Deconstructing the tradeXYZ Pricing Mechanism: How Do They Price Assets in Advance?

- Core Thesis: This article provides a detailed analysis of how tradeXYZ, an on-chain perpetual contract protocol, achieves self-sufficient pricing for traditional assets like crude oil and stock indices during periods when conventional markets are closed. It does so through a parametric pricing system consisting of oracle tracking speed, price discovery boundaries, and funding rate scaling factors. The article points out that this decentralized model is disrupting traditional finance's pricing power but also introduces deep-seated risks, such as accountability for parameter decisions.

- Key Elements:

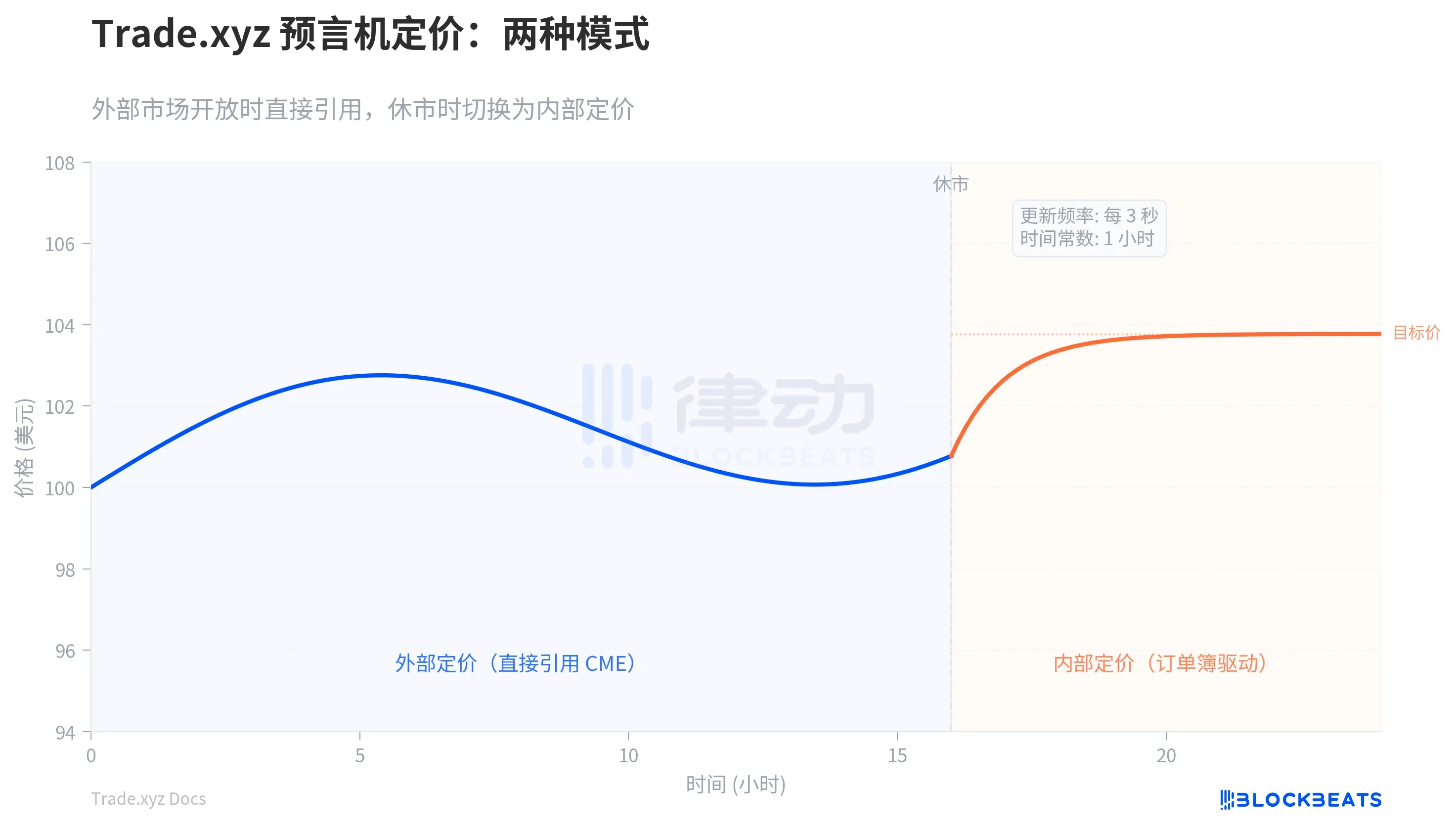

- When traditional exchanges like the CME are closed, tradeXYZ calculates the "impact price differential" from order book information and slowly converges toward the target price (the time constant has been reduced from 8 hours to 1 hour), achieving continuous on-chain pricing.

- To prevent infinite price divergence, the system sets a "price discovery boundary" (cage), which limits the mark price to a certain percentage (the inverse of the maximum leverage) above and below the last external closing price. The v2 version introduces the ability for the cage to move, thereby reducing the opening gap.

- A funding rate scaling factor of 0.5 reduces the annualized rate from 11% to approximately 5.5%, aligning it with the actual carrying costs of traditional assets and lowering the holding costs for traders on the correct side of the market.

- The protocol uses differentiated pricing for various assets: index contracts dynamically calculate discount rates, while Korean individual stocks require the addition of the USD/KRW exchange rate to prevent futures rollovers and exchange rate fluctuations from causing false profits or losses for holders.

- During extreme market conditions, the system relies on external market makers to provide liquidity. If no one takes the other side, it triggers ADL (Auto-Deleveraging) to forcibly close the most profitable opposing positions, rather than relying on the treasury to cover losses.

- This pricing system has been stress-tested during real geopolitical crises (e.g., on March 9, when the escalation of the Iran situation caused crude oil trading volume to surge to $1.2 billion). This performance helped secure S&P's authorization for tradeXYZ to use its indices.

