Nansen Ethereum Merger Report: Censorship Risk of PoS and Its Impact on Staking

TLDR

secondary title

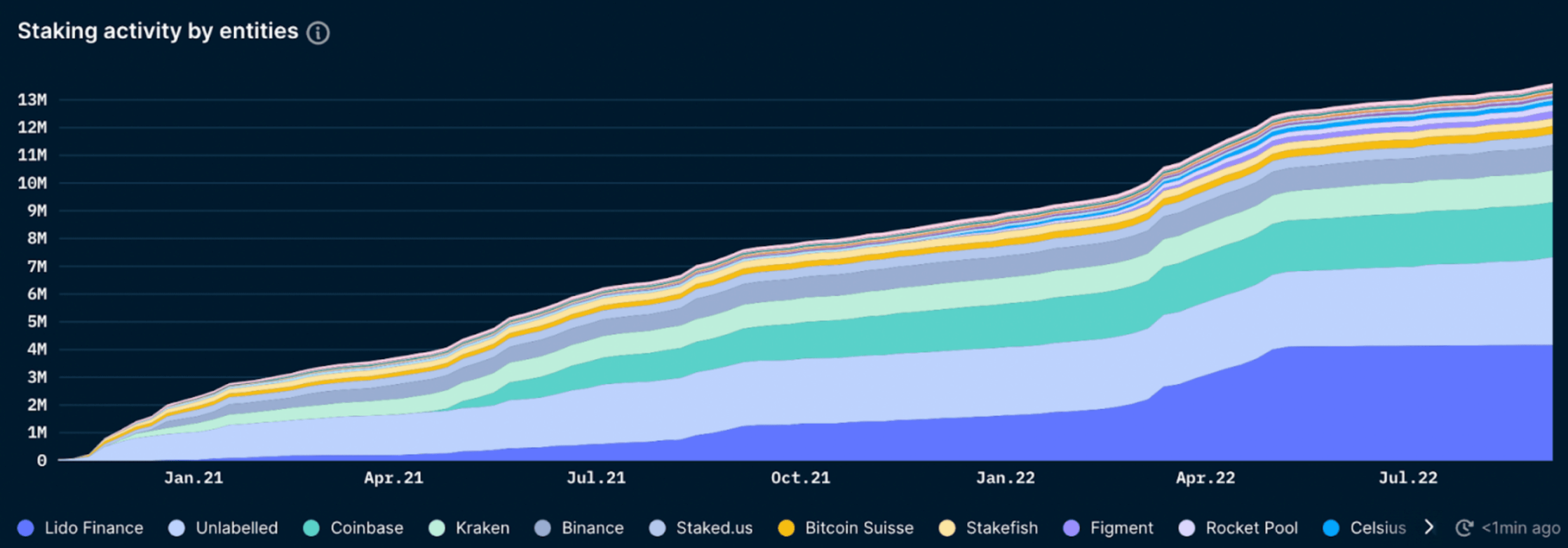

At present, the proportion of pledged ETH accounts for a relatively small proportion of the overall ETH (about 11.3%), of which 65% are liquid pledges and 35% are illiquid pledges. Despite a very high number of validator addresses (426k) and unique deposit addresses (~80k), approximately 64% of staked ETH tokens come from 5 entities.

Lido holds the most staked ETH (31%), followed by Coinbase, Kraken, and Binance with a combined ~30%. Liquid staking services like Lido were created to avoid the possibility of entities like centralized exchanges CEX getting most of the staked ETH. For liquid staking providers like Lido, it is important to become decentralized to resist censorship.

The ownership of Lido's governance token LDO is relatively concentrated, and the largest token holders are identifiable fund and team members, which can be said to be at risk of being censored. For example, the top 9 addresses (excluding treasury) own about 46% of the governance power, with a small number of addresses usually dominating proposals. For an entity with a potentially majority share of staked ETH, the stakes for proper decentralization are very high.

The vast majority of ETH tokens in pledge (about 71%) are currently in a state of floating loss. 18% of all staked ETH are illiquid stakers in floating profit - these people, after Ethereum's Shanghai upgrade enables free conversion, are most likely to sell for a profit.

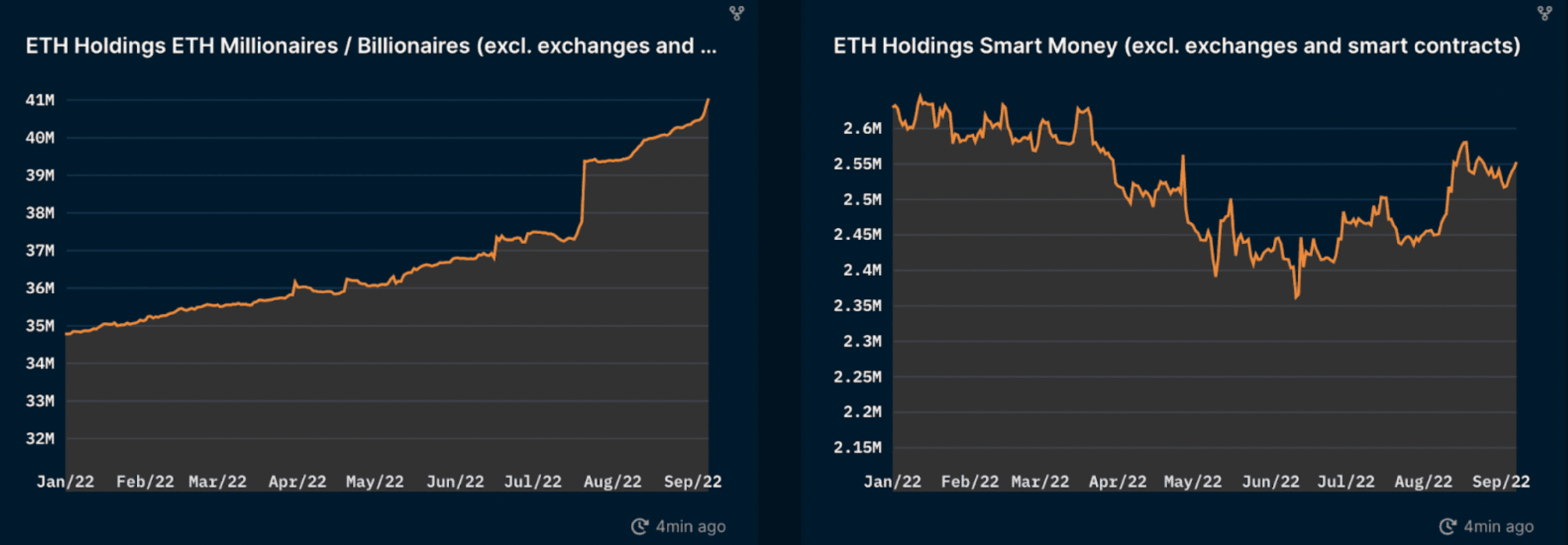

Big ETH whales have been accumulating ETH tokens this year.

Smart Money Smart money began to expand its ETH holdings at the low point in mid-June this year.

Everyone is optimistic about the merger of ETH and Ethereum?

The upcoming Ethereum merger is arguably one of the biggest events in the crypto space since Bitcoin's genesis block. The merger is when Ethereum makes a change at the consensus layer by moving from Proof-of-Work (PoW) consensus to Proof-of-Stake (PoS). With cryptocurrencies now in a bear market, The Merge has been a hot topic for the past few months; but is it really worth the hype?

While everyone agrees, The Merge cut Ethereum’s energy consumption by about 99.95%, a positive development for a crypto industry that has been criticized for its poor energy-wasting image. But other effects of PoS have divided the community.

In the report below, we attempt to discuss and express our views on two main issues:

Will PoS introduce more risk of censorship at the validator level?

Will the shift to PoS lead to increased short-to-medium term selling pressure on ETH tokens from non-stakers?

After converting to POS, will it lead to more centralization?

As Ethereum moves to PoS consensus after the merger, a key issue is the centralization, centralization, of staked ETH.

One of the original ideas of blockchain was to achieve decentralization. But energy costs and economies of scale for mining equipment eventually lead to large centralized mines and pools. This has led, among other arguments, to discussions of other technical solutions such as PoS.

On the other hand, some believe that PoS itself can lead to centralization. Many people tend to choose liquid staking or staking through a third party out of convenience, and staking service providers are also a market that benefits from economies of scale.

Larger entities may have an advantage in the distribution of MEV benefits.

In addition, the most liquid Staking derivatives, integrated with CEXs and DeFi, have a strong leading competitive advantage, and the liquidity is self-reinforcing.

The actual number of unique addresses participating in staking is very high (~80k). However, the situation is more nuanced when looking at the situation of intermediate staking service providers who stake ETH on behalf of users. Thus, while stakers (eg ETH contributors) may be very diverse, the majority of staked ETH and validators may be (indirectly) controlled by a small number of entities or governing bodies.

In light of the recent events surrounding Tornado Cash, many concerns have been raised regarding the transition to PoS and the implications of centralized ownership by a small number of participants. Any major validator that acts maliciously against the network or is directly targeted by regulators could threaten Ethereum's value proposition as a secure, decentralized, and censorship-resistant infrastructure.

