Ethereum has celebrated its first anniversary of merging, what changes have occurred in the MEV supply chain?

Original Author: @Fred, @sui 414

Translated by: Huohuo / Plain Language Blockchain

2023 is the one-year anniversary of the Ethereum merge and the activation of MEV-Boost. To celebrate, we will share insights and trends from the first year of off-chain protocol MEV-Boost on Ethereum. We will first examine the adoption of MEV-Boost and then summarize the behavior we have seen from relayers, blockbuilders, and searchers.

Translator's Note: MEV-Boost is a protocol designed by Flashbots and the community to mitigate the negative impact of Maximum Extractable Value (MEV) on the Ethereum network.

1. Rapid Adoption of MEV-Boost

The merge brought significant changes to Ethereum as the responsibility for block production shifted from a few mining pools to thousands of stakeholders around the world. This change also resulted in a hard reset of Ethereum's MEV infrastructure. With this new set of proposers in control, any relationship between searchers and miners disappeared.

A year before the merge, Vitalik introduced the proposer/blockbuilder separation (PBS) concept as a direct response to the risks MEV poses to PoS Ethereum. Without oversight, MEV would benefit proposers with the most complex infrastructure and relationships with searchers. This would discourage individual staking, promote economies of scale, and threaten the network's trustless neutrality.

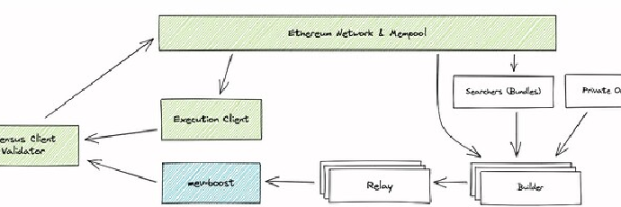

In collaboration with CL Clients, the Ethereum Foundation, and the Eth 2.0 working group, Flashbots developed MEV-Boost as a temporary PBS solution without any changes to the core protocol. MEV-Boost is provided as a sidecar by all CL clients during the merge, enabling off-chain PBS and establishing an open and competitive market for blockbuilders. Through this separation, MEV-Boost democratizes MEV access and allows equal participation for all validators. This is especially important for individual validators who would otherwise be unable to participate and be cut off from any MEV revenue.

From MEV-Boost documentation: Proposer/Blockbuilder separation through MEV-Boost

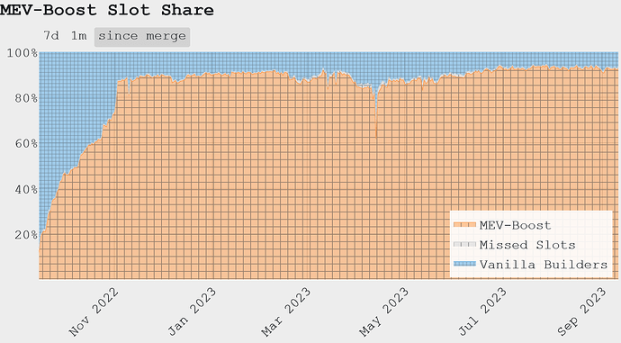

After the merge, MEV-Boost quickly gained adoption, with 50% of validators running it within the first month. By the end of the second month, this percentage reached 90%. Proposers who built blocks through MEV-Boost gained the same median block rewards, thus mitigating the centralizing power that MEV could potentially impose on the Ethereum validator set.

Source: mevboost.pics - Percentage of blocks sourced from MEV-Boost

Source: mevboost.pics - Block rewards of the largest staking entity in the past 6 months

