In-depth analysis of 7 common design architectures: Why is there no perfect decentralized stable currency?

OriginalTitle: "Exploring the Design Architecture of Decentralized Stablecoins"

Author: Joe Kendzicky

written in front

written in front

In the article, the author conducted an in-depth analysis of the DAI, MIM, alUSD, UXD, FRAX, FEI and UST Stablecoin series, respectively, and analyzed the advantages and disadvantages of the above-mentioned Stablecoin design architecture. The author pointed out that the current Stablecoin mechanism needs to make certain trade-offs and trade-offs among stability, capital efficiency, censorship resistance and scalability, and there is no perfect decentralized Stablecoin.

introduce

start of text

introduce

first level title

PART.01 MakerDAO (DAI Stablecoin)

One of the oldest DeFi projects to date, MakerDAO is a decentralized credit protocol that can collateralize various crypto assets and mint debt. This debt exists in the form of the Stablecoin DAI, and Maker uses a system of external market forces, incentives, and policy tools to maintain Dai's 1:1 peg to the U.S. dollar.

Similar to a bank, users take out loans with collateral. In a banking environment, a borrower can put a house, car, accounts receivable, etc. as collateral for a loan.

For loans against digital assets, the value of the loan must always be lower than the value of the collateral to protect the creditor from default risk or liquidation risk, which is closely related to the liquidity of the collateral. In order to guard against this risk, borrowers can choose to deposit various mortgage assets (ETH, UNI, LINK, YFI, etc.) to cast debt, and various assets will have different margin requirements according to their risk levels. Assets with low liquidity and high volatility are more difficult to liquidate on a large scale, and if their collateral is below margin requirements, a larger buffer is required to ensure the smooth liquidation of positions.

Let's take a simple example of margin requirements.

Minting DAI in the ETH-A pool currently requires a minimum collateralization ratio of 145%. Suppose you deposit 1ETH, 1ETH = $4,000, and then you take out a 1,000 DAI loan. Your mortgage ratio is 4,000/1,000 = 400%. If ETH starts to crash and falls below $1,450/ETH, your vaults will be liquidated. During liquidation, the protocol will sell your collateral below the market price, incentivizing arbitrageurs to come in and pay off the debt.

How do we pay off our debts?

We cannot actually recover the DAI sent to the borrower (DAI is an ERC20 Token protected by the user's private key, and the borrower may have transferred it to someone else). We sell their ETH collateral on the open market in exchange for DAI. We then send this 1,000 DAI back to the protocol to be destroyed while closing its outstanding debt balance. At the same time, the incentive for arbitrageurs to perform this liquidation process is that they will receive a small portion of collateral as a reward during the liquidation process.

The really cool thing here is that the protocol is permissionless. There is no credit history check, no KYC process, no certificates of any kind; as long as you meet the deposit requirements, the system doesn't care who you are, and no one can stand in your way.

Another cool feature is that, due to the permissionless nature, the borrower acts as both a creditor and a borrower. There is no real direct counterparty on the other side of the agreement (compared to traditional finance where, in the event of a loan default, the bank acts as a direct counterparty).

Different from the traditional lending system, the default risk is shared by the entire system participants, as shown in the following figure:

first level title

PART.02 Abracadabra (MIM Stablecoin)

Fundamentally, the Abracadabra protocol looks extremely similar to the system mechanics of the MakerDAO protocol.

Debt (MIM) is minted permissionlessly through over-collateralized vaults. If the collateral:debt ratio falls below a certain threshold, the vault is closed and the debt is repaid by liquidating the borrower's collateral in the open market and using it to buy back MIM.

The main difference between MakerDAO and Abracadabra is that the Abracadabra vault is funded by depositing interest-bearing Tokens such as yvYFI, yvUSDT, yvUSDC, and xSUSHI. Interest-bearing Token is just an ordinary counterpart stored in the money market agreement or some kind of certificate (YFI, USDT, USDC, etc.), which can generate continuous interest. Interest Token is just an accounting token, which represents the collateral rights owned by users in the money market agreement.Therefore, we can use them to create MIM debt, instead of simply passively placing these interest tokens in Yearn or Compound.

One advantage Abracadabra offers is that the loan:value ratio tends to degrade over time because the collateral in the vault generates yield over time.