The following table is the statistics of the top five pledge entities

image description

Source: https://etherchain.org/miner, Nansen, September 9, 2022

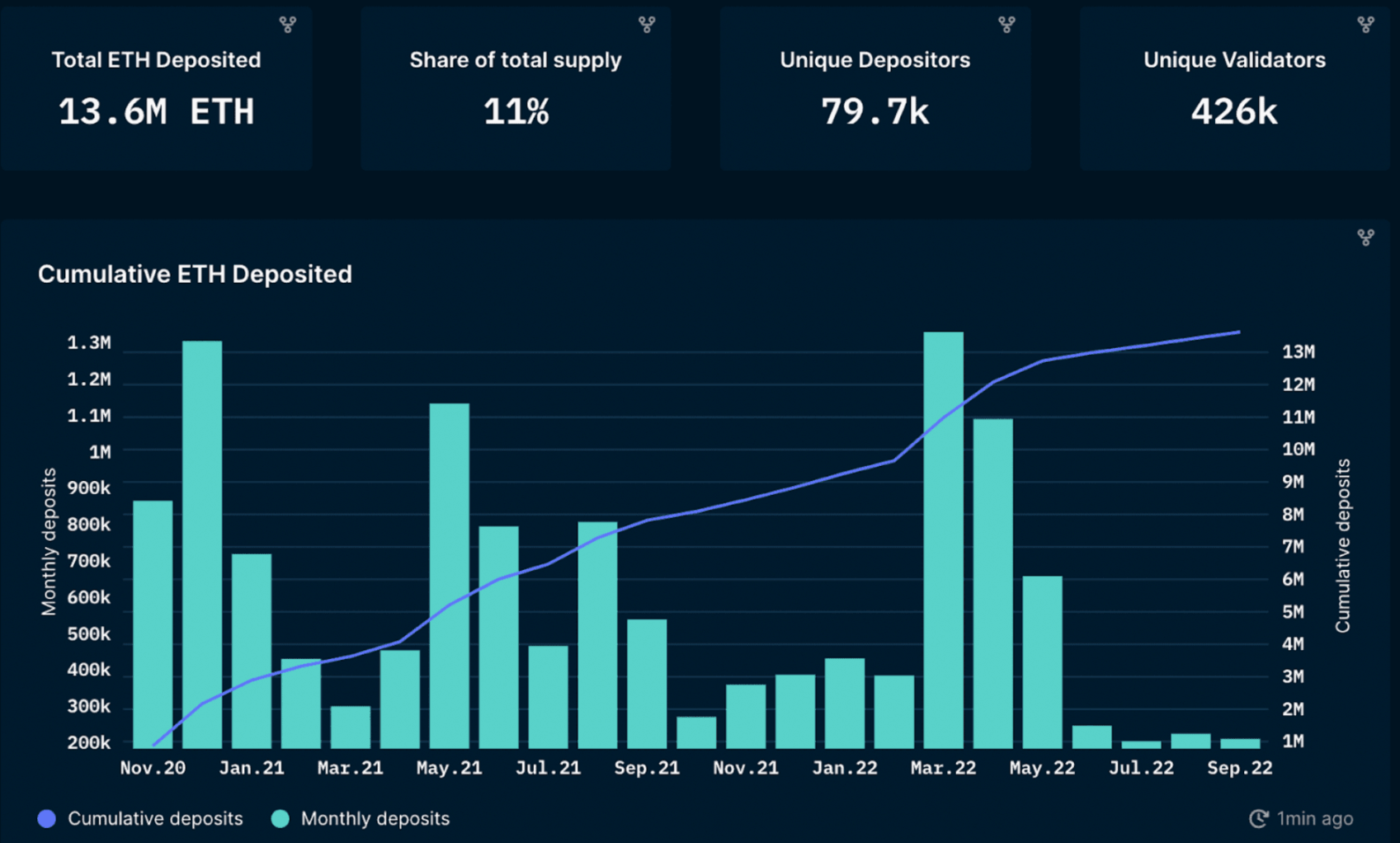

How much Eth is staked and when?

image description

Source: Nansen Query

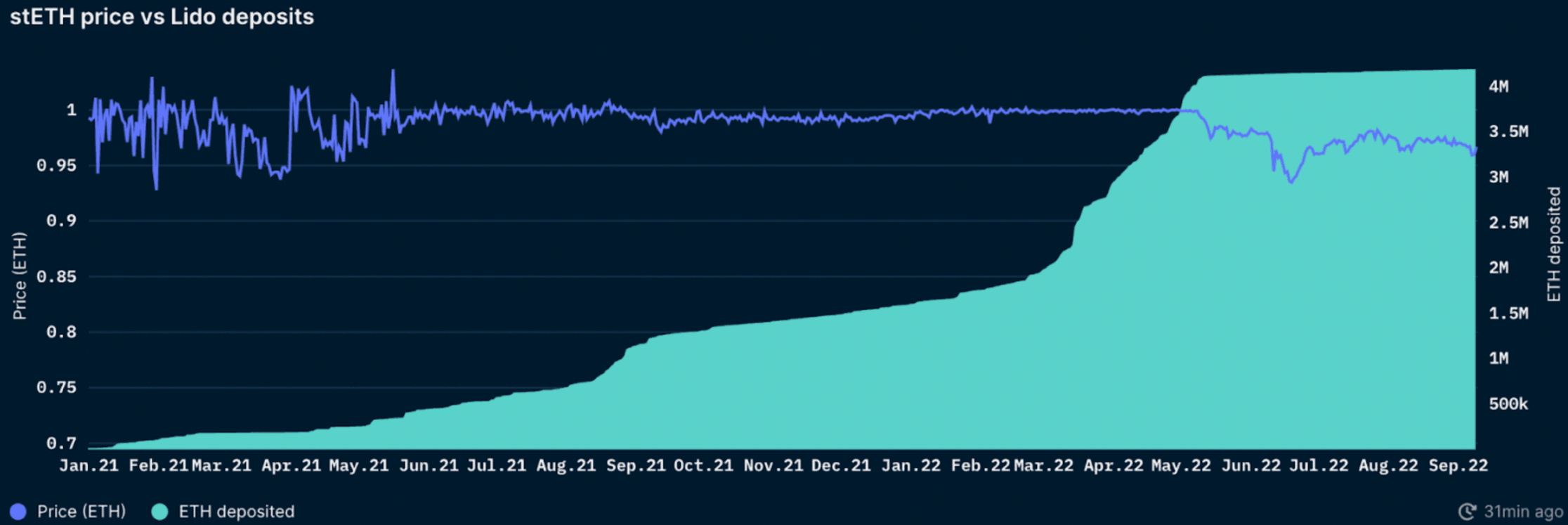

Nansen data shows that the amount of ETH deposited each month is highly volatile and has recently seen a significant decline. Note that the total amount of ETH staked "only increases" since withdrawals have not yet been enabled. The significant decline after May can be attributed to the impact of the LUNA crash and subsequent FUD and the "decoupling" of ETH and stETH. In total, 11.3% of the ETH supply is staked.

This compares to roughly 41% MATIC staked (Polygon) and 77% SOL staked (Solana). The proportion of pledged ETH is relatively small, which may be due to:

The threshold for running a validator node on your own is high (32 ETH).

Lack of liquidity: Post-merger, staked ETH will remain locked until the Shanghai upgrade, expected sometime in 2023, will unlock it.

Liquidity staking providers such as Lido and Binance address this liquidity issue by enabling users to receive fungible derivative tokens representing their staked ETH positions.

A total of 65% of all ETH staked is with liquid staking providers.

Liquid staking providers also enable users to stake in amounts of less than 32 ETH.

However, solving the staking liquidity problem by using Lido and Binance etc. introduces new risks, namely counterparty and smart contract risks.

technical risk

There is uncertainty about when the merger will happen.

Whether Merge can be executed normally, and whether the PoS chain is adopted is uncertain.

In the event of misconduct, validators face the risk of being penalized or even slashed.

Slight penalties (e.g., going offline for a few days) are imposed for unintentional actions (or inaction) that impede consensus.

Significant penalties for malicious behavior (such as proven invalid or contradictory blocks) – outright confiscation.

To minimize slashing risk to stakers, Lido stakes ETH across multiple node operators (with a heterogeneous setup). If your chosen operator goes out of business, you won't be able to re-delegate or switch to another operator until transactions are enabled on the new chain (meaning you won't be able to earn any rewards for your ETH). Additionally, as mentioned above, node downtime is also slashed, although Lido charges a 10% fee on staking rewards between node operators, the DAO, and an insurance fund to help with such incidents.

Low returns compared to other DeFi protocols: Many DeFi protocols offer higher returns than Ethereum staking, which can lead to less incentive to stake ETH.

If the merger goes according to plan, monthly staked ETH may increase as the merger execution risk decreases. Liquid staking derivatives solutions should benefit from this increased confidence given the relatively small amount of ETH currently staked. However, this also depends on market conditions, and the positive impact could be negated if cryptocurrency sentiment deteriorates further. Concerns have been raised about the risks of centralizing staked ETH in a few entities — something that appears to be happening to some extent.

