Arthur Hayes: Be patient, the bull market will start in the fourth quarter

Author: Arthur Hayes

Author: Arthur Hayes

Original compilation: GaryMa, Wu said blockchain (note: the article has been deleted)

Patience is essential in financial markets.

Since the beginning of the US banking crisis this year, I and many others have been saying: the US and global fiat currency banking system will be rescued by a new round of central bank money printing (which will push up risky asset prices). However, after bitcoin and gold completed their initial gains, these hard money assets have pulled back a bit.

In the case of Bitcoin, both spot and derivatives saw lower volatility and trading volumes. Some are starting to wonder why Bitcoin hasn't continued to rise if we are truly in a banking crisis. Likewise, why the Fed didn't start cutting rates and why the US didn't start yield curve control.

My answer to those skeptics: be patient. Nothing goes up or down in a straight line, we zigzag. Remember: the destination is known, but the path is unknown.

Money printing, yield curve control, bank failures, etc., are going to happen, starting in the US first and eventually spreading to all major fiat currency systems. The goal of this article is to explore why I believe a real Bitcoin bull run will begin in late Q3 and early Q4 of this year. Until then, calm down. Take a vacation and enjoy nature and being with friends and family. Because come this fall, you better buckle up and get ready for TO THE MOON.

The goal of this article is to give readers a clear roadmap of the evolution of fiat liquidity and what to expect in the next few months. Once we are comfortable with the expansion of USD and fiat liquidity into the end of the year, we can fully focus on which technical aspects of certain coins are most exciting. When you combine the "money printing press humming" with truly innovative technology, your rewards far outweigh the cost of effort put into it. This is the goal we always pursue.

first level title

premise

Bureaucrats in charge of central banks and global monetary policy believe they can rule a market of more than 8 billion people. Their arrogance shows in the way they talk about all certainties based on economic theory developed by academia over the past few hundred years. But whether they want to believe it or not, they haven't solved the money version of the three-body problem."when"Debt and Production Output"When the equation is out of balance, the economic"law

will crash. This is similar to the way water changes states at seemingly random temperatures. We can only learn about water behavior through hindsight and experimentation, not theoretical speculation in an ivory tower. Our monetary rulers refuse to actually use empirical data to guide the way they adjust policy, insisting instead that the theory taught by their respected professors is correct, regardless of objective outcomes.

In this article, I dig into why, contrary to common monetary theory, raising interest rates would cause the quantity of money and inflation to rise, not fall, due to current debt-to-production-output conditions. This will lead to increased inflation no matter which path the Fed chooses, be it hikes or cuts, and trigger a general withdrawal from the parasitic fiat currency financial system.

As true believers in Satoshi Nakamoto, we want to be as careful as possible when trading on the timing of this mass withdrawal. I'm looking to make good money in fiat until I have to sell my dollars and go all in on bitcoin. Of course, I also displayed a kind of arrogance myself, because I believed that I could predict the best time to exit without self-destructing. But what can I say? At the end of the day, we're all flawed human beings, but at least we have to try to understand what the future might look like.

With that out of the way, let's move on to some (disputed) factual statements.

Every major fiat currency regime faces the same problems no matter where they are in the economic system. Namely, they are all heavily indebted, have shrinking working-age populations, and have banking systems whose assets are dominated by low-yielding government and corporate bonds/loans. Rising global inflation has rendered the global fiat currency banking system functionally insolvent.

The U.S. faces these problems more than any other country, and is in the toughest position, because of its role as the world's largest economy and reserve currency issuer.

Groupthink among central bankers does exist because all senior officials and employees study at the same "elite" universities that teach different versions of the same economic theory.

So whatever the Fed does, every other central bank will eventually follow.

Keeping this in mind, I want to focus on the situation in the United States. Let's take a quick look at the various characters in this tragedy.

The Fed exerts influence through its ability to print money and hold assets on its balance sheet.

The U.S. Treasury raises money to influence the situation by issuing debt to finance the federal government.

The U.S. banking system exerts influence by taking deposits and lending them out to create credit and finance businesses and the government. The solvency of the banking system is ultimately backed by the Federal Reserve and the US Treasury with printed money or taxpayer money.

The U.S. federal government exerts influence through taxation and its ability to spend on various government programs.

Private businesses and individuals wield influence through their decisions about where and how to save money and whether to borrow from the banking system.

