Original article by @BlazingKevin_, the Researcher at Movemaker

Real-World Adoption and Expansion of USD Stablecoins

In our previous analysis, we argued that the creation of Plasma was a key strategic move for Tether, aiming to fundamentally transform its business model from a passive "stablecoin issuer" to an active "global payment infrastructure operator" in order to recapture the enormous value captured by third-party public chains. The urgency and importance of this strategic deployment are being amplified by an irreversible macro trend: the real-world adoption of US dollar stablecoins is undergoing a significant paradigm shift and entering a phase of accelerated expansion.

Quantitative expansion of the total market volume

First, from a macroeconomic perspective, the overall size of the stablecoin market is experiencing a new round of structural growth. Compared to the market cycle two years ago, the total global stablecoin market capitalization has climbed from approximately $120 billion to $290 billion, a 140% increase. This data indicates that demand for stablecoins has transcended the realm of speculation and trading within the crypto-native sector and is beginning to gain broader market recognition as an independent asset class and financial instrument.

The explosion of core application scenarios: cross-border payments

The strongest manifestation of this growth is in the cross-border payments vertical. Two years ago, the actual use case for stablecoins in cross-border settlements was nascent and almost negligible. However, according to the latest data, monthly settlement volume in this sector has now exceeded $60 billion. Even more noteworthy is the rate of growth—20% to 30% month-over-month—clearly demonstrating a steep adoption curve.

Despite rapid growth, market penetration is still in its early stages. Compared to the current global traditional cross-border payment market, which stands at $200 trillion annually, stablecoins still account for a negligible share, suggesting significant potential for growth of tens or even hundreds of times in the future.

Core driving force: the demand for “currency substitution” in high-inflation economies

The accelerated adoption of stablecoins is driven by strong real-world economic drivers, particularly in emerging markets and countries with high inflation.

An in-depth analysis published by Cointelegraph in August noted that in countries like Venezuela, the sovereign currency (the bolivar) has essentially lost its core function as a medium of daily commercial transactions due to hyperinflation. Stringent capital controls, a failing local banking system, and chaotic official exchange rates have combined to create a scorched-earth financial environment. In this environment, citizens and businesses are actively seeking alternative currencies. The US dollar stablecoin, with its ample liquidity and stable value, has become the market's preferred "hard currency," far more reliable than cash or local bank transfers.

This phenomenon is not unique to Venezuela. Since the global inflation wave in 2022, several major economies, including Argentina, Nigeria, Turkey, and Brazil, have faced severe pressure to depreciate their currencies, giving rise to huge demand for value storage and payment hedging.

Venezuela ranks 18th in global cryptocurrency adoption. Source: Chainalysis

According to Chainalysis, Venezuela's cryptocurrency adoption rate already ranks 18th globally. Even more compelling is the fact that by 2024, 47% of the country's small transactions under $10,000 were conducted using stablecoins, making it the ninth-highest per capita crypto adopter in the world. This is no longer a niche activity, but rather a testament to the deep integration of stablecoins into the socioeconomic fabric of Venezuela.

More importantly, this adoption is gradually moving from a "gray area" of spontaneous private initiatives to a "sunlight" area of official recognition. In Brazil, stablecoins have been integrated into PIX, the national instant payment system; in Argentina, the use of stablecoins for large contract payments, such as rent, has also been legally recognized. These cases signal that stablecoin adoption is evolving from "bottom-level initiative" to a higher level of "top-level confirmation."

US dollar stablecoin: three strategic fulcrums of US national interests

Since the clarification of the regulatory framework, exemplified by the Genius Act, the growth trajectory of dollar-denominated stablecoins has accelerated exponentially, and their long-term potential is far from reaching its ceiling. This explosive growth is not merely a market phenomenon; it is deeply tied to the strategic interests of the United States. From a macro perspective, the global expansion of dollar-denominated stablecoins can bring at least three strategic benefits to the United States:

Maintaining US dollar hegemony: an asymmetric extension of monetary influence

Over the past decade, the global process of de-dollarization has been progressing slowly but steadily, eroding the dollar's role as an international reserve currency and settlement instrument. The rise of dollar-denominated stablecoins offers a novel, asymmetric solution to reversing this trend.

