An in-depth look at veToken's shortcomings and potential alternatives

Compilation of the original text: The Way of DeFi

Compilation of the original text: The Way of DeFi

Token voting locks have been all the rage for a while. It was pioneered by Curve first, and then protocols such as Ribbon, Yearn, and Hundred Finance all adopted this model. While there are definite advantages to this approach, the disadvantages are rarely discussed. Instead, it seems like every week a new project team announces their switch to the ve token design, which is seen as a panacea for everything from low TVL to poor price performance.

So, let me play the role of "Bad Bear". What are the downsides of ve tokens and what would potential alternatives look like?

Why the protocol adopts the ve token model

How the ve token works

ve stands for voting escrow

Escrow: Users choose how long they want to lock their tokens (like CRV). It cannot be unlocked in advance. Tokens are unlocked linearly over a selected period. Users can permanently lock their tokens, maximizing their voting power and rewards.

Voting: Proportional to their lockup period, users receive a certain amount of ve tokens (such as veCRV) in return. ve tokens are used for governance, which means that community members who lock tokens for a long time have more weight. This often applies to rewards as well. For example, users who lock CRV for up to 4 years can get 2.5 times LP rewards.

All in all, people who lock up tokens gain voting (and reward) power for the desired amount of time, usually proportionally.

What benefits did the team see

A lock represents a long-term commitment by a staker. They are willing to make their shares illiquid (-> opportunity cost) in exchange for voting rights and rewards. And that should help the team manage better, since committed members have more weight in decisions. These stakers should be: a) interested in the long-term health of the protocol (incentive alignment); b) willing to make informed, time-consuming decisions (self-selection).

These community members are more valuable to the protocol than others and are therefore more rewarded.

Disadvantages of ve tokens

Lower-than-expected incentive adjustments

When the market is bullish, the world seems to be sunny. But once the bears call, game theory turns dark. It is rational for stakers to maximize their personal gain (e.g. accept the largest bribe) rather than make decisions that support the long-term health of the protocol. This behavior especially occurs when sentiment turns bearish. Who knows how much the tokens will be worth in 4 years. It is best to earn as much as you can now. Others can take long time spans for their votes, but I've completely devalued my stake psychologically.

The Convex-style protocol adopts the"Incentive adjustments through lock-in"ridiculous approach. And another protocol sucks up vote-locked tokens like a starving Kirby. This keeps supply out of circulation, reducing selling pressure. Locked tokens, on the other hand, are managed by the holders of the meta-governance token, and the lockup period is usually shorter. Meaning, long-term consistency is gone. You could say that meta token holders don't want the underlying token to fail because it earns them income. But as we know, everyone has their own interests in mind and who knows what will happen in the crypto world in just a few months, let alone years.

Therefore, ve tokens may not be as helpful for long-term consistency as initially thought.

Community"Community", no, it's Bagholder

Once people realize that trust in the ve token model is further eroded by limited long-term consistency, they will seek to sell tokens. Here's the problem for the most committed community members: they can't -- their shares are locked for another 69 months. Stakers who follow the golden path of ve tokens, locking their tokens for the maximum duration, are the ones who get hit the hardest. It's devastating for them, isn't it? And it doesn't help with community building.

Locking works both ways. While it helps reduce selling pressure by taking tokens out of circulation, it also makes tokens less attractive to buy. If I had to lock the token for 4 years to get the best out of it, would I really buy it? In such a dynamic environment as cryptocurrency, the opportunity cost is enormous. To be fair, liquidity wrapping solves this problem by tokenizing the locked pledge. But as mentioned above, this reduces long-term consistency. Also, there is the issue of decoupling tokenized positions from the underlying ve tokens. "Tokenized ve tokens/ve tokens"For example:

For example:

The exit of cvxCRV holders means that cvxCRV is dumped for CRV, and then CRV is sold for ETH/DAI/...cvxCRV holders are affected by both the drop in CRV price and the decoupling of cvxCRV .

Also, meta governance tokens may look more attractive and will steal demand from ve tokens.

Especially with high release tokens, locked stakers can feel like they are constantly being dumped. This affects their behaviour. They may become more short-term profit-seeking. Then, other people will start behaving in the same way after observing this. Trust is eroded even more, and a vicious circle begins to form.

governance pause

This problem can be extended to the protocol level. Unmotivated stakers want to leave, but can't. They are locked. They still hold ve tokens that act as governance votes. The chances of them being interested in any governance decision that doesn't involve short-term profits are low.

Their voting power will only slowly decrease during the lockup period. At the same time, in this case, external capital will be hesitant to buy and lock tokens for a long time.

This makes governance difficult when it is most needed, and may even stop altogether.

Meta-governance tokens lead to cartelization (monopolization) of ve voting rights, but as long as meta-governance rights are allocated to token holders, no additional risks are added except for the aforementioned liquidity encapsulation problem.

Alternative Token Economics

To align token holders in the longer term, protocols can use different alternative token economic mechanisms. However, in the current growth phase of cryptocurrencies, where new narratives and projects emerge almost daily, it may be difficult to retain most of the community members and stakers in the long term. Token economics coupled with other measures of community building will help alleviate this problem.

Protocols need to realize that locking up stakers may not be as valuable as initially thought. You can't buy loyalty. Unsatisfied stakers make bad governance decisions.