At the end of this article, I hope to distill the major decisions of each stakeholder into a framework that shows how we arrived at a situation where there is little room for individual players to maneuver. This lack of flexibility allows us to predict with a high degree of confidence how they will respond to current US currency problems. Finally, because the financial crisis is still closely tied to the cycle of agricultural harvests, we can predict with a fair degree of certainty that the market will wake up and realize that something is bad at exactly the scheduled time in September or October of this year.

first level title

Please bear with me as I still have some groundwork before we get into the details. I'll lay out some underlying assumptions that I believe will occur or intensify come fall.

secondary title

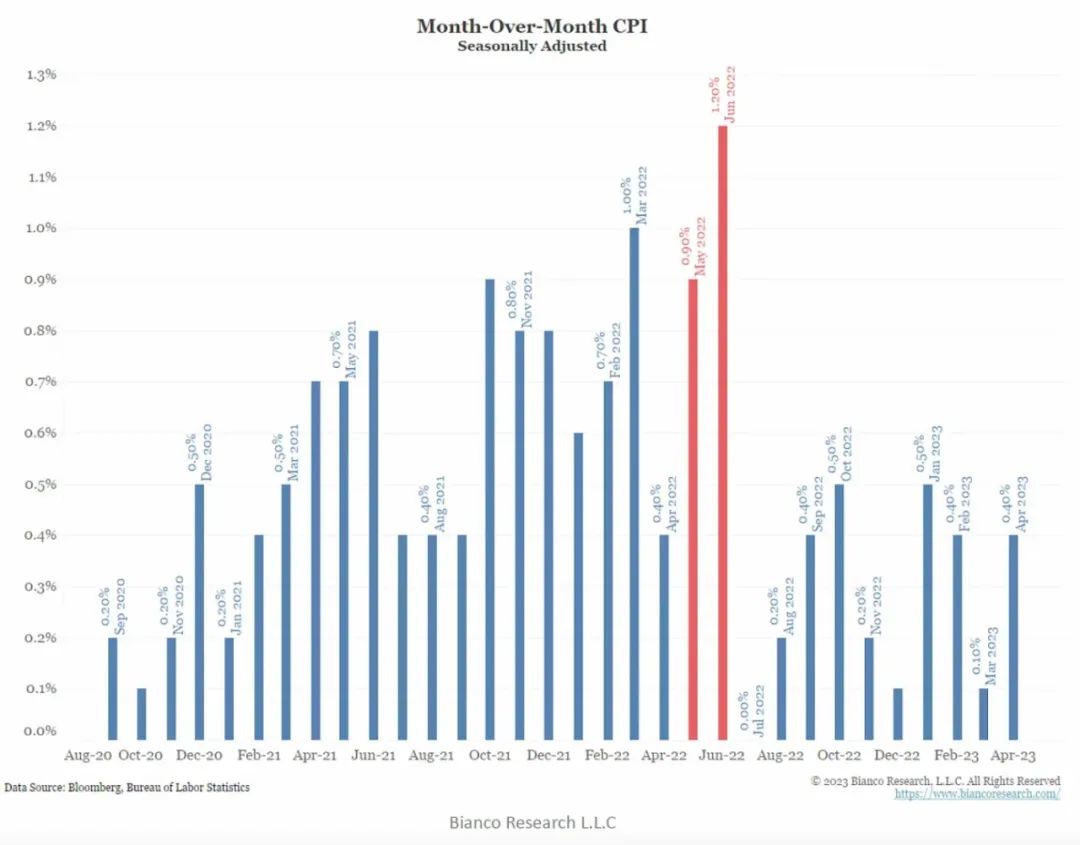

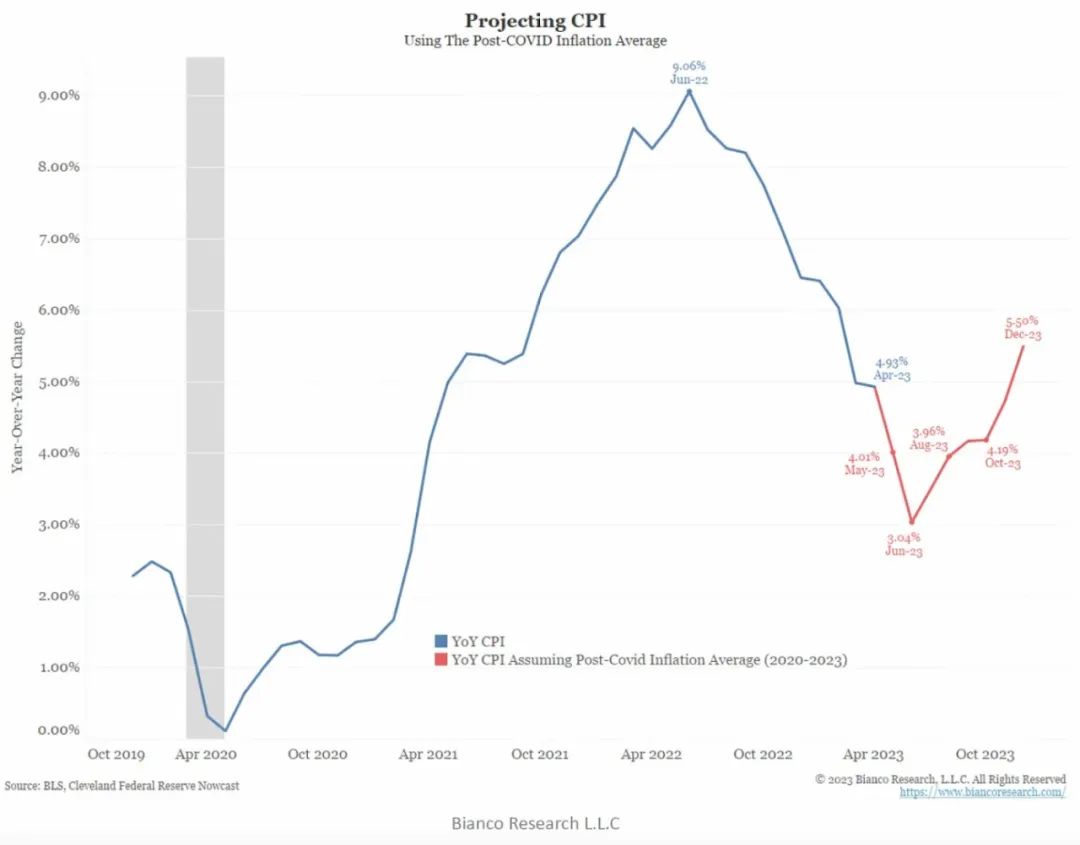

