In-depth analysis of the ENA project

Original author: @Peng_Investment (Dapeng Tongfengqi)

ENA (Ethena) makes it possible for the Web3 world to have independent currency (stable currency) issuance and pricing rights, and has huge growth potential and imagination space in the future. If you want to know more about the investment research of the ENA project, you can read this article in detail.

Chapter 1 Project Overview

1.1 Project Introduction

When it comes to ENA (Ethena), many people still only know that ENA is a decentralized stablecoin USDe project, a synthetic dollar protocol based on Ethereum, which provides a crypto-native currency solution that does not rely on the infrastructure of the traditional banking system, and a globally accessible dollar-denominated tool - "Internet bonds" . Compared with centralized stablecoins, Ethena has many advantages and some disadvantages. However, in fact, in my opinion, the ENA project actually has a deeper meaning - solving the autonomous currency issuance and basic pricing of the web3 world, and returning the currency issuance right to the web3 world.

To understand the deeper meaning of ENA, we must first understand the development of currency. The first division of labor in human history brought about the exchange of objects, but the inconvenience of carrying and trading counterparties led to the emergence of real currency.

The earliest human currencies were mainly shells, etc., which later evolved into bronze (later copper), silver, gold, iron, etc. Because copper and iron are more easily oxidized and difficult to cut, silver and gold gradually became the currencies recognized by people. However, with the rapid development of the handicraft economy and the rapid accumulation of wealth, traditional silver and gold could not meet people's needs, so paper money was invented (China's earliest, silver notes). The invention of paper money has greatly promoted economic development, but paper money must not be printed casually. Behind each paper money, there is a corresponding face value of silver or gold inventory, which is what people often call the silver standard or gold standard. The development of the US dollar is due to the typical gold standard (Bretton Woods system), which ensures the hard currency attribute and international attribute of the US dollar. In other words, the more gold is mined/reserved each year, the more banknotes can be printed (such as the original US dollar).

However, when the economy developed to a new stage and the gold reserves could not keep up, the fixed-ratio monetary system of the Bretton Woods system soon faced challenges and finally had to be declared disintegrated in the "Smith Agreement". Since then, the currency issuance of major countries in the world, represented by the United States, has gradually transitioned from the gold standard to the treasury bond standard. Some time ago, another major country also adopted a treasury bond standard currency issuance mechanism similar to that of the United States. Specifically, when a country issues ultra-long-term treasury bonds (such as 10 years, 20 years, 30 years, 50 years, etc.), the central bank issues currency by printing an equal amount of banknotes to purchase ultra-long-term treasury bonds issued by the country. The benefit is that it can bring a large amount of cash to the government for investment, and at the same time, it also injects more monetary liquidity into the market, commonly known as "flooding". The purpose of flooding is actually to stimulate the economy, but it is easy to trigger a trap of excessive currency issuance.

Let’s go back to the web3 world and re-examine the ENA project. Does its “Internet bond” pricing concept seem particularly familiar? What is the specific investment logic?

1.2 Investment Logic

BTC, ETH, etc. are first of all high-quality assets, similar to gold in the real world. Although they can be used for payment and purchase, they are essentially assets, not pricing currencies or issuing currencies. However, with the booming development of web3, the market needs more liquidity, which is currently mainly achieved through the use of centralized stablecoins such as USDT and SUDC that rely on traditional financial infrastructure. Centralized stablecoins face three biggest challenges:

(1) The storage of bond collateral (such as U.S. Treasury bonds) in regulated bank accounts poses unhedgeable custody risks and is susceptible to regulatory scrutiny;

(2) heavy reliance on existing banking infrastructure and evolving regulations in certain countries (including the United States);

(3) Since the issuer internalizes the returns generated by leveraging the backing assets while transferring the decoupling risk to the users, the users face the risk of “no return”.

Therefore, decentralized and reasonably stable assets that do not rely on traditional financial infrastructure are the only way for the development of web3, which can be used as both transaction currency and core basic assets for financing. Without independent and reasonably stable reserve stable assets, centralized and decentralized order books are inherently very fragile.

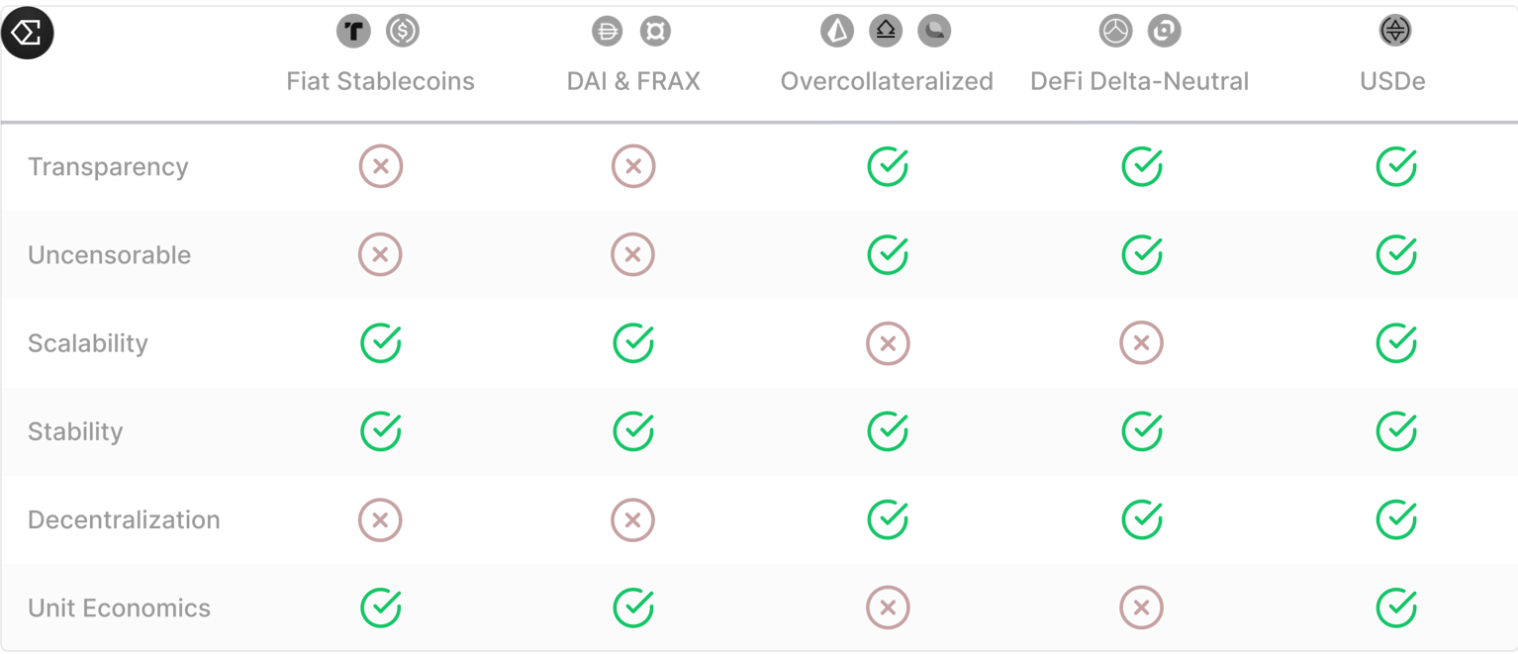

Long before ENA, there were pioneers who had attempted decentralized stablecoins, with MakerDAO (DAI), UST, etc. However, these pioneers encountered many problems related to scalability, mechanism design, and lack of user incentives.