From a user perspective, this is great. This means that their debt decreases over time, and users can mint more MIM due to their reduced debt, without needing to post additional collateral (while still being able to maintain the same loan:value ratio as originally). Alternatively, they can choose to keep the MIM debt unchanged, and their actual debt repayments when closing the vault will be reduced.

first level title

PART.03 Alchemix (alUSD)

Similar to Abracadabra, Alchemix is also a debt protocol that allows users to stake collateral to a vault and mint corresponding Stablecoin debt. Both protocols involve posting yield-generating assets (various yield certificates) as collateral. The main selling point offered by Alchemix is loans that do not require liquidation. Let's explore how the protocol provides this functionality:

When Alchemix is initialized, users over-collateralize y assets into the Alchemix protocol and mint alUSD debt against it (the minimum collateralized debt ratio is 200%). The only collateral it accepts for minting alUSD is yDAI. This creates a 1:1 correlation between the volatility of the collateral and the volatility of the debt.

The only reason liquidations exist in protocols like MakerDAO or Abracadabra is to prevent the system from creating negative equity. If I deposit $200 of ETH in the Maker vault to mint $100 of DAI, and the value of that ETH then drops to $95, now each Dai is only backed by $0.95 of collateral, the system no longer has enough Credits to secure Dai's $1 peg.

This is an inevitable dilemma for any debt protocol using volatile collateral to back non-volatile debt.

However, if we remove the volatility of the collateral, we no longer face this challenge and can remove the liquidation requirement, giving users peace of mind that they no longer need to monitor the vault's margin.

Also, since our collateral is a productive asset that generates yield for us behind the scenes, we can use this accrued yield to actually pay back the base principal of the loan!

This is the essential reason why Alchemix is able to "self-pay the loan".

If there is no need for liquidation, why is there a need for over-collateralization?

Without overcollateralization, we have a recursive loop where depositors can issue debt indefinitely. For example:

1. The user deposits 100 yDai into Alchemix and mints 100 alUSD debt

2. Sell 100 alUSD on Curve.fi for an extra 100 Dai

3. Deposit the new Dai income into Yearn and receive 100 yDai

4. Bring the new yDAI back to Alchemix and mint 100 alUSD

5. Infinite loop

first level title

PART.04 UXD Agreement (UXD)

UXD is a Solana-based Stablecoin protocol that offers a novel compositional structure unlike any previous decentralized Stablecoin alternative. The key innovation here is that UXD uses on-chain perpetual futures contracts (also known as perpetual contracts) to create on-chain market-neutral derivative positions to avoid the risk of unilateral market volatility and generate a stable $1 value.

Let's further analyze its design architecture:

Derivatives markets such as Bitmex, Binance, and FTX allow users to trade synthetic contracts that mimic the spot market, known as perpetual contracts. For example, Bitmex's XBTUSD allows traders to gain exposure to the BTC/USD price without actually owning that Bitcoin spot asset. Perpetual contracts are widely used in the crypto space, mainly because of their simplicity, convenience (no expiration date, so no need for rolling contracts), and most importantly, they also provide leveraged products. While many have scaled back in recent months, 100x leverage is common at some point for exchanges in the space.

Every synthetic contract faces an inherent dilemma - how can our instrument keep our derivative price on par with the spot market price?

While the XBTUSD contract aims to mimic the price dynamics of BTCUSD as closely as possible, ultimately the two prices will never perfectly align unless there is a perfect balance of supply and demand between spot and derivatives order books, an impossible assumption . What happens if buying pressure breaks out on Bitmex, but the spot remains relatively steady? In this case, the price of the XBTUSD contract will increase, while the BTCUSD index will remain flat. Derivatives will deviate from the underlying price oracle.

To overcome this situation, Bitmex introduced an incentive mechanism called "funding rate", which naturally links the two prices. The funding rate is settled and paid every 8 hours, and the corresponding funding fee will be paid by the long or short side of the premium.

If the funding rate is positive (ie derivative price > spot price), the longs will pay a short premium. If the funding rate is negative (i.e. the derivative price< spot price), then shorts will pay a long premium.

Example: Let's say the spot index is priced at $50,000/BTC and the derivative is trading at $55,000/BTC. In this case, the funding rate is positive (derivative price > spot price). Therefore, XBTUSD longs will pay the interest rate to maintain their positions, and the proceeds will go to their short XBTUSD counterparties. Bulls are paying for counterparty liquidity. If the shorts demand more than the longs, the relationship will be reversed; the shorts will pay the longs.

