DigiFT x HashKey Deep Research: Tokenization of real-world assets, leading the next generation of capital markets

Original author: Ryan Chen, Henrique Centieiro

Original source: DigiFT x HashKey Capital

1. Abstract

Limited scale, unlimited potential:Compared with traditional financial markets, the overall market size of RWA (Real-World Assets), which currently has a market value of only billions of dollars, is small. Driven by the efficiency and cost advantages of blockchain technology, the potential market value of RWA could reach tens of trillions of dollars in the next five years.

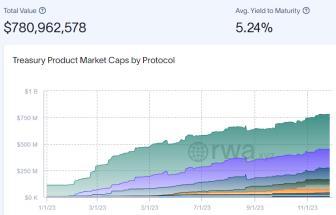

The mainstream supply side is fixed income products, the rise of government bond tokens, and the shrinkage of private credit:According to data from RWA.xyz and Dune.com, the current TVL (Total Value Locked) of the main RWAs is concentrated in U.S. Treasury bond-related products, which has grown from US$100 million in early 2023 to the current total market value of US$784 million. In crypto The market still shows a rapid growth trend despite the cold winter. Private credit product TVL has dropped from its peak of US$1.5 billion in mid-2022 to only US$500 million now due to thunderstorms in projects such as FTX, 3AC, and Luna.

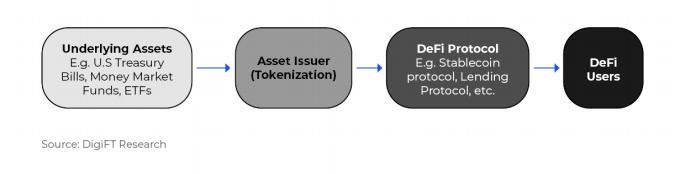

The demand side is mainly institutional investors for short-term cash management and portfolio diversification:By analyzing the wallet addresses related to government bond tokens, we can find that the main holders are institutional investors. The current demand for RWA is mainly focused on the short-term cash management needs of investors in the crypto market. In addition, DeFi protocols, such as stablecoin protocols and lending protocols, have also introduced RWA to diversify their investment portfolios and reduce overall system risks.

There are still serious challenges in supervision:RWAs face a diverse regulatory environment globally. The United States enforces strict securities laws and has global influence. In contrast, Switzerland, Singapore and the Hong Kong SAR have shown active support in providing a friendlier regulatory environment for RWAs.

The innovative model combines RWA with DeFi:Adopting innovative business models such as lending and token packaging enables RWA with high investment thresholds to be integrated into DeFi. But challenges such as anti-money laundering compliance, sales restrictions and unresolved asset ownership issues remain unresolved. The integration of RWA and DeFi will lead DeFi towards compliance to a certain extent.

Outlook:In the short to medium term, due to the lack of stable income products in the crypto market and the need for risk diversification, RWA market products will still be dominated by fixed income products. In the medium to long term, as the market’s understanding of compliant assets deepens and the relevant legal framework improves, we will see more diversified RWA assets and may witness the next generation of RWA assets driven by both blockchain and tokens. capital market.

2. Foreword: Encryption Native and the Real World

Like the concept of stablecoin, the emergence of the concept of Real World Asset is a metaphor proposed by people in the development of encrypted assets based on blockchain technology.These metaphors are not intended to be novel, but to allow people with different backgrounds and experiences to intuitively understand new things using imagination and symbols, without requiring too much background knowledge and overview. In the process of technological innovation, metaphor is a management tool. People create metaphors consciously or unconsciously, and use these metaphors to put explicit knowledge and tacit knowledge together to start communication.

Real estate, gold and other tangible assets that exist in the physical world cannot exist in electronic form compared to the currently widely used electronic systems. In order to embed them in the electronic system, the gold traded also has a corresponding issuer. For electronic systems, such tangible assets in the physical world are also real world assets, but the public has become accustomed to their existence and does not consider them to be a special concept.

The real world assets discussed in the crypto world are actually tokenized, allowing token holders to have legally confirmed ownership of the tokens underlying assets. These real world assets, including tokenized equities, bonds, and real estate, exist outside of the crypto world. The categories of real world assets are too rich, and the implementation models are also diverse. If you want to define real world assets, the simplest way is to define encrypted native assets to separate the two types of assets.

Real-world assets, from a technical point of view, are nothing more than mapping original asset types to the blockchain through technical and legal means, using tokens to represent the ownership of the underlying assets, thereby enjoying new financial High efficiency and low cost brought by settlement tools.

If the new technology does indeed bring about breakthrough efficiency improvements and cost reductions without fatal flaws, the new technology will eventually be adopted.The medium of financial transactions has evolved from paper bills on the counter of the New York Stock Exchange a hundred years ago to the electronic trading system that is widely adopted today. It is an extremely possible development path to move towards a token form with blockchain as the underlying technology.

Before the bridge between the virtual and the real was opened, the cryptographic world and the real world were separated, so the concept of “real world assets” was widely discussed as a metaphor that allows the two worlds to understand each other.

This research report will focus on the most important part of real world assets (RWA) now and the most mainstream part in the future - financial securities, to study the current status of the on-chain capital market and explore the next generation capital market.

These metaphors serve as an intermediate form to make the transition from the original native assets of the crypto world to the integration of the real world; blockchain is a new financial technology infrastructure, and the nature of finance should not change.

3. Introduction: What is RWA (Real World Asset) and how does it work?

Most of the crypto-native assets are realized through smart contracts, and the relevant asset operation logic and business are run through the code on the chain. Typical crypto-native assets include public chain tokens, DeFi tokens, etc. In comparison, real world assets (RWA) are more complex and diverse. RWA can be of any type, and the business and income do not come from assets on the chain. For example, wine, cars, (traditional) financial securities, and precious metals can all be classified as RWA.

Crypto-native assets define rules through smart contracts, which is what the crypto community often calls code is law. But for real world assets, the implementation process is completed through tokenization.Since more asset relationships occur in the real world off-chain, what we often call tokenization is not a simple action of issuing tokens on the chain, but a series of processes, including the purchase and custody of underlying assets. The legal framework linking the underlying assets and tokens, and the issuance of the tokens.Through tokenization, combined with off-chain laws and regulations and related product operation processes, token holders have legal claim rights to the underlying assets.Therefore, especially for financial assets, off-chain laws and regulations are a more important part, and RWA tokenization cannot occur without the framework of the traditional world.

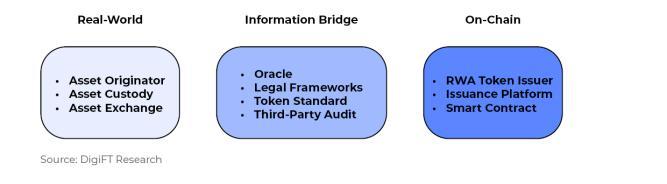

RWA implementation structure

RWA tokenization implementation mainly has three parts. Depending on the asset type, each part will have different roles to assume their respective responsibilities:

Real world: asset originators, asset custodians, asset purchase channels

Information bridge: oracles, legal framework, token standards, third-party audits, deposit and withdrawal payment channels

On-chain part: RWA token issuer, issuance platform, smart contract

Figure 1: RWA implementation structure diagram

4. Issuance model: direct issuance model and asset-backed model

The legal and regulatory requirements for securities-type financial assets are relatively strict. Starting from the discussion of security-type assets, we can cover the situations that most assets may encounter. We mainly discuss here the issuance and trading of security-type tokens.

From the perspective of issuance model, encrypted assets are all direct issuance models, and the registration and registration of asset ownership occurs directly on the blockchain. Since there is no real-world business and underlying assets, its asset nature cannot be clearly defined. Under normal circumstances, the issuance of securities-type assets requires registration and registration with relevant authorities; except for the Swiss DLT (Distributed Ledger Technology Act, DLT Act) Act, there is currently no relevant law that clearly allows the issuance of securities-type products directly on the blockchain, and Due to the lack of relevant precedents for reference, the current direct issuance model of securities is mostly experimental in nature, typical of which include the Diners Club 1-month note issued by DigiFT and Diners Club Singapore.