(1) Proposer Revenue and Significant Events

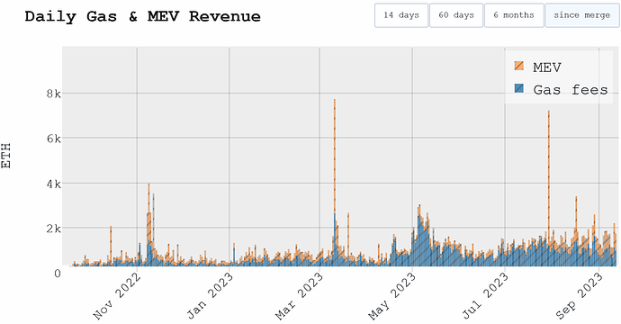

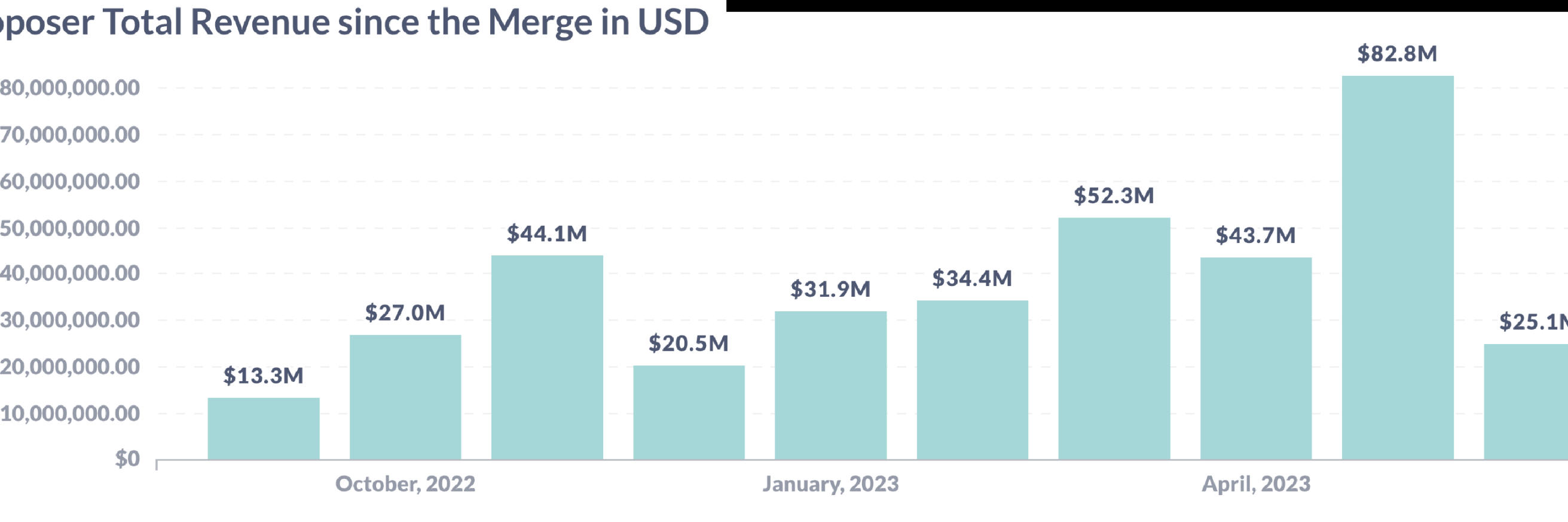

In the first year of Ethereum PBS, validators received over 300,000 ETH from the blocks they proposed, including gas fees and MEV. While gas fees typically constitute the major part of proposers' income, MEV payouts can significantly exceed gas fees during periods of market volatility.

Source: mevboost.pics - Daily Gas and MEV income of proposers since the merge

Last year, there were three notable periods of significant MEV payouts. We will briefly expand on these events here, and more detailed information can be found in our transparency report and this presentation by @elainehu.

1) November 9, 2022: After the FTX crash, we witnessed five days of market liquidation, resulting in a total payout of 14,585 ETH to proposers from gas fees and MEV combined.

2) March 11, 2023: Due to the SVB Bank run and USDC decoupling, on-chain activity surged, leading to a total payout of 7,694 ETH to proposers.

3) July 30, 2023: After the series of exploits in Vyper, arbitrageurs rushed to eliminate the price discrepancy of the decoupled assets in the Curve pool. A total of 7,187 ETH was paid to the proposers. During the turmoil, a single transaction paid 570 ETH to ensure the inclusion of a trade arbitrage between Alchemix ETH and Frax ETH, marking the second highest MEV expenditure in Ethereum history.