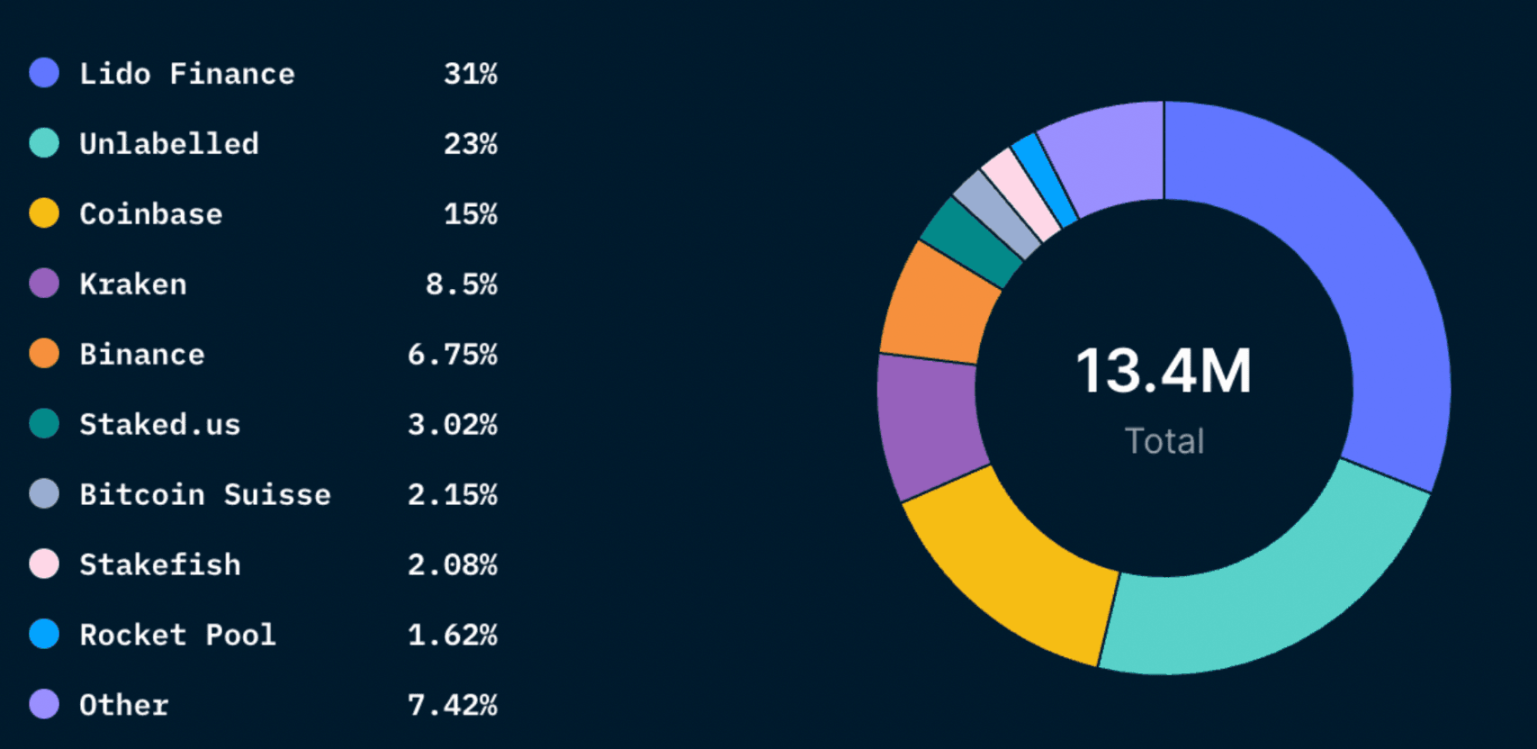

ETH Pledge Entity Distribution Map

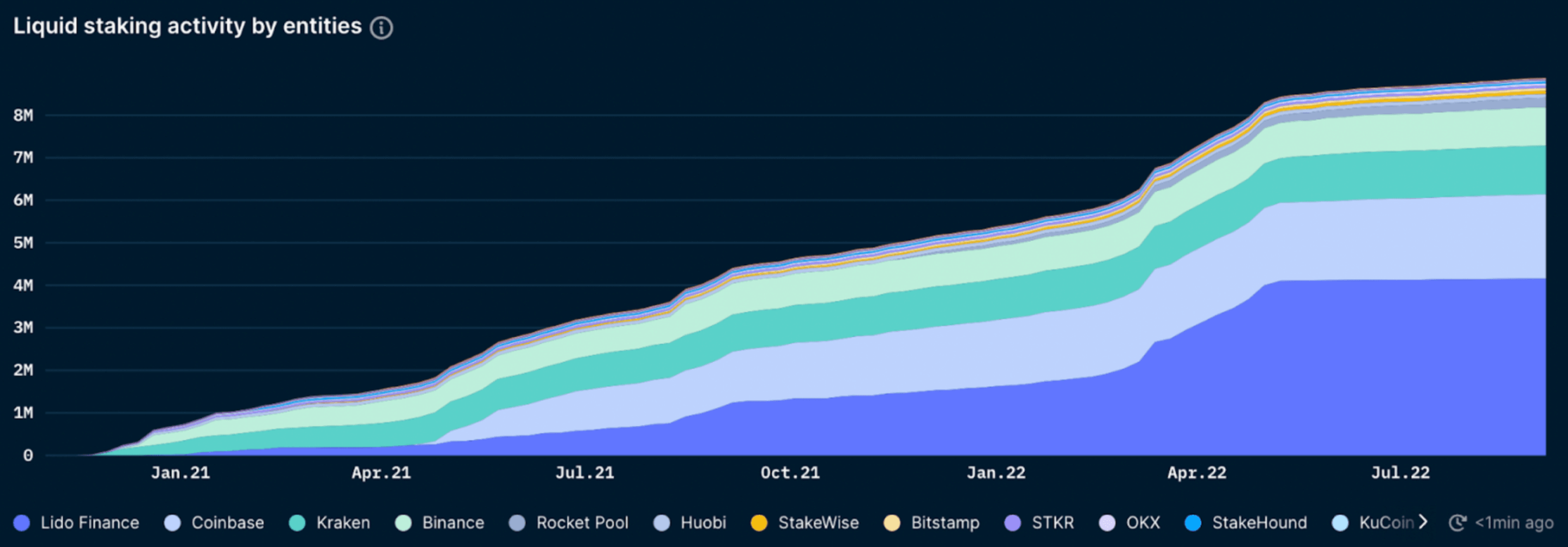

Lido (a decentralized on-chain liquidity staking protocol) is the largest staker of ETH, collectively owning ~31% of all staked ETH. After Lido; Coinbase, Kraken, and Binance own around 30% of staked Ether, according to Nansen's wallet tags and on-chain data. These centralized exchanges must comply with regulators in the jurisdictions in which they operate. In order to solve the major risk of centralized exchanges accumulating most of the pledged ETH, liquid pledge derivatives platforms such as Lido have been established to realize the participation in pledge without permission. Lido is the largest staker of ETH, does its dominance pose another risk?

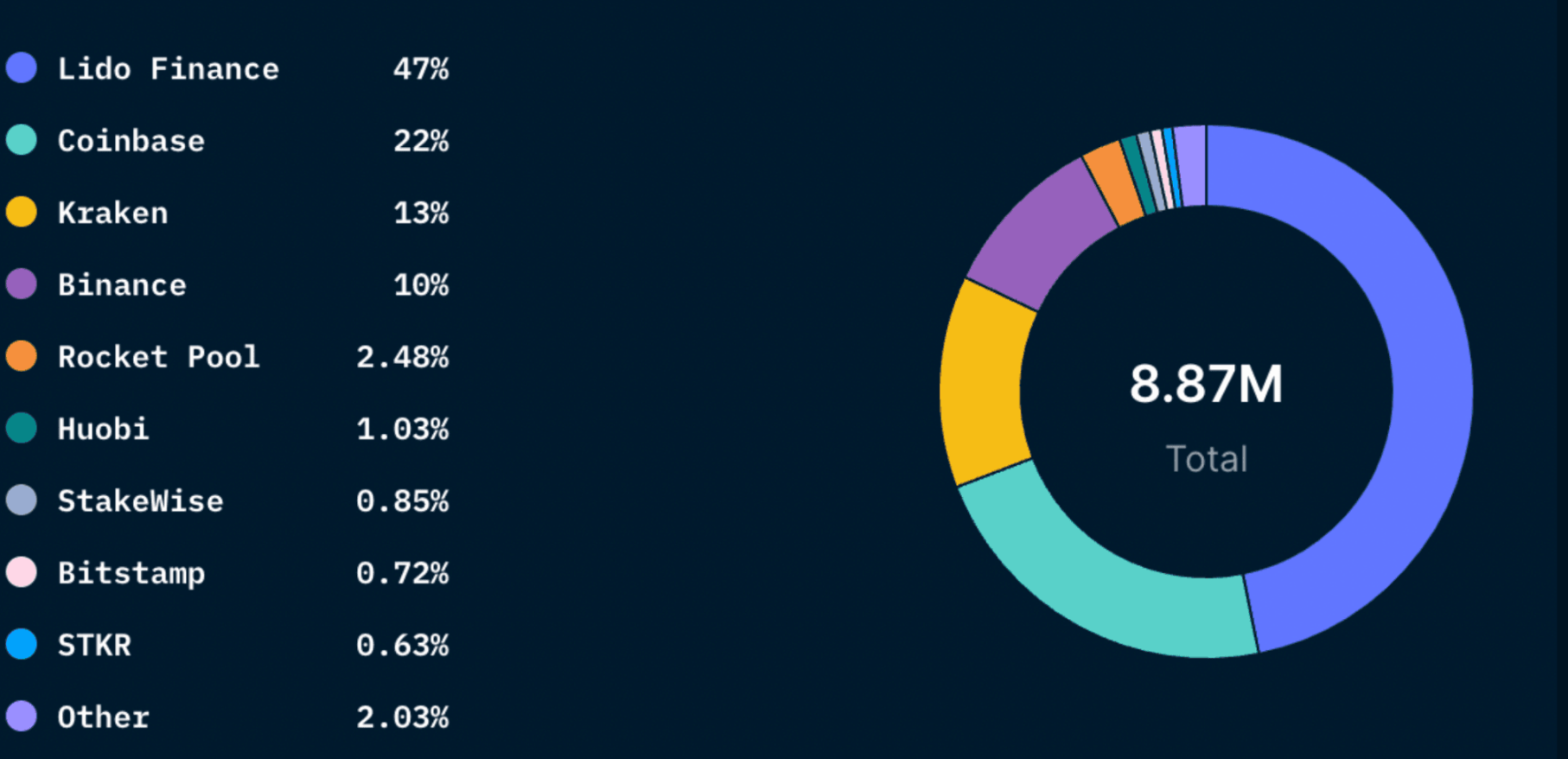

Looking further at the liquidity staking solutions market, Lido is about 47%, while the three major exchanges combined are about 45%. This shows that although Lido occupies a dominant position in market share, it is essentially comparable to the three major centralized exchanges. This reinforces the argument that platforms like Lido are important to mitigate the dominance of centralized exchanges versus staking ETH.

Liquidity ETH pledge after excluding CEX

Zooming in further on liquidity staking providers excluding centralized exchanges, we can see Lido’s dominance. Lido has over 90% of the market, with Rocket Pool in second place with just under 5%.

Can Lido be censored?

Lido is a decentralized DAO organization governed by the LDO token, which is set up in such a way as to allow multiple validating nodes. While this structure is clearly harder to target for regulators, some have raised concerns about the centralization of token ownership. This could make Lido vulnerable and expose it to centralization risks.