The greater the difference between the derivative price and the spot price, the higher the interest paid. As interest rates rise, it incentivizes more counterparties to step in to balance both longs and shorts.

secondary title

1. Enter arbitrage

An interesting arbitrage opportunity exists here - traders can hedge directional risk, isolating funding fees from asset volatility risk. Here's how it works:

Let's say a trader buys $100,000 of BTC and uses it to open a 1x short position. To calculate how much interest he will earn/pay, we simply multiply the interest rate by the notional size of the trader's position. Assuming a "default" funding rate of 0.01%, within an 8-hour window, a trader would receive:

$100,000 * 0.01% = $10

That doesn't seem like much at first, but what if we annualize this value?

$10 * 3 = $30/day

$30 * 365 = $10,950/year

$10,950/ $100,000 = 10.95% directional risk-free trade

secondary title

2. UXD mechanism

Simply put, the UXD protocol receives funds and automatically executes this arbitrage strategy on behalf of its users. If a user sends 1 BTC to the protocol, UXD will transfer this 1 BTC to a decentralized derivatives trading platform (currently starting with Mango Markets, with plans to expand to other markets in the future), and then use this platform to execute 1 BTC short collateral as a security deposit for the transaction.

Assuming the market price of BTC is $50,000, this effectively locks in a $50,000 Stablecoin position. If the spot price of BTC rises, our short position will generate a negative PnL (profit and loss), but it will be offset by a linear increase in the value of BTC spot collateral. Likewise, if the spot price of BTC falls, our short position would generate a positive PnL, but this would also be offset by a loss in the value of the BTC backing it.

The total value of our derivatives position remains at $50,000. UXD then issues 50,000 Tokens to users representing their right to receive collateral from the position. To redeem their collateral, they simply send the Token back to the minting contract, and the agreement will unwind the derivatives transaction on Mango Markets, return the BTC collateral to the user, and then destroy the UXD Token.

Right now, market-neutral derivatives positions have typically been accumulating interest rates. What to do with these funds?

secondary title

3.FRAX

Frax in its current state can best be described as a hybrid centralized and decentralized stablecoin. The core innovation of Frax is that it is a stablecoin built with a credit model based on external market forces.

In short, the protocol uses an algorithm to achieve the following 3 functions:

- Increase mortgage rate

- Lower mortgage rate

- maintain the current balance

Every FRAX is backed by a certain percentage of USDC collateral. At system launch, in order to mint 1 FRAX, users must deposit 1 USDC into the protocol. However, over time, the price of FRAX will fluctuate around $1. The exchange rates of the centralized Stablecoins USDC and USDT will also fluctuate, but in the end the arbitrage process will converge the Stablecoin price back to $1.

The following is the arbitrage process under the centralized Stablecoin mechanism:

If the price of USDC = $1.05, the arbitrageur mints USDC by depositing $1 into Circle's bank account and sells it on the market for a risk-free profit of $0.05. Every time an arbitrageur sends more USDC to the market, it increases its supply, driving down the price. This cycle continues to iterate until the price of 1 USDC returns to the base pegged price.

If 1 USDC = 0.95 USD, then reverse arbitrage exists. They would buy USDC on the open market, send it to the USDC contract for burning, and redeem it for USD in Circle's bank account for a $0.05 difference. With the destruction of USDC caused by arbitrage, the supply will decrease and the price will push up until the price of 1 USDC returns to the base pegged price.

Compared with the above mechanism, FRAX works differently. When the price of FRAX deviates from $1 and stays there for a period of time, an algorithm is activated that increases or decreases the collateralization ratio required to create FRAX.

For example, when the price of FRAX reaches $1.05, this signals to the algorithm that demand is greater than supply, as market participants are effectively buying the asset at a 5% premium to face value. The USDC centralized model allows arbitrageurs to increase the total supply of USDC to bring the price closer to $1, and obtain risk-free profits through arbitrage.

Frax works differently, the protocol not only increases the supply of FRAX through the arbitrage behavior of arbitrageurs, but also reduces the collateralization ratio of Stablecoin FRAX (reducing the collateralization ratio of Stablecoin helps to further restrain the growth of demand to achieve a balance between supply and demand ).