The assets in the crypto world are highly homogeneous and relatively volatile. The volatility of RWA assets is relatively low and has a weak correlation with crypto assets. Therefore, investors in the crypto world have a certain demand for RWA. In order for the crypto world to better accept the concept of RWA, an asset with broad consensus is needed. The first choice is the U.S. dollar, which is a stable currency; followed by U.S. Treasury bonds, which are the current mainstream of RWA and are security tokens. These assets cannot be issued through the direct issuance model unless the sovereign institution, that is, the US government issues it on the chain (such as CBDC). Therefore, another issuance model has been derived. By obtaining corresponding assets as support in the traditional capital market, a corresponding number of tokens are issued, which is called the asset-backed model.

This section mainly discusses these two types of models.

Asset issuance model classification

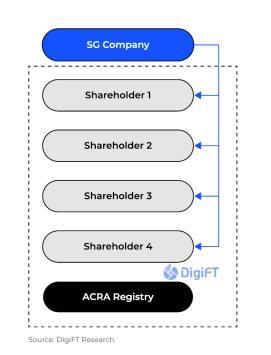

To understand the RWA token issuance model, lets first look back at the issuance model of traditional assets, taking securities as an example. The figure below shows the issuance model of a typical Singaporean companys equity.

Figure 2: Traditional stock issuance model

A company will have multiple equity holders. The ownership of these equity interests will be registered with ACRA (Accounting and Corporate Regulatory Authority, Singapore Accounting and Corporate Regulatory Authority), and its transaction and transfer records will also need to be registered with ACRA.

Among them, ACRA is Singapore’s securities registration agency. If there are corresponding institutions in the markets of other countries, or different market mechanisms are involved, such as transfer agents in the United States, their function here is the registration and registration of security holders.

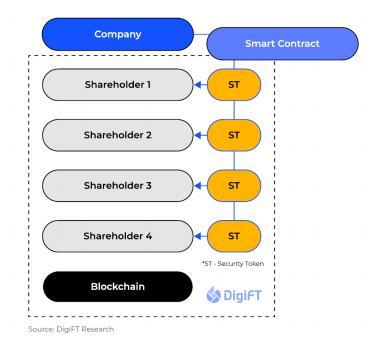

As shown in the figure below, if you want to issue tokens on the blockchain, you actually use the blockchain as a ledger to register and register asset ownership, and record each transfer process.

Figure 3: Direct issuance model

In a few countries and regions, financial innovation is relatively at the forefront. They support the direct registration of securities on the blockchain, such as the DLT Act promulgated by Switzerland. Therefore, in these regions and countries, securities can use the blockchain as a ledger through relevant authorized institutions. Directly issued, these regions and countries recognize blockchain as a tool for equity registration. At present, in other major financial markets, such as the United States, Singapore, Hong Kong Special Administrative Region, etc., relevant laws do not currently support the direct registration and registration of securities on the chain. Therefore, most assets need to detour, such as Franklin Templeton and other Wall Street Funds issued by financial institutions on the chain are still based on centralized accounting systems, with only blockchain as the second accounting tool.

Therefore, the current mainstream issuance models on the market can be classified into two categories: direct issuance model and asset-backed model. Essentially, both issuance models issue related bonds on the chain, but the form of issuance and the corresponding rights and interests are completely different.

It should be noted that if private securities meet certain conditions, such as a limited sale amount, a limited number of investor types, and a very limited impact on the financial market, they can also be issued under the premise of compliance, and the issuer can choose Use blockchain as an equity registration tool. This is also the reason why most RWA projects are currently only open to qualified investors. This will be discussed in detail in the Dilemma: Why it is only open to qualified investors section.

Direct Issuance ModelDirect Issuance Model

In the direct issuance model, the asset issuer uses the blockchain as an accounting tool to register the assets and issue corresponding tokens on the chain. Among them, the token is the underlying asset itself. Investors who purchase and hold such assets can directly obtain various related rights and interests corresponding to the asset, such as voting rights for stocks, repayment rights for bonds, etc.

However, the direct issuance model still has many limitations in the current market environment. For example, such securities are tokenized, incompatible with the current mainstream stock exchange structures (Nasdaq, SGX, etc.), or have certain friction costs. At present, the relevant legal structure is not perfect, and there are currently not enough legal cases that can be used as a reference for future precedents.

Asset-Backed Model

Due to the imperfections of the current laws and the very limited assets on the chain, many projects also choose to use the asset-backed model for issuance. In essence, this type of token is a new security that represents the economic rights and interests of the underlying asset. The asset issuer issues and registers the assets in a system other than the blockchain. After the third party purchases the assets, tokens are issued according to the corresponding proportion. The counterparty risk is the asset issuer (asset issuer) and the token issuer (asset -backed token issuer).

The asset-backed model is a relatively common RWA model at present. It can introduce real-world income into the chain, but it will introduce additional risks. Although the issued tokens can contain the economic value of the underlying security assets, the equity and real security equity May vary.

5. Current situation: The supply side is fixed income products, and the demand side is institutional investors.

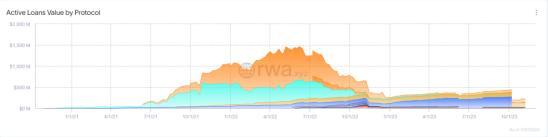

The current security-type RWA on the chain is mainly private credit and US Treasury tokens. RWA-related assets first emerged through the private credit model in 2020. The mainstream product is unsecured credit, and related projects such as Maple Finance, Clearpool, Centrifuge, etc.

Figure 4: RWA private credit active credit volume, classified by agreement, data source: rwa.xyz, data on November 27, 2023

Private credit markets also have cycles. When the market has a good foundation of trust, borrowers are willing to borrow money at appropriate interest rates, and lenders are willing to take risks to provide funds. After the Luna and FTX thunderstorms, multiple lending pools in the private credit market were implicated and defaulted, resulting in a significant decline in TVL, which is currently in a relative bottom cycle.

On the other hand, due to the high interest rates of the US dollar in the external macro market and the lack of returns in the internal crypto asset market, assets related to the tokenization of US Treasury bonds have risen. According to data from DeFi Llama, with clear market demand, the TVL of treasury bond-related RWA projects is in a continuous growth stage.

Figure 5: Total market value on the U.S. Treasury bond-related token chain, source: rwa.xyz, data on November 27, 2023

Among them, the treasury bond tokenization experiment conducted by two American asset management giants, Franklin Templeton (green part in the picture) and Wisdomtree on the public chain Stellar, has also generated hundreds of millions of dollars in TVL. However, this type of project focuses on centralized equity registration and only uses blockchain as a second way to record token ownership.

Address held

Compared with DeFi assets, RWA itself is not sexy enough from the perspective of income and gameplay, butDue to the safety of the underlying assets, it attracts institutional investors who pursue stable returns and high liquidity. Since it is linked to real-world assets, most platforms have KYC and AML requirements. If it is a securities-type asset and the legal and regulatory requirements are more stringent, there will generally be demand from qualified investors.These compliance restrictions and yield factors make it more difficult for RWA assets to enter the hands of retail users. At present, the main RWA TVL is concentrated in US Treasury bond-related products. U.S. Treasury bonds, as the largest asset class with the most market consensus, stable returns and liquidity, have been adopted by many DeFi protocols and crypto asset investors in the context of the macro bear market.