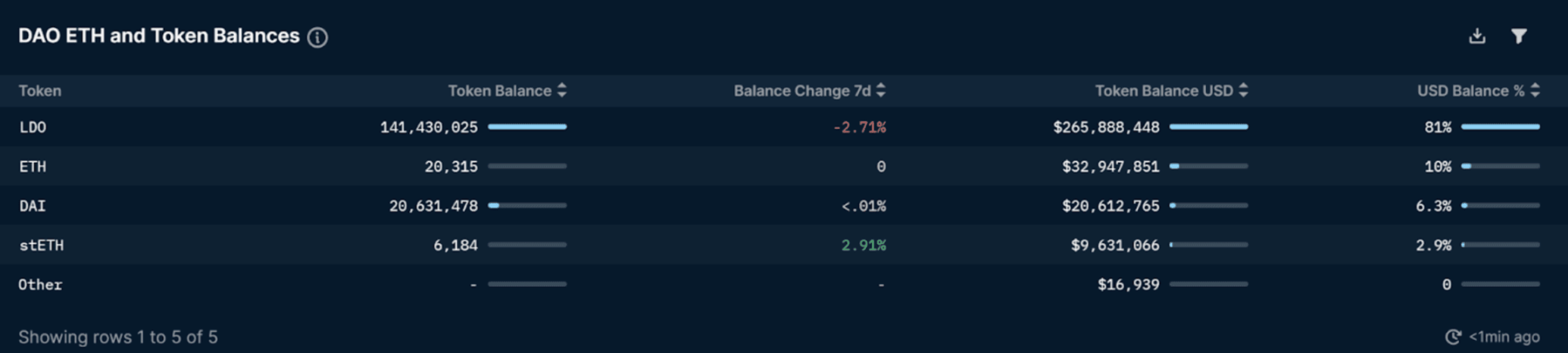

LDO is the governance token of Lido DAO. Lido DAO is responsible for setting protocol fees and other protocol parameters, selecting licensed node operators, designing incentives to improve/accelerate project development, implementing protocol upgrades and managing DAO funds. The chart below shows the breakdown of assets owned by the Treasury. As can be seen, the total amount of liquid assets controlled by DAOs is around $330 million, which is around 3.3% of the total dollar value controlled by DAOs in this spaceb). The main assets under management include LDO, ETH, DAI and stETH. However, note that 81% or ~$265 million of its funding is in the LDO token, which is still subject to high volatility and its deployment for production use has caused the token to face additional selling pressure. Nonetheless, the DAO is well capitalized with over $20.6 million in stablecoins and over $9 million in stETH.

image description

Source: Nansen, https://pro.nansen.ai/dao-god-mode?dao_name=LidoDAO

As can be seen from the price volume chart below, the LDO price reached a high of $6 in late August 2021. Since then, prices have dropped overall for almost a year. After the June lows of this year, prices and volumes only began to recover significantly after early July 2022, as optimism began to grow that The Merge would be implemented by the planned date.

In order to participate in Lido DAO governance, members must hold LDO tokens. Members' votes are given some degree of weight based on how much LDO they hold in the voting contract. An individual's influence is proportional to the amount of LDO tokens he/she has locked in the voting contract.

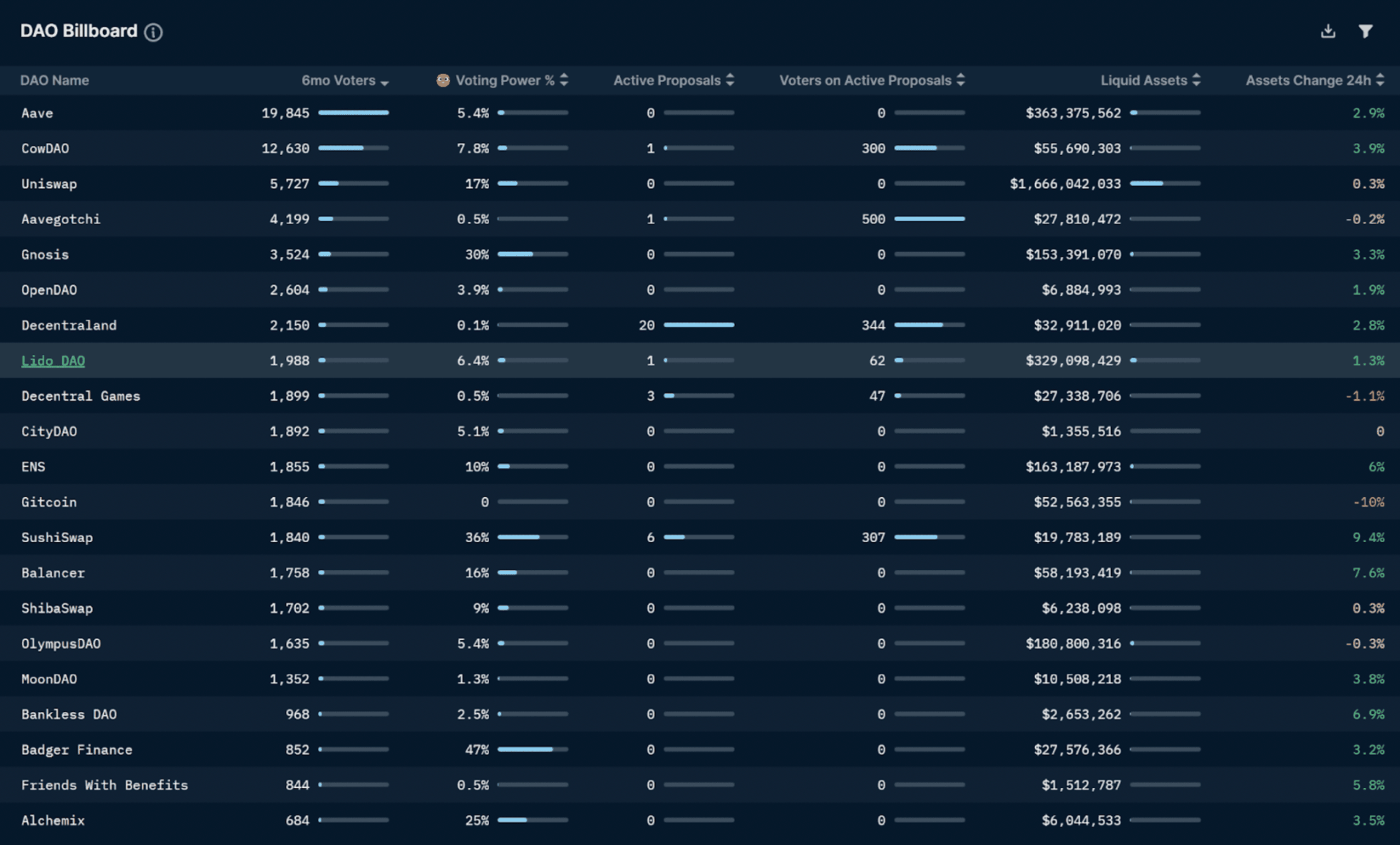

The table below gives core governance participation statistics for all DAOs over the past 6 months. Lido has 1988 unique wallets who have voted on any proposal in the past 6 months, making the DAO one of the most active DAOs in the space (#8). However, this number pales in comparison to ranking-leading Aave's 19,845 unique wallet participants. However, the number of wallets participating in governance does not truly reflect the degree of decentralized governance, because voting power is related to the number of tokens held by the wallet, not on the basis of 1 wallet 1 vote.

The table below gives core governance participation statistics for all DAOs over the past 6 months. Lido has 1988 unique wallets who have voted on any proposal in the past 6 months, making the DAO one of the most active DAOs in the space (#8). However, this number pales in comparison to ranking-leading Aave's 19,845 unique wallet participants. However, the number of wallets participating in governance does not truly reflect the degree of decentralized governance, because voting power is related to the number of tokens held by the wallet, not on the basis of 1 wallet 1 vote.

Furthermore, by analyzing the voting power of the participants, it can be seen that only 6.4% of the voting power is concentrated in tokenized Smart Money wallets. This is much lower compared to Smart Money’s voting power in Perpetual Protocol (60%), Badger Finance (47%) or PleasrDAO (46%), which occupy the first, second and third positions respectively. However, if we look at voting rights exercised by Smart Money wallets over the past 30 days, this number jumps to 9.3%. This suggests that some Smart Money wallets have been actively participating in governance recently. By analyzing Smart Money's voting patterns over time, their participation and influence can be understood to a greater extent.

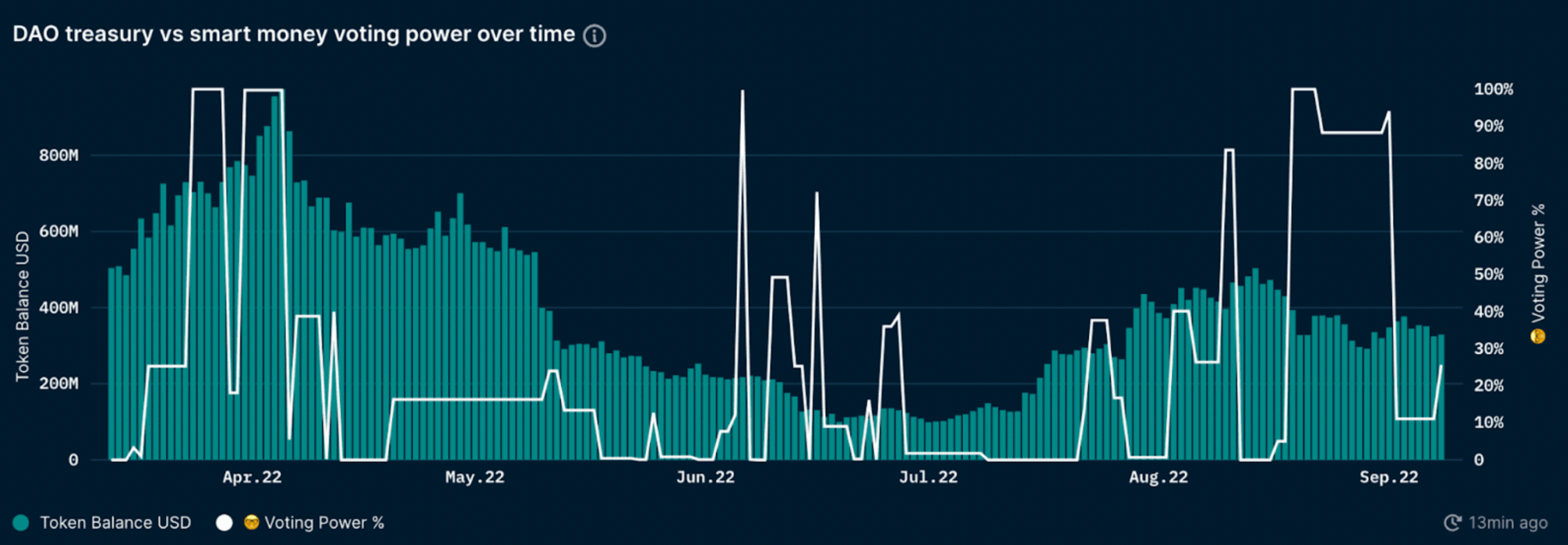

Below is a graph showing Smart Money voting rights and DAO treasury balances over time.