(1) “ Overcollateralized stablecoins ” (typically MakerDAO’s DAI, 1.5x collateralization ratio) have historically encountered scaling issues because their growth is closely tied to the growth of leverage demand on the Ethereum chain and the rapid rise and fall of ETH. For example, DAO, with a 1.5x collateralization ratio and a 1.4x liquidation collateralization ratio, was inefficient and lacked collateralization appetite. Recently, some stablecoins have begun to introduce treasury bonds to improve scalability, but at the expense of censorship resistance.

(2) The mechanism design of “ algorithmic stablecoins ” (typically represented by UST) faces challenges and is inherently fragile and unstable. Such designs are unlikely to have sustainable scalability.

(3) Previous “ Delta Neutral Synthetic Dollars ” were difficult to scale due to their heavy reliance on decentralized trading venues that lacked sufficient liquidity and were vulnerable to smart contract attacks.

ENA has learned from historical lessons and provided a relatively perfect solution. It has corresponding solutions in terms of scalability, stability and censorship resistance. This part will be introduced in detail in the technical chapter. ENA makes it possible for the web3 world to have the right to issue its own currency (stable currency). At the same time, its economic model will also promote more participants to provide more USDe liquidity.

In 2023, the stablecoins used for on-chain transaction settlement alone exceeded $12 trillion. Once stablecoins gain market recognition, their value space is immeasurable. AllianceBernstein, a leading global asset management company with $725 billion in assets under management (AUM), predicts that the stablecoin market size could reach $2.8 trillion by 2028. This forecast indicates that there will be huge growth opportunities from the current market value of $140 billion (previously peaked at $187 billion).

1.3 Investment Risks

Although Ethena has its unique advantages, it also has potential risks that need to be taken seriously, including:

(1) Financing risks

"Funding risk" is related to the possibility of persistent negative funding rates. Ethena can earn income from funding, but it may also need to pay funding fees. First, negative returns tend not to last long and will quickly return to a positive mean; second, the establishment of the reserve fund is to ensure that negative returns will not be passed on to users.

(2) Liquidation risk

Liquidation risk refers to the risk of forced liquidation in centralized exchanges due to insufficient margin during delta neutral hedging. For Ethena, derivatives trading is only for delta neutral hedging, with low leverage and low probability of liquidation risk. At the same time, Ethena uses a variety of methods such as additional collateral, temporary circular entrustment between exchanges, and reserve funds to ensure that liquidation risk does not occur or has little impact after it occurs.

(3) Custody risks

Ethena relies on "over-the-counter settlement" (OES) providers to hold protocol-backed assets, so there is a "custodial risk". To solve this problem, on the one hand, Ethena holds it through a bankruptcy-remote trust, and on the other hand, it cooperates with multiple OES, such as Copper, Ceffu, and Fireblocks.

(4) Risk of Exchange Bankruptcy

First, Ethena works with multiple exchanges to spread risk and mitigate the potential impact of exchange bankruptcy; second, Ethena retains full control and ownership of assets through OES providers, without having to deposit any collateral with any exchange. This allows the impact of any exchange's special events to be limited to the outstanding profit and loss between OES provider settlement cycles.

(5) Mortgage risk

“Collateral risk” refers to the fact that the backing asset of USDe (stETH) is different from the underlying asset (ETH) of the perpetual futures position. However, due to low leverage and small collateral discount, the impact of stETH decoupling on hedge positions is minimal.

Chapter 2 Technology, Risk Response, Business Development and Competition Analysis