Therefore, I advocate soft lock-in, thereby increasing the opportunity cost of stakers, with the goal of reducing short-term volatility and incentivizing long-term thinking, but allowing them to leave at any time. Only satisfied community members are valuable community members.

Let's look at the two token mechanisms and their tradeoffs, shall we?

Time-Based Token Economics

GMX, Platypus, Prism Protocol, and Kalao all use time-based token economics, though slightly differently.

Stakers accumulate growth value over time, being awarded more rewards and/or governance rights. They can unstake at any time, but lose their growth value, which constitutes an opportunity cost. Opportunity costs, in the form of lost future income and voting weight, can help reduce short-term volatility. For example, stakers are less likely to unstake during what they expect to be a temporary price drop. Also, this applies to the weeks when the protocol income is lower. Users will keep staking as long as the medium to long-term outlook is positive.

On the other hand, stakers are flexible and can leave at any time when their long-term evaluation changes. They can react to new information, such as problems with protocol adoption, new competitors or new demands in the market. Since individual (non-whale) voters have limited influence, it is fair to give them the right to withdraw. For the protocol, this has the advantage of resuming the governance process more quickly.

Time-based economics look backwards (how long the user has already staked) compared to ve tokens which consider stakers' commitment to the future (looking forward) in the form of a lock. Past behavior is a predictor, though not perfect, of future behavior. However, the longer a user has staked (and chooses to stake under various conditions), the more likely they are to continue to stake in the future. Opportunity cost is a further incentive to keep staking.

variable

With every token model, there are trade-offs. We can decide the balance among them by setting certain variables.

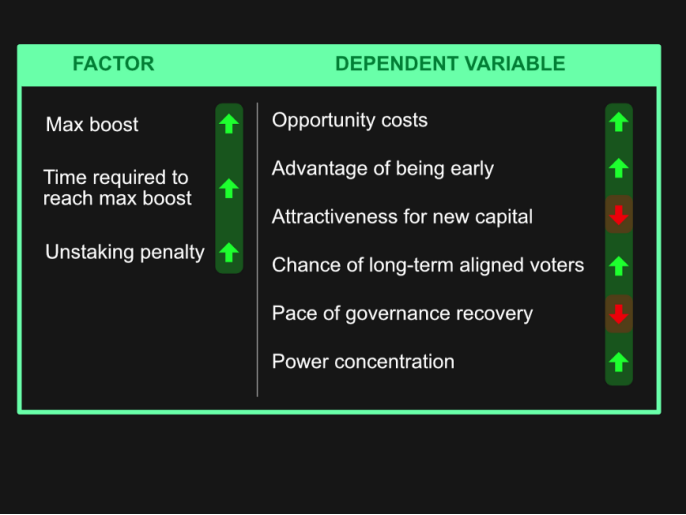

With time-based growth values, we have to balance the advantages of early speculators over new buyers. The greater the advantage, the higher the opportunity cost of unstaking. This reduces selling pressure and also makes late buying less attractive (less buying pressure). Additionally, it makes voting power (when users receive native tokens as rewards) and revenue more concentrated to early stakers. Governance recovery takes longer because long-term stakers are more weighted. On the other hand, long-term staking history shows that users care about a protocol and increases their chances of being well-informed, both of which improve decision quality.

The following factors determine the advantages of early stakers

maximum limit

The time required to reach the maximum cap

The higher the max cap and required time, the greater the early advantage.

There is also the penalty of canceling the pledge, and there are two models for this. When a user cancels any amount of PTP, Platypus' burns all accumulated vePTP (full penalty). This increases opportunity cost. Whereas GMX burns multiplier points (partial penalty) proportional to the user’s share of unstaked tokens.

Protocols could also introduce unstaking periods to further disincentive short-term transactions. The Prism protocol has a 21-day unstaking period for xPrism.

While Platypus and Prism employ separate reward pools (base and boost pools) for time-based boosts, GMX and Kalao have only one pool. A separate reward pool allows the team to ensure a certain minimum APR for non-growth users. Under the structure of a pool, growing users will squeeze out the rewards of non-growing users. The token growth factor needs to change, and the two pool model has another lever by adjusting the reward weight between the pools.

Attribution of awards

The patterns of esGMX and esKLO are particularly interesting to me. Stakers do not earn native tokens, but an escrow token. They can decide to:

Keep es tokens (autocompoundooooor). es tokens are automatically staked and rewarded like normal tokens;

Vest tokens linearly over a period of time (vestoooor). During this time, stakers will not receive rewards for their es tokens. Vesting requires an average amount of tokens staked to obtain es tokens.

This brings several benefits:

opportunity cost. Stakers must decide whether to vest their es tokens or use them to earn protocol income. As such, es tokens are particularly relevant to revenue-generating protocols.

Effectively reduce supply. Not all es tokens will be converted to native tokens due to staking requirements for attribution.

Reduce pressure to sell immediately. es tokens cannot be sold directly. Although at first it appears to be a"pass the buck"style release solution, but in the big picture, this might help. Token rewards are used to bootstrap supply and/or demand, but can only be sold after the protocol is (hopefully) established, which means the price may already be higher and there should be more demand to absorb the selling pressure.

Revenue is shared with long-term consistent stakers. More rewards are distributed to stakers who do not vest their es tokens.

in conclusion

in conclusion

Original link