Editor's Note: Last week, Cerebras Systems, an AI chip startup dubbed the "Nvidia challenger," officially listed on the Nasdaq. On its debut day, the stock price briefly surged to $350, nearly doubling from its IPO price of $185, sparking widespread market attention.

However, before the official listing, Pre-IPO perpetual contracts on tradeXYZ had already provided on-chain price discovery for CBRS hours, or even weeks, in advance. By using perpetual contracts, tradeXYZ enables continuous trading and real-time price discovery that traditional finance cannot achieve, while also allowing ordinary investors to participate in the pricing of new stocks weeks ahead of the IPO. This signifies that the traditional IPO gray market and roadshow model are being disrupted by on-chain finance, and the pricing power of traditional finance is gradually being eroded.

Today, according to official sources, tradeXYZ's Pre-IPO market has officially launched for SpaceX, under the ticker SPCX. As one of the most anticipated private companies globally, SpaceX is seen as a potential candidate for the largest IPO in human history, with market valuation expectations even pointing towards $2 trillion. If tradeXYZ successfully completes on-chain pricing for SpaceX ahead of time once again, its influence could expand further.

This article was first published on March 19, providing a detailed breakdown of tradeXYZ's pricing mechanism and operational logic. The following is the original text:

In the early hours of March 9, tensions escalated in Iran. The CME was closed, the ICE was closed; all major global futures exchanges were shut. The next official quote for crude oil prices wouldn't come until the Monday morning session, over a dozen hours later.

But the crude oil contract CL-USDC on Hyperliquid didn't wait. That day, the trading volume for this on-chain perpetual contract surged from its daily average of $21 million to over $1.2 billion. During the window when traditional markets were closed, traders used an on-chain protocol to instantly price geopolitical risk.

This incident was widely circulated within the crypto community as another victory for DeFi. However, few questioned a more fundamental issue: when external markets are closed, where does the price for this on-chain exchange come from?