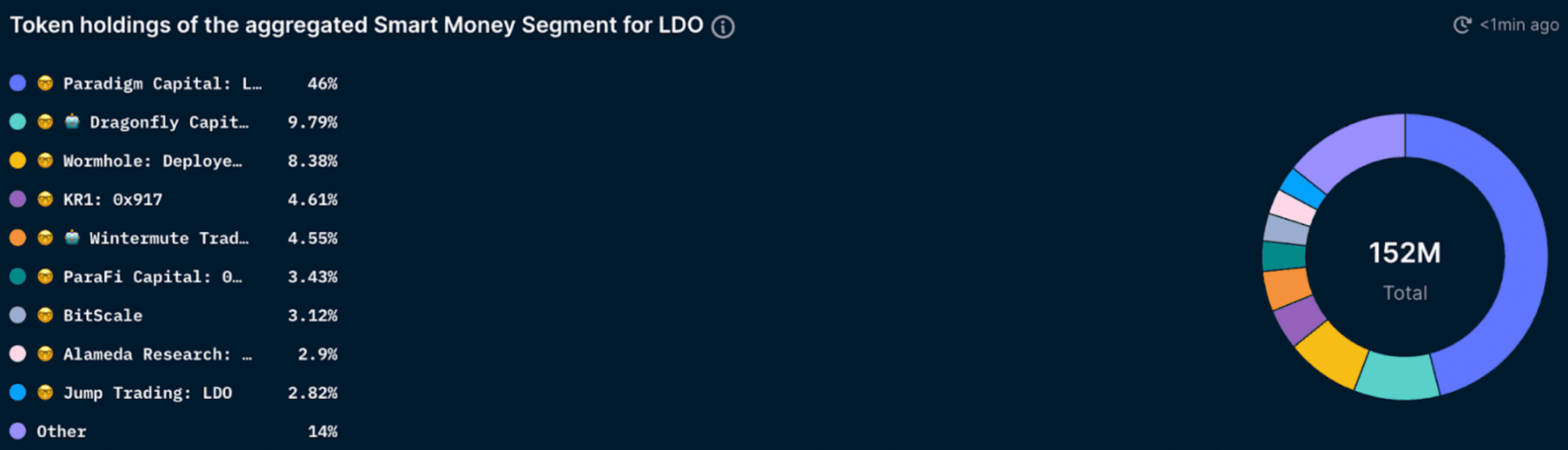

It can be clearly seen that the voting power of Smart Money wallets fluctuates wildly over time. This highlights that Smart Money wallets will not participate in every governance proposal, but will only vote on the most important ones. It is important to note here that voting rights are exercised in any proposal, not governance token holdings. Zooming in, we can also see a breakdown of LDO holdings in Smart Money wallets, as shown in the image below.

As can be seen, the tokenized Smart Money token wallet holds 152 million LDO tokens overall. This is quite a large amount compared to the total circulating LDO supply of approximately 996 million. Of the Smart Money token wallets, Paradigm Capital has a 46% share, followed by Dragonfly Capital at about 9.8% (but it's important to remember that a single entity may be behind multiple wallet addresses that have not yet been flagged ). However, this highlights that even within Smart Money wallets, token holdings are concentrated in a very small number of wallet addresses. The graph below shows the balances of the top wallets holding LDO tokens (for all holders). Interestingly, Smart Money wallets are not dominant (with the exception of Paradigm Capital).

For the purposes of the graph above, Lido DAO treasury wallets (14% of total supply) are not counted as these tokens are neither in circulation nor used for governance. As mentioned earlier, the Lido DAO treasury is used for liquidity incentives, advisory services and further token sales. These allocations can have further concentration effects. As shown, the overall ownership of LDO is relatively concentrated, which may pose a centralization risk for Ethereum if Lido dominates the staked ETH. The top 9 addresses hold about 46% of governance power and could theoretically have significant influence over validators (assuming they are vetted by the DAO and can be removed via governance).

If Lido's market share continues to rise, it is possible that Lido DAO holds the majority of Ethereum validator nodes. This could allow Lido to take advantage of opportunities such as more block MEV, profitable block reorganization, and in the worst case censor certain trade. This can cause problems for the Ethereum network. On the other hand, if Lido is self-limiting, there is also the risk of a centralized exchange-dominated collateralized derivatives market, a situation that may be easier to scrutinize than attempting Lido governance capture. As an example of LDO concentration risk, 50% of the voting power on the proposal to sell tokens to Dragonfly consisted of only 2 wallets, while the top 5 wallets exercised almost 80% of the voting power. This is a sign of governance centralization, which could become a problem if Lido continues to maintain its staked ETH market share.

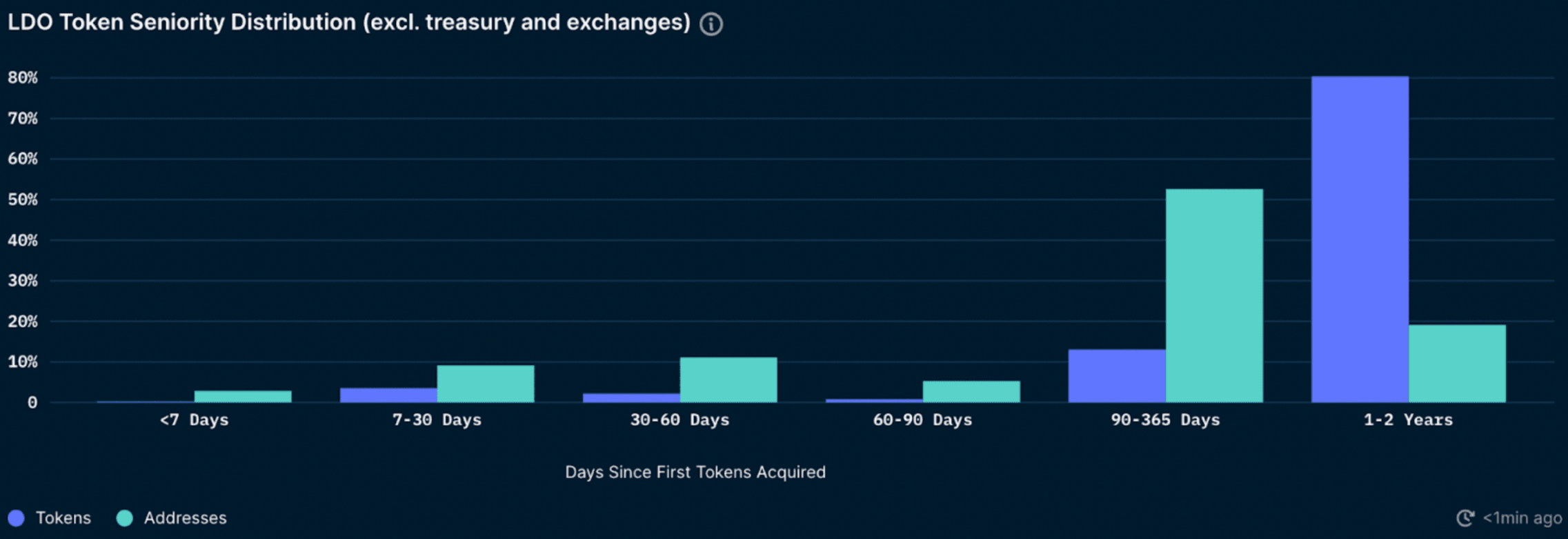

The graph above also gives us a better understanding of LDO token holders. More than 81% of tokens (19% of addresses) were acquired 1-2 years ago, indicating that these addresses have been holding for a long time. Looking at the token seniority distribution graph, you can see a slight uptick in tokens earned between 30-60 days and 7-30 days. However, the small uptick in both cases represents a relatively small percentage of the overall LDO tokens in circulation (only ~2-3.5%).