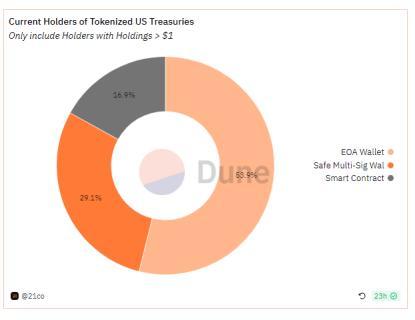

We have observed that the main RWA is held in the hands of institutions and protocols, either for direct short-term liquidity management needs, or as underlying financial assets to implement structured products (which will be covered in the Innovative Business module later). We directly observe the data on the chain to query the current holdings of major U.S. debt-related tokens. The data comes from the token chain information of Ondo Finance OUSG, Maple Finance USDC Cash Management, Backed Finance bIB 01/bIBTA, OpenEden Tbill and MatrixDock STBT. It was found that 29.1% (denominated in US dollars) of tokens are held in multi-signature addresses, which can be understood as held by institutions/companies. 16.9% (in USD value) is held in contracts for DeFi applications such as the Ondo Finance OUSG token in the lending platform Flux Finance. These DeFi projects use lending and other model designs to transmit the benefits of RWA to the DeFi ecosystem in a permissionless manner. Additionally, 53.9% (in USD value) is held in EOA addresses. Considering that some companies/institutions hold assets through MPC wallets, third-party custody or hardware wallets, the address on the chain is still expressed as an EOA address, so a larger proportion of tokens will be held in the hands of institutions.

Figure 6: Distribution of holdings of U.S. Treasury tokens according to address type, source: Dune Analytics, 2 1co, data as of November 27, 2023

Summary of RWA status quo: moving from 2B model to B 2 B 2C model

We believe that in the short term, direct sales of RWA assets will still be mainly 2B. We can also see that RWA is being combined with DeFi to serve as the underlying asset for various structured products.Typical examples include Angle Protocol (the underlying asset is Backed Finance bC 3 M), Spark Protocol (the underlying asset is Treasury bonds and other assets purchased by MakerDAO through a trust structure), USDV (the underlying asset is MatrixDock STBT), TProtocol (the underlying asset is MatrixDock STBT), Mantle mUSD (can be exchanged for Ondo Finance USDY) and Flux Finance (collateral is Ondo Finance OUSG), realizing the B 2 B 2C model. These combinations can accelerate the promotion and application of RWA while meeting compliance requirements.

Figure 7: RWA asset supply chain

6. Dilemma: Why is it only open to qualified investors?

Except for a few projects that implement RWA issuance plans for retail investors under certain restrictions by complying with specific local laws, issuing special prospectuses, and registering specific securities (see the RWA innovation module for details on the plan), most RWAs currently on the market are only Available to qualified investors. According to the regulations of different regions, investors are required to have a certain amount of financial assets to be considered a qualified investor. For example, Singapore requires personal financial assets of 1 million Singapore dollars (approximately US$730,000).

The reason why most RWA products, including U.S. Treasury-related products, are only available to accredited investors or institutional investors is that compliant issuance to retail investors would be costly.

These costs arise from the lack of correlation between the underlying assets and the ultimately issued tokens.Relevant securities laws have strict requirements for the issuance of securities to retail investors, including the preparation and registration of a prospectus. In addition, the laws of most jurisdictions require that ownership of assets such as stocks and bonds needs to be recorded in a specific way (for example, in a register maintained by the issuer). The current authoritative agencies do not accept tokens and blockchain directly as tools for ownership registration, which means that the ownership of tokens cannot directly represent the ownership of the underlying assets under these laws and regulations.

RWA issued using an asset-backed model, such as RWA tokens with U.S. Treasury bonds as the underlying asset, needs a bridge between the underlying assets and the intended RWA token. The RWA token is a new security. This bridge can be established by treating the RWA token as its own independent security, but this also means that the RWA token needs to independently comply with all relevant securities laws, that is, the issuer needs to Additional preparation and registration of a prospectus using the RWA token as a security, etc.

To understand this, we can look at the traditional model of issuing securities to retail users. Whether you are issuing stocks or bonds, you need to go through:

The companys internal preparation phase determines the various characteristics of the companys securities and selects and hires investment banks (underwriters) and other financial professionals, such as lawyers and accountants, to assist in the IPO process.

Select an underwriter. The underwriters will assist the company in preparing and executing the bond offering.

Due diligence, auditing and rating (for bonds), reviewing internal controls and governance structures to ensure compliance; for bonds, ratings will affect the credit quality of the bond.

The prospectus, if it is for retail investors, must be approved by the regulatory agency to ensure that investors receive sufficient information.

Pricing, working with underwriters to determine conditions such as valuation and issuance price.

Marketing, conducting road shows, interacting with potential investors, explaining the company’s business, etc.

Issuance and listing must comply with the listing requirements and standards of the exchange.

Post-transaction management, such as financial information disclosure, announcements, etc.

It can be seen that if you want security assets to be sold to retail investors, you need to go through complicated processes. Among these processes, there are two reasons that make it difficult for RWA to directly face retail investors:

The costs are too high and the benefits are not enough.After a complete set of processes, the issuance of securities to retail investors will bring millions of dollars in costs and require regulatory approval; the overall encryption market is smaller than the traditional market and cannot meet large-scale financing needs. Such compliance Issuance costs are too high and returns are insufficient.

The infrastructure is not perfect enough.There is no compliant stock exchange to provide trading services for the tokens, and the securities registration agency temporarily does not support the registration of tokens as ownership, etc.

If they do not want to bring such high costs and transaction frictions, issuers can only issue products to qualified investors and institutional investors. The current mainstream RWA assets in the Crypto market are SPVs established by start-up companies as issuers. If traditional capital market securities, such as U.S. Treasury bonds, are used as the underlying assets and are issued using an asset-backed model, and investors buy these issued bonds, the essence What is purchased on the SPV is not a treasury bond, but a corporate bond issued by the SPV with treasury bonds as the underlying asset. There is actually a very high counterparty risk, so the U.S. treasury bonds originally rated AA+ have become BBB investment grade companies through this structure. bonds. Other directly issued corporate bonds are basically issued by smaller companies and have not gone through a complete issuance process for retail investors to save costs. As a result, they can only be issued to qualified investors.

7. Driving force: two-way rush from the real world and the encrypted world

RWA is related to both the real world (for securities products, that is, the traditional financial world) and the crypto world. Judging from the current performance of market participants, both sides have sufficient driving forces.

Traditional world driving forces:

Adopt new financial infrastructure to reduce costs and increase efficiency. The ledger synchronization technology implemented by the blockchain consensus mechanism takes into account security and greatly reduces the time and cost of financial transaction settlement.

Self-hosted.After experiencing the collapse of many banks/financial institutions, the black box of traditional finance is not trusted; the self-custody attribute of encrypted assets has begun to be favored by mainstream capital.

Asset flexibility.Tokenized assets are penetrable on the chain and can be seamlessly integrated with on-chain applications to bring users a better experience, such as lending, trading, pledging, etc., and even programmable assets through certain smart contracts. .

Real-time settlement.Transactions and loans are realized through smart contracts on the chain, without intermediaries. Assets are directly cleared and settled on the chain. There is no complex and decentralized accounting system, real-time settlement is achieved, and time costs are significantly reduced.

Transparent and traceable.Transaction records are real-time, open, transparent and traceable, enabling real-time analysis and monitoring.

Globalization.Through DeFi infrastructure, investors have the opportunity to easily access global assets.

Crypto World Drivers:

On-chain asset management needs.On-chain asset management seeks stable income and better liquidity, and financial products such as U.S. Treasury bonds are widely recognized investment targets.

Find alternative sources of income.The native income on the chain mainly comes from pledge income, transaction fee income, and loan interest income. The decline in the activity of financial activities on the bear market chain has led to varying degrees of decline in all three types of income. If you seek returns that are less correlated with the native assets on the chain, you need to introduce RWA related assets.

Diversify your portfolio.The types of assets on the pure investment chain are very single and have high correlation and high volatility. The introduction of RWA assets that are more stable and uncorrelated with the native assets on the chain can achieve hedging and form a richer and more effective investment portfolio strategy.

Introduce diversified collateral.The high correlation of assets on the chain makes lending agreements prone to runs or large-scale liquidations, further exacerbating market volatility; the introduction of RWA assets with low correlation to assets on the chain can effectively alleviate such problems.