Where Does the Price Come From When External Quotes Are Unavailable?

tradeXYZ is the largest provider of traditional asset perpetual contracts on Hyperliquid. It operates on the HIP-3 protocol and accounts for 90% of total open interest on HIP-3. The S&P 500, Nasdaq 100, WTI crude oil, gold, silver, and individual Korean stocks can all be traded 24/7. However, the pricing logic of perpetual contracts is completely different from spot trading. Prices on spot exchanges are generated directly by matching buyers and sellers. A perpetual contract requires an "anchor" to tether the contract price to the real price of the underlying asset. This anchor is the oracle.

In the traditional futures market, the pricing anchor is the exchange itself. The CME's crude oil futures price is the price of crude oil; no additional reference system is needed. But tradeXYZ's contracts run on the Hyperliquid chain, with no direct connection to the matching engine in Chicago. When the CME is open, tradeXYZ's oracle directly quotes the CME's price – this is not technically challenging. The real challenge arises after the CME closes.

tradeXYZ's solution is to have the oracle extract information from its own order book. The system calculates an "impact price spread." Simply put, it measures: if someone were to buy a large quantity now, how much higher would the average execution price be compared to the current price? If someone were to sell a large quantity, how much lower would it be? This deviation reflects the imbalance of buying and selling pressure in the order book. The oracle adds this deviation to the current price to get a "target price," then uses a decay function to slowly move the current price towards this target.

The key word is "slowly." The oracle updates every 3 seconds, but each time it only moves a fraction of the gap between the current price and the target price. This speed is controlled by a time constant. The larger the time constant, the slower and more resistant to manipulation the oracle is, but also the less able it is to reflect genuine market sentiment.

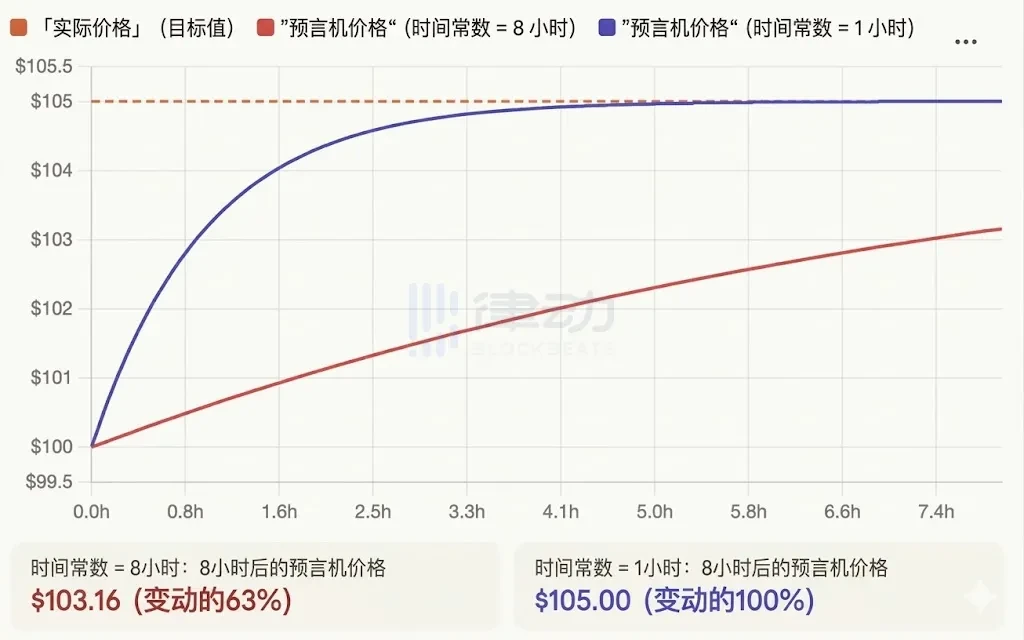

When tradeXYZ first launched, this time constant was set to 8 hours. In November 2025, this parameter was lowered to 1 hour. The reason for the adjustment is tied to traders' real money: tradeXYZ settles funding rates every hour. If the oracle tracks the real price too slowly, profitable traders will see their gains continuously drained by funding costs.

