Inventory of current early LSDFi potential projects

Original Author: Yuuki, LD Capital

Foreword:

Foreword:

text:

The LSD track has been repeatedly hyped, and the market has already had a high degree of understanding and corresponding attention to the track. There is no doubt about the certainty of the future development of the LSD track, but the mainstream targets are facing weaker marginal changes. The high certainty makes the market almost non-existent in the effective expectation gap and provides high-odds trading opportunities. At this time, due to the continuous expansion of the scale of the underlying LST, the interest-bearing asset, the new LSDFi protocol built on this asset will become the α of the entire LSD track.

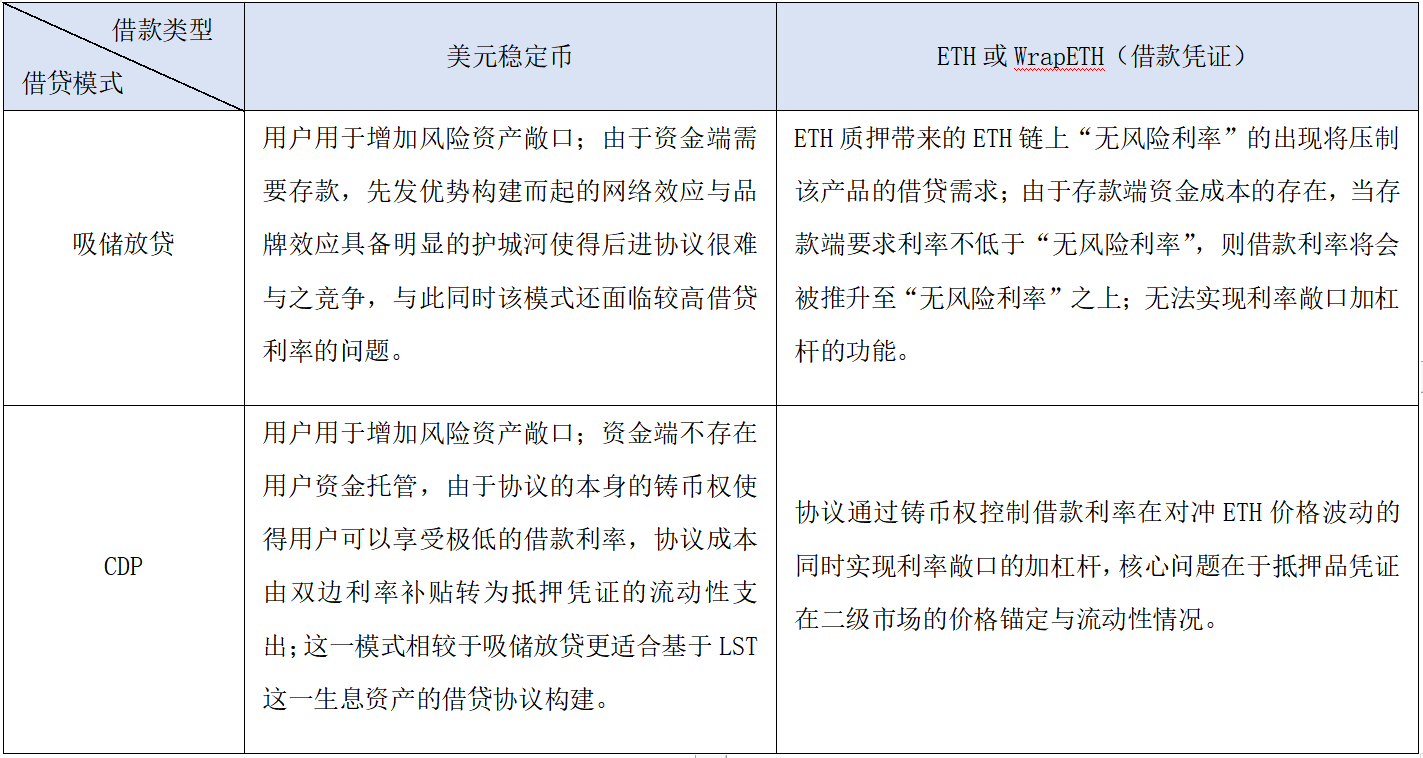

Lending agreements are usually divided into two types. One is the deposit-absorbing and lending model (such as AAVE and Compound), but this model requires user deposits on the capital side, and the network effect and brand effect created by the first-mover advantage have obvious moats. It is difficult for the protocol to compete, and at the same time the model also faces the problem of high borrowing rates. The other is the CDP coinage model (such as Dai). This model does not have user fund custody at the capital end. Due to the protocol’s own coinage rights, users can enjoy extremely low borrowing rates, and the cost of the protocol is changed from bilateral interest rate subsidies to Liquidity expenditure of mortgage certificates; this model is more suitable for the construction of lending agreements based on LST, an interest-bearing asset, than deposit-absorbing and lending, especially the leverage based on interest rate exposure.