Especially in the high-inflation countries mentioned above, the widespread adoption of dollar-denominated stablecoins essentially creates a parallel, dollar-anchored "digital dollar" economy, independent of the sovereign financial system. This effectively circumvents these countries' capital controls and fragile fiat currency systems, allowing the dollar's value proposition to reach end users directly. This not only avoids the use of any traditional geopolitical or military means, but also effectively achieves deep monetary penetration into these economies, significantly expanding the effective reach of the "dollar ecosystem" (traditional dollar + digital dollar), thereby consolidating the dollar's international status in a new dimension.

Relieving fiscal pressure: Creating structural demand for U.S. Treasuries

The second strategic fulcrum is to provide support for the increasingly burdensome US government finances, which is crucial. The stability of the US Treasury market, particularly its yield level, is a core concern of US economic policy. The Trump administration's extreme sensitivity to fluctuations in 10-year Treasury bond yields during the tariff dispute demonstrates that the Treasury market is the cornerstone of the US macroeconomy.

The issuance mechanism of dollar-denominated stablecoins naturally creates a large and growing source of demand for U.S. Treasuries. Although stablecoin issuers currently hold a significant portion of their reserve assets in U.S. Treasuries, their role as major buyers of U.S. Treasuries will become increasingly significant as their total market capitalization continues to expand. A Citibank analytical model predicts that the long-term potential size of the stablecoin market could reach $1.6 trillion by 2030. The model further indicates that hundreds of billions of dollars of this incremental demand for U.S. Treasuries will primarily come from three sources: 1) the reallocation of globally circulating U.S. dollar banknotes to digital forms (approximately $240 billion); 2) the partial reallocation of global central bank base money (M0) (approximately $109 billion); and 3) the reallocation of foreign-held U.S. dollar deposits to stablecoins (approximately $273 billion). This additional purchasing power will play a significant role in stabilizing U.S. Treasury yields and reducing government financing costs.

Consolidating first-mover advantage: Dominating rule-making in the digital asset era

Finally, the United States is fully committed to ensuring its dominance in the global crypto market, and the US dollar stablecoin is a key tool in achieving this goal. The 180-degree shift in regulatory direction, from past suppression to current embrace, clearly reveals the evolution of its strategic intentions. When policymakers realized they couldn't completely stifle crypto technology, they quickly shifted to a strategy of "cooptation" and "utilization," incorporating this emerging field into their regulatory and economic landscape by establishing a comprehensive legal framework.

This strategy isn't unique to the United States; it's part of a global race among major economies. The ultimate goal of all countries and regions actively pursuing stablecoin legislation is to seize a favorable position in this new fintech landscape and share in its future dividends. By supporting dollar-denominated stablecoins, the United States aims to ensure that the underlying settlement standards for the future global digital economy remain firmly in its control.

The Current State of Non-USD Stablecoins: Structural Dilemma and Strategic Necessity

Extreme concentration of the market structure

Despite the strong growth momentum of US dollar-denominated stablecoins, a healthy global digital asset ecosystem should feature the coexistence of multiple fiat currencies. However, real-world data reveals an extremely unbalanced picture: the market space for non-US dollar-denominated stablecoins is being severely squeezed.