Under the overall macro background, DeFi assets lack a rate of return; at the same time, the rate of return of DeFi assets fluctuates greatly and it is difficult to provide certainty; in comparison, traditional financial products are more abundant and diversified, and the hedging methods are more complete, which can provide more stable returns. . Therefore, DeFi protocols and Web3 institutions have turned their attention to RWA.

Due to the smooth legal framework and product process that has been running in the early stage, RWA will mainly be in the form of bonds in the short and medium term until it enters the next development cycle due to emerging market demand. We expect there will continue to be demand for RWA assets, especially bond-type assets, ahead of the advent of risk assets in the crypto world. The main demand comes from short-term cash management needs, and the transmission of income to retail users through the DeFi protocol to meet the liquidity management needs of retail users; during the bull market of risk assets, the demand for RWA assets will weaken, and it will also There will be new RWA assets with higher risks and higher returns emerging to compete with crypto-native assets.

Using blockchain and smart contracts as core technologies to build a new generation of capital markets, the trend will not go back once it is established.

8. Global Regulation: United States, Europe and Asia

Given that most RWA assets are tokenized securities, RWA tokens will be subject to relevant securities laws in each jurisdiction. Since the United States is one of the few jurisdictions that explicitly provides that its securities laws have extraterritorial effect, the crypto industry may be more aware of and wary of U.S. securities laws. U.S. securities laws apply to any securities offered to or by residents of the United States. To address the former, most RWA tokens will specifically emphasize not being sold to U.S. residents. To address the latter, any RWA token launched by a US-based company would need to register its offering with the SEC or (more likely) take advantage of one of the registration exemptions. Some examples of such exemptions include Regulation A/D (small value offerings) and Regulation S (offerings offered outside the United States).

Regulation A(Reg A):Often referred to as a mini-IPO.

Reg A Category 1: Allows companies to raise up to $20 million in a 12-month period, has lower ongoing reporting requirements, and is available to accredited and non-accredited investors.

Reg A Category II: Allows companies to raise up to $75 million in a 12-month period, has stricter ongoing reporting requirements, and is available to accredited and non-accredited investors.

Regulation D(Reg D):Provides exemptions from full SEC registration requirements for certain private placement securities.

Rule 504: Allows companies to raise up to $5 million in a 12-month period. Available to accredited and non-accredited investors.

Rule 505: Allows companies to raise up to $5 million in a 12-month period, but is generally limited to accredited investors and up to 35 non-accredited investors. Non-accredited investors are required to provide certain financial disclosures.

Rule 506(b): Allows unlimited capital raising from accredited investors and up to 35 non-accredited investors. No general solicitation or advertising is allowed.

Rule 506(c): Allows general solicitation or advertising but restricts the offering to accredited investors only.

Regulation S(Reg S):It provides an exemption from the registration requirements of U.S. securities laws for offerings made only to non-U.S. persons that qualify as foreign jurisdictions. Although Reg S offerings are primarily intended for non-U.S. retail investors, U.S. issuers may also participate in Reg S offerings as long as they comply with the relevant rules and restrictions.

Unlike the US, the EU and Asia do not have a comprehensive securities framework - instead, securities laws will vary by specific jurisdiction. Within the EU, Switzerland is a clear supporter of tokenized securities and is one of the few countries to legally recognize and regulate tokens as valid proof of ownership through the adoption of Digital Ledger Technology (DLT).

In Asia, Singapore and the Hong Kong Special Administrative Region of China, historically the centers of traditional finance, are also at the forefront. The Singaporean government has repeatedly stated its support for asset tokenization. According to reports, Hong Kong plans to issue guidelines for security token issuance in the near future.

9. Main Participants: Participation Paths, Models and Current Situation

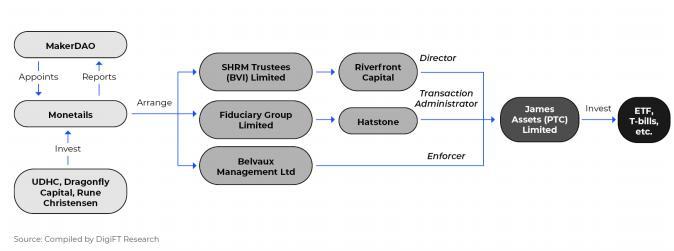

MakerDAO

MakerDAO is a stablecoin protocol that generates stablecoins by pledging assets. As the DeFi protocol with the largest holdings of RWA on the chain, MakerDAO uses RWA as a mortgage asset to generate a new stable currency Dai. Although it seems that most of MakerDAOs RWA holdings are purchased through the off-chain model, it is difficult to discuss RWA without MakerDAO.

MakerDAO began trying to introduce RWA assets as collateral as early as 2021, and was one of the first projects to combine RWA and DeFi. MakerDAO initially cooperated with the lending protocol Centrifuge to introduce off-chain assets onto the chain as collateral to generate new Dai.

Since the assets issued by Centrifuge are private credit, generally bonds issued by small companies (large companies have traditional and mature financing models), they often have higher default risks, such as the loan pool related to freight forwarding invoices ConsolFreight. The default resulted in a $1.84 million risk exposure for MakerDAO.

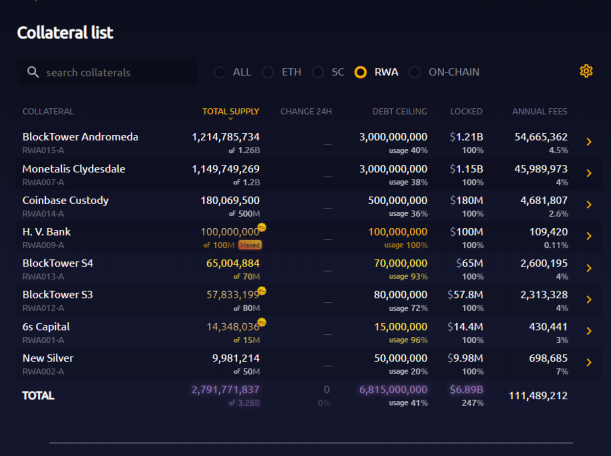

Figure 8: MakerDAO’s current number of RWA collaterals, source: Makerburn.com, data as of November 27, 2023

MakerDAO proposed the idea of purchasing U.S. Treasury bonds as Dai collateral in early 2022. The initial demand was to hope that the USDC in the Dai stability module PSM (peg stability module) could generate income for the protocol. The resulting two projects were launched in 2022. Monetails Clydesdale and BlockTower Andromeda launched in 2023; both purchase money market funds, U.S. Treasury bonds or U.S. Treasury bond ETFs through off-chain trust structures whose beneficiaries are MakerDAO MKR and DAI holders. The above two projects currently have more than 2 billion US dollars in related asset purchases, and use these assets as collateral to generate Dai. For details on the implementation method and trust structure of Monetails Clydesdale, please check the previous MakerDAO RWA report written by DigiFT.

Figure 9: MakerDAO Monetails Clydesdale Trust Structure Chart

The MakerDAO community is currently considering the possibility of tokenizing U.S. debt products, which was proposed by strategic consultant Steakhouse. It has already received proposals from multiple platforms.

MakerDAO passes the treasury bond proceeds to Dai holders through Spark Protocols Dai Saving Rate (DSR). Previously, the DSR was raised to 8% and the interest rate was maintained for about one month, attracting a large number of assets (mainly USDC) to be minted into Dai. Currently, the DSR interest rate has been lowered, and there are 1.62 billion Dai in the DSR pool.