As shown by the red line in the chart below, if you go long on crude oil and are correct, but the oracle takes 8 hours to catch up to the real price, your price never reaches your target (the real price) during those 8 hours. Your profits are significantly eroded by funding costs.

After the parameter was lowered to 1 hour, the price reaches your expected level in just 5 hours (blue line). The price confirms your judgment faster, and you pay fewer funding fees compared to before.

However, a faster oracle also introduces new risks. If the oracle stops functioning for, say, 6 hours and then suddenly resumes, the formula would cause the price to jump instantly to 99.7% of the target. Such a sudden price spike could trigger mass liquidations. tradeXYZ's solution is to add a safety valve: regardless of the actual elapsed time, the effective time difference for each update is capped at 6 minutes. Even if the oracle recovers after a crash, the price can only inch its way up step by step.

Price Cages, Re-anchoring, and Monday's Opening Gap

The oracle pricing solved the "how to quote over the weekend" problem. But another issue arises: how freely can the price move?

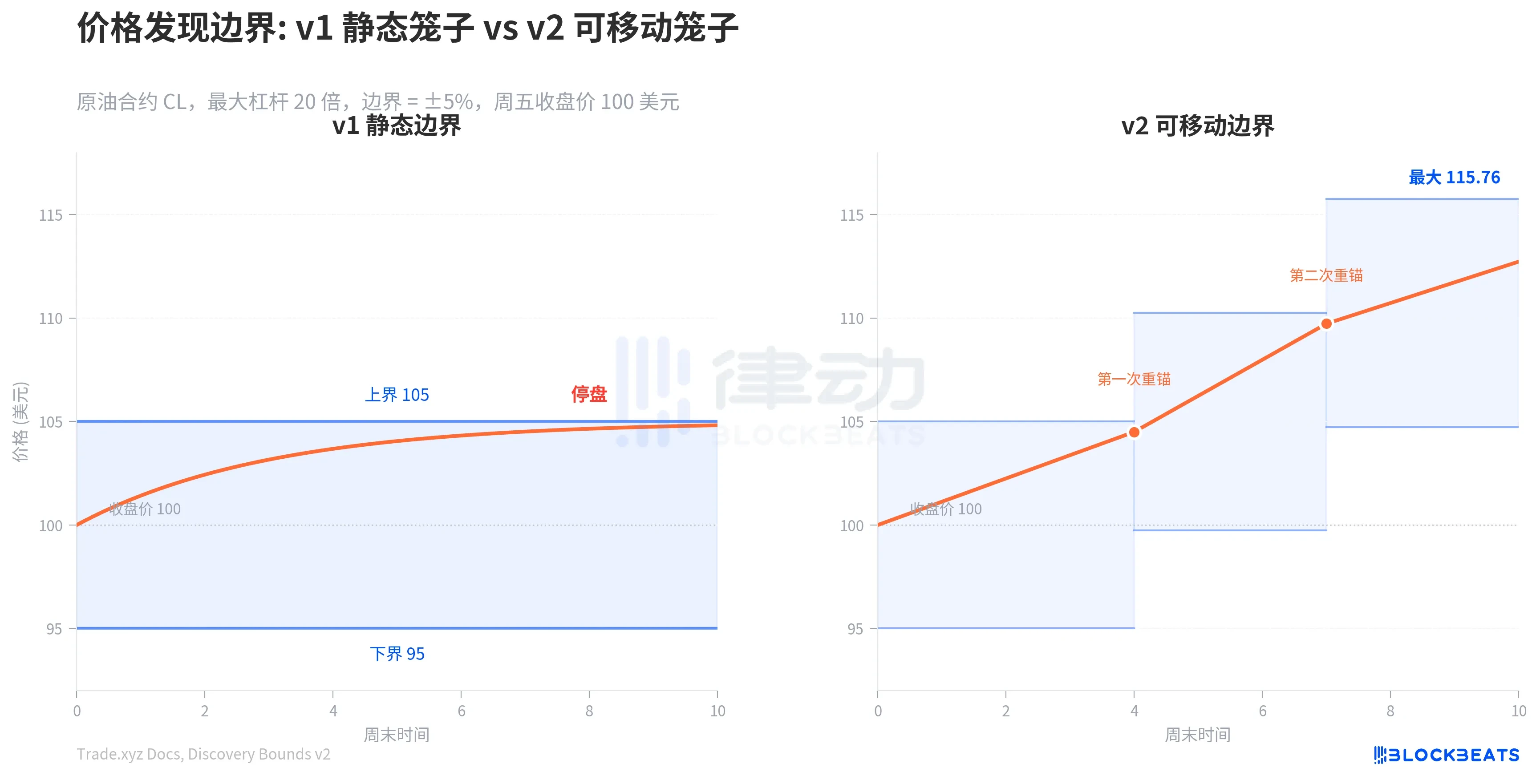

tradeXYZ draws a "cage" for each contract. The mark price is limited to a certain percentage above and below the last external closing price. This percentage equals the reciprocal of the maximum leverage. The crude oil contract has a max leverage of 20x, so the cage is +/- 5% around the closing price. If crude oil closes at $100 on Friday, the weekend mark price can only fluctuate between $95 and $105. If it hits the boundary, trading is halted.

Weekend trading halt for crude oil contract in early March

