「股神」特朗普3642笔交易披露:政策与仓位的「完美闭环」

While handling the Iran war, he also placed 3,642 orders in his U.S. stock account.

That was Trump's Q1.

At the same time, he was dealing with tariffs, negotiating trade agreements, and signing executive orders. Last Thursday, the U.S. Office of Government Ethics website released a 113-page document. A handwritten note on the cover indicated that the filer had paid a late fee. The world's most closely watched trading disclosure was finally made public.

That same week, the U.S. Congress was advancing a bill to prohibit officials from trading stocks. According to Axios, the relevant proposal has garnered signatures from over 120 lawmakers, with versions in both the Senate and the House, and public support exceeding 70%.

But the biggest loophole in this bill is that it cannot regulate the President.

The White House's response was also familiar. The President's assets are managed by his children, and trades are executed by account managers, fully complying with all requirements of the U.S. Officials Stock Trading Disclosure Act, with no conflict of interest. This statement has been repeated many times over the past year. Every time new details emerged, it was repeated again. The frequency of repetition itself became a form of information.

A person who can influence tariffs, trade, industrial subsidies, crypto regulation, and market sentiment also maintains a substantial U.S. stock account.

The disclosure document says the trades are compliant. What the market really wants to see is what he actually bought, how much he made, and whether these stocks are aligned with his policy direction.

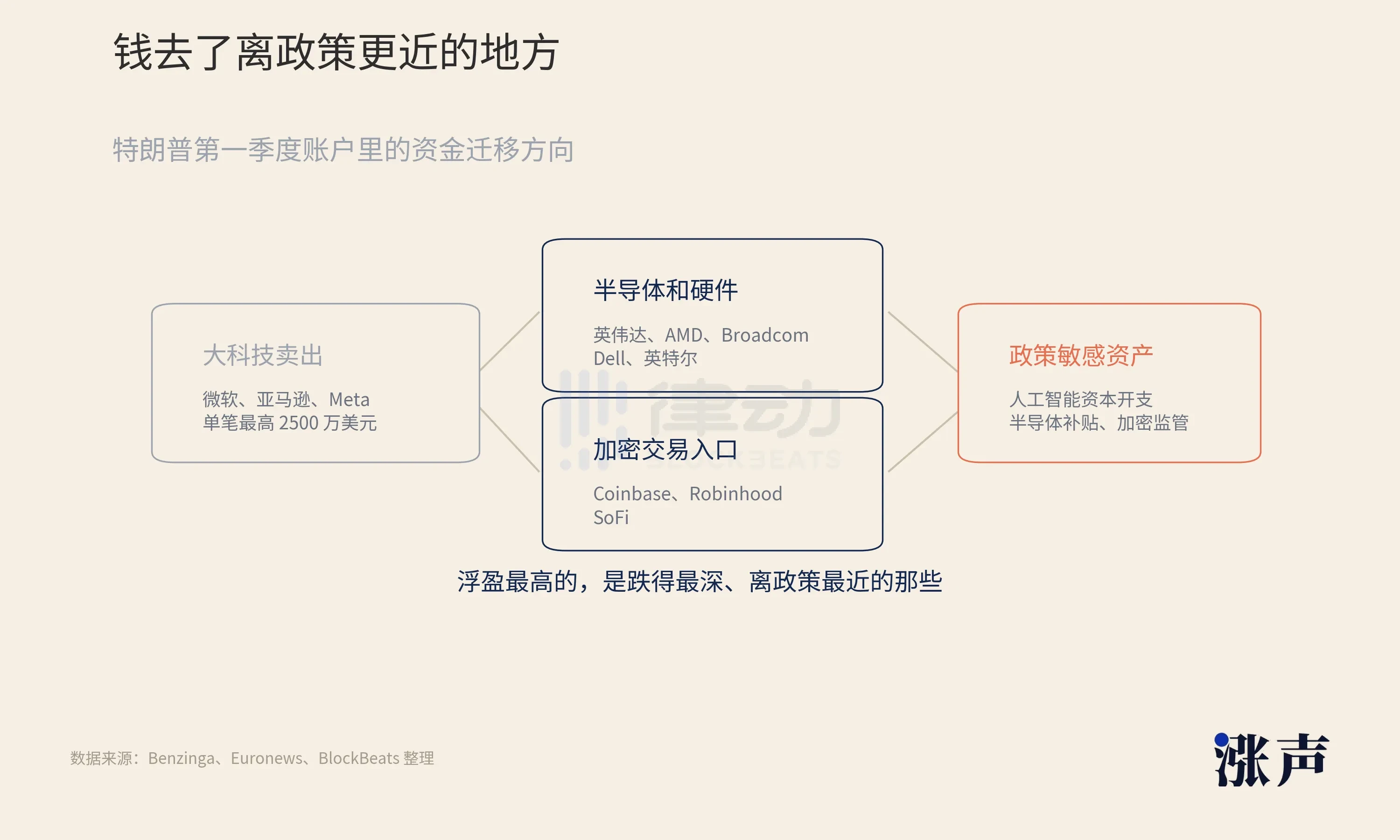

Money Flowed Out of Big Tech, Into Areas Closer to Policy

Federal disclosure rules only require value ranges, not exact prices or actual gains/losses.

