如何定義「真實美股」:鏈上代幣、價格合約與券商直連的差異

- 核心觀點:2026年以穩定幣購買美股產品的三種主流模式(代幣化股票、股票永續合約、券商直連模式)在風險收益、法律權利和底層邏輯上截然不同,僅券商直連模式能真正實現持有美股的完整權益,且該模式下合規架構(如接入美國清算體系)是保障用戶資產安全的關鍵。

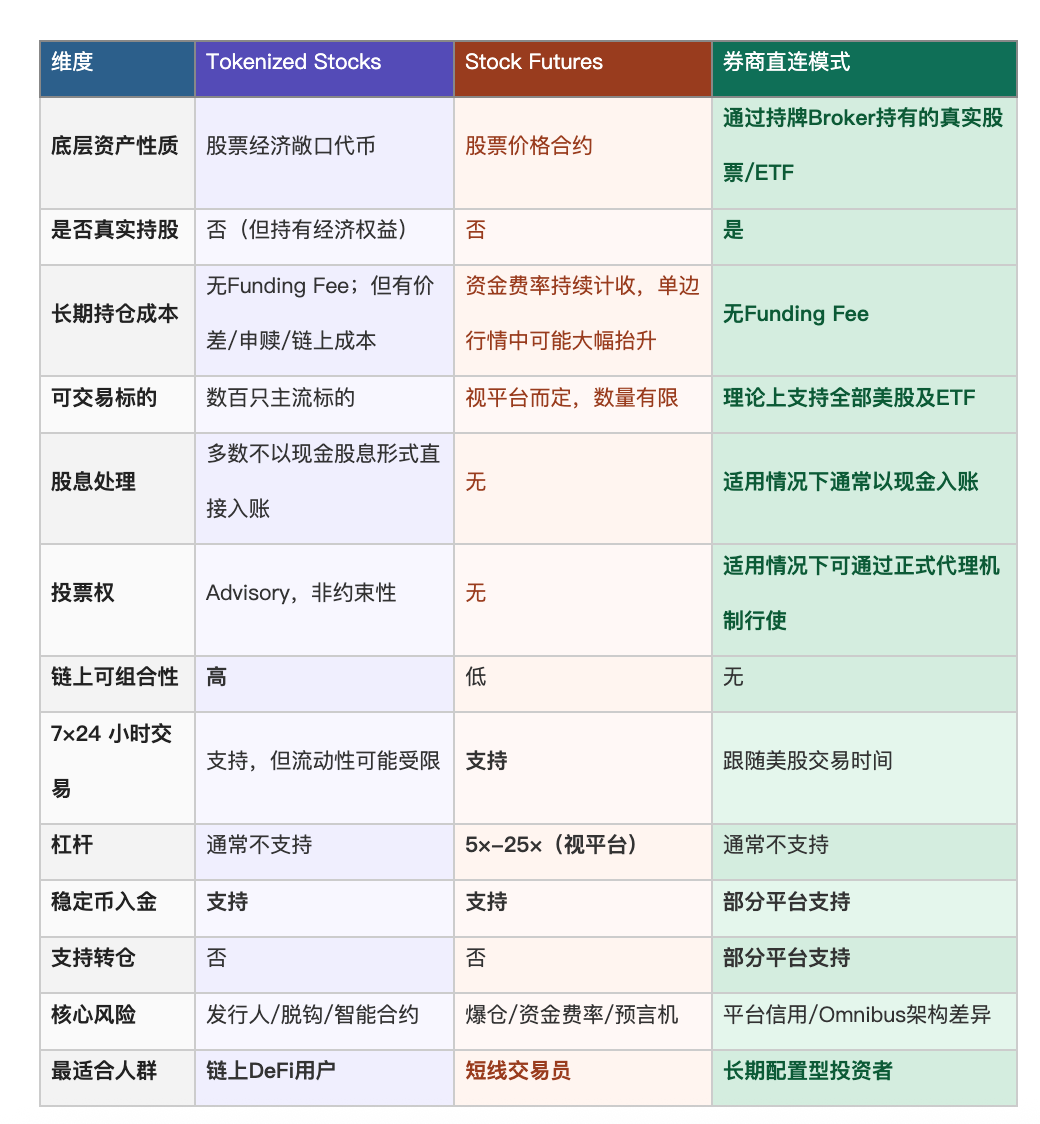

- 關鍵要素:

- Tokenized Stocks(例如 Ondo Finance)持有鏈上經濟映射,股東身份在發行方,支援 DeFi 組合,但權益不完整且股息非現金入帳。

- Stock Futures 追蹤價格,與股票所有權無關,資金費率年化可能超過 100%,適合短週期價格博弈而非長期持有。

- 券商直連模式(例如 BIT)透過持牌經紀商接入 NSCC/DTC 清算體系,是唯一實現真實股權、現金股息和正式投票權的路徑。

- 在券商直連模式中,資產保護取決於底層架構:Fully Disclosed IB 路徑的 SIPC 保護最清晰,Omnibus IB 路徑的保護則透過客戶協議傳導。

- 關鍵差異還包括長期持倉成本:券商直連模式無資金費率,僅含傳統交易成本;Tokenized Stocks 有申贖價差,Stock Futures 則有持續的資金費率。

In 2026, buying US stocks with stablecoins has become a mainstream trend. However, behind the phrase "buying US stocks with USDT," although various products claim to provide users with exposure to the US stock market, they are actually selling completely different assets. Some products convert US stock economic exposure into on-chain tokens; others launch perpetual contracts tracking US stock prices; and yet others provide real US stock trading services through licensed broker-dealers. The risk-return profiles, rights structures, and underlying logic of these three approaches are entirely distinct.

1. Overview of US Stock Trading Platforms

The current mainstream solutions for "buying US stocks with USDT" on the market can be clearly categorized into three types: Tokenized Stocks, Stock Futures, and the Brokerage Direct Access Model.

1. Tokenized Stocks

Tokenized Stocks are typically held by the issuer or its SPV/custodian arrangement. Users hold the economic rights represented by on-chain tokens, not direct shareholder status in a traditional securities account. The most representative issuer, Ondo Finance, has a TVL exceeding $1 billion, supporting over 200 major stocks and ETFs; the overall market size has reached tens of billions of dollars.

2. Stock Futures

Stock contracts are the most efficient trading tools but have the least connection to "holding US stocks" – users buy a price contract with no legal link to stock ownership.

In 2026, several mainstream trading platforms have launched stock-related perpetuals/CFD products, with significant variation in covered assets, leverage multiples, and available regions (approximately 5× to 25×). On-chain platforms represented by Hyperliquid HIP-3 / Trade.xyz are also expanding into the traditional asset perpetuals market, with the core value proposition of allowing global traders to express long or short views on traditional asset prices using stablecoins.

3. Brokerage Direct Access Model

The operational logic of the Brokerage Direct Access Model is similar to traditional brokerages: users execute stock or ETF trades through a Broker-Dealer, with assets held within the U.S. clearing and custody system. It is the only one of the three models that truly results in purchasing the stock itself. However, it's important to note that there are significant differences between platforms operating under this model.

Source: Public Information Compilation

2. Comparison of Differences in US Stock Trading Products

The differences between the three models are not just in trading experience but also in three core dimensions: legal rights, holding cost structure, and regulatory protection.

Source: Public Information Compilation

(1) Tokenized Stocks

The essence of Tokenized Stocks is an "on-chain shadow" of the stock – convenient and composable, but with incomplete rights, as shareholder status resides with the issuer.

On-chain composability is the true differentiated advantage of this model: tokens can be used as collateral in DeFi lending protocols while earning additional yields, can circulate 24/7 on-chain, and can be bought in fractional amounts – things traditional securities accounts cannot do. The limitations are equally clear: shareholder status is with the issuer, not the user; most platforms do not credit dividends directly in cash; voting rights are advisory expressions and not legally binding. While there are no funding fees, subscription/redemption spreads, on-chain gas fees, and market-making spreads also constitute holding costs.

