Regulatory easing narrows the path ahead for Hyperliquid?

- Core Viewpoint: The US CFTC’s approval of perpetual contracts legalization brings regulatory clarity for on-chain protocols like Hyperliquid, but it also triggers pushback from traditional giants like CME. Hyperliquid faces three paths: staying offshore, full compliance, or squeezing through the “narrow gate” of seeking decentralized approval. Its future hinges on the balance between decentralization and regulatory accountability.

- Key Elements:

- On May 29th, the CFTC approved Kalshi's BTCPERP perpetual contract and allowed Coinbase to onboard US clients via a Bermuda entity, effectively “stamping” approval on the model and removing regulatory uncertainty.

- Hyperliquid, leveraging HIP-3 protocol, launched perpetual contracts for traditional assets like stocks and crude oil, directly threatening CME and ICE's core business, prompting the latter to lobby Congress for mandatory KYC and AML requirements.

- Hyperliquid faces an “accountability dilemma”: its closed-source nature and concentrated node structure lack a regulated legal entity. The recent SPACEX contract flash crash exposed the risk of being unable to assign responsibility.

- The CFTC’s new policy is not a formal rule; it is implemented via policy statements and “no-action letters,” which have a weak legal foundation. The next chairperson could overturn it, posing a risk of policy reversal.

- The “8-prong decentralization test” in the future Clarity Act could offer a compliant “narrow gate” for Hyperliquid without requiring a clearinghouse license, but it needs to accelerate network decentralization.

In the past few days, the world's largest on-chain perpetual contract platform by trading volume has been undergoing a rare value discovery.

This platform is called Hyperliquid, and its token valuation has already surpassed Solana, closing in on BNB. At least in terms of token price, its competition with CEXs like Binance is no longer lagging behind.

But a sword has always been hanging over Hyperliquid's head.

At the end of May, the CFTC approved the first compliant perpetual contracts within the United States for the first time. Many saw this as yet another victory for Hyperliquid, unaware that the clarification of the rules actually signals that a group of more powerful enemies are on their way, and a protracted war has already begun.

The CFTC's Amnesty for Contracts

On May 29, the CFTC approved Kalshi to list BTCPERP, the first true Bitcoin perpetual contract. On the same day, it issued a no-action letter to Coinbase's CFM, allowing the latter to connect US clients to global options and perpetual contracts, routed through Coinbase's Bermuda entity, treated as "foreign futures." It also permitted clients to use Bitcoin, Ethereum, and stablecoins as margin. Supporting actions included a commission policy statement on listing perpetual contracts, related interpretive guidance, and a staff guide covering 7×24 trading, clearing, and settlement.

CFTC Chairman Selig wrote in a column that the existence of perpetual contracts was never the issue; the real question is whether they operate under US regulation, standards, and the rule of law, or are driven offshore to grow unchecked. Trump took credit on Truth Social, claiming that the previous administration's "anti-crypto army" nearly destroyed the US crypto industry, and that he saved it.

Hyperliquid's policy advocacy group, the Hyperliquid Policy Center, welcomed this while expressing hope that the framework would cover not just centralized intermediaries but also on-chain protocols that handle a significant volume of perpetual contract trading.

Hyperliquid's biggest critic, former Multicoin partner Kyle, poured cold water on the Hyperliquid community: "What you have now is a guarantee that a regulated US company will never distribute Hyperliquid liquidity."

So, what does the CFTC's approval actually mean for Hyperliquid?

Offending CME is Scarier than Offending Binance

A perpetual contract is a futures contract with no expiry date. Traditional futures must be settled or rolled over upon expiry. Perpetual contracts don't expire; they use a "funding rate" to maintain balance, where long and short positions periodically pay each other a fee, keeping the contract price anchored to the spot price. This allows traders to hold a directional position long-term with less capital in a 7×24 market, which is why they are far more popular in crypto than traditional futures.

As anyone who frequently opens trading platforms knows, to legally operate a perpetual contract trading platform in the US, you need three types of businesses and licenses: DCM (Designated Contract Market) for the trading platform itself; DCO (Derivatives Clearing Organization) for the clearinghouse, which acts as the central clearing counterparty; and FCM (Futures Commission Merchant) for the intermediary broker. All three are indispensable.

However, the entire regulatory framework for operating a trading platform, when originally designed, excluded venues like Hyperliquid—which lack DCO status—from the access list of brokers. This is because these Perp DEXs, by their very nature, don't rely on a "clearinghouse."

Before this policy change, to compliantly list perpetual contracts, Coinbase first acquired a trading platform holding a DCM license, then used the clearinghouse Nodal Clear, forcing the product into a five-year, cash-settled futures contract, using the clearinghouse's cash adjustments to simulate the funding rate.