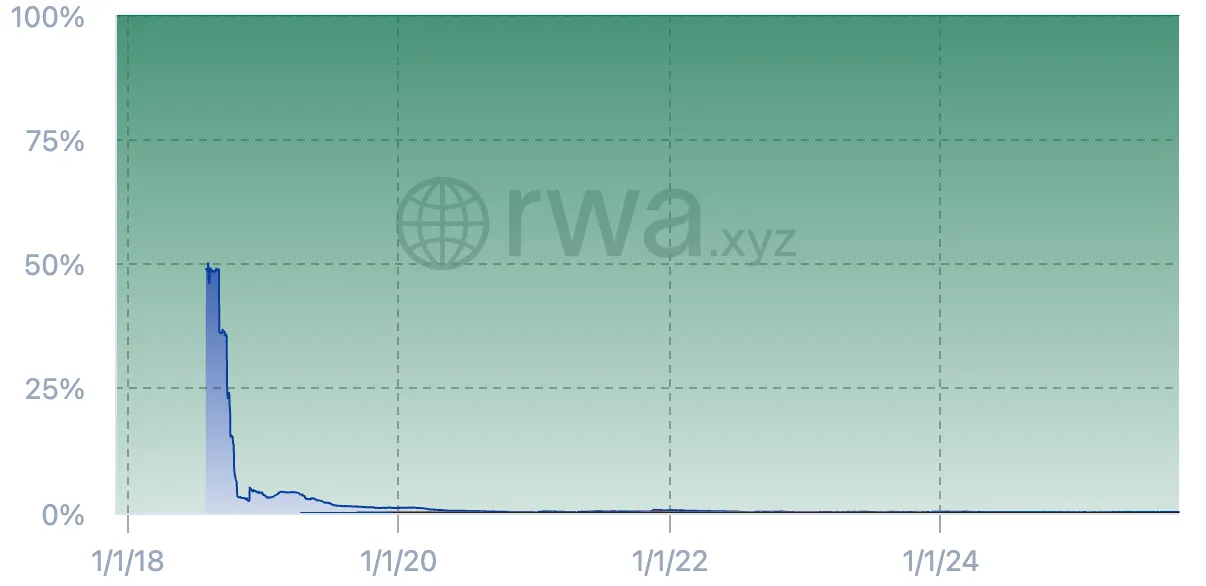

Stablecoin market share by fiat currency. Source: rwa.xyz

Data shows that this sector has experienced a dramatic decline. In 2018, at the dawn of the market, non-USD stablecoins held a 48.98% market share, virtually rivaling USD stablecoins (51.02%). However, today, their total market share has shrunk to just 0.18%. In terms of absolute size, the total market capitalization of non-USD stablecoins is only $526 million, of which Euro stablecoins ($456 million) command a commanding 88.7%. This demonstrates that, aside from the US dollar, no other fiat currency has yet established effective market competitiveness in the stablecoin market.

Structural risk: “Exchange rate tax” for users in non-dollar zones

As the stablecoin market becomes increasingly integrated with real-world economic activity, this "unipolar system" of US dollar-denominated stablecoins poses potential structural risks for users in non-dollar economies (particularly developed economies experiencing similarly low inflation). The core issue is that these users are forced to bear unnecessary foreign exchange volatility risk in the process of participating in the global cryptoeconomy.

We can illustrate this problem with a typical user journey:

Imagine a user in Tokyo who purchased Ether (ETH) using Japanese Yen (JPY) on the local regulated exchange bitFlyer. When she wishes to invest these assets in a global DeFi protocol (such as lending on Aave or providing liquidity on Uniswap), she discovers that the core funding pools of these mainstream protocols are almost entirely denominated in US dollar stablecoins (USDC, USDT, etc.).

The "yen balance" in her bitFlyer account cannot be directly transferred to the on-chain world. To participate in DeFi, she must hold an on-chain, tokenized stable asset. In the absence of a sufficiently liquid and composable yen stablecoin, her only option is to convert her ETH into a USD stablecoin. This step adds an additional layer of JPY/USD exchange rate exposure to her portfolio. Regardless of future profits or losses, when she eventually converts her funds back to yen, she will be subject to exchange rate fluctuations during this period, effectively imposing an invisible "exchange rate tax."

Systemic Risk and the Strategic Necessity of Diversification

From a broader perspective, the entire crypto economy's liquidity lifeline currently relies almost entirely on US dollar-denominated stablecoins, creating a potentially highly concentrated systemic risk point. Any extreme regulatory oversight, technological failures, or monetary policy shocks originating in the United States could have a catastrophic impact on global markets.

Therefore, promoting the development of multiple high-quality stablecoins, such as the euro, pound, and yen, has far greater significance than market competition itself. It is equivalent to building a " risk isolation wall " and a " systemic backup plan " for the global crypto economy. A diversified multi-fiat stablecoin ecosystem can effectively hedge the risks of over-reliance on a single national currency and a single regulatory system, enhancing the overall system's anti-fragility.

For major economies like the European Union and Japan, promoting stablecoins regulated by their own financial systems and pegged to their currencies is no longer simply a commercial undertaking; it is an extension of their "monetary sovereignty in the digital age" and a national strategic task . While non-USD stablecoins currently lag far behind USD stablecoins in terms of scale and liquidity, their existence has a solid rationale, and their development is an inevitable historical trend. Below, we will provide a detailed overview of the development of major non-USD stablecoins.