On a normal weekend, this mechanism works well. A 5% range is enough to absorb most overnight volatility. But a geopolitical event on the scale of March 9 pushes the price directly to the cage boundary. All market information gets pent up. When the CME opens on Monday, if the real price jumps 8%, a significant gap forms. Short positions get liquidated instantly, and market makers suffer losses as they cannot gradually hedge their positions.

In March 2026, tradeXYZ deployed "Price Discovery Boundary v2" for its crude oil contracts. The core change: the cage size remains the same, but the cage can move. When the oracle price reaches 90% of the current boundary, the system re-anchors the cage's center to that boundary value and draws a new cage of the same size around the new anchor. Re-anchoring can occur a maximum of two times per direction.

Using concrete numbers: Initial cage $95 to $105. When the oracle rises to $104.50, re-anchoring is triggered, creating a new cage from $99.75 to $110.25. After a second trigger, it becomes $104.74 to $115.76, which is the endpoint. Starting from $100, the maximum discoverable range expands to approximately $115.76.

This design ensures the immediate fluctuation range is always within 5%, meaning market makers don't need to change their risk models. At the same time, re-anchoring signifies that the system "acknowledges" the price movement that has already occurred, reducing the gap size at Monday's open. However, the trade-off is clear: a long position with a liquidation price at -8% was absolutely safe under v1 (because the price couldn't reach -8%), but under v2, it might enter the liquidation zone after a downward re-anchor. tradeXYZ chose to deploy v2 first on two crude oil contracts and stated it will decide whether to roll it out further after observing the results.