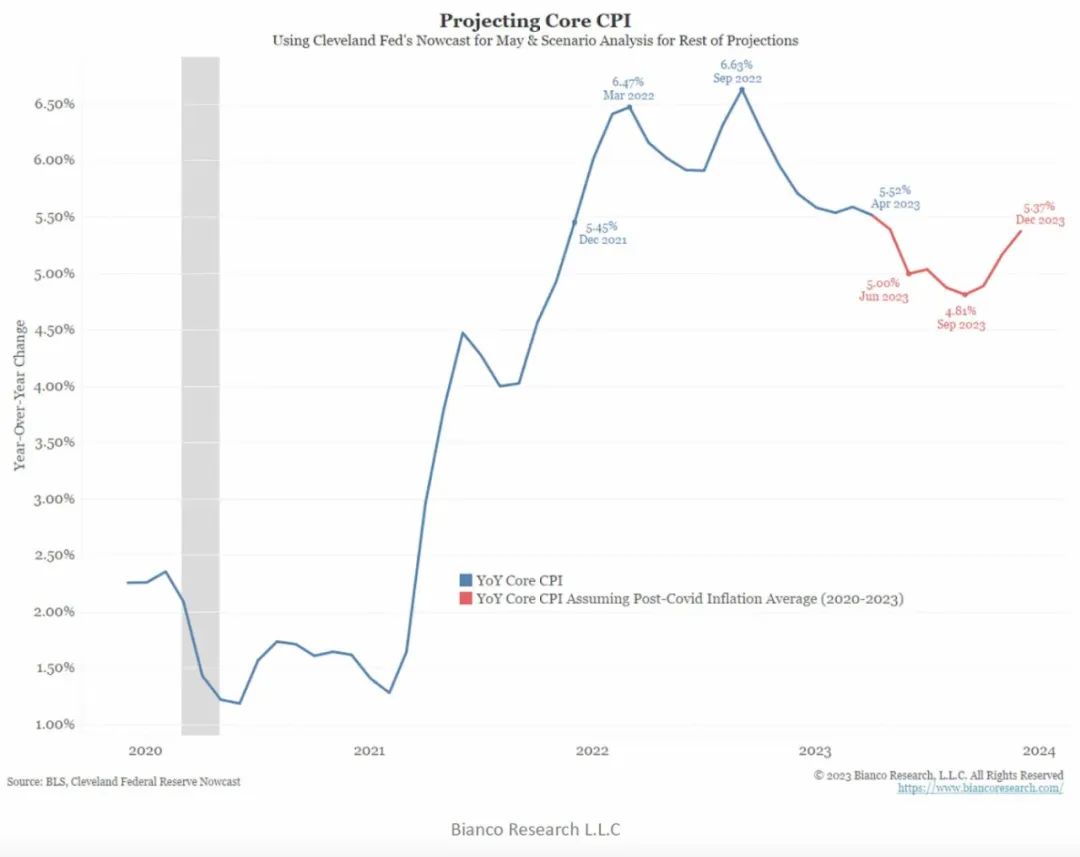

Inflation will hit local lows this summer and re-accelerate by year-end

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

Don't get bogged down in why these inflation measures don't match the price movements you and your household are actually feeling. This is not an intellectually honest exercise - rather, we just want to understand the indicators that influence how the Fed adjusts policy rates.

secondary title

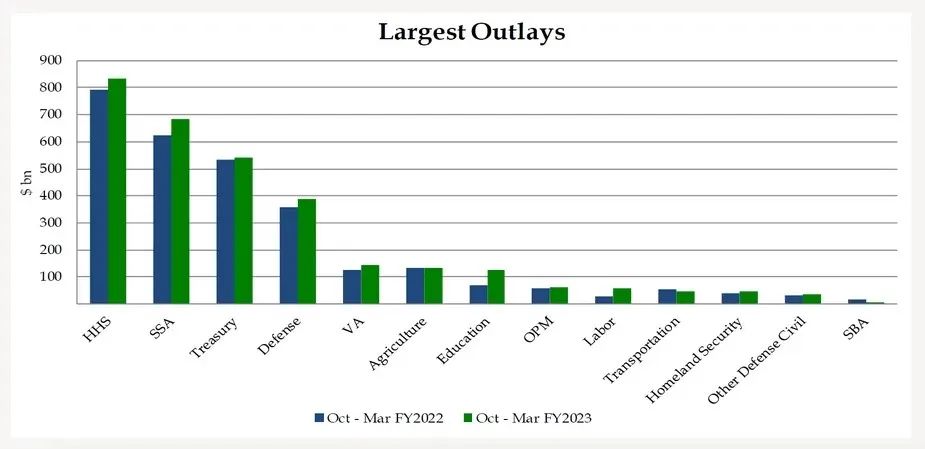

US federal government can't reduce deficit due to Social Security spending

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

HHS (Department of Health and Human Services) + SSA (Social Security Administration) = Old Age and Medicare Benefits

Treasury = interest paid on outstanding debt

Defense = War

The end result is that the market has to absorb huge amounts of debt on an ongoing basis.