The CFTC's new policy hasn't touched the current framework that relies on "centralized clearinghouses."

Hyperliquid's new "clearinghouse-less" model has faced opposition from two giants in the traditional financial industry.

According to Bloomberg, the Chicago Mercantile Exchange (CME) and ICE, the parent company of the New York Stock Exchange, have been conducting "concern lobbying" on Capitol Hill. Their core demand is to force Hyperliquid into the DCM registration framework, mandate KYC and AML, and increase transaction monitoring and position limits.

CME and ICE are not players in the crypto world. CME's foundation is in commodities and equity index futures—crude oil, gold, agricultural products, interest rates, stock indices—these contracts have been its cash cows for decades; ICE holds a series of exchanges, including the NYSE. Hyperliquid initially only did perpetual contracts for crypto assets, staying out of their turf.

What truly crossed the line for Hyperliquid was the subsequent creation of markets like TradeXYZ, built on its native protocol "HIP-3." With HIP-3, anyone can list new perpetual contracts on top of Hyperliquid's underlying liquidity. The underlying assets can be stocks, or real-world assets like crude oil and gold. During the Iran conflict, trading volumes for crude oil and gold perpetual contracts on TradeXYZ surged. Hyperliquid effectively moved CME's most profitable business onto the chain, with 7×24 trading, permissionless access, and on-chain settlement.

TradeXYZ's open interest continues to grow

Offending CME is scarier than offending Binance.

Another recurring concern is the question: "Who takes the blame?"

Regulators instinctively seek an accountable entity: if something goes wrong, whom do they subpoena, whom do they penalize? In the traditional framework, the regulated entities are tangible intermediaries like FCMs, DCOs, and DCMs. But under the banner of "decentralization," the question of "who takes the blame" remains a legal void.

Hyperliquid is caught in the middle; it's closed-source, initially had only a few validator nodes deployed in the same location, far from being "unaccountable," yet it doesn't have a clear legal entity standing at the forefront like a traditional exchange.

Not long ago, the SPACEX-USDH pre-IPO contract on Hyperliquid flash-crashed 45% in thirty minutes. An oversized position ate up the thin liquidity, causing losses for many users. The "ADL" mechanism, often criticized in its contract design, inherently harms the interests of some retail investors. A trading platform that "cannot be held accountable" is clearly unacceptable to the CFTC.

Finally, what the CFTC provided this time is not a formal rule but a combination of a policy statement, a "no-action letter," and guidance. It lacks legal force, meaning the next CFTC chairman could overturn everything with a single sentence. Until it becomes a formal rule or congressional legislation, all progress today is merely temporary.

Good News

The product form that Hyperliquid relies on is perpetual contracts with stablecoins as margin. The CFTC's approval essentially stamps the entire model. The question of whether the US would impose a blanket ban on perpetual contracts is no longer a suspense. The biggest cloud hanging over this sector for years has been removed.

The pie itself is still growing. Today, the vast majority of Americans, both retail and institutional, have no idea what a perpetual contract is. Once the compliant channels open up, the scale of market expansion will be measured in orders of magnitude.

A deeper positive comes from the CFTC's regulatory philosophy. The CFTC has never prescribed specific actions; it focuses on principles and outcomes: no market manipulation, no stealing client funds, maintaining market integrity. As long as these principles are upheld, whether you are a traditional exchange or an on-chain protocol, you can theoretically be brought under its regulation. More critically, once the CFTC obtains jurisdiction, it is exclusive—state laws and other regulations automatically give way. For an industry that fears inconsistent regulatory stances, this certainty is indispensable.

Furthermore, the expected Clarity Act includes an "8-prong decentralization test." If a protocol passes this test, it could offer perpetual contract trading services without holding clearing and trading licenses. This leaves a narrow door for Hyperliquid.

The optimistic narrative put forward by well-known trader Ansem has gained recognition from many in the HL community. He stated: "If Hyperliquid becomes the underlying liquidity engine for various financial trading platforms, called upon by countless frontends like AWS is for cloud computing, and its settlement stablecoin is USDC, then every bit Hyperliquid grows is creating demand for the US dollar out of thin air." A pro-crypto government that understands this relationship has no reason not to protect it.

A Fork in the Road

Hyperliquid faces three paths.

First, stay offshore, keeping "Americans out." Maintaining the status quo isn't bad for Hyperliquid; liquidity is still improving, and 7×24 trading and pre-IPO contracts will only increase its attention. But as Kyle said, choosing this path means you are a product that can attract users but can never be legally integrated into the US financial system.