The highest single MEV payment transaction originated from the white-hat hacker c 0 ffeebabe.eth to Beaverbuild, as they were able to exploit the vulnerability discovered in the contract and returned the funds before the vulnerability was exploited, resulting in a profit of up to 678 ETH. Beaverbuild forwarded this MEV to the block proposer to win the bid.

2. Relay Situation

MEV-Boost introduced the role of trusted relays between builders and proposers, responsible for validating blocks and hosting block bodies. Anyone can run a relay, and proposers can register with any number of relays they trust. To help guide a diverse and healthy relay market in preparation for the merge, Flashbots open-sourced our relay under the LGPL Copy-left license one month in advance. Blocknative followed suit and open-sourced its implementation as well.

As Ethereum transitions to proof-of-stake on September 15th, validators can connect to seven different relays, which receive bids from 27 unique block builders. To exclude Flashbots relays from this, we deliberately avoided setting it as the default value in MEV-Boost.

(1) Concerns about the Review System

The rapid adoption of MEV-Boost still exceeded our efforts to foster a diverse relay market. One month prior to the merge, OFAC added the Tornado Cash contract addresses to the sanction list. This resulted in many relays, including Flashbots, choosing not to accept blocks containing these transactions. Due to the architecture of MEV-Boost, there is complete separation between block builders and proposers. Validators must blindly sign the blocks they propose without being able to add any further transactions and bypass this review.

Flashbots relays are the only permissionless relays in the merge, allowing any builder to submit bids. Relayooor is the second permissionless relay and the first uncensored relay, which began operating on October 26th. Even so, Flashbots relays were the most popular in the initial months, reaching their peak on November 11th, relaying 69% of all new Ethereum blocks. On November 21st, the percentage of blocks from all review relays reached a historical high, accounting for 79% of all new Ethereum blocks.

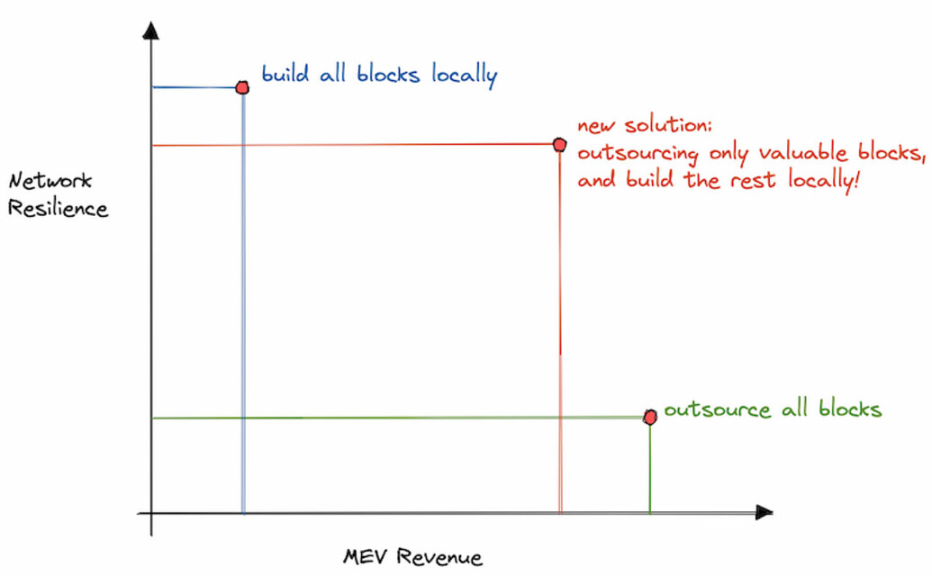

On November 22, we released "The Cost of Resilience". If the bidding for MEV-Boost is lower than the minimum bid, this post encourages validators to propose locally built blocks using the newly added flag. By using this feature, validators will no longer risk missing out on high-value MEV-Boost blocks, while still being able to maintain network resilience on Ethereum by proposing locally built blocks unrelated to content during low MEV periods.