secondary title

foreign participants

As I've written in several articles this year, foreign players turned net sellers of U.S. Treasuries (UST) for a number of reasons, here are a few:

Property rights depend on whether you are friend or foe of American politicians. We have seen the rule of law give way to national interests, with the United States freezing Russian state assets in the Western financial system. So, as a foreign holder of U.S. Treasuries, you can't be sure that you'll be allowed to access your wealth when you need it.

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

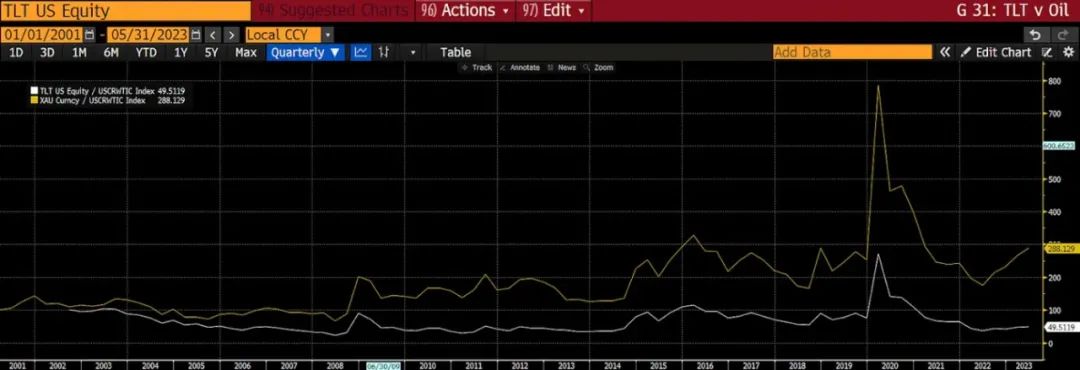

Over the past two decades, U.S. Treasuries have lost purchasing power when it comes to energy. As far as energy is concerned, gold has maintained its purchasing power. Therefore, in a world of energy shortages, it is better to save gold on the margin than US Treasuries.