Second, go fully compliant. Hyperliquid has enough capital to buy all the necessary licenses, replicate Polymarket's approach, and create a clean "Hyperliquid US." This would mean sacrificing "decentralization," compromising on the "clearinghouse-centric" framework, and losing offshore liquidity.

Third, continue pursuing decentralization until passing the "8-prong decentralization test" of the Clarity Act. This path is the sexiest but faces the greatest resistance.

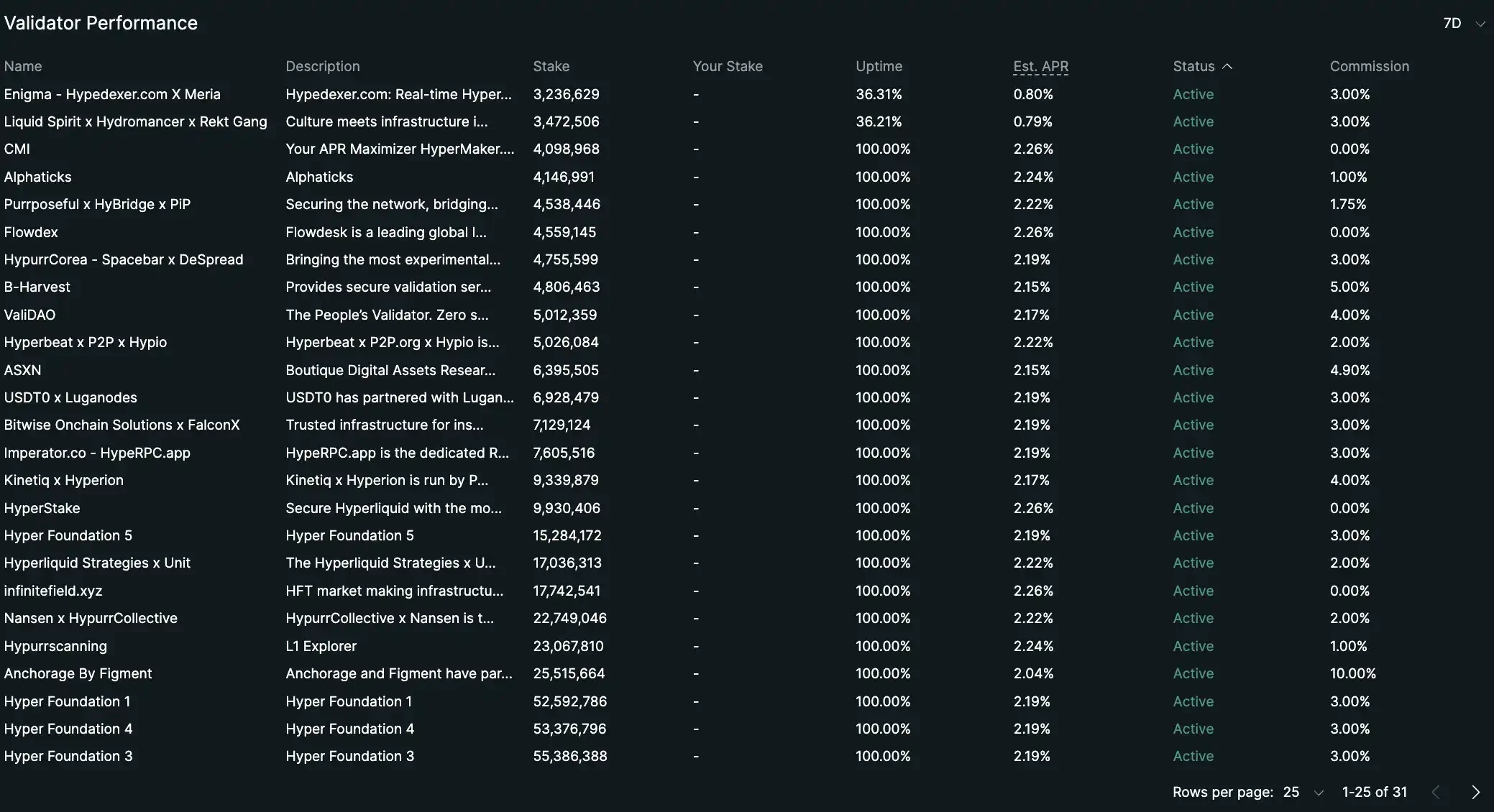

Since its TGE, the number of validator nodes on the Hyperliquid network has grown from single digits to 26, the vast majority belonging to external teams. If Hyperliquid can accelerate its decentralization and walk through this "narrow door," it will become the first perpetual contract market to be accepted into the US compliance system as a pure protocol, without relying on a clearinghouse.

Hyperliquid's validator nodes