Euro stablecoin

Against the backdrop of the global stablecoin market being absolutely dominated by the US dollar, the evolution path of the euro stablecoin provides us with an excellent example to observe how non-US dollar currencies attempt to break through under regulatory drive.

Two phases of market evolution: from early exploration to regulation-driven acceleration

The development of the Euro stablecoin can be clearly divided into two stages, with the EU's Markets in Crypto-Assets Directive (MiCA) as the watershed:

- Early Exploration Phase (pre-MiCA) : This phase was exemplified by the launch of STASIS Euro (EURS) in 2018. As a market pioneer, EURS faced a period of slow growth, with its market capitalization hovering between tens of millions and 100 million euros. This reflected the lack of a clear regulatory framework and institutional demand, limiting the market to a small number of European crypto enthusiasts and preventing it from achieving scale.

- Accelerated Development Phase (Driven by MiCA) : The introduction and gradual implementation of MiCA was a fundamental game-changing catalyst. It provided market participants with unprecedented legal certainty, attracting the formal entry of industry giants. Stablecoin issuers Circle (issuer of USDC) and Tether (issuer of USDT) launched Euro Coin (EURC) and Euro Tether (EURT), respectively. Circle, in particular, began actively advancing its multi-chain deployment strategy in 2023-2024, expanding EURC to multiple mainstream public chains, including Ethereum, Solana, and Avalanche, as MiCA approached.

The success of this strategic shift is borne out by data: between 2023 and October 2025, the total market capitalization of euro-denominated stablecoins experienced rapid growth, currently reaching $456 million. Circle's EURC contributed the vast majority of this growth, with its market capitalization increasing by 155% in 2025, from $117 million at the beginning of the year to $298 million . While the absolute value still lags significantly behind that of US dollar-denominated stablecoins, its growth rate demonstrates strong catching-up momentum.

Market acceptance assessment: Infrastructure in place, but network effects insufficient

- Exchange and DeFi Integration : The foundational infrastructure for Euro stablecoins has been laid. All major exchanges, including Coinbase, Kraken, and Binance, have listed EURC or EURT and offer trading pairs with major crypto assets. Furthermore, leading DeFi protocols such as Aave, Uniswap, and Curve have also integrated with Euro stablecoins. In particular, on protocols optimized for stablecoin exchange, such as Curve, the liquidity of Euro stablecoin pools is steadily increasing.

- Potential application scenarios : In the field of payment and remittance, some Web 3 payment applications and fintech companies have begun small-scale pilots, using euro stablecoins for instant settlement and cross-border payments within the euro area.

- Core Obstacle: Cognitive Gap : Despite the initial infrastructure, the Euro stablecoin faces a significant cognitive gap and network effect deficit . In the minds of the vast majority of global crypto users, the concept of "stablecoin" is almost synonymous with "US dollar stablecoin," making it difficult to acquire new users and maintain liquidity.

The dual dilemma of future development

- Potential competition from official digital euros (CBDCs) : The European Central Bank (ECB) is actively promoting the research and development of a digital euro. Once a central bank-issued, credit-risk-free digital euro is launched, it will pose a direct, asymmetric competition to privately issued euro-denominated stablecoins. By then, the digital euro is likely to gain an overwhelming advantage in regulatory status and application scenarios, squeezing out private stablecoins.

- Business model challenges posed by interest rate differentials : This presents a more fundamental economic constraint. Stablecoin issuers' core profits derive from interest income on their reserve assets (primarily short-term government bonds). Historically, interest rates in the Eurozone have been consistently lower than those in the United States. This means that, given the same scale, the profitability of issuing euro-denominated stablecoins is inherently weaker than that of issuing dollar-denominated stablecoins . This profitability differential directly limits issuers' ability to promote DeFi protocol integration and user adoption through revenue sharing and liquidity incentives, creating a negative cycle that hinders initial success and scale expansion.

Australian dollar stablecoin

The Australian dollar stablecoin market exhibits a distinct development paradigm from the Eurozone. While its public market capitalization is approximately $20 million, ranking second among non-USD stablecoins globally, its most notable characteristic is its top-down exploration, led by traditional banking institutions rather than crypto-native companies .