Region: Decentralized Organization

Product: sDai (Dai stable coin in DSR)

Issuance model: off-chain trust model

Investor requirements: No license required

DeFi protocol integration: lending protocol Spark Protocol, other protocols also indirectly obtain the income of RWA through direct investment in sDai

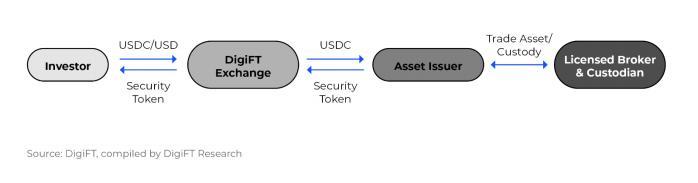

DigiFT

DigiFT was established in Singapore in 2021. It is the first licensed on-chain real-world asset exchange. It is certified as a recognized market operator by the Monetary Authority of Singapore and holds a capital markets services license.

DigiFT allows asset owners to issue blockchain-based security tokens and provide liquidity through a variety of channels, including innovative automated market maker (AMM) trading mechanisms, over-the-counter (OTC) and peer-to-peer (P2P) trading ). Investors can conduct continuous liquidity transactions through the AMM mechanism and retain control over the digital asset tokens in their wallets.

Currently, DigiFT offers a variety of products, including a single U.S. Treasury bond, DUST (DigiFT U.S. Treasury Token; DUST is a series of tokens with AA+-rated U.S. Treasury bonds as the underlying asset, backed by highly liquid investment-grade short-term U.S. Treasury notes. , aiming to generate income while ensuring the safety and liquidity of assets to meet the needs of cash management.), U.S. Treasury bond funds, bank bills and ETH pledge products that meet regulatory requirements.

Figure 10: DigiFT product flow chart

Region: Singapore

Products: Single U.S. Treasury token DUST, U.S. Treasury fund tokens, bank bond tokens, compliant Ethereum pledge tokens, etc.

Supported currencies: USDC, USD

Issuance model: asset-backed model, direct issuance model

Investor requirements: Qualified investors and institutional investors

DeFi protocol integration: No DeFi protocol integration yet

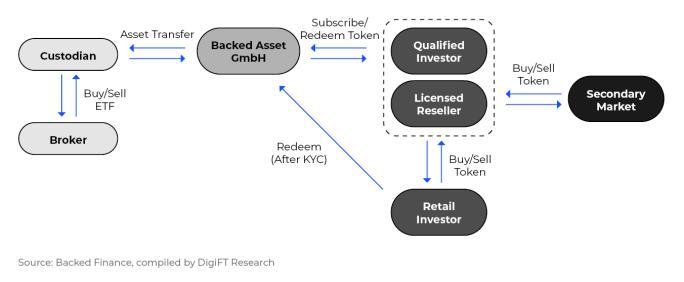

Backed Finance

Backed Finance is a RWA tokenization platform that tokenizes real-world assets such as ETFs and stocks and can transfer them arbitrarily on the chain. Tokens issued by Backed Finance track the price of the underlying asset and are backed by the underlying asset 1:1. Backed Finance hopes to build a platform focused on decentralization that can be integrated with multiple DeFi protocols and support multiple blockchains.

The design of Backed Finance tokens is relatively special. There is no whitelist mechanism. Users can transfer money at will after subscribing. Tokens can be sold on the chain through licensed resellers. Some tokens were previously liquid on Uniswap. The specific implementation methods will be detailed in the Innovation Module.

Figure 11: Backed Finance product flow chart

Region: Europe

Products: U.S. Treasury Bond ETF tokens, Eurozone Treasury Bond ETF tokens, stock tokens, etc.

Supported currencies: USDC

Issuance model: asset-backed model

Investor requirements: Subscription: Qualified investors; Redemption: After KYC, you can be a retail investor; Secondary market purchase: No license required

DeFi protocol integration: Angle Protocol integrates the Eurozone government bond ETF token bC 3 M as collateral to generate its euro stable currency

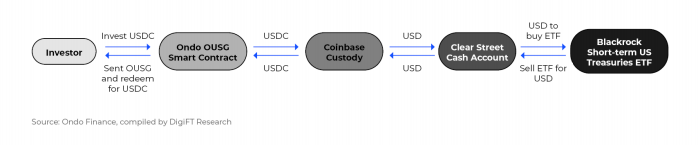

Ondo Finance

Ondo Finance provides investors with tokenized ETFs, including bond funds, U.S. Treasury bond funds and U.S. money market funds, etc. Its main products are for qualified investors. At present, Ondo Finances main product is the short-term US Treasury bond fund token OUSG.

Figure 12: Ondo Finance product flow chart

The underlying assets of USDY issued by Ondo Finance in August 2023 are short-term US Treasury bonds and bank demand deposits. USDY is registered under SEC Reg S and can be sold to non-U.S. retail investors.

Region: United States

Products: U.S. Treasury Bond ETFs, U.S. Money Market Funds, High Yield Bonds

Supported currencies: USDC

Issuance model: asset-backed model

Investor requirements: Qualified investors; non-U.S. retail investors (USDY)

DeFi protocol integration: Layer 2 network Mantle integrates USDY to its on-chain decentralized exchange; Ondo Finance integrates the Flux Finance lending platform to provide lending services to OUSG holders

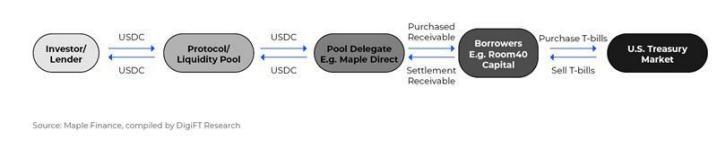

Maple Finance

Maple Finance is a lending platform that selects pool delegators through DAO voting. The agents manage the use of the pool and connect borrowers and lenders.

Figure 13: Maple Finance product flow chart

Region: United States

Products: Various lending products, underlying assets include treasury bonds, accounts receivable, etc.

Supported currencies: USDC

Issuance model: asset-backed model

Investor requirements: Main products, such as U.S. Treasury bond products (Cash Management), are open to qualified investors and institutional investors; some lending pools have no investor restrictions

DeFi protocol integration: UXD Protocol purchases Maple Cash Management products as collateral to generate stable coins

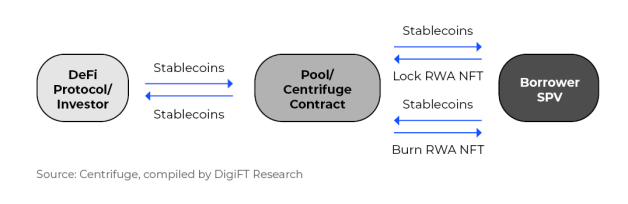

Centrifuge

Centrifuge is a RWA lending infrastructure to realize on-chain financing for real-world assets and build a lending capital market. The asset initiator sets up a special purpose vehicle (Special Purpose Vehicle), sets up a capital pool on Centrifuge, encapsulates RWA assets on the chain through NFT, locks them in the capital pool as collateral, and generates tokens for investors to purchase. Centrifuge is partnering with 2021 and MakerDAO to introduce RWA assets as collateral to MakerDAO. MakerDAO is the largest buyer of Centrifuge platform assets.

Figure 14: Centrifuge flow chart

Region: determined by its product issuer

Products: Asset-backed bonds for various RWA assets, such as accounts receivable, emerging market corporate bonds, etc.

Supported currencies: Dai

Issuance model: Asset-backed model

Investor requirements: For individual investors (KYC required), investors located in the United States need to meet qualified investor requirements

DeFi protocol integration: multiple RWAs are used as collateral in MakerDAO to generate stable currency Dai

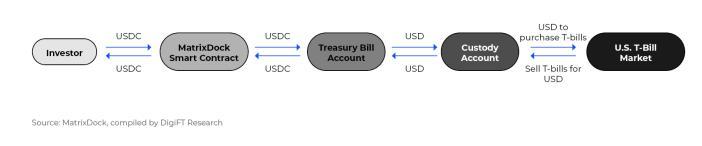

MatrixDock

MatrixDock is a platform for investing in real-world assets, providing digital asset financial products and services to qualified investors. MatrixDocks main product STBT provides holders with U.S. Treasury bond income. The underlying asset is a basket of U.S. short-term Treasury bonds. It is designed with dynamic adjustment (rebase) rules. Each STBT token is anchored at 1 US dollar, and the token balance is updated every working day. thereby reflecting its benefits. STBT supports Chainlinks Proof of Reserve to ensure sufficient reserves of underlying assets and gain the trust of investors.