From "The Cost of Resilience: Balancing Network Resilience and Minimum Bid-determined MEV Revenue"

On November 30, two new permissionless and content-agnostic relays, Agnostic Relay and ultrasound relay, were announced. To support their initial growth, Flashbots builders started sending blocks to them in the following week. Additionally, we also released technical guides and knowledge repositories on operating MEV-Boost-Relay at scale, to help people efficiently run relay infrastructure. Aestus began operating in December, serving as the fourth content-agnostic and permissionless relay, bringing the total number of relays to 11.

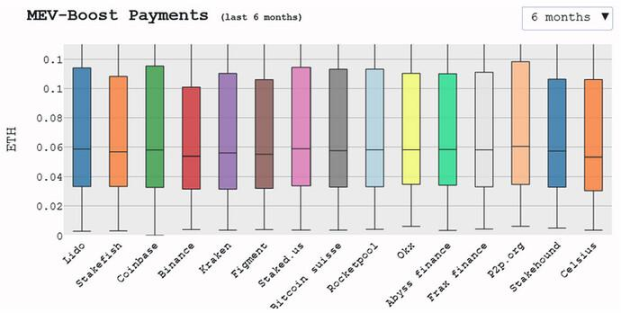

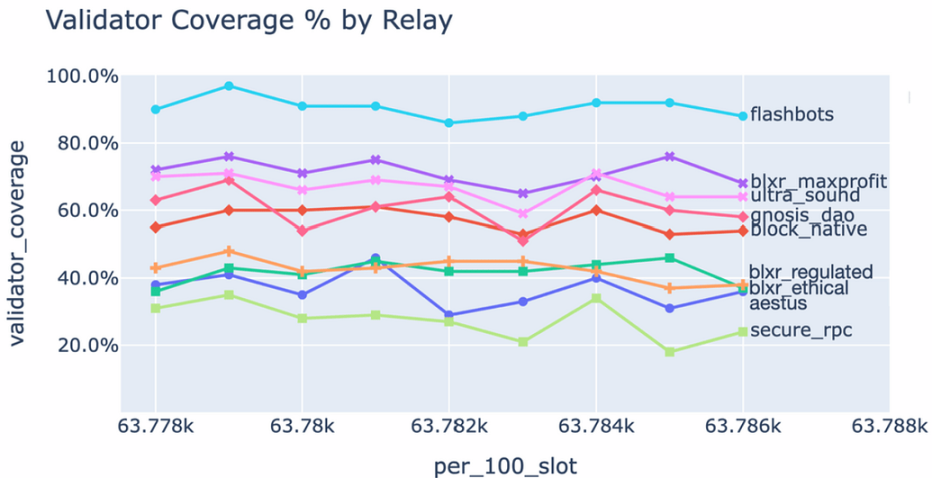

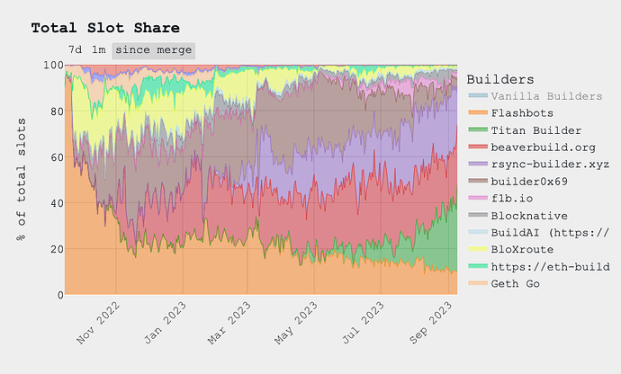

(2) Diversification and stability in the relay market

Although Flashbots relays are still the favorite choice for validators to register, there has been a significant diversification of slot shares in the past six months. In April, both Agnostic relays and Ultrasonic relays grew to the same slot share level as Flashbots relays. Currently, Supersonic relays and BloXroute are in the lead, although the top six relays account for 90% of the market share, with no single relay exceeding 25%.