Market dominance: the entry of traditional banks

Australia's most notable stablecoin projects originate from two of the country's "Big Four" banks—ANZ and NAB—who have launched A$DC and AUDN, respectively. This is a rare phenomenon globally, signaling a direct recognition by the mainstream financial system of the potential value of stablecoin technology. However, it's worth noting that these two bank-issued stablecoins are currently primarily in the inter-institutional settlement and internal pilot phases and have yet to be widely released to the public.

The supply of Australian dollar stablecoins for the retail and crypto trading markets is mainly filled by third-party payment companies, among which AUDD is a representative.

AUDD (by Novatti)

- Issuer Background : Novatti is a licensed payment service provider listed on the Australian Securities Exchange (ASX) with a dual background in compliance and fintech.

- Target customer group : It has a clear positioning and mainly serves three types of users: cryptocurrency traders, individuals or enterprises with cross-border remittance needs in Australian dollars, and Web 3 application developers.

- Technical path : AUDD chose to be issued on public chains such as Stellar, Ripple, and Algorand, which are known for their payment efficiency, rather than Ethereum. This reflects its strategic consideration of focusing on payment and settlement.

- Market Position : Currently, AUDD is the most accessible and usable Australian dollar stablecoin for retail users.

Core Development Dilemma: Dual Uncertainty of Regulation and Official CBDC

- Lack of a regulatory framework : Unlike the EU, which has fully implemented the MiCA legislation, Australia has yet to introduce a comprehensive and clear legal framework for stablecoins as of October 2025. This regulatory lag poses a significant bottleneck to market development. Even strong banks like ANZ and NAB can only conduct exploration on a small scale, unable to promote products to the public on a large scale amidst the lack of clear regulatory definitions. This significantly limits the speed and scale of development of the entire Australian dollar stablecoin ecosystem.

- Potential competition from the official digital Australian dollar (CBDC) : The Reserve Bank of Australia (RBA) has been actively researching the issuance of an official CBDC and recently successfully completed a pilot program. This development introduces a second level of uncertainty into the market. If the RBA decides to formally issue a digital Australian dollar, as an "ultimate risk-free asset" directly held by the central bank and free of credit risk, it will directly compete with stablecoins issued by commercial banks or private institutions. Whether the two will coexist in a complementary or competitive manner remains unclear, and the long-term market landscape remains uncertain.

Korean Won Stablecoin

The South Korean market presents a unique paradox: despite its high acceptance of crypto assets, it lacks the internal "soil" for the growth of stablecoins. This contrasts sharply with the bottom-up adoption driven by the private sector in countries with high inflation. The fundamental reason is that South Korea's highly developed FinTech and instant payment systems already meet the daily needs of the vast majority of users, thereby weakening the "endogenous motivation" for stablecoins as a payment alternative .

Therefore, if the Korean won stablecoin wants to gain market adoption, the only viable path is a top-down , strategic push led by large institutions. This may include the following scenarios:

- Led by the government or tech giants such as Naver and Kakao, it will be seamlessly embedded into existing payment or remittance backends.

- Promoted by mainstream exchanges, the Korean won stablecoin replaces the physical Korean won as the core transaction medium.

- The platform will launch innovative incentives or small payment functions based on stablecoins.

However, before these scenarios can be realized, the market faces a series of deep structural obstacles.

The core dilemma of development: legislative vacuum and corporate caution

The primary bottleneck currently is the significant delay in legislation . Despite a backlog of five relevant bills before the South Korean National Assembly, legislative progress remains extremely slow. Based on current projections (October 2025), even if the Financial Services Commission (FSC) submits a government proposal on time, the relevant laws would not officially take effect until early 2027 at the earliest. Until then, no company will be able to legally and scalably operate stablecoin businesses within the legal framework.

This regulatory uncertainty has directly led to divisions and widespread caution in the Korean business community:

- Small businesses : They show an active willingness to participate, but their activities are more for public relations effects and market voice. They generally lack the capital, compliance and technical capabilities required to operate stablecoin businesses on a large scale.

- Large corporations (chaebols) have generally adopted an extremely cautious "wait-and-see" strategy. Their core considerations are twofold: first, the legal risks are too high; second, they assess that the actual commercial returns from turning to blockchain technology in a highly inward-looking domestic market are not sufficient to attract the massive investment of resources.