After page-by-page verification of Trump's scanned document, Benzinga estimated purchases of approximately $2.4 million to $6.6 million in Nvidia, $2.4 million to $8.1 million in Microsoft, $2.5 million to $8.3 million in Amazon, and $2.2 million to $10.6 million in Oracle.

Big Tech saw a different set of moves.

The largest sell orders were for Microsoft, Amazon, and Meta, with individual transactions reaching up to $25 million. For these same companies, holdings were established early in Q1 and sold later, with buys and sells appearing interchangeably in the statements. Money exited Big Tech and flowed into semiconductors and the AI hardware chain.

Nvidia, AMD, Broadcom, Dell, and Intel were the most frequently occurring names on this list. Also present were Coinbase, Robinhood, and SoFi. The position-building timeframe fell within the window of discussions about the federal Bitcoin reserve and the successive introduction of the "Trump Account" retirement plan.

According to Euronews statistics, if holdings were maintained until the disclosure date, stocks with unrealized gains exceeding 100% included AMD, Intel, Marvell, SanDisk, Seagate, and others.

The stocks with the highest unrealized gains were those that had fallen the deepest and were closest to policy.

In this set of trades, Big Tech still formed the core holdings. Microsoft has enterprise software and cloud services, Amazon has cloud computing and advertising, Meta has advertising cash flow and AI recommendation efficiency, and Oracle has databases and cloud infrastructure. They are the most natural names for U.S. stock funds to re-enter when returning to risk assets.

The incremental movement was in the hardware chain.

Nvidia is the center of GPU supply, AMD is the second option, Broadcom provides custom chips and data center networking, and Dell delivers complete AI server systems. For every additional GPU cloud providers buy, companies on this chain receive one more order. Big Tech money bets on the valuation logic of platform companies, while hardware chain money bets on those who receive payments first when AI capital expenditure materializes.

In comparison, Dell represents the cleanest timeline case among these.

On February 10, 2026, the Trump account established a position in Dell, valued between $1 million and $5 million. On May 8th, at a White House event, Trump publicly praised Dell's hardware products, causing Dell's stock to rise approximately 12% that day. Six days later, the trading disclosure was released.

There's also background context along the same line. The Dell family had previously committed $6.25 billion to the "Trump Account" retirement plan. Each link in this chain is legal when viewed individually, as confirmed by the U.S. Officials Stock Trading Disclosure Act.

Furthermore, no one is under investigation.

This is another aspect that distinguishes the Trump account from typical politician trading. For ordinary officials' stock disclosures, readers look to see if they timed a policy direction. Trump's disclosure adds another layer. He isn't just betting from the sidelines of the market; his public activities, policy projects, and industry relationships themselves become part of market pricing.

The Dell line is short and complete.

The account bought first, the White House spoke later, the company's stock price rose that day, and family funds subsequently entered Trump's policy project. It doesn't need to prove any single link is illegal for the market to treat it as a textbook example of politician trading.

Intel Became an "American State-Owned Enterprise"

There's one trade in the U.S. stock account, but it's not in Trump's personal account.

In August 2025, the CHIPS and Science Act still had $5.7 billion in subsidies unallocated for Intel, plus $3.2 billion from the "Secure Enclave" program, totaling $8.9 billion.