From API relay data: Validator coverage of relays, snapshot between slot 6377800 and 6378800

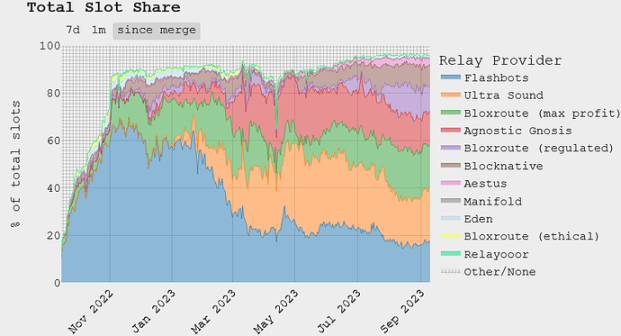

From mevboost.pics: Total slots shared by relays since the merge

In April, the percentage of blocks from review relays dropped to a low point of 17%. Since then, this trend has increased and is now close to 30%. It is worth noting that less than 2% of merged blocks contain one or more transactions interacting with sanctioned addresses. Due to the rarity of these transactions, the majority of blocks from reviewing entities actually do not delay any unconfirmed transactions from being included on the chain. Furthermore, since these transactions do not rely on timely inclusion, they are not at risk of failing due to increased latency.

(3) Reducing latency through optimistic relaying

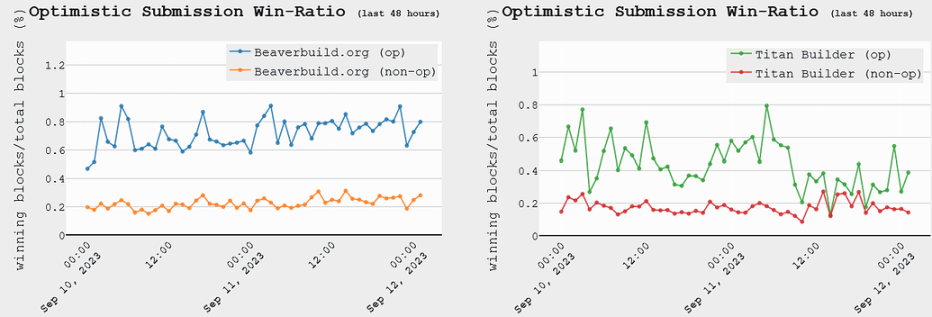

In order to reduce the latency during block propagation, Ultrasonic relays introduced the concept of optimistic relaying. In optimistic relaying, blocks are immediately forwarded to the proposers without being simulated by the relays to ensure their validity. This saves about 100 milliseconds of relay time and allows builders to construct blocks with higher rewards, giving the relays an advantage in competition. To ensure builders act sincerely, they must provide collateral to the relays.

This allows builders to adjust more flexibly at the end of the slot. The graph below shows that the winning rate of bids submitted by Beaverbuild and Titan Builder optimistically is nearly three times that of normal bids. The optimistic relay was activated by the ultrasound relay on March 17th and remains the only relay to effectively utilize this function.

From mevboost.pics: Bid success rate divided by submission type for Beaverbuild and Titan Builder

(4) Relay Exploits on April 2nd

On April 2nd, malicious proposers exploited vulnerabilities in mev-boost-relay to manipulate the ultrasound relay and steal approximately $20 million from multiple sandwich robots. The malicious proposers received blocks from the relay, lured the sandwich makers to open the sandwiches they created, and sandwiched their transactions in the middle. This vulnerability allowed proposers to send invalid headers to the relay to ensure their victory in the block race.

The vulnerability was fixed on the same day, but in the following days, the number of network forks increased. More information about ambiguous attacks, where malicious proposers double-sign headers in an attempt to uncover blind spots in builder blocks, can be found in ambiguous attacks in mev-boost and ePBS, as well as in time, periods, and sequential events in Ethereum's proof-of-stake. This incident also sparked discussions among MEV-Boost relay operators about customer diversity.