Figure 15: STBT product flow chart

Region: Seychelles

Product: STBT

Supported currencies: USDC

Issuance model: asset-backed model

Investor requirements: For qualified investors and institutional investors

DeFi protocol integration: STBT can be traded on the decentralized exchange Curve on Ethereum; the DeFi lending protocol TProtocol integrates STBT to provide a lending fund pool for the token; the stable currency project Verified USD uses STBT as the underlying asset to issue USDV.

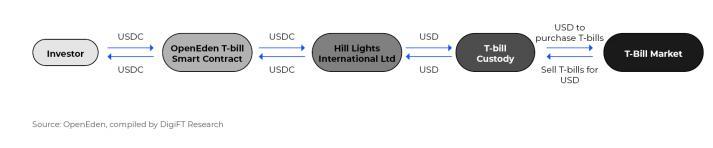

OpenEden

OpenEden is a platform that builds on-chain U.S. short-term Treasury bond products through a bankruptcy isolation structure. Currently, the only product is TBILL VAULT. OpenEden is operated and managed through a professional fund registered in the BVI, investing in short-term US Treasury bonds and placing the bonds in compliant institutional custody.

Figure 16: OpenEden product flow chart

Region: BVI

Product:TBILL

Supported currencies: USDC

Release mode: Direct release mode

Investor requirements: For qualified investors and institutional investors

DeFi protocol integration: UXD Protocol purchases OpenEden Tbill products as collateral to generate stable coins

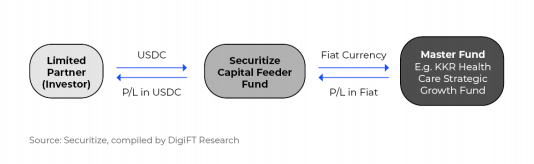

Securitize

Securitize is a private equity fund market, which is relatively special. Securitize consists of Securitize, Inc and its affiliates. Affiliated company Securtize Markets is a broker dealer, a member of FINRA, and an SEC-registered ATS (Alternative trading system, license obtained through acquisition), capable of primary market issuance and secondary market transactions. Affiliated company Securitize LLC is an SEC-registered transfer agent capable of using blockchain technology to transact and record asset ownership.

Securitize cooperates with a number of funds and securities firms to issue tokenized funds, mainly for qualified investors and institutional investors. The issuance model is mainly direct issuance.

Figure 17: Securitize product flow chart

Region: United States

Products: Mainly various funds

Supported currencies: USDC

Release mode: Direct release mode

Investor requirements: Mainly for qualified investors and institutional investors

DeFi protocol integration: None yet

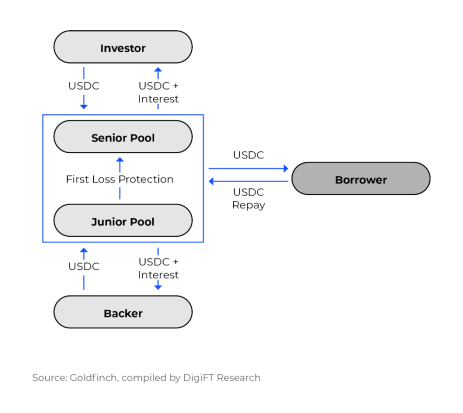

Goldfinch

Goldfinch is a decentralized credit protocol that allows borrowers to issue asset-backed securities using off-chain assets as collateral through the protocols technical and legal framework, and borrow USDC from the capital pool to achieve financing. As the liquidity provider of the capital pool, users invest in USDC to obtain income. In fact, they are purchasing senior bonds with lower default risk. In addition, backers will purchase subordinated bonds to bear higher default risks. Goldfinchs main borrowers are from third world countries and have high development potential.

Figure 18: Goldfinch Senior Pool product flow chart

Region: United States

Product: Asset-backed bonds

Supported currencies: USDC

Issuance model: asset-backed model

Investor requirements: For U.S. qualified investors and non-U.S. retail investors

DeFi protocol integration: None yet

Data observation

The current TVL of the RWA track participants in the above-mentioned crypto market mainly focuses on US Treasury bond-related products, so we use Treasury bond-type products as the object to observe the participation of issuers and investors in the market. The data mainly includes: U.S. Treasury bond-related products of MatrixDock (STBT), Maple Finance (Cash Management USDC), Openeden (Tbill), Ondo Finance (OUSG) and Backed Finance (bIB 01).

The data in this part are as of November 27, 2023. Some tokens are deployed on multiple chains, but this report only looks at the data on the Ethereum blockchain.

Figure 19: MatrixDock (STBT), Maple Finance (Cash Management USDC), Openeden (TBILL), Backed Finance (bIB 01), Ondo Finance (OUSG) TVL situation since issuance

Figure 20: MatrixDock (STBT), Maple Finance (Cash Management USDC), Openeden (TBILL), Backed Finance (bIB 01), Ondo Finance (OUSG) on-chain activity since issuance

in:

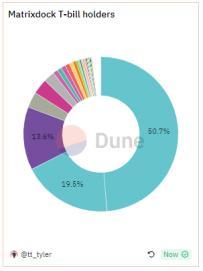

MatrixDock STBT (released in January 2023):

Total amount: 111.29 M USD

Number of holding addresses: 163

Average subscription amount: 836, 721 USD

Average redemption amount: 1,076,914 USD

Total number of subscriptions: 266

Total number of redemptions: 106

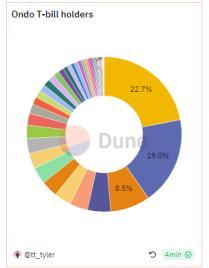

Figure 21: MatrixDock STBT position distribution

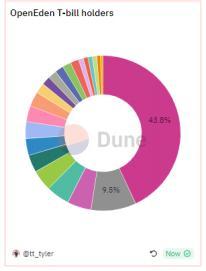

Openeden TBILL (released in March 2023):

Total amount: 11.64 M USD

Number of holding addresses: 28

Average subscription amount: 219, 186 USD

Average redemption amount: 68, 720 USD

Total number of subscriptions: 67

Total number of redemptions: 43

Figure 22: Openeden Tbill position distribution

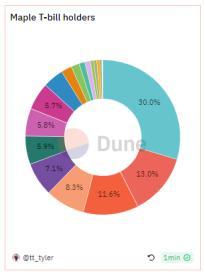

Maple Finance Cash Management USDC (issued in May 2023):

Total: 17.23 M

Total number of holding addresses: 20

Average subscription amount: 472, 312

Average redemption amount: 692, 152

Total number of subscriptions: 98

Total number of redemptions: 42

Figure 23: Maple Finance Cash Management USDC position distribution

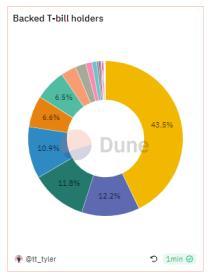

Backed Finance bIB 01 (released in March 2023):

Total amount: 46.27 M USD

Total number of holding addresses: 27

Average subscription amount: 3, 855, 531 USD

Average redemption amount: No redemption transactions yet

Total number of subscriptions: 12

Total number of redemptions: No redemption transactions yet

Figure 24: Backed Finance bIB 01 position distribution

Ondo Finance OUSG (issued in January 2023):

Total amount: 143.43 M USD

Total number of holding addresses: 61

Average subscription amount: 1, 424, 793 USD

Average redemption amount: 1, 494, 384 USD

Total number of subscriptions: 191

Total number of redemptions: 92

Figure 25: Ondo Finance OUSG position distribution

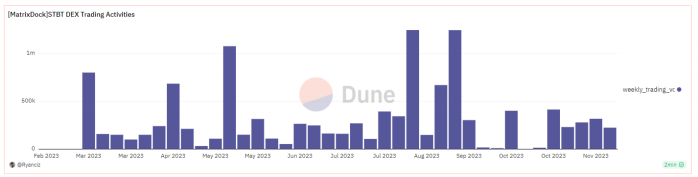

Among them, MatrixDocks STBT has deployed liquidity on the decentralized exchange Curve. It currently has about 4.8 million US dollars of liquidity, which is enough to support a single transaction of 100,000 US dollars. STBT can be exchanged for the US dollar stable currency DAI, USDC or USDT. .