TLT ETF (20+Y U.S. Treasuries) divided by WTI crude oil spot price (white line)

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

The total return performance of long-term US Treasuries has underperformed the price of oil by 50%. However, since 2002, gold has outperformed oil prices by 190%.

In short: if there is a lot of debt to sell, foreigners cannot be expected to buy it.

secondary title

Private Businesses and Individuals in the United States - Private Sector

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

That stimulus money was deposited into the US banking system, and since then the private sector has been spending its free money on whatever they like.

The U.S. private sector is happy to keep money in banks when deposits, money market funds, and short-term U.S. Treasuries yield essentially 0%. As a result, deposits in the banking system exploded. But when the Fed decided to fight inflation by raising interest rates faster, the U.S. private sector suddenly faced a choice:

Continue to earn essentially 0% in the bank.

Or, open their mobile banking app and buy a money market fund or U.S. Treasuries yielding up to 10x in minutes.

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

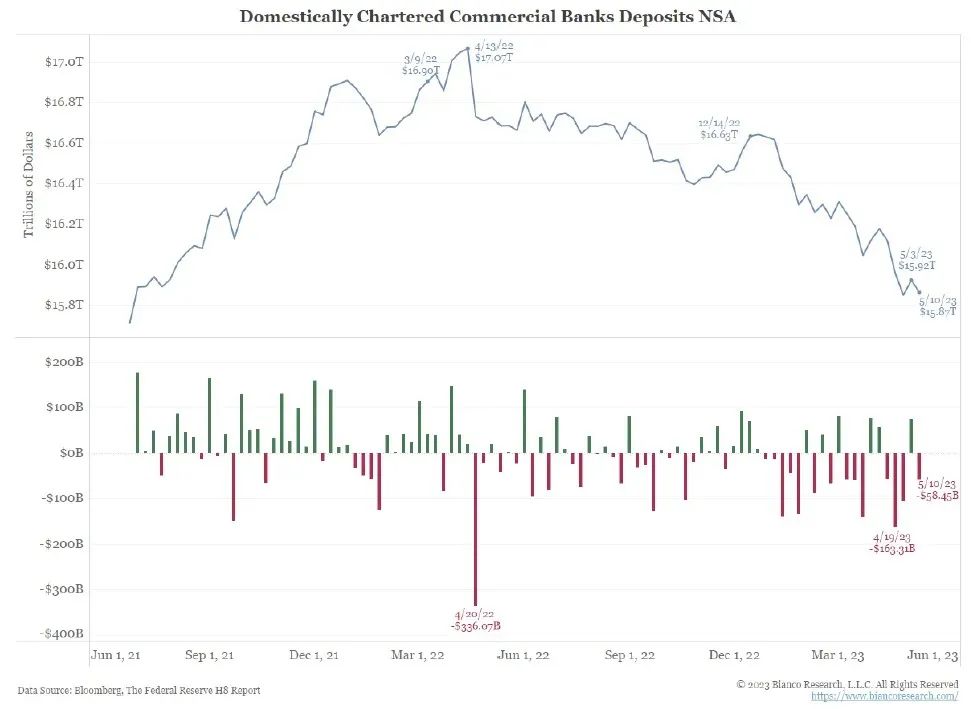

Since last year, more than $1 trillion has been withdrawn from the US banking system.

The big question going forward is, will this drain of funds continue? Will businesses and individuals continue to move money from 0% bank accounts to money market funds that yield 5% or 6%?

Logic tells us that the answer is obvious, "Of course it will". If they could increase their interest income 10x by spending just a few minutes on their smartphone, why wouldn't they? The U.S. private sector will continue to draw money from the U.S. banking system until banks offer competitive rates that match at least the federal funds rate.

The next question is, if the US Treasury is selling debt, what type of debt, if any, does the public want to buy? This question is also easy to answer.

Everyone feels the effects of inflation and therefore has a high preference for liquidity. Everyone wants immediate access to money because they don't know where inflation is going to go in the future, and given that inflation is already high, they want to buy things now so they don't get more expensive in the future. If the US Treasury offered you a one-year note at 5% or a 30-year bond at 3% because the yield curve is inverted, which would you choose?

first level title

the fed

the fed

I have already mentioned similar themes above, but allow me to expand on the same in a more vivid and visual way.