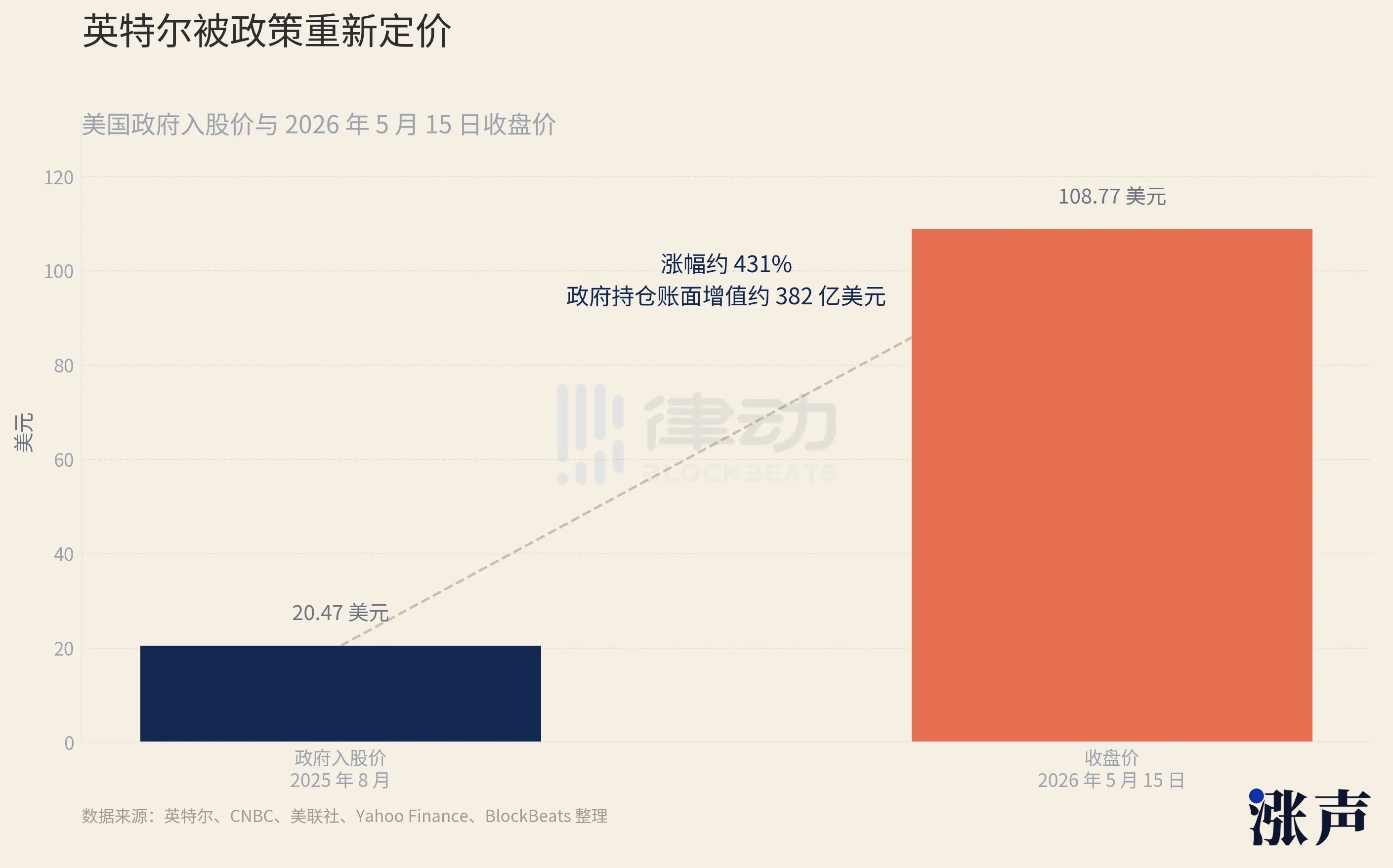

The Trump administration converted this subsidy into equity: 433.3 million shares of Intel common stock at $20.47 per share, acquiring approximately a 9.9% stake. The U.S. government became Intel's largest shareholder, officially designated as a "passive investor" without demanding a board seat.

This wasn't a provision designed in the CHIPS and Science Act. Subsidies were intentionally structured as non-equity to ensure the government gave money but didn't interfere in corporate governance. Taking money was acceptable; holding shares was not. Because holding shares gives the government a financial interest in the company's future, making it difficult to remain detached.

Trump changed the rules.

Before this transaction, Intel's stock price had languished below $20 for nearly a year, with declining revenue and lagging process technology. The market's assessment was of a company losing competitiveness. After the government stepped in, a new variable was added to Intel's valuation: the U.S. government would not let this company fail.

This assessment doesn't fit into a discounted cash flow model, but the market can price it in.

Chip manufacturing is a national strategy. The largest shareholder will not stand idly by. Intel's tail risk was curtailed by policy from this point onward. Trump's personal account position in Intel was established in early March 2026, six months after the government completed the transaction.

By then, Intel had exceeded earnings expectations for six consecutive quarters, AI inference demand was driving CPU order recovery, rumors of Apple contract manufacturing persisted, and the fundamental recovery narrative was becoming self-sustaining. By May 15, 2026, Intel closed at $108.77. From the government's entry price of $20.47, the increase was approximately 431%, and the government's holding had gained about $38.2 billion in book value.