As a simplified analogy, suppose a restaurant is faced with a 5% increase in food costs, and they are faced with several options for passing these costs on to the end consumer:

1) Increase meal prices by 5%;

2) Reduce meal portion sizes by 5%.

or both.

FRAX responds to changes in supply and demand in a similar fashion, with arbitrageurs increasing the supply by a certain percentage (increasing meal fees) when the price is above the target price, while it is up to the protocol to decrease the pledge rate (making meal sizes smaller).

The protocol governance token of the Frax protocol is FXS, which plays a vital role in promoting system credit. FXS Token accumulates value during credit expansion and loses value during credit compression.

*Translator's note:

*Translator's note:

The protocol adjusts the collateralization rate every hour by 0.25%. The function decreases the collateralization ratio every hour when the FRAX price is at or above $1, and increases the collateralization ratio every hour when the FRAX price is below $1. There will be a deviation between the mortgage ratio dynamically adjusted by the contract and the actual total collateral value ratio. In order to unify the two, the protocol provides the functions of remortgage and repurchase.

Remortgage:

Anyone can call the recollateralize function and check to see if the total collateral value in dollars across the system is lower than the current collateral ratio. If so, then the system allows the caller to aggregate the amount needed to reach the target collateral ratio, in exchange for a certain reward rate for newly minted FXS. This is roughly equal to, when the mortgage rate increases, the system will purchase the corresponding USDC in the market by minting new FXS to increase the required reserve assets.

Example A: There are 100 million FRAX in circulation at a collateralization ratio of 50%. The total collateral value of the entire USDT and USDC pool is $50 million, and the system is balanced. When the price of FRAX falls to 0.99 USD and the agreement will increase the collateral ratio to 50.25%.

A collateral of $250,000 is now required to reach the target ratio. Anyone can call the recollateralize function, put up to $250,000 in collateral into the pool, and get the same amount of FXS and a 0.20% bonus rate of FXS.

The process of remortgaging is the process of FXS inflation, which will increase the Token selling pressure in the market.

redemption:

The opposite occurs when there is more collateral in the system than is needed to maintain the target collateral ratio.

Example B: There are 150 million FXS in circulation at a collateralization ratio of 50%. The total collateral value of USDT and USDC is $76 million. $1 million worth of excess collateral is available for repurchase by FXS.

Anyone can invoke the repo function and burn up to $1 million worth of FXS for excess collateral.

On the contrary, the redemption process is the deflation process of FXS. Using excess collateral to purchase FXS will increase the purchasing power of Token in the market.

When the agreement is procyclical, that is, demand exceeds supply, FXS will continue to be repurchased by the agreement as the mortgage rate continues to decrease; on the contrary, as the mortgage rate continues to rise, FXS will continue to inflate, and market selling pressure will increase.

Throughout the lifetime of the protocol, we have frequently seen FRAX trading at >$1, allowing the protocol to algorithmically wean itself off USDC over time.

Only 83% of every FRAX in existence is backed by USDC. As mentioned above, this value may change in an instant (though there is an inherent time delay built into the algorithm...i.e. it cannot flip to 100% USDC collateral in minutes).

secondary title

4.Fei

Fei is another algorithmic stablecoin that shares some similar characteristics with FRAX. However, unlike Frax, FEI aspires to be a completely trustless stablecoin that does not rely on centralized intermediaries (USDC, USDT, etc.). Like the Frax protocol, the Fei protocol introduces two independent Tokens into its design architecture: FEI (Stablecoin) and TRIBE (Governance Token).

The original mechanism maintains the peg of the exchange rate by using a Protocol Controlled Value (PCV). PCV is just a fancy term for selling its native token (FEI) in exchange for some exogenous capital (ETH). The protocol now has ETH collateral and can be deployed as needed. This is different from the typical liquidity mining model of most Defi projects. Those agreements essentially rent liquidity at an expensive price and are forced to pay high APY to attract liquidity. Once these subsidies wear off, liquidity evaporates and the protocol is left with nothing to do.

In the original design, users would deposit $100 in ETH, and the protocol would mint a corresponding 100 FEI in return through the bonding curve. However, this process of minting FEI through the bonding curve is a one-way channel; if you want to exchange your FEI back to ETH, you must trade it through a secondary market such as Uniswap. The system maintains the price peg using something called a direct incentive.