Figure 26: Liquidity deployment of MatrixDock STBT on Curve, source: Curve.fi, data as of November 27, 2023

As of November 27, 2023, there were 514 transactions on STBT on Curve, with a total transaction volume of 11,819,420, and an average transaction amount of 22,995 USD. There are hundreds of thousands of dollars in trading volume every week.

Figure 27: MatrixDock STBT weekly trading volume data, source: Dune.com, compiled by DigiFT, data on November 28, 2023

Backed Finance uses an anonymous securities structure to issue its treasury bond token bIB 01. The token does not have a whitelist design and does not require permission during the circulation process (please see the RWA business model innovation section for details). Therefore, its on-chain transfers are also relatively active, with a total of 207 transfer.

From the above data we can observe:

U.S. Treasury tokens are generally held in large amounts and for long periods of time.Subscription/redemption frequency is low and the amount is large.

There is a need for secondary market transactions.Most treasury bond tokens require more than T+2 time to achieve subscription and redemption, and there is a lack of secondary market trading scenarios for security-type tokens on the chain. Currently, only STBT has liquidity on Curve, and a whitelist address is required for interaction. Judging from STBT transactions, compared with subscription/redemption operations, the volume of a single transaction in the secondary market is smaller, but transactions are more frequent.

Treasury token holdings are relatively concentrated.For the above five projects, the sum of the positions held by the top three addresses in each project exceeds 50% of the total.

10. RWA business innovation model: combining RWA with DeFi

Since most securities RWA assets are only available to qualified investors, the market space is very limited. Many RWA protocols explore innovative business models from legal and business aspects to introduce RWA into DeFi, allowing users to obtain income from U.S. Treasury bonds without permission, or build an infrastructure similar to YuE Bao on the chain.

Lending model: Ondo OUSG - Flux Finance

Ondo Finance has designed Flux Finance, a lending protocol for its U.S. Treasury token OUSG. Flux Finance copied the code of the lending protocol Compound V2 and made a series of modifications to support assets with whitelist restrictions as collateral, and modified its interest rate curve and mortgage rate to adapt to the characteristics of OUSG. Currently, the only collateral on Flux Finance is OUSG, with a mortgage rate of 92%.

The other side of the lending protocol is permissionless and any DeFi user can participate. Users can deposit stablecoins into Flux Finance’s lending pool and earn interest on lending rates. Flux Finance currently supports four stablecoins: Frax, USDC, USDT and Dai, with a usage upper limit of 90%. OUSG holders mortgage OUSG to borrow stablecoins from Flux Finance to obtain liquidity. Flux Finance controls the borrowing interest rate to be lower than the OUSG income. Through the lending model, the income from holding OUSG is transferred to USDC holders in a permissionless manner. At the same time, the capital pool maintains 10% liquidity and can be used by users at any time. extract.

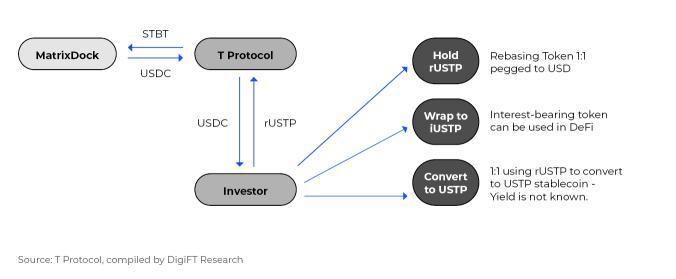

Token packaging and lending model: MatrixDock - TProtocol

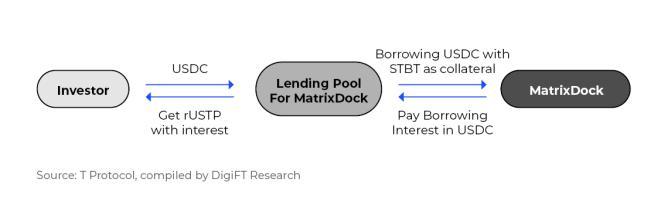

Recently, T Protocol announced its cooperation with MatrixDock, which will provide MatrixDock with a lending pool in the lending protocol of T Protocol V2, and help MatrixDock transmit the income of its US Treasury token STBT to DeFi applications.

TProtocol v1

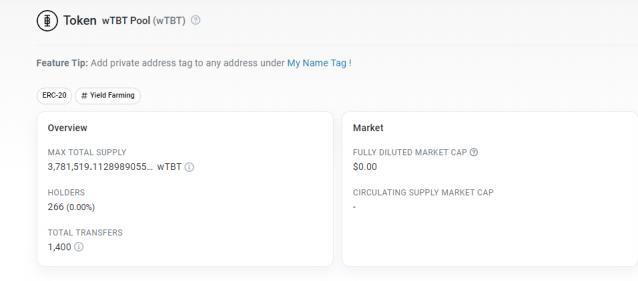

Previously, in TProtocol V1, MatrixDock STBT was repackaged to sell its U.S. Treasury bond tokens without permission; TProtocol used the purchased STBT as collateral to issue the corresponding token wTBT, following the change in the number of held STBT, but there was no whiteout. Limit the list, so as to better integrate with various DeFi applications, and can also interact with different blockchains through cross-chain bridges. Its corresponding token wTBT currently has a circulation of 3.7M.

Figure 28: TProtocol V1 wTBT token, source: Etherscan, data as of November 27, 2023

TProtocol v2

Figure 29: TProtocol V2 product flow chart

In September 2023, TProtocol and MatrixDock reached a cooperation to provide a lending pool for MatrixDocks STBT. MatrixDock STBT is a token with a dynamic adjustment (rebasing) mode. A single STBT is anchored to 1 US dollar; the underlying assets of STBT are a basket of short-term U.S. debt and money market funds, which provide holders with income, and their income is dynamically adjusted (rebasing). The model reflects that the number of tokens is updated daily based on the price of the underlying asset.

TProtocol will open a lending pool for relevant cooperative institutions in the future. Currently, it only supports MatrixDock STBT. Users put USDC into the lending pool and obtain the corresponding number of rUSTP tokens. MatrixDock STBT holders can use STBT as collateral to lend USDC at a lending rate (LTV) of 99%.

The rate of return provided by the lending pool to USDC users is floating and will not exceed the interest rate of STBT itself. The protocol design will transmit as much interest rate as possible to USDC users.

The rUSTP tokens obtained by users who deposit the corresponding amount of USDC are rebasing mode tokens, and each rUSTP is anchored to 1 US dollar. The interest rate is reflected by the daily increase in quantity; in theory, based on the design of the lending rate, the rate of return of rUSTP will follow the rate of return provided by STBT.

MatrixDock currently retains a certain amount of USDC in the lending pool. If users need to redeem their USDC, they will be redeemed through these USDC first. The excess, if the amount is small, will be sold directly through STBT on Curve. If the redemption amount is large, it will be realized through the redemption of STBT on MatrixDock. According to the current design, it takes T+3 to redeem.

rUSTP can be converted into the stablecoin USTP which does not include earnings. Theres no indication of where the remaining interest rate gains will go (possibly TProtocol itself). Users can also exchange it for iUSTP according to the internal exchange rate. It is a token that accumulates income. The number of the token itself will not change. Its value accumulates over time, and it can be better integrated with various DeFi protocols.

The overall process is as follows:

Figure 30: TProtocol V2 product flow chart

TProtocol V2 adopts the form of lending to avoid compliance issues that may arise from the direct introduction of security tokens. Its composition is similar to Ondo Finance and Flux Finance. According to the TProtocol document, users will be able to deposit USDC into fund pools managed by different institutions in the future and obtain income from RWA assets. Behind this is a plan for a stable currency supported by RWA tokens.