3. Evolution of Market Builders

After the merger, Flashbots builders initially won 95% of blocks from MEV-Boost. However, block construction diversified more quickly compared to the relay market. Just a week later, with the addition of BloXroute, the proportion of Flashbots builders dropped below 60%, occupying 25%, while other early adopters (such as Blocknative and builder 0x 69) began to win blocks. In November, we open-sourced the block builder and saw more builders go live.

The intervention of Beaverbuild in January further decentralized the situation, with no single entity producing more than 30% of blocks currently. However, Beaverbuild, with its unique position as a searcher-builder, is able to gain exclusive high MEV arbitrage flow, giving them a significant competitive advantage. Vertical integration allows Beaverbuild to produce 40-50% of blocks in a short period of market volatility, far surpassing other builders and temporarily concentrating the market.

Afterwards, more competitive builders entered the market and gained a considerable market share, among which rsync was launched in March and Titan Builder was launched in May. Unlike the relay market, the builder market is driven by economic incentives. The competition remains fierce, with new players joining and strategies constantly improving to win the competition. As of the time of this report, the top 4 block builders accounted for 90% of the total market share.

From mevboost.pics: Builder slots sharing since the MEV-Boost merger

The current market has evolved into a complex game involving various strategic approaches to gain an advantage in competition, such as:

1) Seeker - Builder vertical integration: Given Ethereum's 12-second block time, seekers involved in off-chain high-frequency markets like Binance benefit from more control over transaction completion and inclusiveness. Therefore, it makes economic sense for seekers to also become builders. It is worth noting that CEX-DEX arbitrage constitutes a significant part of the seeker-builder strategy and heavily relies on off-chain capital acquisition.

2) On-chain data indicates that seekers often consider seeker-builders less trustworthy than neutral builders. Some seekers strategically avoid sending data to these entities to mitigate the risk of data leakage or censorship, especially when there may be competition on the same stream. With the emergence of multiple seeker-builders, seekers need to strategically consider which builder to bundle their packages with.

3) Strategic bidding: builder 0x69 is the first renowned builder that differs from solely bidding the total value of blocks. They sometimes adjust their bids by subsidizing blocks with their own funds to make them higher than the block value, and sometimes lower their bids for profit. By subsidizing blocks, they have a higher chance of winning seats, increasing market share, and attracting more private order flow. Today, this strategy is increasingly adopted by new entrants in the builder field.

4) Order flow sharing: With the rise of MEV-share and MEVBlocker order flow auctions, as well as Telegram Bot requiring private mempool settlement, developers face increasing pressure to quickly include transactions to optimize user experience. Due to the decentralized nature of the builder market, sharing order flow between builders has become a solution to accelerate inclusion time. This practice makes order flow tracking complex until more standardized solutions are developed.

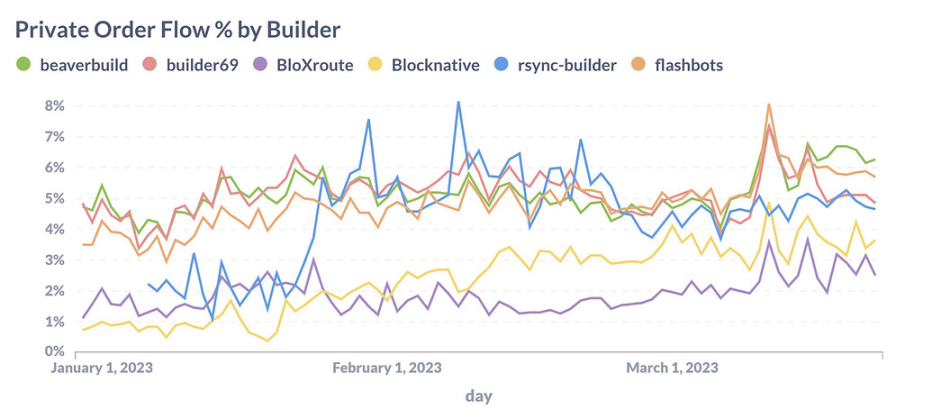

5) Private order flow acquisition: Acquiring private order flow containing MEV value is crucial for building competitive blockchains. Most well-known builders have adopted private order flows, either through their RPC endpoint products or exclusive transaction purchase flows from applications.