1 FEI = $1 of ETH collateral is market equilibrium, but what happens if ETH collateral falls below $1? The Uniswap pool has a custom parameterization where there is a penalty for selling FEI at an underwater price. The penalty is double the difference between the current FEI price and the $1 spread (the greater the spread, the greater the penalty). Therefore, if the price of FEI is $0.98, a penalty of ([1.0-0.98]*2) = $0.04 will be charged.

Likewise, if you buy FEI below the fixed exchange rate, you will get an incentive that comes from the seller's additional tax above. So in this case, if you minted 1 FEI for $0.98, you would end up with $1.02 worth of value. These are the infrastructure of the direct incentive mechanism.

secondary title

5.V2

The system cancels the direct incentive as the main module for maintaining the peg, and replaces it with PCV income distribution and TRIBE Token support. The protocol increased exposure from just 2 narrowly focused assets (ETH and FEI) to now 7 (FEI, ETH, DAI, RAI, INDEX, DPI, LUSD). The goal here is to spread risk across a broader asset base to reduce downside volatility and the threat of FEI unanchoring should ETH price crash. Additionally, PCV is being deployed in various money market protocols (AAVE, Compound, Lido, Tokemak) to earn interest on collateral on an ongoing basis, increasing collateralization ratios. In a way, the FEI protocol almost looks like an investment DAO whose investment mission is to keep the system PCV > FEI circulating for users.

If the protocol fails under the V2 mechanism, TRIBE holders will give the system support to keep the price pegged to $1. If undercollateralization occurs (ie, $value of PCV < $value of user's circulating FEI), TRIBE will be minted and sold on the market to raise funds to cover the shortfall.

first level title

PART.05 Terra(UST)

UST is a decentralized stablecoin whose price is backed by Terra blockchain's native Token LUNA. At the heart of the Terra ecosystem is the algorithmic market module that balances system incentives to stabilize the peg.

Consists of 2 Tokens:

- Terra UST: A USD-pegged stablecoin

- LUNA: The underlying gas Token of the Luna smart contract blockchain (that is, ETH in Ethereum)

LUNA Token essentially absorbs the volatility of UST Stablecoin. When the price of UST is trading outside of its peg, this is where incentives come into play; the algorithm module will incentivize arbitrageurs to mint more UST supply, thereby pushing the price back to parity. Regardless of the market price of UST, 1 UST can always be minted/redeemed for $1 worth of LUNA. The spread between the two (the difference between the UST market price and $1) provides arbitrageurs with a risk-free profit while helping to maintain the $1 peg parity.

As an example, let's say UST is trading at $1.05 on Binance.

- The arbitrageur sends LUNA Token worth $1 to the protocol

- The agreement will burn the 1 USD LUNA Token and mint 1 UST at the same time

- The arbitrageur then sends this 1 UST to Binance and sells it for $1.05, getting a 5% spread

End result: UST is inflated, and LUNA is deflated. The expansion of UST coincides with the contraction of LUNA, causing LUNA Token holders to increase in value as the price rises. LUNA holders are the cheerleaders for the growth of UST and the DeFi ecosystem, because they are the direct beneficiaries of the value of these ecological developments.

Now, let's say UST is trading at $0.95 on Binance.

Arbitrageur will buy 1 UST on Binance for $0.95 and send it to the protocol

The protocol will always honor $1 in UST regardless of the luna price. Arbitrageurs exchange 1 UST for 1 USD of LUNA.

Then the arbitrageur sells his LUNA for $1, earning a difference of $0.05.

End result: UST is deflationary, while LUNA is inflationary. UST supply contraction pushed the price back to $1. LUNA Token holders suffer value dilution in the process, as their current holdings are diluted by the new LUNA.

first level title

secondary title

1. Stability

Stability can be described as the effectiveness of the protocol to maintain its $1 peg. Maintaining parity when prices > $1 is easy, maintaining parity when prices are below $1 is the hard part.

Having an efficient arbitrage process is the most critical component of stability. The faster this arbitrage process is done, the more robust the protocol is, as it reduces the time-price range outside the peg. Ideally, at even the slightest deviation, we'd like professional arbitrageurs to step in and take profits, pushing prices back to their original levels immediately. Long-term deviations out of bounds increase protocol risk, cause users to lose confidence in market mechanisms, and exacerbate downward reflexivity.

