custody, and minimal trading activity may carry more weight than assets that have been recently acquired or frequently transferred.

Stablecoins may be considered separately. Tokens like USD Coin (USDC) and Tether (USDT) are designed to maintain a stable value relative to the U.S. dollar, which may make them more suitable for underwriting purposes. Even so, the treatment of stablecoins will depend on regulators’ acceptance of their structure, custody arrangements, and transparency standards.

Private markets have already taken the lead

Milo Credit, a Florida-based lender, launched one of the first crypto-mortgage products in the U.S. in 2022. It allows borrowers to pledge digital assets such as Bitcoin, Ethereum, or certain stablecoins as collateral without having to sell cryptocurrencies and pay a cash down payment. This setup allows customers to obtain financing of up to 100% of the value of their home without liquidating their crypto assets. As of early 2025, Milo reported that it had issued more than $65 million in crypto-mortgage home loans.

Similarly, Figure Technologies, a fintech company led by former SoFi CEO Mike Cagney, has explored a large-scale crypto-backed mortgage program, offering loans of up to $20 million using digital assets as collateral.

In addition, the “Bitcoin Savings Account” launched by Ledn can also be seen as a mortgage product, allowing users to obtain US dollar loans with a 50% LTV ratio.

However, these private products operate outside the federal mortgage system. Their loans are not eligible for resale to Fannie Mae or Freddie Mac, which means they do not benefit from the same level of liquidity and risk sharing as traditional loans. As a result, interest rates tend to be higher, and lenders often keep the loans themselves or work with alternative investors for financing.

Another limitation is risk. Crypto-collateralized loans typically require overcollateralization — meaning borrowers must pledge crypto assets worth more than the loan amount to offset volatility. But even with that buffer, price swings can present challenges.

In short, if FHFA chooses to promote this policy, it will mark the transformation of cryptocurrencies from investment products to practical financial tools. Although it will take some time for the specific implementation, it has already sent a strong signal to the market: the mainstream financial system is opening the door to crypto assets.