(2) Stock Futures / Equity Perps

Stock Futures are "price betting tools" for stocks – efficient, flexible, 24/7, but funding rates erode holding costs over the long term and are unrelated to actually holding the stock.

Stock Futures are the path most familiar to crypto traders – margin, stop-loss/take-profit, long/short. The operational logic is identical to trading BTC perpetuals, just on a different underlying asset, operating 7×24 hours without market close. The core cost is that funding rates can increase significantly in trending markets, with annualized costs reaching double digits or even over 100%, representing a chronic drain on a "buy and hold" strategy. Once the contract is closed, there are no shareholder rights left, only a USDT profit or loss.

(3) Brokerage Direct Access Model

The Brokerage Direct Access Model is the closest path to "buying stocks" – offering the most complete rights and cleanest long-term holding costs, at the expense of on-chain composability and 24/7 trading.

The Brokerage Direct Access Model offers the most complete rights: real stocks, direct cash dividend crediting, official voting rights (where applicable), and coverage of thousands of stocks. The main limitations are trading hours following the U.S. market open, assets not being on-chain, and inability to integrate with the DeFi ecosystem. It's important to note that differences in brokerage architecture between platforms directly affect how user rights are transmitted, making it worthwhile to understand the specific compliance structure before choosing a platform.

3. Defining "Real US Stock Purchase"

While the three paths have differentiated characteristics and target user groups, for users seeking a convenient way to use stablecoins for long-term US stock allocation, the advantages of the Brokerage Direct Access Model are very direct – every one of its core differentiators precisely addresses the most prominent shortcomings of the other two models, including:

Advantage 1: No Funding Fee, Cleanest Long-Term Holding Cost Structure

Real US stock spot holdings have no concept of funding fees. Holding the same stock for a full year incurs no additional funding fee regardless of market sentiment.

Stock Futures can have annualized holding costs reaching high double digits during strong market trends. Tokenized Stocks have no funding fees but involve spreads and on-chain transaction costs. Comparatively, the holding cost structure of real US stock spots is the cleanest among the three.

Advantage 2: Unmatched Coverage Depth Compared to the Other Two Models

The Brokerage Direct Access Model covers thousands of U.S. listed stocks and ETFs, far exceeding the ~200-260 stocks of Tokenized Stocks and the limited assets of Stock Futures. For users needing exposure to mid-cap companies, sector-specific ETFs, or REITs, the Brokerage Direct Access Model is the more robust stablecoin on-ramp.

Tokenized Stocks and Stock Futures primarily cover popular, high-profile assets, offering almost no choice for mid-cap companies, sector ETFs, or REITs. In terms of asset coverage, the Brokerage Direct Access Model currently has no comparable competitor.

Advantage 3: Real Shareholder Rights – A Difference in Nature, Not Degree

Holding real stocks typically means dividends are credited to the account in cash. Voting rights, where applicable, can be exercised through formal proxy voting mechanisms (specific rights are subject to account structure and regional restrictions).

Stock Futures have no shareholder attributes whatsoever. The so-called "voting" for Tokenized Stocks is merely "expressing preferences to the issuer" and carries no legal weight. The Brokerage Direct Access Model is the only path among the three that offers legally recognized shareholder rights.

Advantage 4: Stablecoin On-Ramp, Reducing Reliance on Traditional Banking Channels

Some brokerage platforms support USDT/USDC deposits and withdrawals, reducing reliance on traditional USD wire transfers. For users without overseas bank accounts, this represents a substantial lowering of the barrier to entry.

Traditional Hong Kong/US stock brokers generally require bank wire transfers, which is troublesome without an overseas account. Supporting stablecoin deposits is the biggest practical advantage of platforms that currently offer this feature.

Advantage 5: Transferable Holdings, Open Exit Path

In the Brokerage Direct Access Model, if the platform supports standard securities transfer mechanisms like ACATS/DTC, users can directly transfer their positions to other licensed brokers without needing to sell and rebuild positions. This means the exit path is open, and users are not passively locked in due to platform changes.

Tokenized Stocks can only be redeemed for stablecoins, and closing a contract leaves only USDT; neither option allows for position transfer. The ability to transfer positions means users are not passively tied to a single platform.