Currently, all activities surrounding the Korean won stablecoin remain at the surface stage of theoretical discussion and trademark application.

Four major structural barriers

In summary, the difficulties faced by the Korean won stablecoin can be attributed to four interrelated structural obstacles:

- The battle of technology paths: private vs. public chains. Regulators like the Bank of Korea and the FSC, primarily concerned with risk control, strongly favored the initial issuance of the stablecoin on a "customized, Korean-style private blockchain." However, this concept was widely considered disappointing by the industry. Not only did it violate the core values of blockchain—openness, permissionlessness, and interoperability—it also risked further fragmenting the Korean financial system into multiple, disconnected private networks, creating inefficient "walled gardens."

- The dual constraints of the reserve asset market: scarcity and low yields . The business model of stablecoins is fundamentally based on reserve assets. South Korea faces a dual challenge here: First, its domestic financial market lacks short-term government bonds with maturities under one year , making it deprived of the ideal and safest reserve asset class for stablecoins. Second, even with alternative assets like currency-stabilized bonds, the market size and liquidity are insufficient to support large-scale stablecoin issuance. More critically, the yield of the South Korean bond market, approximately 2%, is far lower than the approximately 4% in the United States. This significantly reduces the profitability of stablecoin operations for issuers , making them commercially unattractive.

- The South Korean government's widely held view that public chains are too risky and difficult to regulate is, to some extent, a misunderstanding of existing technology. In reality, through well-designed smart contracts, effective oversight and compliance control of user identity authentication (KYC) and capital flows can be achieved on open public chains.

- The fundamental problem of this collective lack of vision and urgency lies in the fact that no key player, from the government to financial institutions to large corporations, has articulated a clear goal or concrete plan for the future of the Korean won stablecoin. The entire market has fallen into a strategic stagnation of "collective waiting." However, the evolution of global blockchain finance won't wait for latecomers. If South Korea waits until 2027 to launch its stablecoin on a closed, private blockchain, it will find itself significantly behind the world.

Hong Kong dollar stablecoin

The development of stablecoins in Hong Kong presents a complex landscape characterized by a three-pronged game of clear local regulations, active market participation, and prudent supervision from mainland China. Currently, Hong Kong is at a critical turning point. After an initial period of overheating, the market is entering a new phase of "local cooling" and structural differentiation.

Despite market volatility, Hong Kong's official stance remains firm. Financial Secretary Paul Chan has publicly stated that applications for compliant stablecoin licenses are proceeding according to the established framework, with the first batch of licenses expected to be issued in early 2026, as planned.

Hong Kong's proactive layout and the initial overheating of the market

Hong Kong’s strategic goal of becoming a leading global virtual asset hub is clear. To this end, the Hong Kong government has implemented a series of proactive and well-paced measures:

- March 2024 : Launch of the stablecoin issuer “sandbox”, providing the market with a regulated testing environment.

- August 1, 2025 : The Stablecoin Regulations are officially implemented, establishing the world's first comprehensive and clear legal framework for stablecoin regulation.

This leading regulatory certainty significantly stimulated market enthusiasm, attracting over 77 companies to express their intention to apply, which at one point made the market appear "overheated." However, the overwhelming rush of Chinese-backed financial institutions to participate has drawn the cautious attention of mainland regulators.

Prudent intervention by mainland regulators

The core concern of the recent "window guidance" issued by mainland regulators to relevant Chinese-funded institutions is not to stifle innovation, but is based on the following considerations:

- Risk isolation : ensuring that potential risks of Hong Kong’s virtual asset business will not be transmitted back to the mainland’s large and strictly regulated parent financial system through equity relationships.

- Capital control : Strictly prevent mainland funds from flowing into Hong Kong's virtual asset market through non-compliant channels.

- Market order : Chinese institutions are required to keep a low profile and avoid excessive publicity or creating hot topics to prevent irrational overheating of the market.

This tension between " Hong Kong's global ambitions " and " mainland China's financial prudence " is the core background for understanding the current dynamics of the Hong Kong dollar stablecoin market.