From Flashbots Internal: Percentage of transaction builders included in blocks not visible in the public mempool

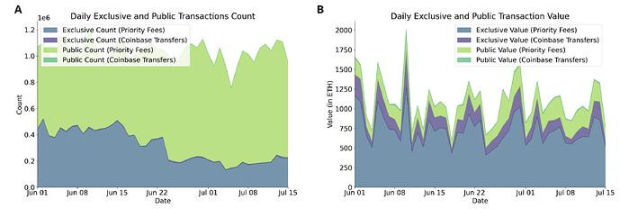

Empirical analysis of Market-Building Behavior Profile (BBP) provides a deeper analysis of the strategies used by builders. The study introduces a range of metrics to describe how builders construct blocks and act in MEV-Boost auctions, providing insights into their strategies and optimizations. The data shows that exclusive order flows accounted for approximately 25-35% of total transactions by builders from June to mid-July, but represented 80% of total value.

From Builder Behavior Profile (BBP) empirical analysis: Importance of exclusive order flows for block builders

One major issue with the current PBS architecture is still the centralization of builders and resistance to censorship. MEV-Boost does not produce this centralization of power, MEV does. MEV-Boost simply shifts the risk from validator sets to builders, who are easier to address.

4. Merger Searcher Profits

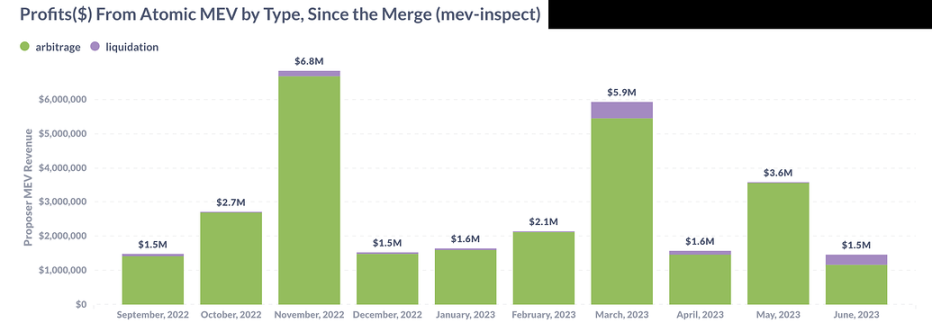

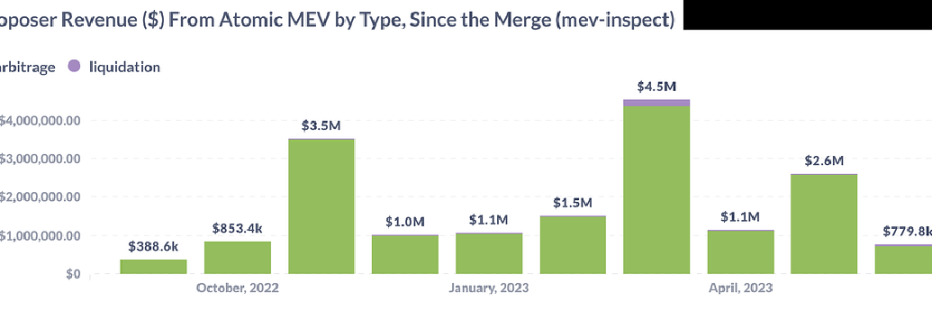

(1) Atomic MEV: Majority of profits paid to proposers

Using mev-inspect-py to identify atomic MEV, such as arbitrage and liquidation, we are able to quantify the monthly profits of atomic MEV hovering around $2 million and soaring to $4-6 million during periods of intense market volatility.