2.1 Technology

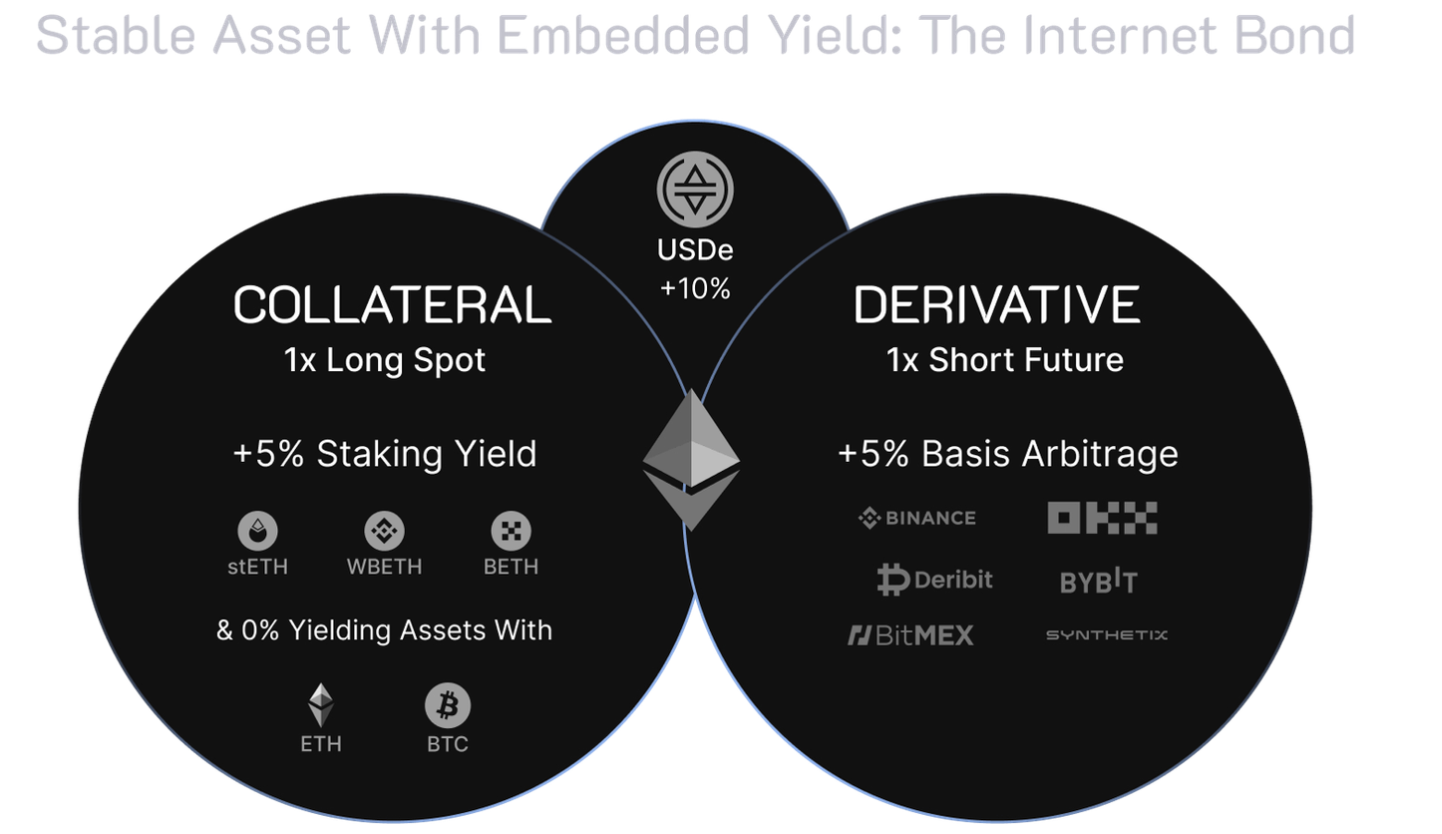

Technically speaking, Ethena is a synthetic dollar protocol based on Ethereum, which provides a crypto-native currency solution that does not rely on the infrastructure of the traditional banking system, and a globally accessible dollar-denominated instrument - "Internet Bond". Ethena's synthetic dollar USDe provides a crypto-native, scalable currency solution that supports USDe peg stability through delta hedging of Ethereum and Bitcoin collateral.

“Internet Bonds” combines the yield generated by staked assets (such as staked Ethereum) (to the extent of the backing asset) with funding and basis spreads from perpetual and futures markets to create the first on-chain crypto-native currency solution.

So how does USDe achieve stability, censorship resistance, and economic benefits, and address and solve the shortcomings and risks of other projects?

(1) Stability

Users can obtain USDe from permissionless external liquidity pools (USDT, USDC, DAI, etc.), or they can mint and redeem USDe on demand by directly using Ethena contracts to hold assets such as stETH and stBTC.

At the same time as USDe is minted, Delta neutral hedging (derivatives) is performed through multiple external centralized exchanges to ensure that its dollar value remains unchanged regardless of market changes. The price of ETH may triple in one second and then fall 90%, and the dollar value of the portfolio will not be affected (except for a brief dislocation between the spot market and the derivatives market). This is because the profit from the tripling of the price of 1 ETH is completely offset by the loss of the short perpetual position of the same size.

(2) Scalability

Since the Delta neutral strategy makes the ratio 1:1, coupled with the liquidity guarantee of multiple centralized exchanges, as well as high-value and highly scalable pledged currencies such as ETH and BTC, USDe has great scalability. Currently, only ETH has a pledge ratio of up to 27% (as of April 2024), and the total pledge amount is about 160 billion US dollars. The consensus of Ethereum researchers and Ethereum ecosystem staff is that the pledge amount of ETH will soon reach more than 40%. This also brings a lot of imagination space for the scale growth of USDe.

(3) Resisting censorship

Ethena utilizes “over-the-counter settlement” (OES) providers to hold backing assets. This enables Ethena to delegate/deregister collateral to centralized exchanges without being exposed to the idiosyncratic risks that are specific to exchanges.

While using an OES provider requires a reliance on the OES provider’s technology, this does not mean that counterparty risk has been transferred from the exchange to the OES provider. OES providers typically hold funds in a bankruptcy remote trust when not using an MPC solution to ensure that the OES provider’s creditors have no right to claim assets. If the custody provider fails, these assets are expected to be outside the provider’s estate and are not subject to the custodian’s credit risk.

None of these OES providers are based in the U.S., so they don’t need U.S. scrutiny. Traditional custody of funds through exchanges or holding fiat currencies or treasuries or even stablecoins in U.S. bank accounts or U.S. custodians all carry significant scrutiny risk due to the current U.S. regulatory environment and the heightened focus on global regulatory compliance.

(4) Economic benefits

The revenue generated by the ENA protocol comes from two sources:

Staking asset consensus and execution layer rewards (mainly ETH staking income)

Funding and Basis from Delta Hedging Derivatives Positions

Historically, participants who short this delta (delta is 0) exposure have earned positive funding rates and basis due to the mismatch in supply and demand for the digital asset.

In addition, if USDe holders do not trade, they can also pledge USDe to obtain sUSDE. When the pledged USDe is cancelled and the sUSDE is destroyed, the original USDe and the pledged income can be obtained. This design can attract more ETH holders to participate, not just those who need to leverage, so it can provide more USDe liquidity for the entire web3.

2.2 Risk Response

Although decentralized stablecoins are good, there are also some risks that must be taken into account. The advantage of ENA is that these risks are taken into consideration at the beginning of the design of the entire technical solution, and the possibility of risks is resolved or reduced as much as possible. Let's take a look at it in detail.

1. Financing risks

“Funding risk” relates to the possibility of persistent negative funding rates. Ethena is able to earn income from funding, but may also need to pay funding fees. While this poses a direct risk to protocol returns, data shows that negative returns tend not to last long and quickly return to a positive mean.

Negative funding rates are a feature of the system, not a bug. USDe was built with this in mind. Therefore, Ethena has set up a reserve fund that will step in when the combined yield between LST assets (such as stETH) and the funding rate of short-term perpetual positions is negative. This is designed to protect the spot support that supports USDe. Ethena will not pass on any "negative yield" to users who pledge USDe as sUSDe.

Using LST collateral (such as stETH) as collateral for USDe can also provide an additional safety margin for negative financing (stETH can obtain an annualized yield of 3-5%), that is, the protocol yield will only be negative when the sum of the LST yield and the funding rate is negative.

2. Liquidation Risk

The liquidation risk mentioned here refers to the risk of forced liquidation in centralized exchanges due to insufficient margin during delta neutral hedging. For Ethena, derivatives trading is only for delta neutral hedging, with low leverage and low probability of liquidation risk. Although Ethena's margin on the exchange is composed of two assets, ETH spot and stETH (stETH accounts for no more than 50%), since the Ethereum network has undergone Shapella upgrade, one of the functions is to allow users to cancel their stETH pledge, and the stETH/ETH discount has never exceeded 0.3%. In other words, the value of stETH is almost exactly the same as the spot value of ETH.

In addition, Ethena has also made the following arrangements to ensure that liquidation risks can be well dealt with in extreme situations:

(1) Once any risk scenario occurs, Ethena will systematically entrust additional collateral to improve the margin status of hedged positions.