Market status: local cooling, expected slowdown, structural differentiation

The intervention of mainland regulators has had an immediate impact on the market. The current situation can be summarized as follows:

- The first wave of withdrawals has emerged : Before the official application deadline of September 30th, at least four Chinese financial institutions, including Guotai Junan International, have publicly announced their withdrawal from stablecoin license applications or have suspended RWA-related activities. Market expectations are that some previously active Chinese banks (such as Bank of China (Hong Kong)) may also postpone their applications.

- Shifting strategies to "do, don't talk" : Mainland China's regulatory guidance doesn't entail a blanket ban, but rather a requirement to "keep a low profile." This has forced Chinese institutions to shift their strategies from their early high-profile forays to more cautious internal research and quiet planning.

- Market structure divergence : This round of cooling is localized and asymmetric . Affected entities are highly concentrated among Chinese-funded institutions. Meanwhile, Hong Kong and other international financial institutions continue to advance their virtual asset businesses in an orderly manner within the existing legal framework.

- Expected licensing rhythm : The market generally expects that the first batch of licenses will follow a prudent rhythm similar to that of VASP exchange licenses, that is, only a very small number of licenses (possibly only one or two) will be issued by the end of 2025 or the beginning of 2026, and then gradually relaxed according to market development.

The strategic dilemma facing the Hong Kong dollar stablecoin

- Uncertainty under the influence of mainland regulations : This is the core dilemma at present. Chinese institutions are an integral part of Hong Kong's financial market. Their collective "holding back" or "low-key" approach will undoubtedly affect the market size, liquidity depth, and breadth of application scenarios of the Hong Kong dollar stablecoin in its initial launch. Hong Kong authorities need to strike a delicate balance between promoting market openness and addressing mainland regulatory concerns.

- The tension between development pace and global competition : Compared to the "overall heating up" of the US market, Hong Kong, influenced by mainland China, has adopted a more restrained and cautious development pace. While this steady pace helps control risks, it also presents the risk of missing the window of opportunity and falling behind competitors in the global race for financial innovation.

- Balancing Risks and Rewards : The intervention of mainland regulators is essentially forcing Chinese institutions to reassess the risk-reward balance of being "first movers." While early adopters enjoy the greatest policy dividends and first-mover advantages, they also bear the highest market and compliance trial-and-error costs.

Japanese Yen Stablecoin

Japan's stablecoin development path is a top-down, carefully designed financial infrastructure reform by the government, within its unique macroeconomic context. Its core driving force is not private speculative demand, but rather the urgent need to address the country's long-standing structural economic difficulties, including low interest rates, low growth, and deflationary pressures. Stablecoins are highly anticipated as a policy tool that can improve financial efficiency, stimulate capital flows, and inject new impetus into a weakened domestic payment system and illiquid government bond markets.

To this end, the Japanese government has established what is arguably the world's most rigorous regulatory framework for stablecoins, passing a series of legislation, including the Revised Financial Debt Law. Its strategic intent is clear: to transform stablecoins from mere "cryptoassets" into "financial infrastructure" serving national strategy .

From theory to practice: the launch of the first compliant product

At present, Japan's stablecoin market has officially entered the "commercial practice period" from the "theoretical preparation period".

- Landmark event : Fintech startup JPYC Inc. has received regulatory approval to issue the first fully compliant Japanese yen stablecoin "JPYC" in the fall of 2025.

- Key Collaboration Model : This issuance reveals a model for market entry in Japan: "technological innovation from a startup (JPYC Inc.) combined with the compliance infrastructure of a major platform (Mitsubishi UFJ Trust and Banking Corporation's Progmat Coin)." This demonstrates that regulators are open to innovation, but only if it is anchored within the strong compliance framework of licensed financial institutions.

- Technical Path and Business Ambitions : JPYC plans to be issued on multiple mainstream public blockchains, including Ethereum and Avalanche, demonstrating its commitment to openness and composability while adhering to regulatory compliance. Its goal of issuing 1 trillion yen within three years, as well as its Series A investment from international giants such as Circle, demonstrates its determination to seize market share.

JPYC is not positioned to replace fiat currency, but to serve as the " on-chain yen ", becoming a bridge that seamlessly extends the functions and value of the yen to the global digital economy.