RWA-based stablecoin: MatrixDock - USDV

The stablecoin project USDV (Verified USD) uses STBT as the underlying asset and issues stablecoin USDV based on RWA. Compared with centralized stablecoin issuers such as Circle and Tether, stablecoins based on RWA are more transparent as the underlying assets are on-chain assets, thus bringing a more solid credit foundation to stablecoins.

Generally, stablecoin issuers obtain U.S. dollars and mint corresponding amounts of stablecoins, and then use the U.S. dollars to purchase U.S. Treasury bonds or high-rated bank bonds as one of their sources of income; some stablecoin issuers such as Circle will use a certain amount of Proportional profits are distributed to ecological partners. USDV adopts a similar idea, sharing the income from the underlying assets directly to ecological participants through smart contracts to promote the development of the stablecoin ecosystem, such as minters, market makers, and liquidity providers.

STBT holders can become miners of USDV after KYC certification, and deposit STBT into the contract to mint new USDV. USDV uses a special coloring design, similar to Bitcoins UTXO mechanism, to identify the minters of this stable currency on the chain. The income generated by the dynamic adjustment of the corresponding number of underlying assets STBT will be retained in the contract, of which 50% of the income will be allocated to the miners corresponding to these stablecoins, and the other 50% will be allocated to market operators and liquidity providers. These USDV markets Participants can obtain benefits or use these benefits as a basis to further stimulate the development of the ecosystem.

Bearer instrument: Backed Finance Bearer instrument design (Bearer instrument)

The above-mentioned several schemes are to pass the income through another related party through packaging and lending to the DeFi protocol in a permission-free manner, retaining the compliance requirements of the original entities, and the models of Backed Finance and subsequent Ondo Finance USDY have changed. Most of them are breakthroughs at the level of laws and regulations.

Before understanding how Backed Finance is implemented, we first understand registered notes and bearer notes:

Registered instruments: Generally, instruments circulating in the market, especially securities assets, are registered instruments. The issuer or the registration agency authorized by the issuer needs to register the holder of the instrument for every transaction and transfer. .

Bearer instruments: Only when necessary, such as subscription/redemption/transaction, the issuer or registration institution needs to know the identity of the note holder. There is no need to record the identity of the note holder in real time during the circulation process. Owner status.

Backed Finance issues tracker certificates, which are derivatives that track the prices of underlying real-world assets. Each token represents a tracking certificate, and token holders have contractual rights to the value of the underlying asset.

Backed Finance registered the Basic Prospectus for this Tracking Certificate with the Financial Market Authority of Liechtenstein. Since Backed Finance is a company registered in Switzerland, under Swiss law, Backed Finance can only promote it to qualified investors. Authorized Participants, that is, licensed banks, securities companies and non-Swiss regulated financial institutions authorized to sell securities, can sell Backed Finance products to retail customers after subscribing from Backed Finance. On the Backed Finance platform, the subscription of its tokens is only available to qualified professional investors, but retail investors who purchased Backed Finance related products from other places can also redeem them after going through KYC at Backed Finance.

In the prospectus, the tokens issued by Backed Finance are designed as bearer instruments. In the design of the token contract, there is only a blacklist mechanism. Therefore, after issuance, transfers can be made without permission, or directly with various types of DeFi protocol interaction. Identity authentication is only required during the subscription and redemption process with Backed Finance.

Figure 31: Backed Finance token’s transaction record on Ethereum, you can see that the token has liquidity on Uniswap, source: Etherscan, data as of November 27, 2023

Judging from the subscription and redemption situation, the Backed Finance short-term treasury bond ETF token bIB 01 subscription address only has two addresses: 0x 43 and 0x 5 f, and there is no redemption. After subscription, they are provided to other investors through token transfer, so the above two addresses may be authorized dealers to transfer Backed tokens to DeFi protocols or users. Tokens sold through resellers may only need to meet KYC, thus bypassing the restrictions on accredited investors and institutional investors that end users may encounter.

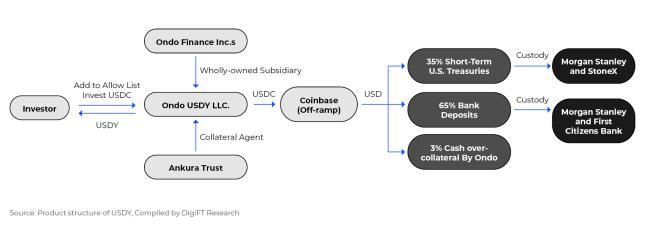

Interest-bearing stablecoin: Ondo USDY - Mantle

Ondo Finance’s newly launched USDY has landed on the Layer 2 network Mantle to serve as the interest-bearing stable currency of the Mantle network. Users of the Mantle network will be able to purchase USDY directly in the DEX. Backed Finance embeds RWA in DeFi through special European laws, and Ondo Finance has chosen another approach.

Figure 32: USDY product structure chart

USDY is issued by Ondo USDY LLC., a wholly-owned subsidiary of Ondo Finance Inc., and is a bankruptcy isolation SPV. USDY uses short-term U.S. Treasury bonds and bank demand deposits as tokens as underlying assets. It is registered through U.S. Reg S and can be sold to non-U.S. retail users subject to certain restrictions. The current restriction on USDY is that there is a 40 to 50-day lock-up period after the sale, which means that users must wait for the lock-up period to end before they can obtain on-chain tokens after subscribing, and they cannot sell to American investors within one year.

There are whitelist and blacklist designs in the USDY token contract issued on Ethereum. Different from other RWA token designs, USDYs whitelist design is special. Anyone can add his or her address to the whitelist by calling the contract. , the user experience is an authorization-like transaction. USDYs official website directly provides the function of sending this transaction. After detecting the IP address, users can directly add their address to the whitelist after agreeing to the terms without KYC. In addition, the USDY token contract is associated with a legal document stored on IPFS, which may mean that the user agrees to the legal terms when adding his address to the whitelist.

Currently, USDY is a token that accumulates profits over time. Then Ondo Finance released USDY and mUSD on Mantle, removing the whitelist and retaining only the blacklist function. mUSD is a stable currency with a unit price anchored to the US dollar in the form of dynamic adjustment (rebase), and the balance is periodically adjusted based on earnings. mUSD can be directly exchanged with USDY on the Ondo Finance platform at the current ratio.

The above five models solve the problem of RWA assets requiring qualified investors at the compliance level from different perspectives such as technology, business, and law, and introduce RWA assets into DeFi to target a wider public. For RWA project owners, it can increase the sales volume of their own platforms; for DeFi, it adds more asset categories, can have stable basic income, and achieve more diversified financial products through a combination of assets.

But no matter which model is adopted, there are many challenges:

AML restrictions.The DeFi protocol cannot prevent non-compliant assets, such as stablecoins from risky addresses, from entering its own protocol; while the RWA protocol requires converting stablecoins into legal currency to purchase real-world assets. The source of funds is usually reviewed and has strict rules. KYC and AML requirements. Such mismatches will affect some DeFi protocols to strengthen the audit of fund sources. If more RWAs enter the DeFi field, the compliance of DeFi funding sources will also be strengthened.

Time mismatch.The market for traditional financial assets is only open five working days a week, only a few hours a day, and is closed on holidays. Asset transactions need to go through banks, securities firms and other systems, often requiring T+1 or even longer settlement time. And DeFi protocols operate 24 hours a day. If there is a demand for liquidity, such as market fluctuations during holidays, the DeFi protocol will need to liquidate assets, and RWA assets will require a longer processing process and time. Protocols that allocate RWA assets need to fully consider liquidity.

Sales restrictions.Many of the above-mentioned RWA projects will require investors not to be residents of certain countries and regions. Possible reasons include tax (for example, the tax system for US residents is very complex), AML (sanctioned in some regions), or