However, the "Brokerage Direct Access Model" is not monolithic. Platforms all claiming to offer "real US stocks" can have vastly different underlying broker architectures – which directly determines where user assets are held, how SIPC protection is transmitted, and whether users can effectively assert their rights if the platform encounters problems.

While US stock trades appear to be executed on the NYSE or Nasdaq, the actual transfer of ownership of funds and securities is determined by the clearing and settlement system under SEC regulation. This system is centered around DTCC: DTC (Depository Trust Company, holding assets worth over $100 trillion) handles the final settlement for virtually all US stock trades.

The core mechanism of this system is CCP novation (Central Counterparty novation) – upon any trade execution, NSCC immediately becomes the central counterparty for all transactions. This CCP mechanism reduces direct counterparty risk from a broker's insolvency. The key is that user assets entering this clearing system share the same underlying infrastructure with clients of large, established brokerages – not on any public blockchain, not within a platform's custom accounts, and not reliant on the platform's own balance sheet.

Currently, there are four mainstream architectures for accessing the clearing system, with differences in capital requirements, client identity disclosure, and SIPC transmission paths:

Source: Public Information Compilation. Note: DVP/RVP are settlement methods commonly used for institutional clients and are not directly parallel to retail brokerage architectures.

For users:

- Fully Disclosed IB: Client identity is fully transparent to the Clearing Broker. The SIPC protection path is clearest, suitable for users who value legal certainty.

- Omnibus IB: The clearer only sees the IB's aggregate position. SIPC protection is transmitted via the Clearing Broker, with the specific path determined by the client agreement – this is a common access model in international cross-border securities services.

- Self-Clearing: Directly holds NSCC/DTC membership, offering the most direct protection, but requires extremely high capital thresholds, typically only available to large, established firms like Schwab, Fidelity, and IBKR.

So, when a platform says it offers "real US stocks," the truly important question to ask is: Through which architecture does it access the U.S. clearing system? At which layer are user assets protected?

Taking BIT (formerly Matrixport) as an example, its compliance architecture is structured in three layers:

- Layer 1, the GMC License, addresses the issue of "whether user assets are segregated." Bhutan's GMC license has strong requirements for segregating client funds from the firm's own assets. User funds are held by an independent custodian and subject to oversight. This means BIT cannot use user stocks for the platform's own financing or positions – this is the first institutional safeguard distinguishing it from less transparent platforms and a prerequisite for "real holding."

- Layer 2, the Omnibus IB Architecture, addresses the core issue of "where user assets actually are." BIT accesses the NSCC clearing and DTC depository/custody system through two U.S. licensed clearing brokers. Both institutions can be independently verified via FINRA BrokerCheck: the US stocks users purchase through BIT are ultimately held in custody with these two institutions, not in BIT's own accounts or internal ledger. The assets share the same U.S. securities clearing and custody infrastructure as the clients of Schwab and Fidelity.

- Layer 3, SIPC Protection, addresses the "worst-case scenario safety net." Since BIT's clearing brokers are SIPC members, this layer of protection can be transmitted to end-users through the account structure and client agreements via the Clearing Broker, providing a statutory floor of protection (the specific transmission path is subject to the client agreement).

Source: Public Information Compilation

4. Conclusion

Buying US stocks with USDT represents three fundamentally different assets behind the three paths. Tokenized Stocks hold on-chain economic exposure, with shareholder status residing with the issuer. Stock Futures track prices and have nothing to do with owning stock. The Brokerage Direct Access Model is the only path to truly owning the stock itself – offering the most complete rights and the cleanest long-term holding costs. Even within the Brokerage Direct Access Model, architectural differences determine the actual level of asset protection. The transparency and public verifiability of the underlying clearing institutions and compliance architecture are worth carefully investigating before choosing a platform.

This article is for educational and informational purposes only and does not constitute investment advice. It should not be construed as a recommendation to buy, sell, or hold any security or financial instrument. All investments involve risk. Readers should conduct their own thorough research and consult a licensed financial advisor before making any investment decisions.