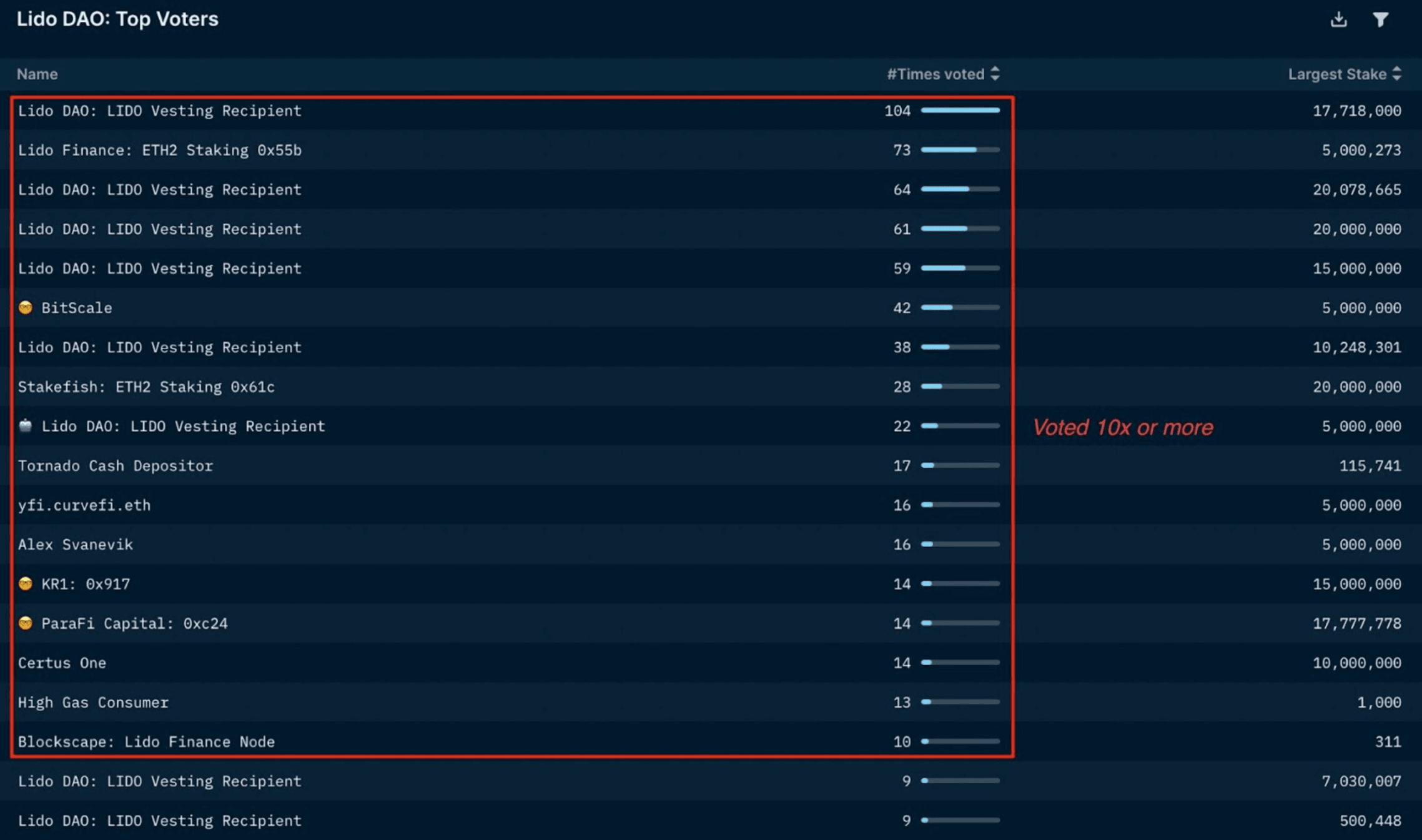

The top voters and influencers in the DAO can also be identified by looking at historical votes, as shown in the table below. Nansen data shows that there are a large number of wallets with significant influence in DAO governance, most of which are Lido investors. This makes sense and isn't necessarily a criticism of Lido, as it's still a relatively new protocol. Early iInvestors will inevitably have a larger share of voting rights. However, it will be interesting to see if this voting power declines over time and becomes more distributed.

The “turnout” for most proposals in the Lido DAO was low, with only 17 wallets participating in 10 or more proposals. There are also significant differences between the most active wallets in The DAO. While the wallet with the most votes participated 104 times, that number dropped to 17, making it the 10th wallet with the most votes. Also, there are only three Smart Money wallets (especially all funds) among the top 20 wallets with the most votes. BitScale topped the list with 42 votes, followed by KR1 and Parafi Capital with 14 votes each. Additionally, by examining each wallet's maximum voting power in proposals (over the past 6 months), we can identify the top influencers in the DAO.

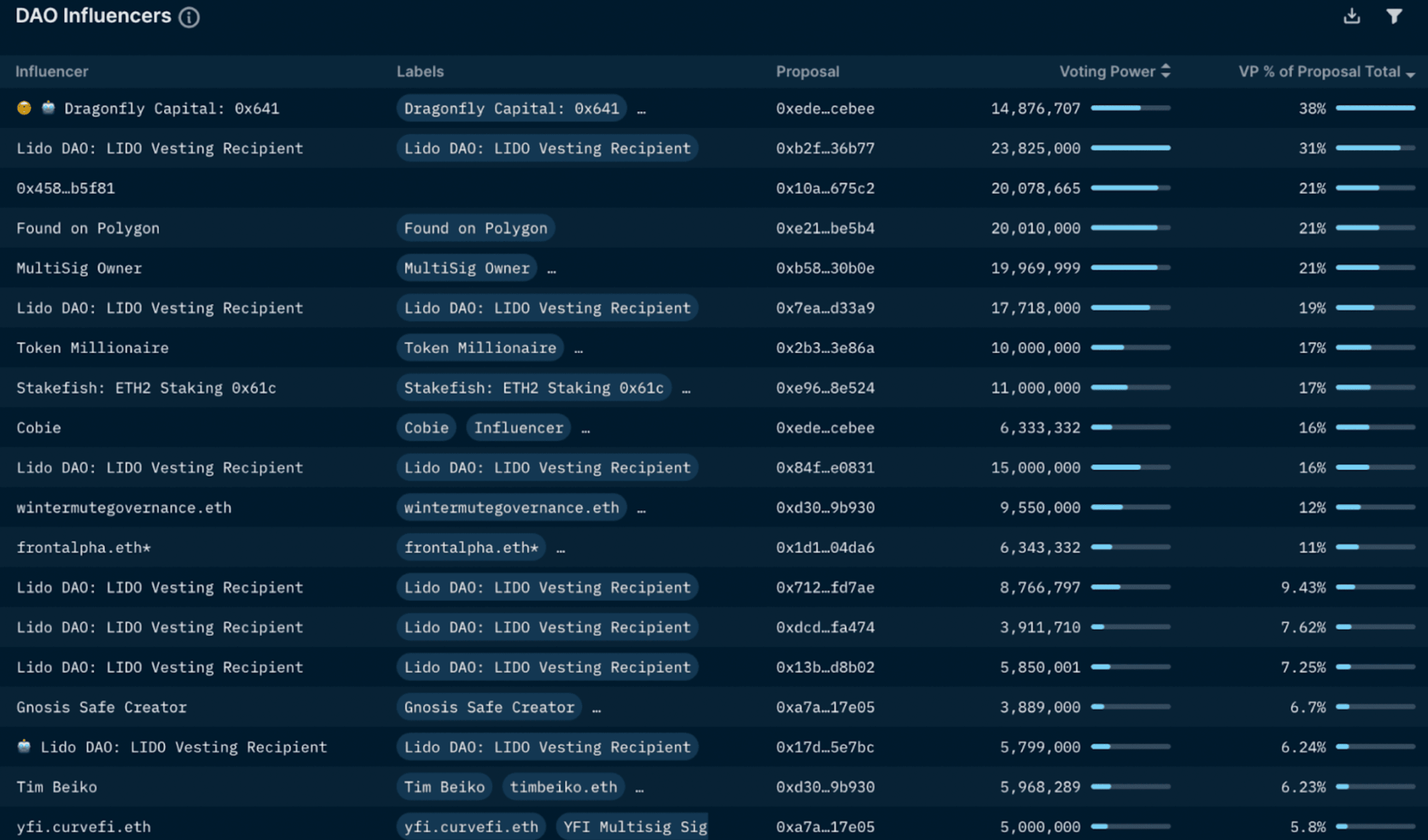

Interestingly, the largest token holders have not historically been the largest influencers. The highest voting power exercised by an influencer in a proposal is 23.8 million tokens, or 31% of the total voting power in a proposal. On the other hand, the wallet's highest influence in the proposal belongs to Dragonfly Capital (38% of the total voting power in the proposal). The proposal involves allocating 1% of LDO tokens to Dragonfly Capital in exchange for a total of 14,521,530 DAI.

Interestingly, the largest token holders have not historically been the largest influencers. The highest voting power exercised by an influencer in a proposal is 23.8 million tokens, or 31% of the total voting power in a proposal. On the other hand, the wallet's highest influence in the proposal belongs to Dragonfly Capital (38% of the total voting power in the proposal). The proposal involves allocating 1% of LDO tokens to Dragonfly Capital in exchange for a total of 14,521,530 DAI.

By looking at the data from previous votes, we can see that the risk of centralization in Lido DAO does exist. Although some top token holders (including Smart Money) exercise their voting rights from time to time, their votes can have a large impact on the final decision on key proposals that may affect them the most (directly or indirectly).

It's also worth mentioning that some of the largest token holders in the Lido DAO are doxxed entities with significant off-chain funds. Therefore, if there is pressure from an external force to comply with certain proposal votes (e.g. censoring certain transactions), they are more likely to comply (out of fear of reprisal/penalty), which undermines the fairness of the vote.

Behind LidoDAO, who is operating these nodes?

Lido currently has 29 different node operators, which some believe makes Lido decentralized, and the protocol aims to increase this number of validating nodes over time. However, one can also question that the validator nodes will essentially act as one entity since they are unified by the LDO token. Becoming a Lido node operator is subject to review as the decision rests with the Lido DAO. This could lead to collusion between validators and LDO holders. In addition, Lido's node operator set is mainly concentrated in Europe and the United States. Lido has acknowledged this and is working to reduce this reliance by building a compliant and physically decentralized validator node.

How to reduce Lido centralization risk?

Lido Dual Governance Process

Lido is considering adopting a dual governance model of LDO and stETH. While LDO will remain Lido's governance token, stETH holders will be able to protect themselves by vetoing proposals that directly affect them. Rather than making stETH a governance token, it should be given a safety mechanism against Lido proposals that could adversely affect them. This is to ensure that the interests of LDO and stETH holders are better aligned, while also ensuring that the overall governance of Lido remains with LDO holders.