Core application scenarios

- International Remittances and Corporate Settlements : Provides near-real-time, low-cost payment solutions for international students, cross-border e-commerce, etc., and uses smart contracts to simplify B2B payment processes and cross-border fund management between enterprises.

- Building a local Web 3 ecosystem : As a "native liquidity carrier" on the chain denominated in Japanese yen, it provides a stable value medium for Japan's huge Web 3 applications such as games and NFTs, building its underlying financial infrastructure.

Multi-level national strategic intentions

The launch of the Japanese Yen stablecoin carries Japan's multi-level strategic considerations:

- Defensive Strategy: Striving for Digital Currency Sovereignty . This is the most core initiative. By launching a compliant Japanese Yen stablecoin, the goal is to break the monopoly of US dollar stablecoins in the digital world, providing a non-US dollar option for cross-border trade and international settlements in Japan, thereby reducing reliance on traditional systems such as SWIFT.

- This economic strategy: activating the government bond market and innovating monetary policy tools . This is a brilliant design that kills two birds with one stone. By requiring a large allocation of reserve assets to Japanese government bonds (JGBs), not only will a new, structural buyer be created in the government bond market, which has long suffered from insufficient demand, helping to lower government financing costs, but in the longer term, the central bank may even adjust the reserve requirements of stablecoins, using them as a new monetary policy tool to regulate market liquidity.

- Developmental Strategy: Promote the upgrade of financial infrastructure . The approval of JPYC will have a "catfish effect" within Japan's conservative financial system, activating the innovative vitality of local giants such as Sony and Mizuho, promoting the modernization of the domestic payment system, and securely connecting the Japanese financial system to the global Web 3 ecosystem in a highly compliant manner, preventing it from falling behind in the next round of digital finance.

Challenges and the Demonstration Effect of the "Japanese Model"

- Business model challenges : In a zero-interest environment, the traditional profit model relying on interest from reserve assets is completely ineffective. This requires issuers to quickly achieve a large issuance scale and maintain operations through economies of scale through "small profits but quick turnover."

- The ultimate risk prevention and control framework :

- Legal characterization : Stablecoins are strictly defined as "electronic payment tools", fundamentally stripping away their speculative attributes.

- Entity limitation : Issuers are limited to licensed financial institutions such as banks and trust companies.

- A unique "asset top-up clause" mandates that issuers use their own capital to cover any depreciation in reserve assets. This robust constraint, unseen in European and American regulatory frameworks, significantly safeguards user asset security.

- Mandatory AML/KYC checks .

In summary, the "trust-based," "strongly regulated," and "semi-centralized" stablecoin model pioneered by Japan achieves the ultimate in security and compliance. It provides a valuable reference model for other Asian economies like Hong Kong and South Korea, which also prioritize financial stability, and has the potential to lead the entire East Asian region in forming a new regulatory consensus on the path of "compliant stablecoins."

About Movemaker

Movemaker, authorized by the Aptos Foundation and co-founded by Ankaa and BlockBooster, is the first official community organization dedicated to promoting the development of the Aptos ecosystem in the Chinese-speaking region. As the official representative of Aptos in the Chinese-speaking region, Movemaker is committed to building a diverse, open, and prosperous Aptos ecosystem by connecting developers, users, capital, and numerous ecosystem partners.

Disclaimer:

This article/blog is for informational purposes only and reflects the author's personal views and does not necessarily represent the views of Movemaker. This article is not intended to provide: (i) investment advice or a recommendation; (ii) an offer or solicitation to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. Holding digital assets, including stablecoins and NFTs, carries a high degree of risk and carries significant price volatility, potentially becoming worthless. You should carefully consider whether trading or holding digital assets is appropriate for you based on your financial circumstances. If you have questions regarding your specific situation, please consult your legal, tax, or investment advisor. The information provided in this article (including market data and statistics, if any) is for general informational purposes only. While reasonable care has been taken in preparing these data and charts, no liability is assumed for any factual errors or omissions contained therein.

- 核心观点:美元稳定币正加速全球扩张。

- 关键要素:

- 跨境支付月结算量超600亿美元。

- 高通胀国家推动货币替代需求。

- 美债需求新增数千亿美元。

- 市场影响:巩固美元霸权,重塑全球支付格局。

- 时效性标注:长期影响