(2) Ethena is able to temporarily cycle delegated collateral between exchanges to support specific situations.

(3) Ethena has access to a reserve fund that can be quickly deployed to support the exchange’s hedging positions.

(4) If an extreme situation occurs, such as a serious smart contract defect in the pledged Ethereum assets, Ethena will immediately reduce the risk and protect the value of the supporting assets. This includes closing hedging derivatives to avoid liquidation risk becoming a problem, and disposing of the affected assets for another asset.

3. Custody Risk

Since Ethena relies on an “over-the-counter settlement” (OES) provider to hold the protocol-backed assets, there is a certain dependency on their ability to operate, which is what we refer to as “custodian risk.” Custodians’ business models are built on asset protection, rather than leaving collateral on a centralized exchange.

There are three main risks of using an OES provider for hosting:

(1) Accessibility and usability . Ethena is capable of deposits, withdrawals, and delegation to exchanges. Any unavailability or degradation of these features will hinder the transaction workflow and usability of the minting/exchanging USDe functionality. It is worth noting that this will not affect the value that underpins USDe.

(2) Fulfilling operational responsibilities . If an exchange fails, OES transfers any unrealized PnL risk to the exchange quickly. Ethena reduces this risk by frequently settling PnL with exchanges. For example, Copper’s Clearloop settles PnL between exchange partners and Ethena every day.

(3) Custodian operational failure . While there has not yet been any major operational failure or bankruptcy of a large cryptocurrency custodian, this is a real possibility. Although assets are held in separate accounts, custodian bankruptcy will cause operational problems for the creation and redemption of USDe, as Ethena is responsible for managing the transfer of assets to other providers. Fortunately, the backing assets do not belong to the custodian, and the custodian or its creditors should not have legal claims on these assets, because OES providers either use bankruptcy-isolated trusts or MPC wallet solutions.

Ethena mitigates these three risks by not providing excessive collateral to a single OES provider and ensuring that concentration risk is managed. Even for the same exchange, there will be multiple OES providers to mitigate the above two risks.

4. Risk of Exchange Bankruptcy

First, Ethena diversifies risk and mitigates the potential impact of exchange bankruptcies by partnering with multiple exchanges;

Second, Ethena retains full control and ownership of its assets through an OTC settlement provider, without having to deposit any collateral with any exchange.

This allows the impact of a particular event on any one exchange to be limited to the outstanding profit or loss between settlement cycles of the OTC clearing provider.

Therefore, if an exchange goes bankrupt, Ethena will entrust the collateral to another exchange and hedge the outstanding delta previously covered by the bankrupt exchange. If an exchange goes bankrupt, the derivative position will be considered closed. Capital preservation is Ethena's top priority. In extreme cases, Ethena will always strive to protect the value of the collateral and the USDe stable peg (using reserves).

5. Mortgage risk

The "collateral risk" here refers to the fact that the backing asset (stETH) of USDe is different from the underlying asset (ETH) of the perpetual futures position. The backing asset ETH LSTs is different from the underlying asset ETH of the hedge contract, so Ethena needs to ensure that the price difference between the two assets is as small as possible. As discussed in the liquidation risk section, due to the low leverage and small collateral discount, the impact of stETH decoupling on the hedge position is minimal, and the possibility of liquidation is extremely small.

2.3 Business development and competition analysis

Since its inception, ENA has experienced a meteoric rise, with a significant increase in value in a short period of time. This surge is not only attributed to its strong technical and institutional support, but also to the high returns it offers, making it attractive to both retail and institutional investors. On March 29, 2024, Binance announced that Binance Launchpool will launch the 50th project Ethena (ENA). Users can mine BNB and FDUSD in the ENA mining pool after 08:00 Beijing time on March 30 for a period of 3 days. In addition, Binance will launch Ethena (ENA) at 16:00 Beijing time on April 2, and open ENA/BTC, ENA/USDT, ENA/BNB, ENA/FDUSD and ENA/TRY trading pairs. Binance's mining activities and listing transactions also illustrate the rapid development of ENA.

The advantages of ENA's solution also make it stand out and truly represent decentralized stablecoins, competing with traditional major competitors USDT and USDC, two centralized stablecoin projects. Although there will be many difficulties in the early stage, the development momentum is very rapid, which also makes many people in the industry have a lot of expectations for it.

Chapter 3 Team and Financing

3.1 Team situation

Ethena was founded by Guy Yang, whose design was inspired by a blog post by Arthur Hayes. The core team consists of 5 people.

Guy Young is the founder and CEO of Ethena.

Conor Ryder is the Head of Research at Ethena Labs and was previously a Research Analyst at Kaiko. He is a graduate of University College Dublin and Gonzaga College.

Elliot Parker is Head of Product Management at Ethena Labs and was previously a Product Manager at Paradigm. He graduated from the Australian National University.

Seraphim Czecker is Head of Business Development at Ethena. Previously, he was Head of Risk at Euler Labs and an Emerging Markets FX Trader at Goldman Sachs.

Zach Rosenberg is the General Counsel of Ethena Labs and previously worked at PwC. He is a graduate of Georgetown University, American University Washington College of Law, American University Kogold School of Business, and the University of Rochester.