From mev-inspect-py: Profit breakdown of atomic MEV since the merger

We estimate that the total income for proposers benefiting from atomic MEV trades falls within the range of 1-4 million US dollars. This constitutes only 5-10% of the overall income for proposers within the same time frame. Please note that this is a conservative lower-bound estimate, limited by the scope of mev-inspect-py.

From mev-inspect-py: Income obtained by proposers from atomic MEV trades compared to total income

Before merging, searchers need to increase gas prices in order to prioritize transactions within a block. After merging, with the adoption of MEV-Boost, searchers can now receive additional tips through MEV payments in addition to standard gas fees to prioritize their bundles. The percentage of total MEV paid to proposers reflects interesting paradigm shifts before and after merging:

1) Before merging, the share of proposers in MEV income was on average less than 50%.

2) When MEV-Boost was first introduced, there was almost no competition between builders, resulting in a decrease in the profit share forwarded to proposers, followed by an upward trend.

3) Starting from 2023, as more builders entered the field, the share forwarded to proposers stabilized at over 50%. Proposers increasingly obtained the majority of atomic MEV profits, sometimes even reaching 80-95%.

From mev-inspect-py: Percentage of atomic MEV profits paid to proposers before and after merging

(1) Non-atomic MEV: Higher income, higher profit margin

Searchers can engage in cross-market arbitrage involving DeFi and CeFi platforms... Tracking these profits has become particularly challenging as one of the transactions exists off-chain. The conclusion from the story of two arb's:

"... Comparison of Atomic Strategies and CeFI-DeFi Arbitrage in the first quarter of 2023. CeFI-DeFi generated a revenue of 37.8 million US dollars in the first quarter of 2023, while the revenue of Atomic Strategy was 25 million US dollars. 91-99% of the income from Atomic Arbitrage is paid to validators for inclusion, while only 37-77% of the income from CeFi-DeFi is paid to validators for inclusion."

This helps us estimate that compared to Atomic MEV, non-Atomic MEV flows contribute a similar amount of revenue to proposers; while searchers can achieve higher profit margins from the total revenue.

5. Final Conclusion

(1) The Future of the Public Broadcasting Corporation

MEV-Boost was developed as a temporary solution for Ethereum PoS until research on PBS within the protocol matures as part of the Ethereum roadmap. Relays were initially seen as temporary components in the current protocol outside of the PBS structure, but are likely to continue to play a role, even within PBS. There is still work to be done in relay diversification, and we are committed to encouraging an open, permissionless, and transparent MEV market by open-sourcing our work, sharing our experiences, and participating in discussions.

To help support research, development, and operation of PBS on Ethereum now and in the future, the MEV-Boost community has proposed the PBS Guild. The PBS Guild is a non-commercial ecosystem R&D funding tool to support the development of the PBS ecosystem. It aims to address short-term, medium-term, and long-term research, development, and operational challenges for PBS and enable power decentralization. The initial stage aims to raise $1 million for independent relays, research, data transparency, and PBS education.

(2) Data Transparency

As the MEV supply chain evolves into a complex network of suppliers, tracking the entire lifecycle of order flows throughout the stack becomes challenging. While MEV-Boost's open relay data API helps understand the final steps before on-chain settlement, tracking the initial entry points of orders remains elusive.

Flashbots remains committed to providing transparency to the MEV ecosystem and research data to contributors and collaborators. The recently released Mempool Dumpster provides historical mempool transaction data aggregated from five different node providers. It aims to provide free and easy access to data for any community research or developer building.

(3) Future Outlook

The transition of Ethereum to Proof of Stake, coupled with the rise of MEV-Boost, fundamentally reshapes the dynamics of the transaction supply chain. While this achievement is significant and worth celebrating, the centralized power of MEV continues to pose inherent challenges to the neutrality and decentralization of blockchain. The future path requires research, fierce debates, and innovation to ensure a deliberate response to these concentration effects. Ethereum's journey has always been a community-driven evolution. As we venture into the next chapter, let us harness our collective energy to uphold the spirit that brought us here. The future is exciting, and together we will embrace the challenges."