It is suggested that LDO holders must pledge LDO to obtain governance rights. If LDO voters approve a proposal rejected by stETH holders, their staked LDO will be slashed. While this would bring the interests of LDO and stETH holders more aligned, it could also lead to a governance deadlock for stETH holders. To prevent them from abusing the veto, another option proposed was a significant time lock rather than an outright cut. If stETH holders fail to resolve their veto, the timelock will be lifted. If this happens, the stETH that vetoes the proposal will also be seized.

There are many different permutations of how this dual governance model can be implemented, and the nuances of the dual governance model are beyond the scope of this article. For example, the slashing mechanism for rejected transactions may prevent ordinary community members from participating in governance. Note that the community has not yet decided on a final solution.

Another point to consider is that most stETH is used for DeFi protocols and may not be able to vote, reducing its governance capabilities. According to Nansen data, 21.2% of LDO holders hold one or more of stETH, astETH, crvstETH and wstETH at the same time.

Given that this segment of LDO holders own ~33% of the total LDO supply, it will be interesting to see how this affects potential vetoable decisions. One might think that what is good for Lido (and therefore LDO) is good for Ethereum (and therefore ETH), and that holders of both should take this into account when it comes to Lido governance. However, there could be a potential situation where the value and upside potential of their LDO holdings exceeds their ETH, which would incentivize these holders to protect the value of their portfolio (LDO) at the expense of Ethereum. main part. Lido is not unique to Ethereum, and if other blockchains become major growth areas, those holders may vote in ways that may not be in the best interest of the Ethereum community.

Ultimately, a well-designed dual governance system that helps align the interests of LDO holders with stETH will be important, especially if Lido maintains its leading market position. Another point to note is that if Lido can establish a secure dual governance system recognized by the market, this can allow Lido to further consolidate its leading position. If this happens, it will be extremely important that Lido remains secure and satisfactorily decentralized against censorship.

Free exchange without permission

Another measure to reduce the risk of liquidity staking derivatives platforms is to allow depositors to withdraw funds without permission (after the Shanghai upgrade). Lido stated that they prefer triggerable exits implemented at the protocol level (Ethereum) rather than pre-signed exit messages due to potential centralization tendencies and security concerns. The risk is that node operators may run away during this exit.

Lido's Moat

It will also be interesting to see if Lido depositors decide to withdraw their ETH from Lido and deposit it with competitors such as Rocket Pool. In the past 3 months, the growth of Rocket Pool's pledged ETH has almost matched that of Lido. Perhaps there will be many wallets that want to avoid the Lido monopoly and re-stake their ETH with other platforms (once withdrawing ETH is enabled).

As shown in the chart above, Lido currently holds about 91% of the liquid staking derivatives platform (excluding CEX) market share, and holds about 30% of pledged ETH. Lido's economies of scale could give it an edge in capturing additional revenue from MEVs, which could make it difficult for other players to gain market share. This leads users to choose Lido for staking because it offers the best yield (even if it is not in the best interest of the Ethereum network). This highlights the importance of the Lido DAO needing to ensure that Lido can be satisfactorily decentralized as soon as possible.

Why use Lido and other liquid staking platforms?

Many users want to earn yield on their ETH, which has led to a huge increase in staking services offered by centralized exchanges. Without the presence of Lido and other liquid staking providers, the reach of CEXs could cause serious problems for Ethereum. Liquid staking platforms offer an alternative and can be designed in a way that limits the risk of censorship. Protocols like Lido are still in their infancy, and include many community members who value decentralization and censorship resistance. If they can be satisfactorily decentralized, they can play a key role in ensuring that Ethereum remains secure, decentralized, and censorship-resistant. While PoS may be designed to achieve a "winner-in-a-majority" situation, if that winner is fragile, satisfactorily decentralized, and censorship-resistant, then Ethereum should be able to preserve these same properties.

This shows that centralized exchanges have recently received much more deposits than Lido. Limiting Lido — which has become the most popular provider of liquid staking — could lead to centralized exchanges increasing their share of staked ETH.

image description

Source: Nansen Query, September 9, 2022

Unmarked wallets are assumed to be illiquid stakes because they do not belong to the entity providing liquid stakes.

Looking at the same graph and zooming out to see the deposits of these liquid collateralized entities over time, it is interesting to see an overall flat line starting to appear when UST started decoupling and the subsequent stETH "decoupling" and FUD. Additionally, while pledged ETH deposits have slowed significantly since then, Lido’s deposit growth in particular has stagnated, while the three largest centralized exchanges have experienced higher growth.

Therefore, if users want to obtain stETH, it is more economical to buy stETH directly instead of obtaining ETH through Lido pledge. Lido doesn't hide this fact either, and actively points out to their users the cheapest options to get stETH on their website. Note that most other liquid staked ETH tokens are also trading at a discount so far, which could lead to an overall slowdown in similar staking activity.

image description

Source: Nansen Query

Other less impactful reasons could be easier access and greater perceived security when staking with CEXs, especially for retail investors or the Ethereum community's growing concern about Lido's monopoly.

How will the merger affect staking behavior?

Will more people do Eth pledge staking?

While only a relatively small amount of circulating ETH is staked, this will increase if/when the merger succeeds (as mentioned above, the total amount of staked ETH can only keep increasing until the Shanghai upgrade can unstake it).

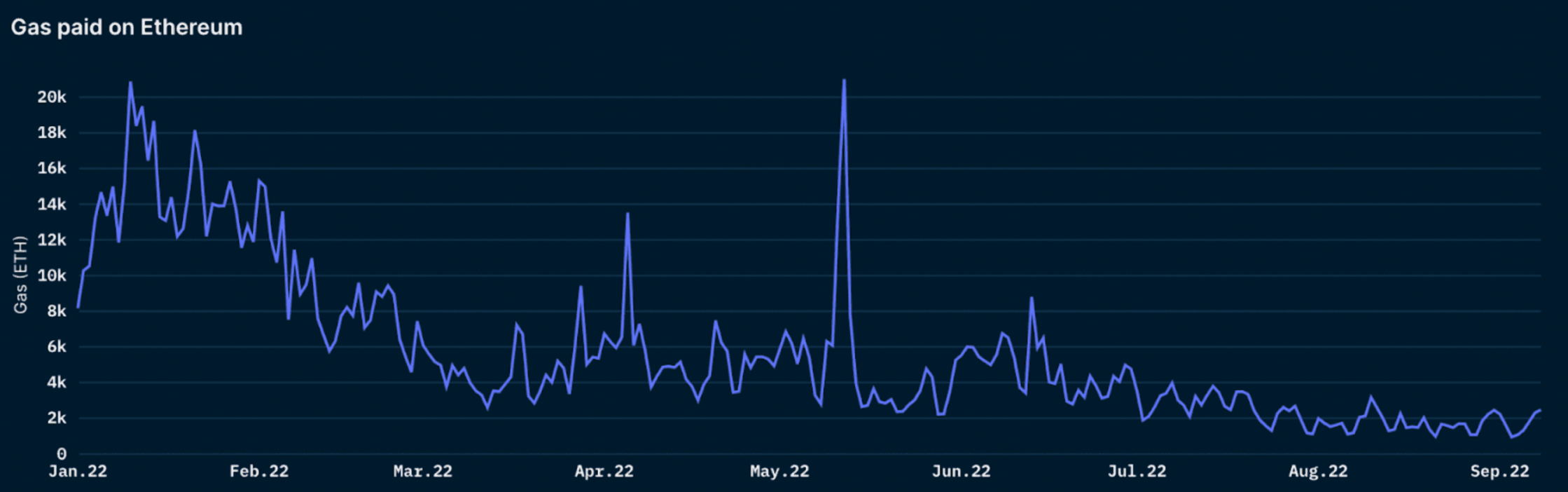

Additionally, many believe that stakers who own the underlying assets themselves are less likely to sell in the medium term than Ethereum miners before them. However, be aware that gas costs vary widely and depend on network activity on Ethereum. As the Nansen data below shows, this number has been declining over the year.

image description

Source: Nansen Query

Will those who pledged Ethereum sell after Merge?

After the merger, the pledged Eth cannot be withdrawn and sold. ETH can only be withdrawn after the upgrade in Shanghai, which is planned to be around 6-12 months after the merger.

Will stakers sell off after Ethereum Shanghai upgrade?

Even then, not everyone can immediately withdraw their staking, as the exit queue for validators is similar to the activation queue of approximately 6 validators (typically 32 ETH each) per epoch (~6.4 minutes). It currently takes about 300 days for everyone to withdraw their stake and exit as a validator, with more than 13 million ETH staked. However, validators can withdraw rewards in excess of the required stake of 32 ETH they previously acquired, as this does not require the validator to withdraw completely.