3.2 Financing

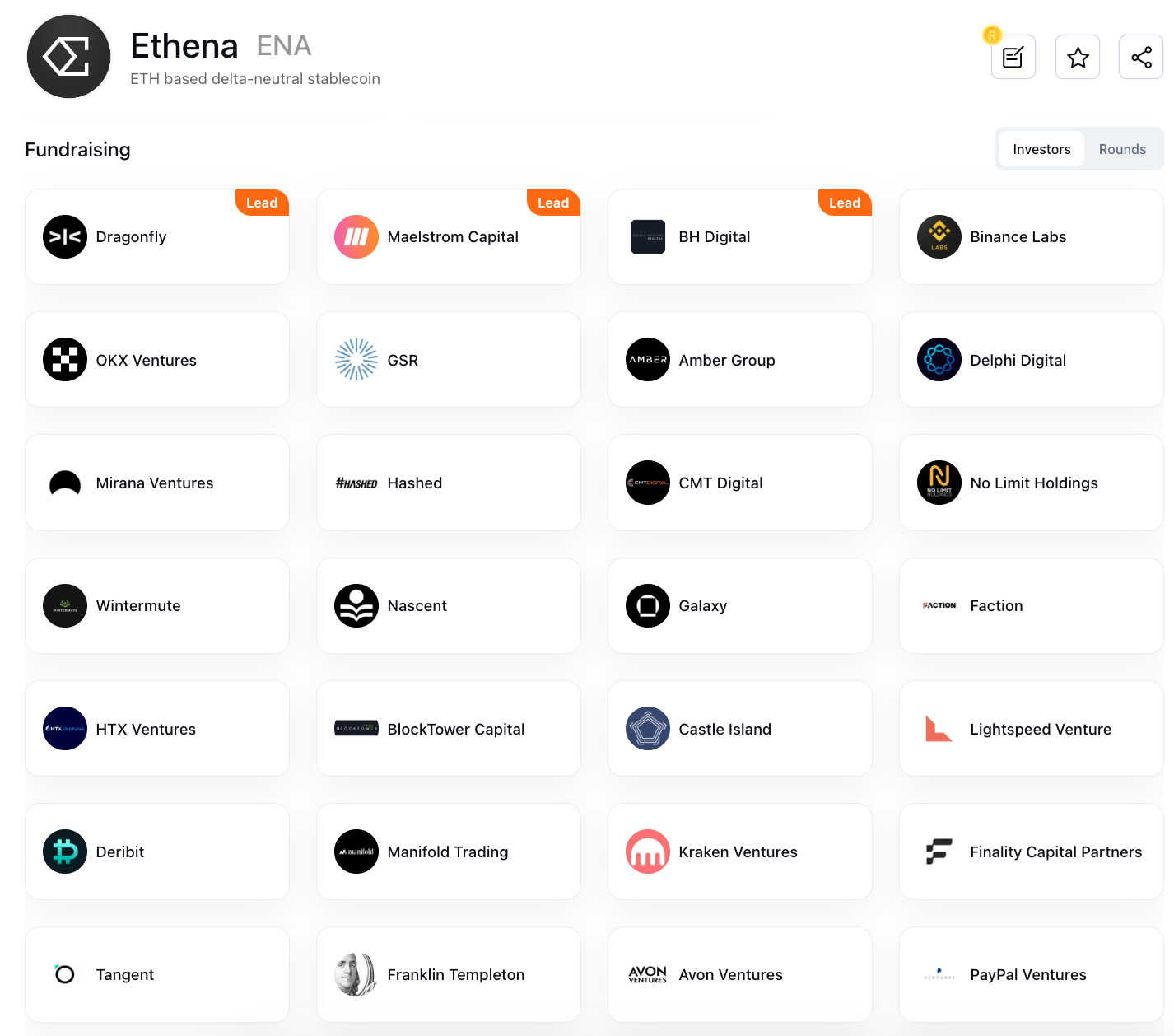

In July 2023, Ethena completed a US$6.5 million seed round of financing, led by Dragonfly, followed by Deribit, Bybit, OKX Ventures, BitMEX and others.

In February 2024, Ethena received a strategic investment of US$14 million led by Dragonfly, with participation from PayPal Ventures, Binance Labs, Deribit, Gemini Frontier Fund, Kraken Ventures, etc., with a valuation of US$300 million in this round.

Chapter 4 Token Economy

4.1 Token Allocation

Total supply: 15 billion

Initial circulation: 1.425 billion

Foundation: 15% will be used to further promote the popularization of USDe, reduce the crypto world’s dependence on the traditional banking system and centralized stablecoins, and be used for future development, risk assessment, auditing, and other aspects.

Investors: 25% (25% in the first year, unlocked linearly every month thereafter)

Ecosystem development: 30%, this part of the tokens will be used to develop the Ethena ecosystem, of which 5% will be distributed to users as the first round of airdrops, and the rest will support various subsequent Ethena plans and incentive activities. Binance's lanuchpool token activity is one of them, accounting for 2% of the total scale.

Core Contributors: 30% (Ethena Labs team and advisors, 25% unlocked in 1 year)

After the launch of Ethena's governance token, it will immediately launch the " Second Quarter Activities " to further expand its token economic model. This activity will focus on the development of new products using Bitcoin (BTC) as a supporting asset. This step not only expands USDe's growth potential, but also brings Ethena a wider market acceptance and application scenarios.

Sats Rewards, as the core of the second quarter activities, aims to reward users who participate in the construction of the Ethena ecosystem. By increasing the rewards for early users, Ethena further strengthens the sense of participation and belonging of the community, while also encouraging new users to join. The design of this incentive mechanism demonstrates Ethena's recognition of the importance of building a lasting and active community.

Through a carefully designed token economic model and incentive mechanism, Ethena is committed to building a DeFi platform that is both inclusive and sustainable, exploring new paths for the future of decentralized finance.

4.2 Token Unlock

2024.6.2 Unlock 0.36%;

2024.7.2 Unlock 0.36%;

2024.8.2 Unlock 0.36%;

2024.9.2 Unlock 0.36%;

2024.10.2 Unlock 0.36%;

2025.4.2 Unlock 13.75% , the proportion is very high and needs special attention .

Chapter 5 Target Valuation

Currently, ENA's circulating market value is 1.4 B$, and FDV's market value is 14 B$. The valuation of stablecoins is generally not low. In 2023, the stablecoins settled in on-chain transactions alone exceeded 12 trillion US dollars. Once stablecoins are recognized by the market, their value space is immeasurable. AllianceBernstein, a leading global asset management company with $725 billion in assets under management (AUM), predicts that the stablecoin market size may reach $2.8 trillion by 2028. This forecast shows that there will be huge growth opportunities from the current market value of $140 billion (previously peaked at $187 billion).

So how do we value ENA?

First of all, there is no valuation object that can be fully referenced. Secondly, the stablecoin market is huge and there is still a lot of room for growth in the future. In such a context, it is difficult to give a definite valuation. What we should consider more is whether Ethena's solution can solve and adapt to the development needs of web3's decentralized stablecoins, and whether it can respond to and resolve possible risks.

However, Arthur Hayes, the founder of BitMEX, tried to value ENA using a valuation similar to Ondo . His valuation model is based on the fact that the long-term split will be 80% of the revenue generated by the protocol going to the staked USDe (sUSDe), and 20% of the generated revenue going to the Ethena protocol. The details are as follows:

Ethena protocol annual revenue = total revenue * (1 – 80% * (1 — sUSDe supply / USDe supply));

If 100% of USDe is staked, that is, sUSDe supply = USDe supply: Ethena protocol annual income = total income * 20%;

Total yield = USDe supply * (ETH staking yield + ETH Perp swap funds);

Both ETH Staking Yield and ETH Perp Swap funds have variable interest rates.

ETH staking yield — assuming a PA yield of 4%.

ETH Perp Swap Funds — Assuming PA is 20%.

A key part of the model is the fully diluted valuation (FDV) of revenue multiples that should be used. Using these multiples as a guide, the potential Ethena FDV was estimated.

At the beginning of March, Ethena generated a 67% yield on $820 million in assets. Assuming a 50% supply ratio of sUSDe to USDe, extrapolating one year later, Ethena's annualized revenue is about $300 million. Using a valuation similar to Ondo gives a FDV of $189 billion.

Therefore, ENA's growth space = 189/14 = 13.5, which is equivalent to 12.6 in currency price.