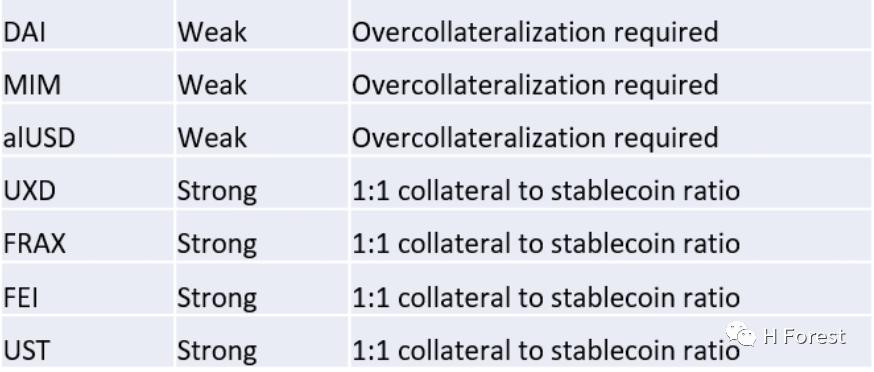

Instead of trying to give a ranking index to stability (too subjective), we discuss each project's strengths/weaknesses in terms of stability:

secondary title

2.MIM: Same as Dai

alUSD: There is no arbitrage mechanism for rebalancing when the price of alUSD is unpegged, so alUSD is especially challenging.

Under normal circumstances, when selling pressure outweighs buying pressure, it pushes the price below $1 regardless of the existence of collateral backing its intrinsic value of $1. This is because people mint alUSD primarily to gain leverage, and immediately after minting users will sell their alUSD for the X asset of choice. At the same time, the buyer's demand for alUSD is relatively low, and there is little DeFi application support for alUSD, which means that there is also little demand for the market to hold alUSD. Therefore, the price will continue to decline slowly. To overcome this problem, the liquidity rewards at the protocol layer are directed towards 3pool LP vaults, which provide liquidity between alUSD and DAI, USDT, USDC.

UXD: UXD may have the strongest stability guarantees of any non-overcollateralized Stablecoin, and its unique structure can even compete with overcollateralized models. However, like any other decentralized protocol, UXD is subject to peg instability during periods of high volatility, in which case the derivative protocol may not be properly liquidated and the protocol is forced to absorb losses. However, a large portion of this risk is initiated by various system stakeholders (including the Mango Markets derivative agreement and the UXD agreement) before being passed on to UXD Token holders. The Mango Markets Insurance Fund provides the first line of defense. The UXD Protocol Insurance Fund is the second line of defense if the first line of defense fund is depleted. Finally, if both resources are depleted and outstanding debts remain, there is a third line of defense among UXP governance token holders that support protocol risk (the protocol will mint UXP out of thin air and sell it on the open market to obtain additional collateral to fill the gap). If the liquidity of all UXP Tokens evaporates completely, then UXD itself will be repriced in the market accordingly. We think it is very unlikely that all 3 lines of defense will fail, and may only happen in an industry-ending event (eg, an undisclosed quantum computer developed by a secret agency that steals everyone's assets).

FRAX: FRAX has "strong" stability in the exogenous USDC that supports its Token. If the price is below $1, there are immediate incentives that help revive the peg, but one of the inherent problems is that it takes a while for these incentives to work through the protocol design.

In addition, FXS holders guarantee "under-collateralized" gaps when market forces signal demand for higher USDC collateral. If no buyer is willing to come in and buy FXS while selling USDC, the system is inherently under-collateralized due to the invalid value of FXS.

FEI: FEI may be the weakest in terms of stability, because a) the pledged assets backing FEI are inherently volatile, unlike stable assets like USDC/USDT b) lack of excess collateral buffer c) lack of direct arbitrage mechanism

secondary title

3. Censorship resistance

secondary title

4. Capital efficiency

secondary title

5. Scalability

The excellent supply of stablecoins needs to expand in response to increased demand. If integration with different DeFi services, the growth and adoption of the associated Stablecoin continues to rise, but the total supply remains the same, then through fundamental economics we can conclude that the price will have to go up in this case. However, this fundamentally violates the coveted property of a Stablecoin - achieving dollar parity. Therefore, we need a mechanism by which arbitrageurs and various other market participants can satisfy increased market demand (reflected in prices > $1) by depositing new collateral into the protocol and minting new tokens.

*Translator's note:

*Translator's note:

Original link