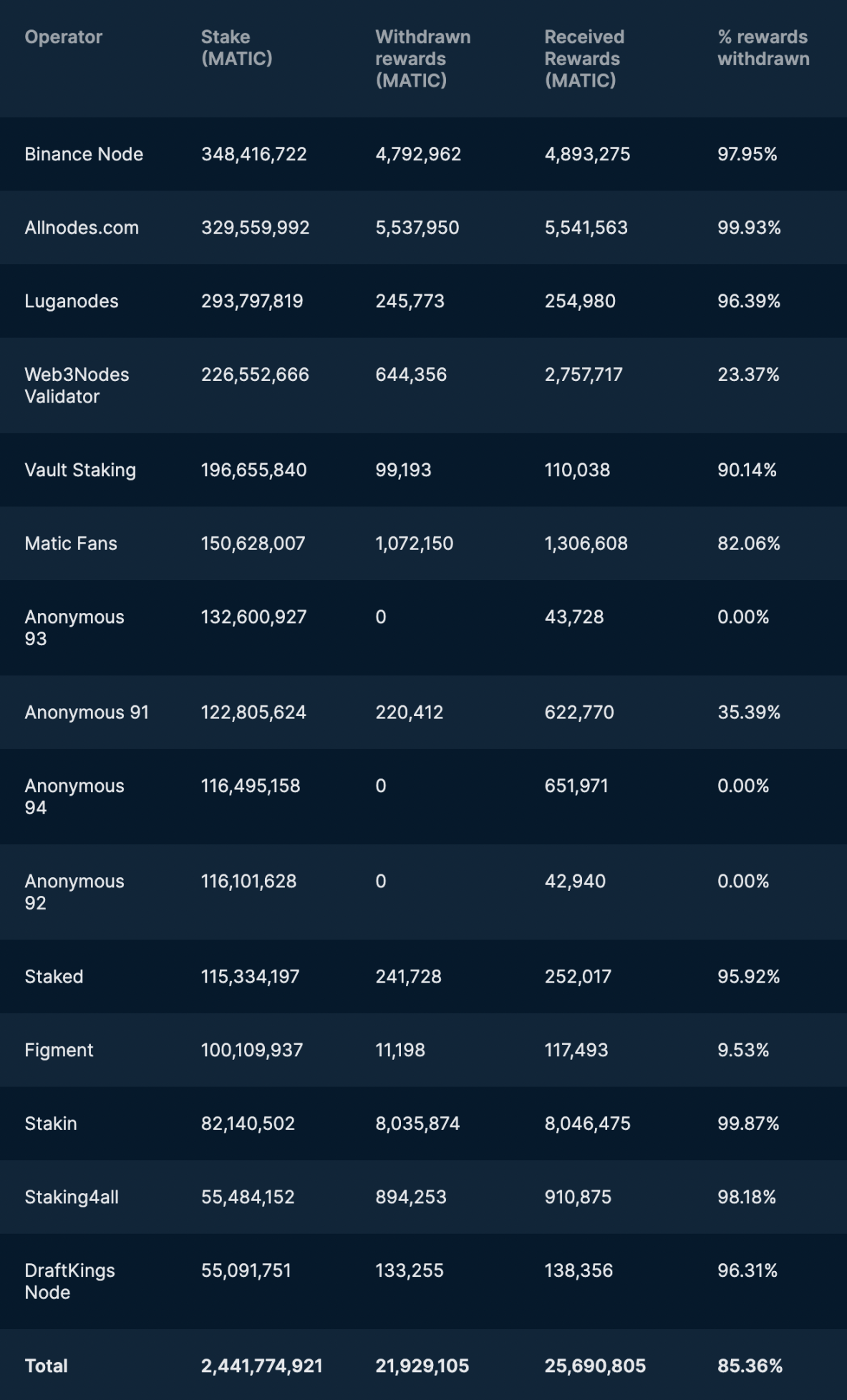

Rewards for staking

Using Polygon as a comparison, most of the rewards earned were withdrawn. However, this usually occurs more with institutional rather than anonymous and private stakers, possibly due to their internal process of redistributing staking rewards or for liquidity purposes (complete unstaking on Polygon can take ~3-4 sky).

According to data from the 15 top validators, accounting for approximately 80% of all staked MATIC, 85% of earned staking rewards have been withdrawn:

If Eth stakers could get back their staked Eth, would they sell it?

To answer this question, we first have to make some assumptions

1. Most of the sell-off came from profit-taking

The overall encryption market is stable and there is no risk of decoupling

Shanghai upgraded successfully, Ethereum is on an uptrend, overall sentiment towards ETH as an asset is neutral to bullish

2. Most illiquid stakers will unstake and sell as liquid stakers may have already exited their positions

Liquidity stakers who want to sell don't mind the possible penalties for selling liquidity tokens at a slight discount (e.g. stETH is currently trading at ~0.97 ETH)

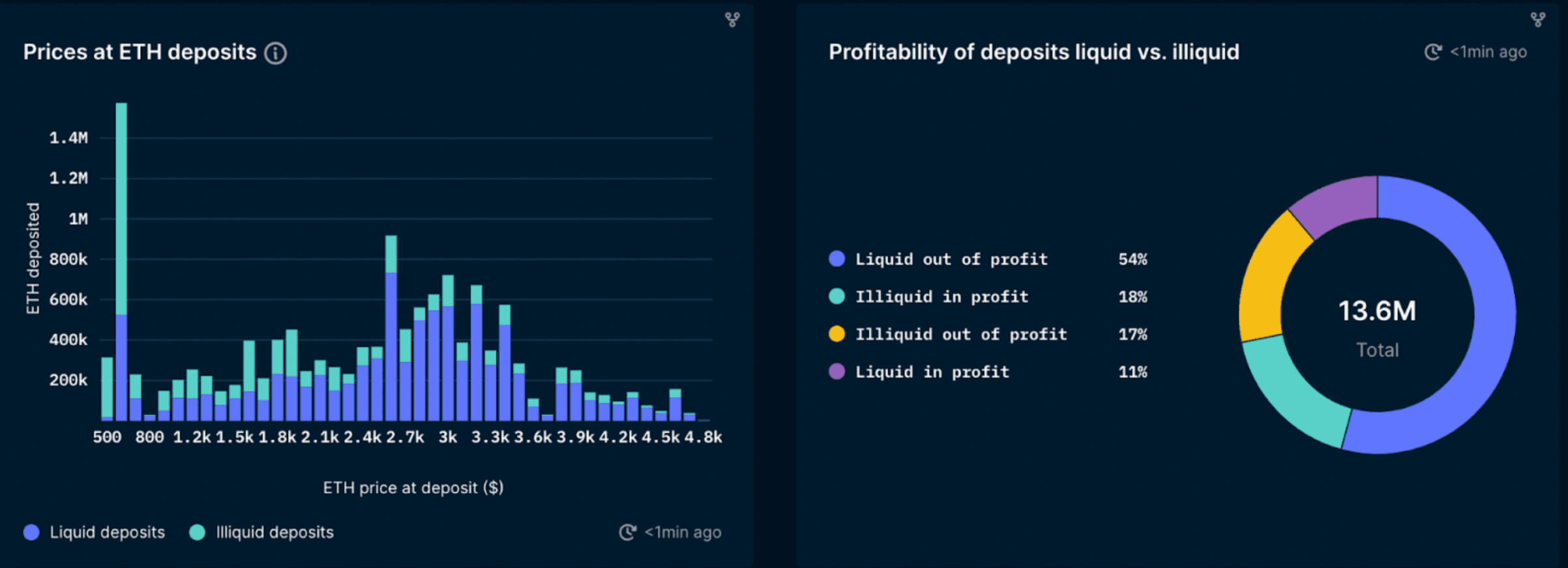

Based on these assumptions, insight into how much is staked at which price and whether it is illiquid or liquid can provide some insight and help us monitor who is most likely to sell - profitable illiquid stakers

image description

Source: Nansen Query

Let’s start with the obvious, the data shows a lot of ETH being staked around $600, with the earliest stakers in November and early December 2020 (the only times you can stake ETH at these prices). This group may be a group of early adopters and supporters of ETH2.0 (as it was called at the time) who staked as soon as the beacon chain went live.

Unsurprisingly, most of these early staked ETHs are illiquid, as the services of established liquid staking providers are now lesser-known, and it is likely that many early stakers would prefer to do so themselves. Also, at this point people might be hesitant to staking with large CEXs, since most CEXs didn't introduce liquid staking until much later, so staking means locking up your tokens for an indeterminate period of time in front of an impending bull market.

So when withdrawals are enabled after the Shanghai upgrade, ETH staked around $600 will profit (if the price stays above that level). Around 1 million locked ETH at this price level could flow into the market if withdrawn through the unlock queue. However, it should be noted that some of these early stakers were strong Ethereum believers and diamond hands, and may not necessarily wish to sell their stake (e.g. Vitalik and the like).

However, looking at the overall situation, most of the pledged ETH (about 71%) is not profitable at the current price.

Only 18% of staked ETH currently belongs to profitable illiquid stakers, and these holders are most likely to sell once they are able to unstake.

Given that number and validators dropping out of the queue, even a Shanghai upgrade is unlikely to lead to a massive sell-off by stakers. Note, however, that this analysis is at current price levels and must be adjusted accordingly closer to the actual date of the Shanghai upgrade.

How much Smart Money is involved in Merge?

Looking at Nansen’s tokenized addresses that are not tokenized as exchanges or smart contracts can give some idea of this.

image description

Source: Nansen Query

Looking at the ETH holdings of ETH coin millionaires and billionaires, one can see a clear trajectory: all the way up.

Overall, ETH millionaires and billionaire whales, who have been hoarding ether since the start of the year, seem unaffected by volatile markets.

Interestingly, Smart Money seems to be expanding their holdings again after the early/mid-June lows.

in conclusion

in conclusion

The current ratio of ETH pledged is relatively low. If the merger is implemented as expected, it will reduce the risk of staking ETH, which may encourage further staking of ETH. Redemption will not be possible until after the Shanghai upgrade in 2023, which means collateralized ETH will not increase until then, and depending on market conditions, there may be additional hype after the merger execution risk disappears.

Contrary to some thinking, the Shanghai upgrade may not lead to a sharp sell-off in ETH. First, most staked ETH is unprofitable. Second, about 65% of pledged ETH is already liquid (liquid pledge derivatives), which has little incentive to redeem and sell ETH. Third, profitable illiquid staked ETH (the group most likely to sell) accounted for only 18% of total staked ETH. Also, it won't be unlocked all at once, and there could be weeks of exit queues. Note that all these numbers, and corresponding assumptions, are subject to change as Shanghai upgrades change.

Decentralized liquidity staking providers such as Lido and Rocket Pool are likely to play a key role in ensuring that Ethereum can remain a decentralized, censorship-resistant, and open network. They are set up in part to avoid the result that most of the staked ETH is controlled by centralized exchange entities like CEXs (the top 3 CEXs own about 30% of the staked ETH). These entities must be sufficiently decentralized to remain censorship-resistant, thereby ensuring the integrity of the Ethereum network.

The liquidity staking market seems to be moving towards a "winner takes all" situation. However, if existing players are gradually decentralized and properly aligned with the Ethereum community, this outcome should not compromise Ethereum’s core value proposition.

Lido governance is relatively centralized at the time of writing. However, the community is aware of the risks this poses and is actively seeking a solution. Initiatives include dual governance (to better coordinate LDO and stETH holders), and physically decentralized validators to comply with regulations.

Original link