Whether analyzed from the perspective of market size or income structure, ENA still has huge room for growth and is worthy of attention and investment. How to operate it specifically at the investment operation level? Please see the next chapter.

Chapter 6 ENA Investment Analysis and Recommendations

Since ENA is the currency that is worth investing in for the long term, one way is to buy now and hold it for a long time; the other mode is to buy at the right time, sell at the right time, and continue to make waves for long-term investment. This chapter will focus on studying and analyzing the second investment method and give current investment advice, using the chip distribution and MVRV research methods.

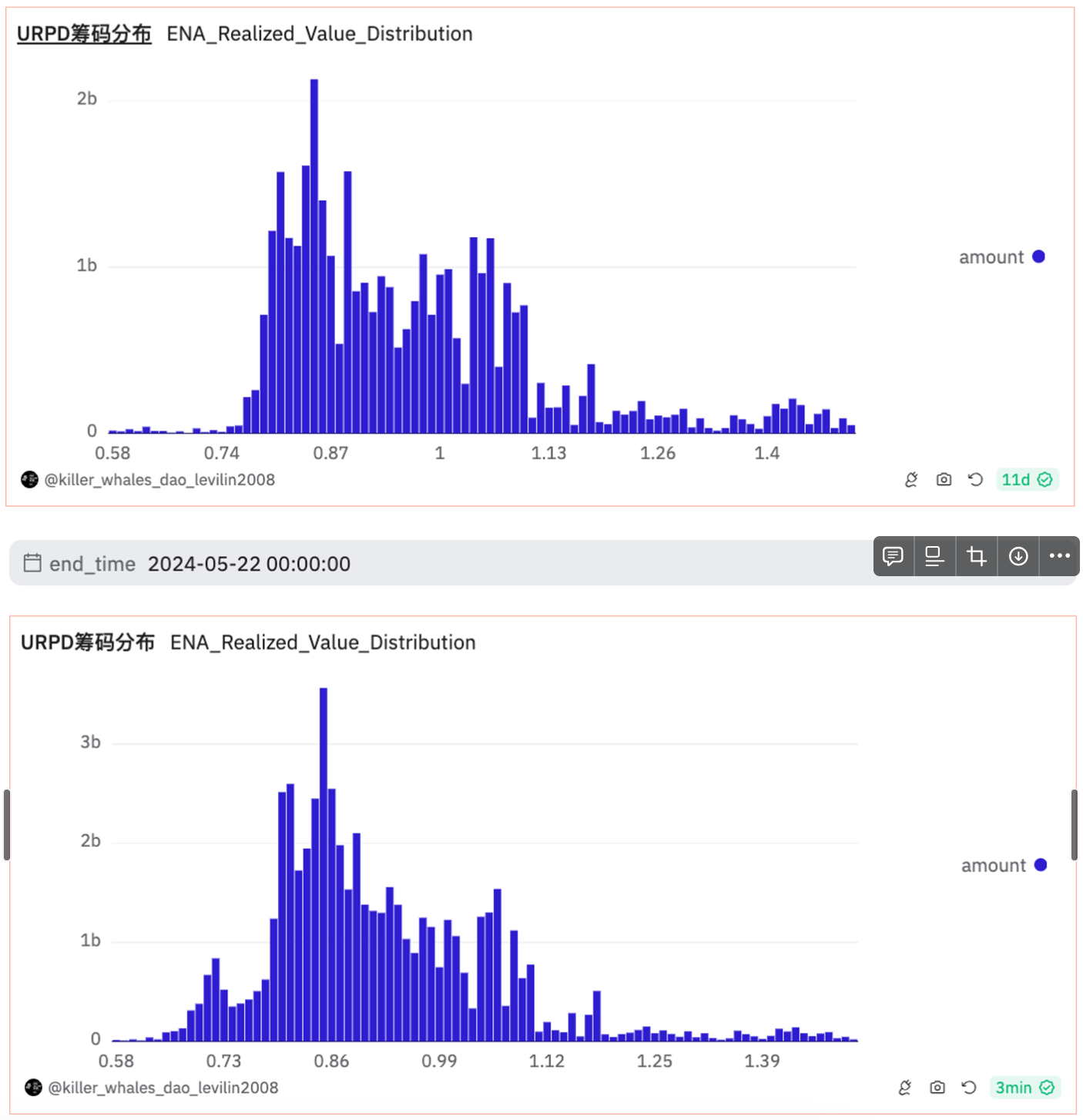

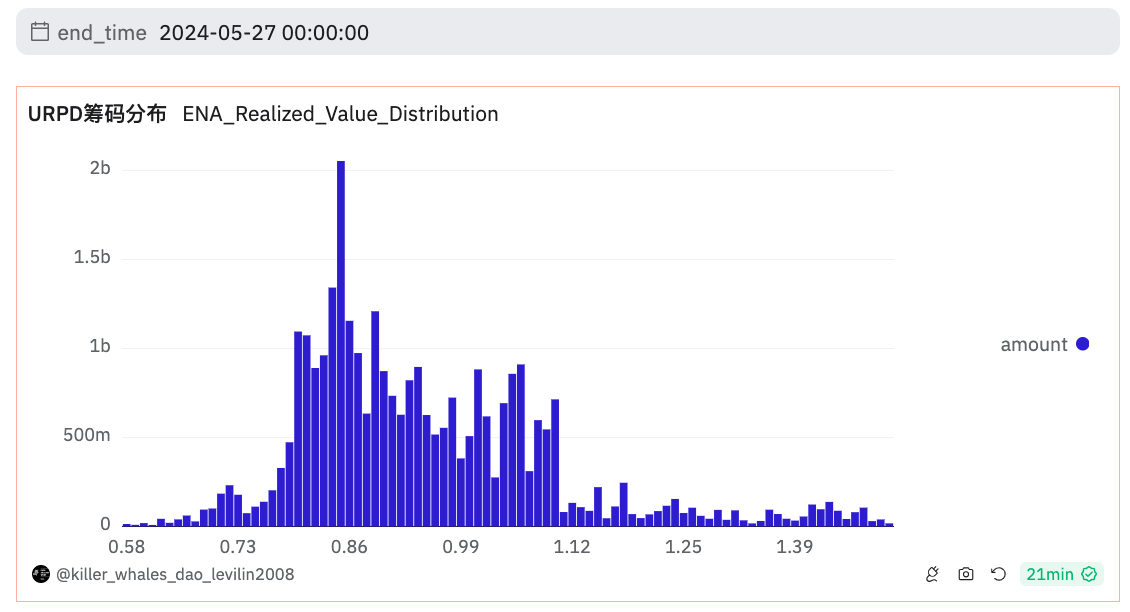

6.1 Research on Chip Distribution

According to the URPD chip distribution chart of ENA Dashboard shared by Mr. Lin @levilin 2008 VIP group, we can easily find that:

Starting from May 15, the chips above the price of 1 have been gradually decreasing, and a very large chip consensus area has formed around 0.85, especially reaching a peak on May 22;

Secondly, from May 22 to date, nearly 1/3 of the chips have been lost between 0.7-1.2, especially around 0.85. However, the consensus area is still concentrated around 0.85. A very large support level is formed around 0.85. If you can build a position near this level, it will be very beneficial.