Imagine there are two politicians.

Oprah Winfrey wants everyone to be happy and live their best lives. She made sure everyone had food on the table, a car in the garage full of gas, and the best medical care until they died. She also said she would not raise taxes to pay for the benefits. She will borrow money from the rest of the world to make it happen, and she believes it can be done because the US is the global reserve currency issuer.

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

Imagine you're in the later stages of an empire where income inequality has skyrocketed. Mathematically, most people will always earn below average, so who wins? Oprah Winfrey wins every time. A free item paid for by someone else by using a money printing machine always wins.

Unless long-term debt markets or hyperinflation are to blame, there is no reason why platforms based on "free goods" should not be adopted. This means that from here on out, I don't expect to see any substantial change in the spending habits of the US federal government. As for this analysis, trillions of dollars will continue to be borrowed each year to pay for these benefits.

first level title

US banking system

In short, the US banking system, as well as other major banking systems, is in trouble. I'll quickly review why.

Assets in the banking system swelled due to stimulus provided by governments around the world. Banks are required to lend these deposits to governments and corporations at very low interest rates. This worked for a while because banks had 0% interest on deposits, but they were lending to others at 2-3% through longer term loans. But then, inflation came along and all the major central banks (with the Fed being the most aggressive) raised their short-term policy rates significantly higher than yields on government bonds, mortgages, corporate loans, etc. Depositors can now earn higher yields by buying money market funds that invest in the Fed's reverse repurchase agreements (RRPs) or short-term U.S. Treasuries. As a result, depositors began withdrawing funds from banks to obtain better yields. Banks cannot compete with the government as this would destroy their profitability - imagine a bank with a 3% loan rate but a 5% deposit rate. One day, the bank will go bankrupt. As a result, bank shareholders started selling bank stocks as they realized that these banks were mathematically unprofitable. This led to a self-fulfilling prophecy, with some banks' solvency called into question as their share prices plummeted.

In my recent interview at Bitcoin Miami, I asked Zoltan Pozar what he thought of the US banking system. He replied that the system was fundamentally sound, with only a few rotten apples. That's the same statement made by various Fed chairs and U.S. Treasury Secretary Janet Yellen. I strongly disagree.

Bank of America now faces two choices:

Option 1: Sell assets (US Treasuries, mortgages, auto loans, commercial real estate loans, etc.) at huge losses, then raise deposit rates to lure customers back to the bank.

This option means acknowledging an implied loss on the balance sheet, but guarantees that the bank cannot sustain profitability. The yield curve is inverted, which means banks pay higher interest rates on short-term deposits and cannot take those deposits out to longer-term loans at higher rates.

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

Banks can't buy long-term government bonds because that would be a loss - very important!

The only things banks can buy are short-term government bonds, or park their money with the Federal Reserve (IORB) and earn slightly more interest than they pay on deposits. According to this strategy, it is difficult for banks to achieve a Net Interest Margin (NIM) of more than 0.5%.

This is basically what the Bank Term Funding Program (BTFP) does. I discussed this issue in detail in a previous article. Don't worry about whether the assets held by banks on their balance sheets qualify for the BTFP - the real problem is that banks cannot expand their deposit base and then use these deposits to buy long-term government bonds.

first level title

us treasury department

I know the media and markets are focused on when the US debt ceiling will be reached and whether the two parties will find a compromise to raise it. Ignore the circus - the debt ceiling will be raised (as it always has been, given the harsher alternative). And when it gets raised, around this summer, the US Treasury has some work to do.