First, use taxpayer money to provide a backstop; then, use your own money to follow suit. This statement sounds harsh, but it highlights the sensitivity of the Intel case.

Public information already exists, and Trump's personal account purchase of Intel may not necessarily involve non-public information. The problem is that when the government has pushed a company to the center of national strategy, and the President's personal account appears alongside the same company, it becomes difficult for the market to view it merely as an ordinary investment.

The community calls Intel an "American State-Owned Enterprise" (SOE). Joking aside, there's a very realistic judgment behind it.

It differs from traditional SOEs, but when the government spends $8.9 billion to become the largest shareholder, Intel is placed within the policy framework of American manufacturing, supply chain security, AI computing sovereignty, and semiconductor subsidies. What investors are buying, besides Intel's next quarter's profit, is the expectation that the U.S. government won't let it fail.

This is also why Intel is more important than Dell.

Dell represents a clear individual stock timeline.

Intel represents an institutional timeline. Starting with the conversion of subsidies into equity, it connects industrial policy, government financial interests, personal holdings, and market pricing.

In the past few years, the logic behind tracking the Pelosi family's trades has always been singular: policymakers knew something in advance, so they bought in advance. That was unidirectional causation: policy generates information, information creates trading opportunities, officials front-run.

Intel is different. The key point here extends beyond knowing a policy in advance; the government itself directly becomes part of the trade. Subsidies, equity, manufacturing reshoring, AI computing power, personal accounts – all converging on the same company.

This case explains why the batch of AI hardware and semiconductor assets in Trump's account is so important.

Nvidia and AMD are compute chips, Broadcom is networking and custom chips, Dell is server systems, and Intel is domestic manufacturing backed directly by the U.S. government.

These seemingly diversified holdings all point in the same direction. The U.S. market is buying into AI capital expenditure, the U.S. government is buying into domestic semiconductor capability, and the Trump account appears alongside these assets.

The Closed Loop: Positions and Policy Propel Each Other Forward

Tracking the U.S. stock accounts of politicians is something the market has done for many years.

The Pelosi family's trades have been tracked for a long time, the logic always simple. Policymakers knew something in advance, so they bought in advance. Policy generates information, information creates trading opportunities, officials profit from the timing advantage.

This logic has a legal framework to deal with it. The U.S. Officials Stock Trading Disclosure Act was created for this purpose.

Trump's U.S. stock account adds another layer, and it's more difficult to handle.

Holding Intel gives him a financial incentive to maintain semiconductor subsidies. Holding Coinbase and Robinhood incentivizes advancing crypto legalization. Holding the AI hardware chain incentivizes continued expansion of data center capital expenditure. Holding broad-based index funds and Big Tech incentivizes maintaining overall risk appetite in the U.S. stock market.

When the account and policy move in the same direction, the two reinforce each other. Over time, it becomes difficult for outsiders to distinguish which is driving which.

Policy influences holdings; holdings, in turn, influence policy preferences, and then policy further increases the value of the holdings. Once this cycle starts, it's hard for outsiders to determine, in any specific decision, whether financial interests played a role and to what extent.

This is the core reason past presidents insisted on using blind trusts. Money is placed in a trust, the holder doesn't know what they own, and when formulating policy, there is no financial bias. Disconnecting this feedback loop is the fundamental premise of institutional design.

Trump doesn't have this.

The CHIPS and Science Act originally designed subsidies as non-equity precisely to prevent the government from losing its detachment after becoming a shareholder. Trump converted them into equity, the government took 9.9%. Six months later, his own account also entered Intel. Now, the direction of semiconductor subsidy policy and the market value of his two accounts are aligned.

The U.S. Officials Stock Trading Disclosure Act governs officials trading on non-public inside information.

Most of the information here is public. The problem is that decision-making power and financial interests are bundled in the same person. The current rules have no means to constrain this bundling; they only require the results to be reported.

On April 9, 2025, he posted that it was a great time to buy. Less than four hours later, Trump announced a tariff pause, and the S&P 500 rose 9.5%. University of Washington law professor Kathleen Clark later said, "He is signaling that he can manipulate the market with impunity."

A year later, the account emerged.

The Dell family invested $6.25 billion into the "Trump Account." Trump established a Dell position in Q1, publicly endorsed Dell at the White House in Q2, Dell rose about 12% that day, and six days later, the transaction records entered the public file.

Everyone in this chain got what they wanted.

The market got a story explaining the stock price. The company got exposure from the White House. The Trump account got unrealized paper gains. The policy project got corporate family funding.

The 113-page disclosure document can tell you what he bought, but it doesn't tell you that policy influences holdings, and holdings, in turn, influence policy.