Above 1, there is no large area where chips are concentrated, and it can even be said that it is a smooth road. Once the bull market comes, the resistance to the rise will be very small. Once it rises, the speed and increase will be very fast.

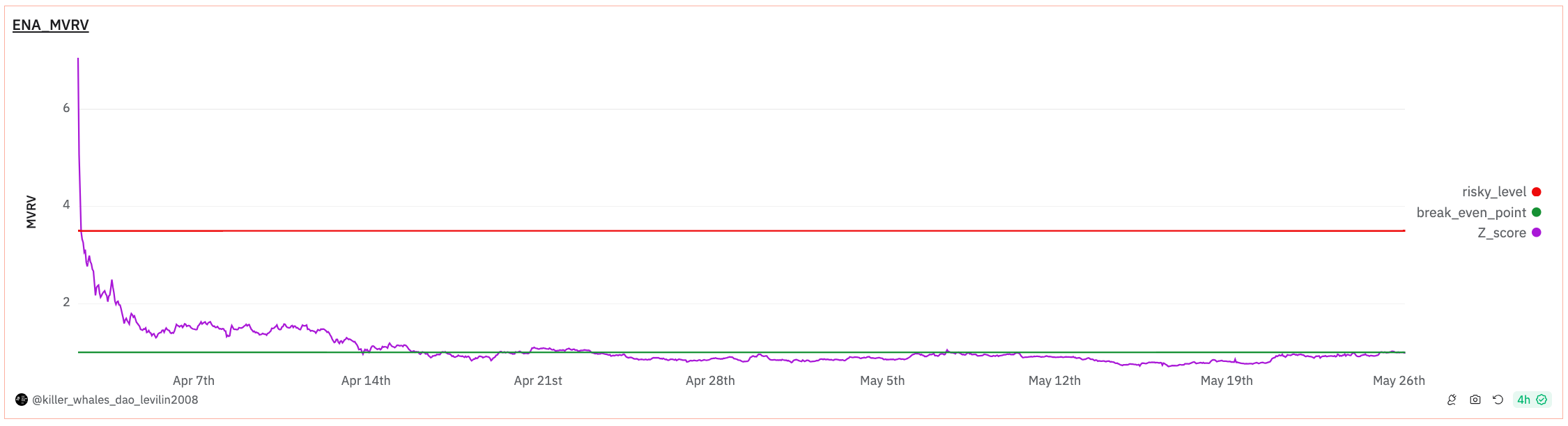

6.2 MVRV indicator analysis

Let’s look at the Z_score indicator of MVRV (Market Value to Realized Value) .

MVRV-Z Score = Circulating Market Value / Realized Market Value, where "Realized Market Value" is based on the value of the currency transferred on the chain, and is calculated by summing up the "last moved value" of all the currencies on the chain. Therefore, if this indicator is too high, it means that the market value of the currency is overestimated relative to the actual value, which is not conducive to the continued upward movement of the currency price; otherwise, it is underestimated. According to past historical experience, when this indicator is at a historical high, the probability of the currency price showing a downward trend increases, and attention should be paid to the risk of chasing high prices. When this indicator is below 1, it means that the average holding cost of the entire network is a loss, and opening a position in the range below 1 will have greater psychological and cost advantages than all holding users.

When the indicator is above 3, it means that the profit of the entire network is more than 3 times, and it has entered the risk area. You can consider taking profits in stages and batches.

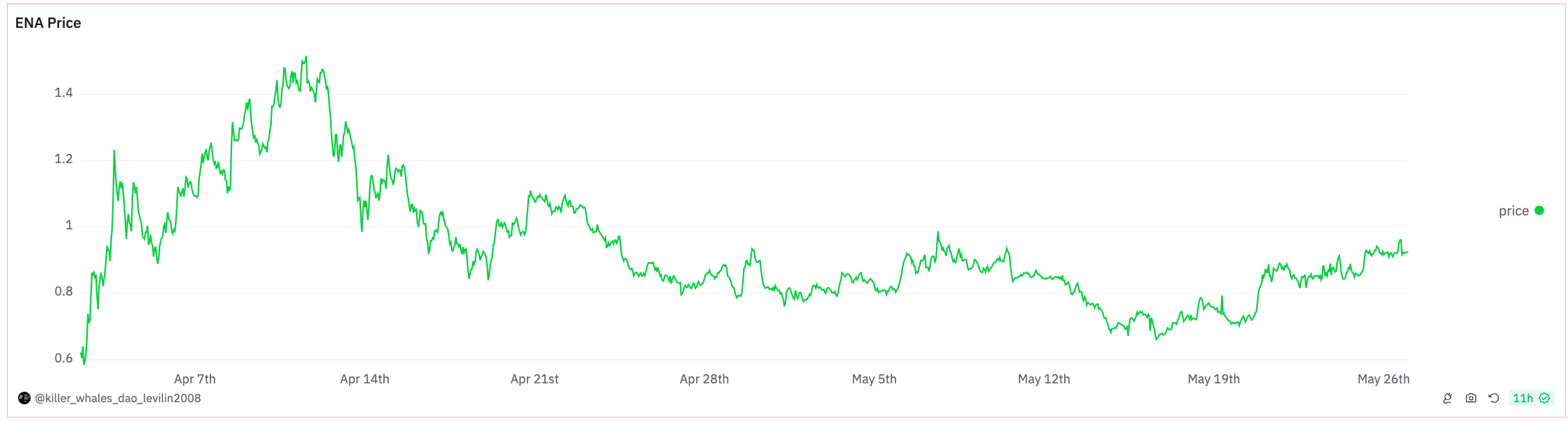

As for ENA's MVRV indicator, we can see from the above figure that since April 14, ENA's MVRV indicator has been concentrated around 1, with the lowest reaching 0.71. Currently, Z_score is 1, which is a good time to invest and build a position.

Therefore, the current area is suitable for building a position. It would be better if you can build a position at around 0.85 or even lower.