Source: LD Capital

Source: LD Capital

first level title

Type 1: CDP USD stablecoin protocol with LST as collateral

secondary title

product description:

Features:

Features:

Economic Model:

Economic Model:

In terms of the token economic model, Prisma Finance introduces the ve model. veToken will obtain the governance rights of the agreement to determine the distribution of tokens in different lending pools, agreement fee rates, pool parameters and LP mining yield, aiming to attract LSD agreement (The asset issuer) locks the protocol tokens with LP, forming interest binding and reducing secondary market selling pressure.

secondary title

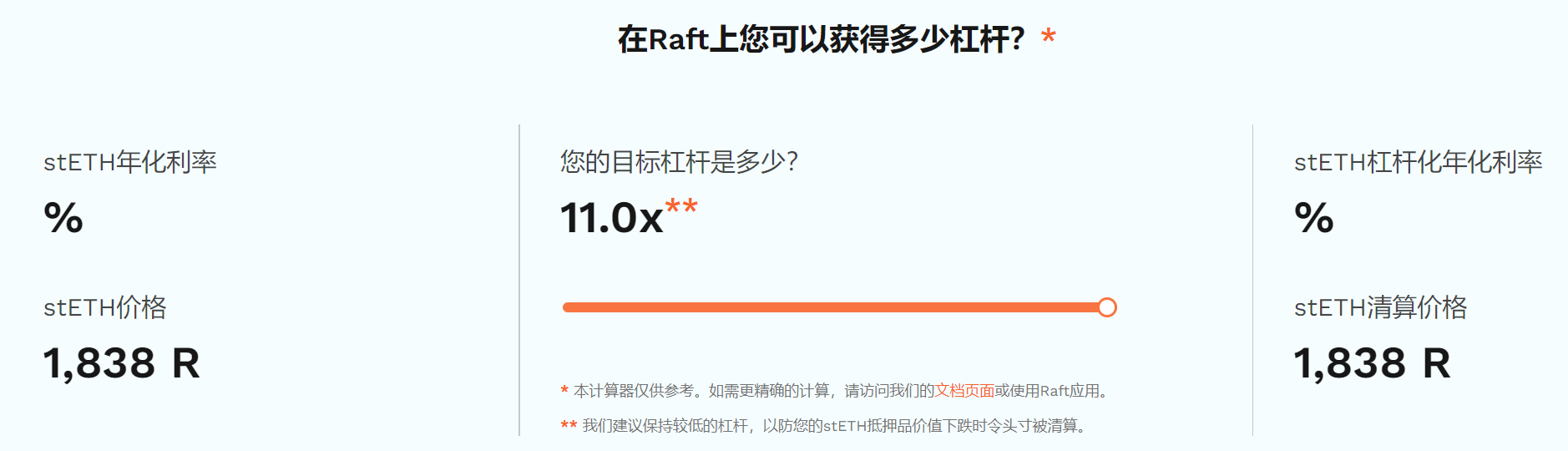

image description

source:https://www.raft.fi/,LD Capital

Features:

image description

source:https://www.raft.fi/,LD Capital

Economic Model:Economic Model:

unpublished

secondary title

product description:

Features:

Features:

Compared with Liquidity, Gravita also has a lower borrowing rate in addition to supporting LST assets; users need to pay a one-time borrowing fee of 0.5% in advance when borrowing in Gravita. If the repayment is within 6 months, Gravita will pay according to the loan period To refund the borrowing fee, the user will be charged at least 1 week's borrowing fee.