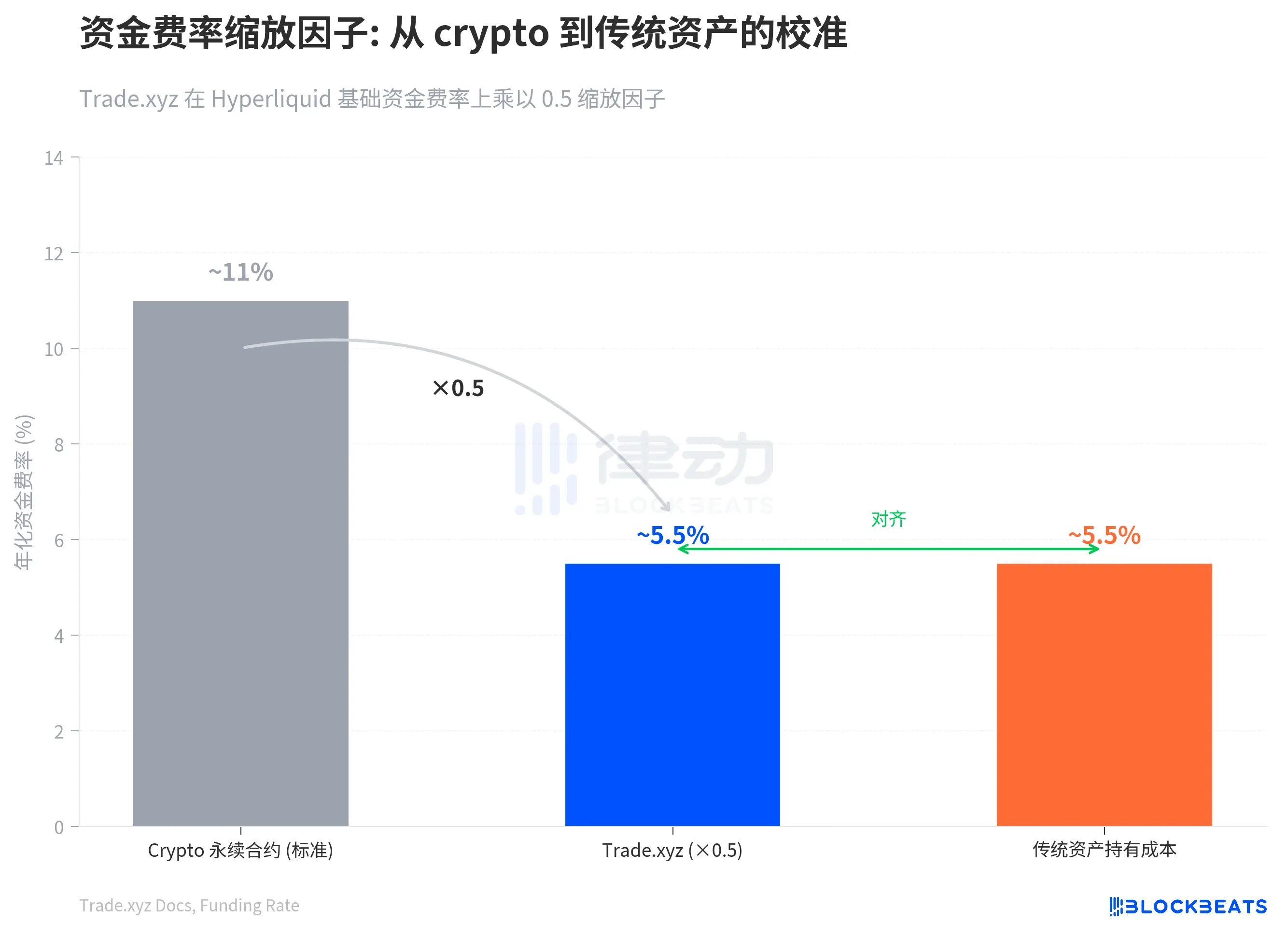

Another key component of the pricing system is the funding rate. The funding rate acts as the rubber band that ties the perpetual contract price to the oracle price: if the mark price is above the oracle, longs pay shorts; if below, shorts pay longs. tradeXYZ's funding rate formula shares the same structure as most crypto exchanges but incorporates a scaling factor of 0.5.

This 0.5 is an adjustment calibrated for traditional assets. The baseline annualized funding rate for crypto perpetuals is about 11%, reflecting the cost of pure leverage, which is reasonable for a non-dividend-paying asset like Bitcoin. However, for stocks and commodities, the real cost of carry is close to SOFR plus 1-2 percentage points, or about 5-6%. Multiplying by 0.5 reduces the baseline annualized rate from around 11% to about 5.5%, aligning it with traditional assets. This is particularly crucial on weekends: the scaling factor cuts the weekend funding rate in half. Working in tandem with the oracle's 1-hour time constant, it allows traders who are correct in their direction to retain most of their profits.