secondary title

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

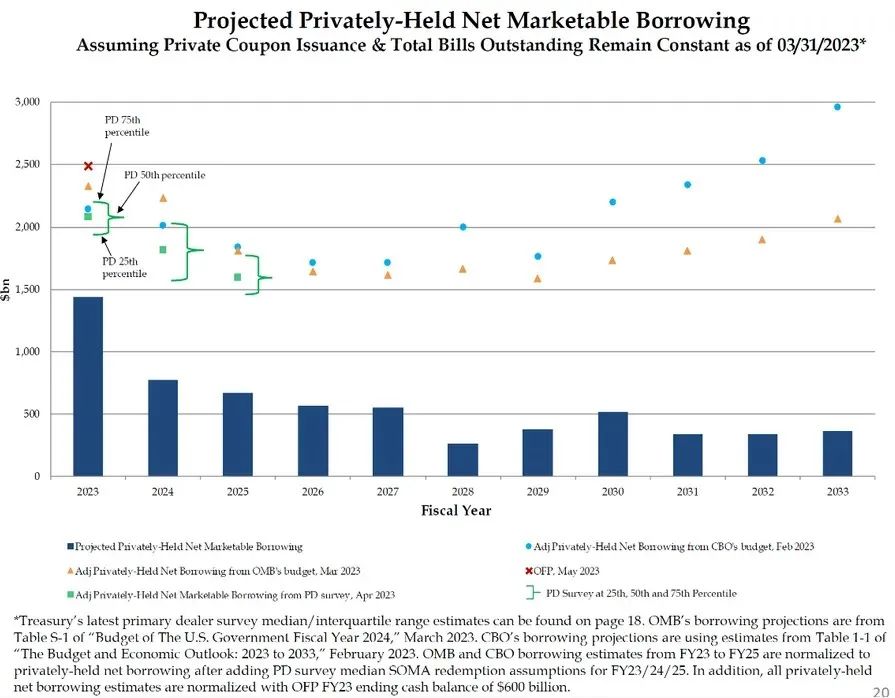

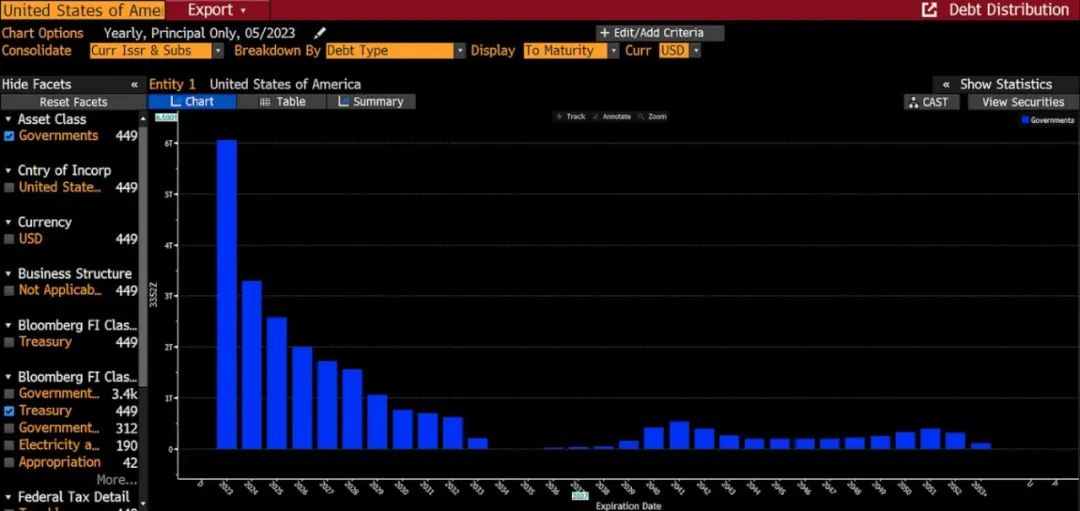

Between now and the end of 2024, about $9.3 trillion in debt needs to be rolled over. As you can see, the U.S. Treasury is unwilling or unable to issue most of its long-term debt and instead finances it with short-term debt. Oh oh! This is bad news because short-term rates are higher than long-term rates, which increases interest payments.

Let's see.

No major buyer is willing or able to buy long-dated U.S. Treasuries. So if the US Treasury tries to flood the market with trillions of dollars of long-term debt, the market will demand higher yields. Imagine if the 30-year yield rose from 3.5% to 7%, which would send bond prices plummeting, signaling the end of many financial institutions. That's because these financial institutions are encouraged by regulators to buy large amounts of long-term debt using virtually unlimited amounts of leverage. That must be the end!

secondary title

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

first level title

the fed

In this final segment, Powell has a rather messy situation on his hands. Each stakeholder is pulling his central bank in a different direction.

secondary title

interest rate cut

The Fed controls/manipulates short-term interest rates by setting rates on the RRP and IORB. Money market funds can earn income in RRP, and banks can earn income in IORB. Without these two tools, the Fed would be powerless to regulate interest rates as it wishes.

The Fed could slash interest rates on both tools, which would immediately steepen the yield curve. Benefits will include:

Banks are profitable again. They can compete with the rates offered by money market funds, rebuild the deposit base, and start making long-term loans to businesses and governments. The US banking crisis is over. The U.S. economy will thrive because everyone has access to cheap credit again.

secondary title

hike

hike

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

Here are the negative consequences of continuing to raise rates:

The private sector continues to prefer to borrow from the Fed through money market funds and RRPs rather than depositing funds in banks. U.S. banks continue to fail and receive bailouts as their deposit base declines. The Fed's balance sheet may not be stockpiling these bad loans, but the FDIC is now full of bad loans. This is still fundamentally inflationary because depositors will be repaid in full in printed money, and they will be able to earn more and more interest income by borrowing from the government rather than from the bank.