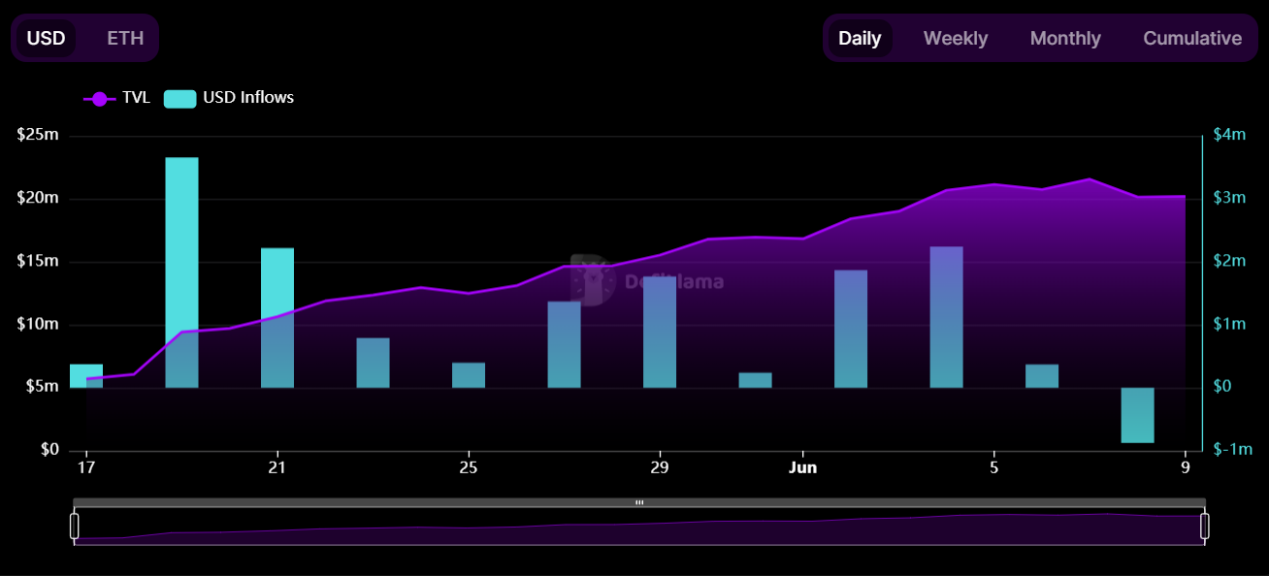

Source: Defillama, LD Capital

Economic Model: Unpublished

secondary title

product description:

Features:

Features:

first level title

The second type: CDP WrapETH protocol with LST as collateral

secondary title

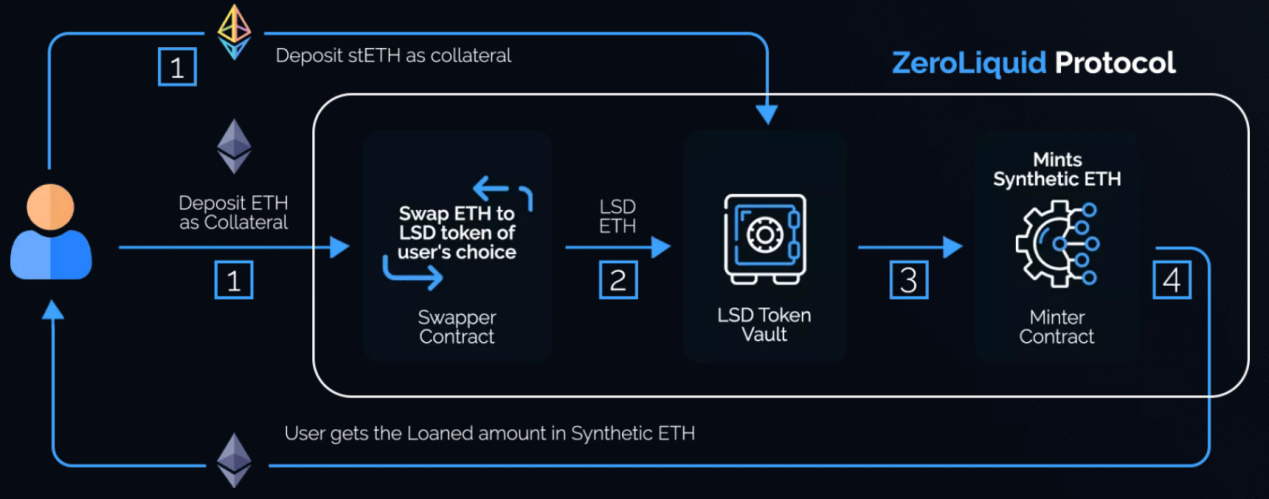

product description:

ZeroLiquid is currently in the testnet stage, allowing users to mortgage LST to mint ZETH (when users deposit ETH, ZeroLiquid will convert it into LST, the initial LTV is 50%), ZETH is a loan certificate for price anchoring ETH, because it has the same Price fluctuations in the same direction, so without considering the risk of the underlying LST assets coming from the LSD agreement (hacking, a large amount of capital fines, etc.), ZeroLiquid can achieve no liquidation, hedge the risk of price fluctuations, and do long ETH pledged interest rate exposure mouth. ZeroLiquid initially plans to charge 8% of the LST rate of return as protocol income, and the subsequent ratio can be adjusted through governance.