Different Assets, Different Processing Pipelines

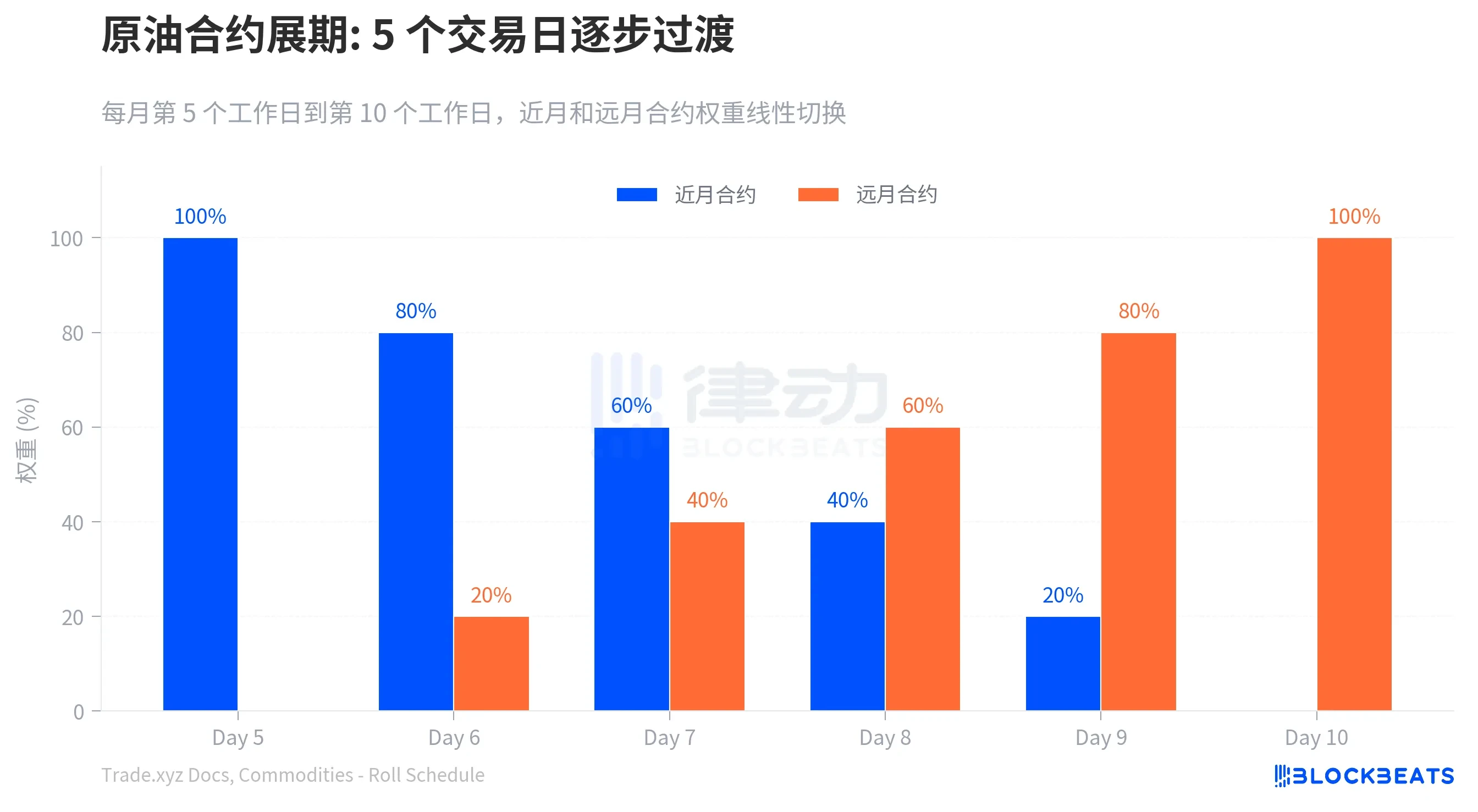

Precious metals have active global spot markets. External prices for gold, silver, platinum, and palladium are taken directly from spot quotes, avoiding the issue of futures rollovers. However, crude oil and industrial metals lack a unified spot quotation, so tradeXYZ must use CME futures contracts as the pricing basis. Futures have expiration dates, requiring the system to roll positions from the current month's contract to the next month's contract each month. The problem is that the prices of the two contracts are usually different. Storage costs and supply-demand expectations can cause deferred-month contracts to trade at a premium to nearby contracts. If the price jumps during the rollover, a holder's profit or loss would experience an unreal fluctuation, potentially triggering undeserved liquidations.

tradeXYZ's handling method is a gradual transition over 5 trading days: from the 5th to the 10th business day of each month, the oracle price is a weighted average of the nearby and deferred-month contracts, with the weights changing linearly each day.