The yield curve continues to invert, making it impossible for the U.S. Treasury to issue long-term debt at the required scale.

I would like to expand on the point that raising interest rates also leads to inflation. I agree that the quantity of money is more important than the price of money. What I'm focusing on here is the amount of dollars injected into the global market.

As interest rates rise, there are three ways global investors can earn income in printed dollars. The printed currency can come from the Federal Reserve or the US Treasury. The Fed pays interest to holders through reverse repos and banks' reserves. Remember: If the Fed wants to continue manipulating short-term interest rates, it must have these tools.

If the U.S. Treasury Department issues more debt and/or the interest rate on new debt rises, it will pay more interest to the debt holders. Both of these things are happening.

New Article by Arthur Hayes: Be patient, the bull market will start in the fourth quarter

As we can see, the effect of QT has been completely outweighed by the interest paid through other means. The amount of money is increasing even as the Fed shrinks its balance sheet and raises interest rates. But will this continue to happen in the future, and to what extent? Here are my thoughts:

1. The private sector and US banks prefer to park their funds at the Fed, so the RRP and IORB balances will increase.

2. If the Federal Reserve wants to raise interest rates, it must raise the interest rates on funds deposited in RRP and IORB.

3. The US Treasury will soon need to finance a $1-2 trillion deficit for the foreseeable future, and must do so at high and rising short-term interest rates. Given the maturities of total U.S. debt, we know that real money interest payments can mathematically only go up.

Of course, the Fed could speed up QT to offset these effects, but that would require the Fed to end up being a direct seller of US Treasuries and mortgage-backed securities (MBS), apart from foreign investors and the banking system. If the largest bondholders are also selling (Fed), dysfunction in the US Treasury market will rise. That will spook investors, sending long-term yields soaring as everyone rushes to sell their bonds before the Fed starts selling.

first level title

transaction related

If you are a Satoshi believer, time is on your side. If you choose to join hands with the traditional financial devils, the time bomb is ticking...

Between now and the fall harvest, something important will happen.

First, the US debt ceiling will be raised this summer. This would allow the US Treasury to start issuing debt to finance the government. As the U.S. Treasury repays maturing debt and issues new debt, the net effect will be more debt outstanding and higher interest rates. Debt issuance may temporarily put some pressure on dollar liquidity as the Treasury's general account (TGA) increases. But over time, the Treasury spends money, TGA falls, and dollar liquidity increases.

Second, as I have stated before, inflation will bottom out and start to rise slowly. That means the Fed could pause rate hikes in June, only to reignite the flame and raise rates at its July meeting. By the end of August when central bankers gather in Jackson Hole, the policy rate could be closer to 6%. Higher interest rates will increase the amount of interest paid on RRP and IORB balances.

Finally, depositors will continue to move funds from non-systemically important banks to systemically important banks, or into money market funds. Money market funds park their funds in the RRP, while systemically important banks park their funds in the IORB. In both cases, the balance of RRP and/or IORB will grow. Systemically important banks have a lot of cash, which is why they pay little or no interest on deposits, and park any additional funds they receive in the Federal Reserve System (hence the IORB rise). This increases the amount of money the Fed prints to pay for funds held in these facilities.

Taken together, the amount of USD liquidity injected into the system on a daily basis will continue to grow. The rate of change in USD liquidity injections will also accelerate, as the larger the balance, the more interest paid. Compound interest is a geometric progression.

Bitcoin experienced a roughly 10% correction from its April high. All these interest payments are effectively a stimulus package for wealthy asset holders. Wealthy asset holders buy risky assets when they have more money than they need. Gold, Bitcoin, artificial intelligence technology stocks, etc. will all be the beneficiaries of the "wealth" printed and distributed by the government.

I expect bitcoin to remain stable here. I don't believe we're going to retest $20,000 or anywhere near that. As funds gradually flow into the global risk asset market, a strong support base will be formed. Volatility and trading volumes are often disappointing during the northern hemisphere summer, so I’m not surprised adventurers beset by boredom are taking a break from crypto trading. I will use this quiet time to gradually increase my Bitcoin allocation after the TGA refills.