image description

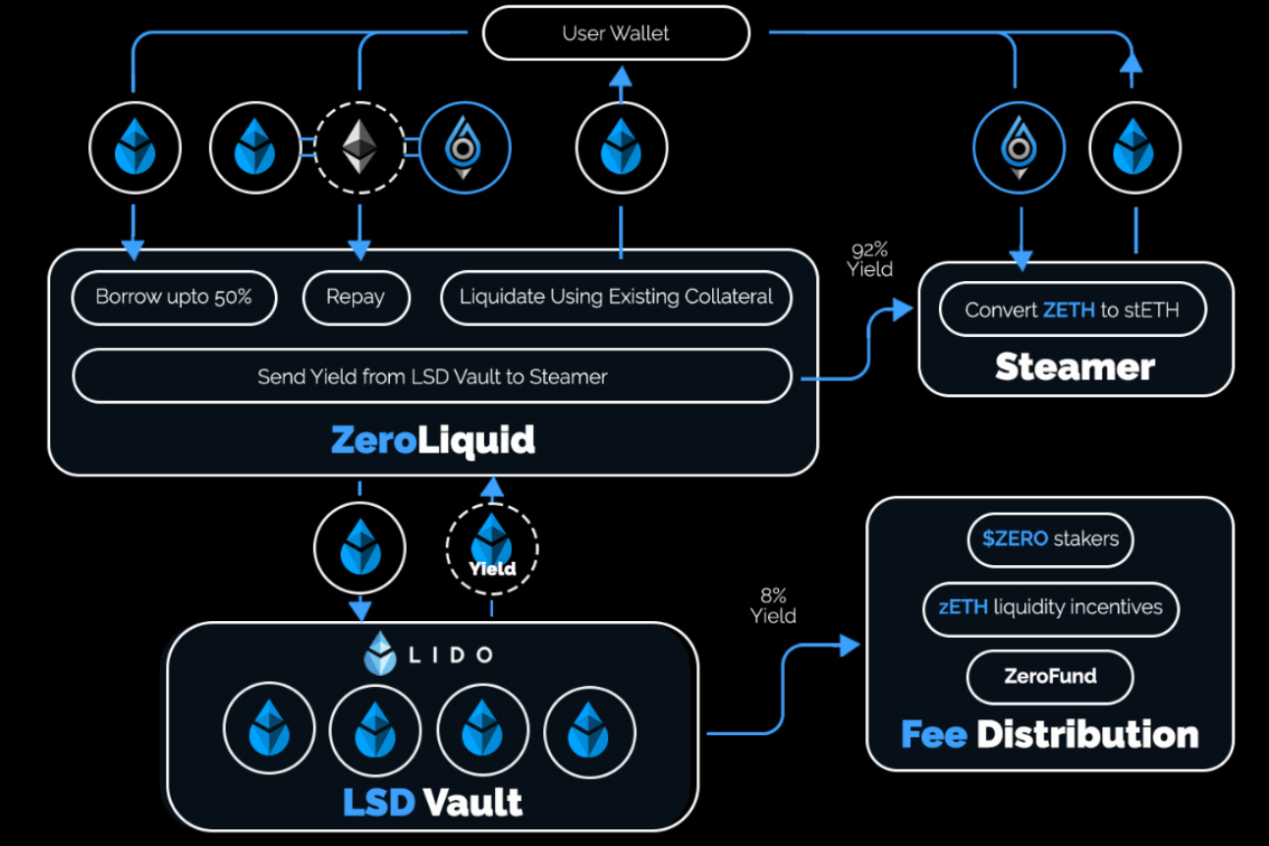

ZeroLiquid's current problem lies in how low LTV, high protocol pumping and ZETH are anchored; among them, LTV and protocol pumping can be adjusted through governance, and the main problem at present focuses on how ZETH is anchored. In ZeroLiquid's economic model, the liquidity incentive cost accounts for 20% of the total tokens (low), which requires it to have a good redemption mechanism to maintain the stability of the ZETH/ETH exchange rate.

image description

Economic Model:

Economic Model:

image description

Source: zeroliquid.gitbook.io, LD Capital

secondary title

product description:

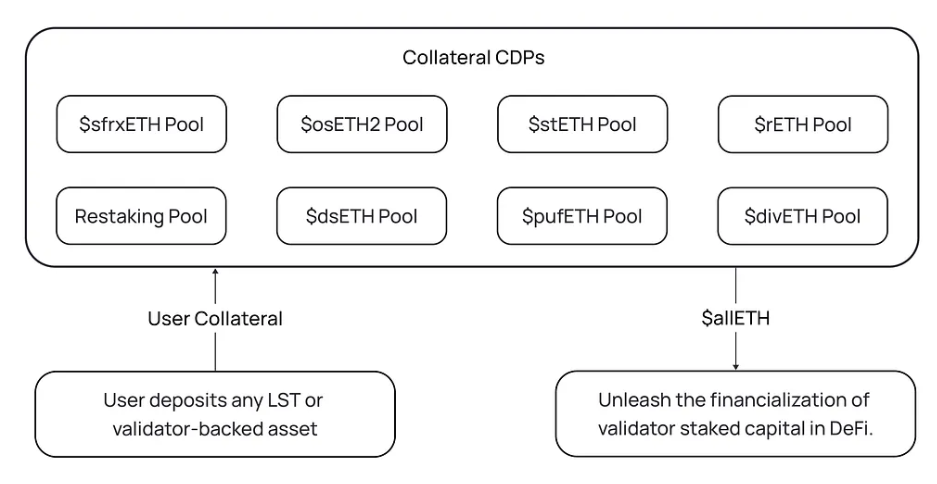

Ion Protocol supports a variety of collaterals, including LSTs, LST LP Positions, Staked LST LP Positions, EigenLayer Validator/LST/LST LP Restaking Positions, and LST Index Products. At the same time, Ion Protocol intends to customize the risk model of this agreement according to the inherent risk-return structure of different collaterals, and guide user deposits by adjusting the LTV or borrowing rate of different collaterals, so as to ensure the over-collateralization and anchor of allETH while improving the efficiency of funds as much as possible. Certainly.

image description