Pricing for stock index contracts is even more complex. XYZ100 tracks the Nasdaq 100, but CME Nasdaq futures trade almost around the clock (5 days x 23 hours), offering a longer reference period than the spot index. Initially, tradeXYZ used futures prices to infer the spot price, applying a fixed 4% discount rate to strip out the cost of carry. However, this fixed value would drift whenever the Fed adjusts interest rates. The v2 solution, launched in February 2026, switched to dynamic calculation: during US stock market hours, the spot index value is used directly, while the implied discount rate is calculated from the spread between futures and spot; outside trading hours, this discount rate is used to infer the spot price.

There is also a special category: individual Korean stocks. tradeXYZ lists Samsung Electronics, SK Hynix, and Hyundai Motor, which are quoted in Korean Won on the Korea Exchange. The oracle needs to layer a USD/KRW exchange rate conversion on top of the original quotation. Consequently, a holder's profit or loss reflects both the stock price movement and the currency exchange rate fluctuation.

Who Bears Responsibility for the Consequences of Parameter Choices?

All these pricing mechanisms rest on a fundamental premise: there are enough market makers willing to continuously provide liquidity. Hyperliquid's HLP market-making treasury provides liquidity for native BTC and ETH perpetual contracts but does not cover third-party contracts deployed on HIP-3. tradeXYZ's liquidity depends entirely on the voluntary participation of external market makers. In extreme market conditions, if a liquidated position cannot find a counterparty to take the other side, the system does not rely on a treasury backstop like Hyperliquid's main exchange. Instead, it directly triggers ADL (Auto-Deleveraging), forcibly closing the most profitable opposing positions in order.

The brilliance of this pricing system lies in its use of a set of mutually balancing parameters—the oracle's tracking speed, price discovery boundaries, and the funding rate scaling factor—to build a self-sufficient pricing environment that functions even without external quotes. When the S&P chose to authorize tradeXYZ on March 18, it likely recognized this infrastructure that had proven itself during a real geopolitical crisis.

However, this system also has its costs. The oracle extracts information from the order book, meaning that during periods of thin liquidity (like late-night sessions for Korean stock contracts), a few orders can significantly move the oracle. The Price Discovery Boundary v2 expands the range of possible liquidations over the weekend, requiring leveraged traders to reassess their safety margins. ADL means that even if your trade thesis is correct, you could be forcibly liquidated in extreme market conditions.

tradeXYZ has chosen a path completely different from traditional exchanges: transferring pricing power from a centralized matching engine to a set of on-chain parameter systems. Traditional exchanges close because clearing, risk management, and market-making require windows for human intervention. tradeXYZ cannot close because on-chain contracts don't have the concept of "off-hours." It must be able to provide a price at any moment. The crude oil event on March 9 proved this system works under pressure. But it also exposed a deeper problem: when on-chain protocols assume the pricing function of traditional financial infrastructure, who is responsible for the consequences of the parameter choices?

Adjusting the time constant from 8 hours to 1 hour was a parameter decision by the tradeXYZ team. Upgrading the Price Discovery Boundary from v1 to v2 was another. These decisions affect the liquidation lines and funding rates for every position holder. In a traditional exchange, such rule changes require regulatory approval and a public announcement period. On-chain, a single parameter update can accomplish it.

In a system without an HLP backstop, without regulatory arbitration, and relying entirely on parameter design to maintain order, understanding how these parameters affect your position is understanding the true risk you are taking.