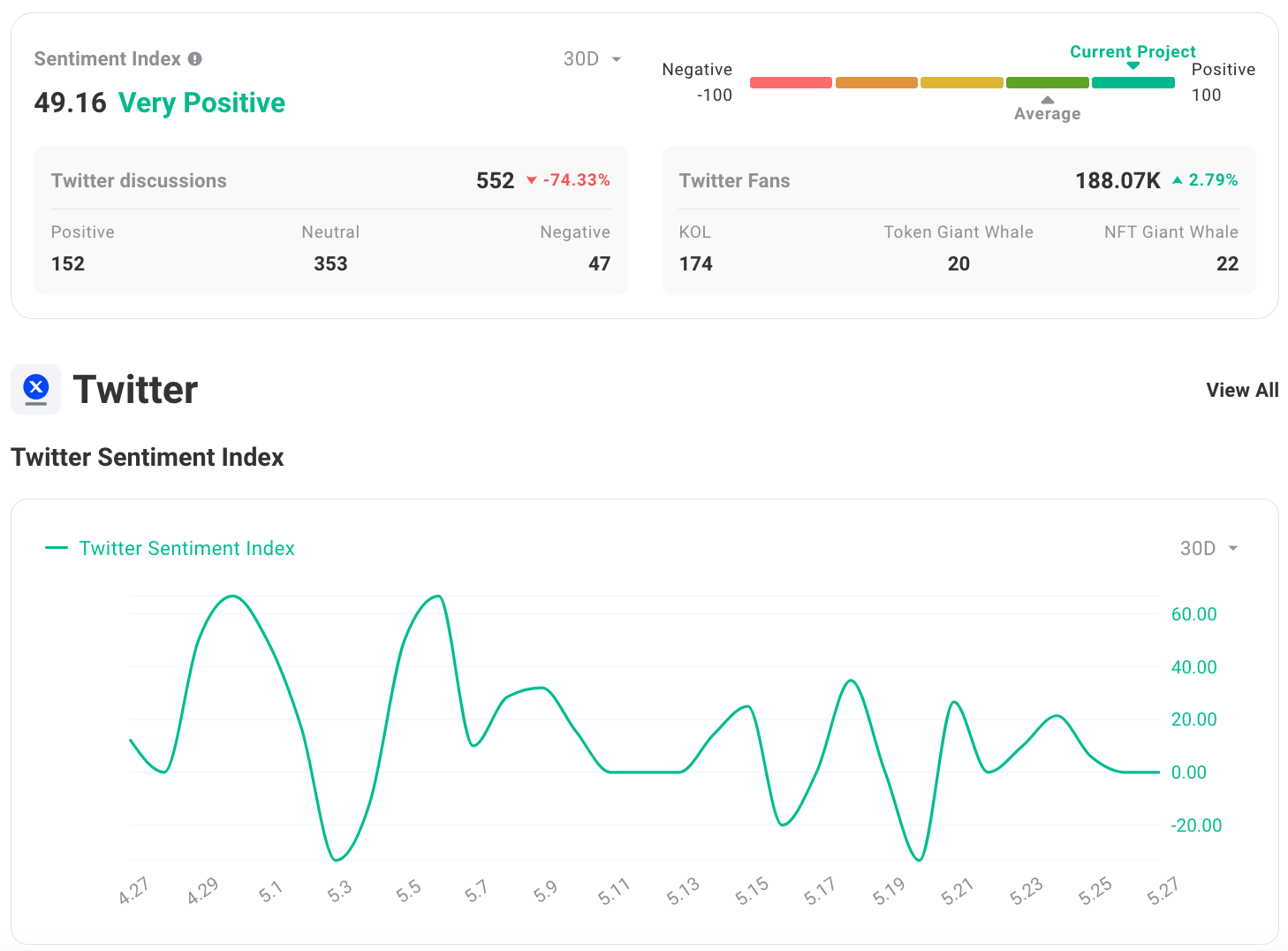

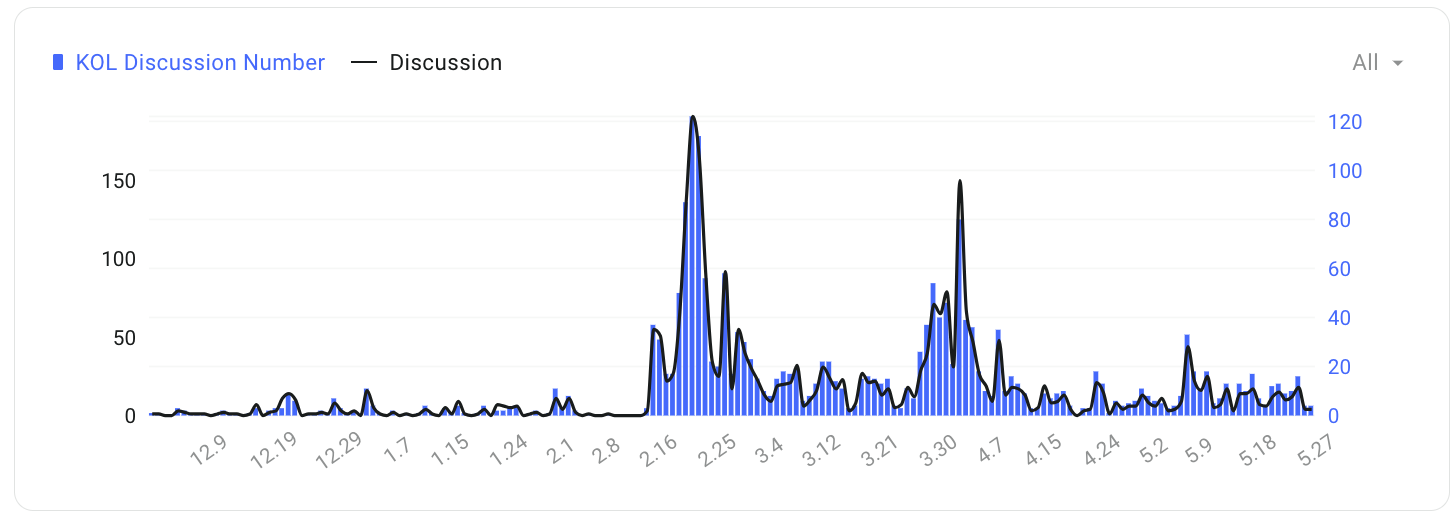

Chapter 7 Market Heat

The market is also very enthusiastic about ENA. From the following three pictures, we can easily find that:

Although the price of ENA has been adjusted due to the overall market correction, the market and KOLs have always been very positive about ENA. In addition, KOLs' attention to ENA has shown an overall increasing trend in May compared to April, which also indirectly illustrates ENA's technical advantages and future development prospects.

Chapter 8 Summary

ENA (Ethena) makes it possible for the web3 world to have independent currency (stablecoin) issuance and pricing rights. It has huge growth potential and imagination space in the future. Combining Mr. Lin @levilin 2008 chip distribution and MVRV chain data, it is now a good time to invest in batches and build positions with relatively low risks.

ENA (Ethena) is currently the most perfect decentralized stablecoin project. We hope that the ENA project can continue to update and iterate, and resolve potential risks with more appropriate technologies and methods.