Tiger Global: The best blitz player in venture capital today

Article written by Mario Gabriele

Article translation: Block unicorn

Article written by Mario Gabriele

Article translation: Block unicorn

If you only have a few minutes to spare, here's what investors, operators, and founders can learn about Tiger Global.

We may be here sooner than we think. Tiger's current private market thesis is simple: We're still in the open stages of the digital revolution. To those who started preaching the "software opportunity" decades ago, it may come as a surprise that we haven't reached maturity yet. If Tiger is right, we should expect more unicorns to be minted, and the payoff will be bigger than expected.

There are different ways to win in venture capital. Just as a16z did a decade ago, Tiger is disrupting the venture capital market, demonstrating a new way to win. Its approach is based on rapid capital deployment, reducing founder friction and accepting lower returns.

There are benefits to outsourcing due diligence. How does Tiger invest across geographies at a rate of roughly one transaction per day? By delegating elements of deal sourcing and evaluation to a consultancy like Bain. By doing this, Tiger is able to move faster with wider coverage. This strategy also turns fixed costs into variable costs.

Founders may be tired of "hands-on" investors. Part of Tiger's claim is that it will be an unobtrusive capital partner. This approach runs counter to industry norms, as most companies are racing to show a willingness to roll up their sleeves and help. The fact that many founders find Tiger's laissez-faire attitude attractive is a testament to the lack of trust many have in the VC's value proposition.

A hedge fund manager can bring a fresh perspective to a startup. While perhaps less visionary than their VC counterparts, some founders find the detail and rigor of a hedge fund manager's thinking refreshing. That could make crossover funds like Tiger an increasingly attractive partner.

Venture capital is more of a speed game than ever. While previous private equity investors could build deep relationships and choose investments carefully, timelines have become tighter as competition has intensified. As a result, what once looked like a standard game of chess—with all its careful strategy and deliberation—has accelerated into blitzkrieg. This variation requires players to take action in 10 minutes or less, favoring quick decision-making and acting on instinct.Actually, it's a different game. Even Hikaru Nakamura, one of the greatest chess players of all time, said: "[Blitzkrieg] is just getting positions where you can move quickly. I mean, it's not chess."

Tiger Global is the best blitz player in venture capital today. The nearly $100 billion crossover fund is being deployed almost daily around the world at a pace that no other firm can compete with. To the casual observer, Tiger appears to be operating on a dark mix of hedge fund bravado, overvaluation and fast-twitch foreboding. Perhaps that's why it's easy to imagine Nakamura's off-the-cuff comments being adjusted to apply to the fund:

Of course, Tiger has invested in a lot of startups. But, I mean, it's not a venture capital firm.

It's a sentiment people often hear about tigers. The corollary of this complaint, as investor Everett Randle brilliantly outlines, is that the fund isn't playing the game it's supposed to, it's using too much of its amygdala and not enough of it. frontal lobe. As narratively tempting as it is, writing Tiger this way misses almost everything that makes it special. This isn't some mindless capitalism-infused "buy" button, but a 21-year-old fund with a unique culture, storied partnerships, strong returns and a history of adapting its mission to the macroeconomic environment.

It is no accident that Tiger can move faster and invest more than any other fund, but the result of a deliberate strategy. While Nakamura has his misgivings, even a blitzkrieg requires real brain power.

In today's article, we're going to go into a tiger's cage and ask how he got his stripes. In particular, we will outline:

History of the tiger. Without the famous "Wizards of Wall Street", there would be no fund today.

Coleman's leadership. Coleman, 25, saw an opportunity in the tech industry. To take advantage of it, he had to adjust the fund's mandate several times.

How Tigers Win. No other fund operates the same playbook as Tiger -- perhaps because no one else does.

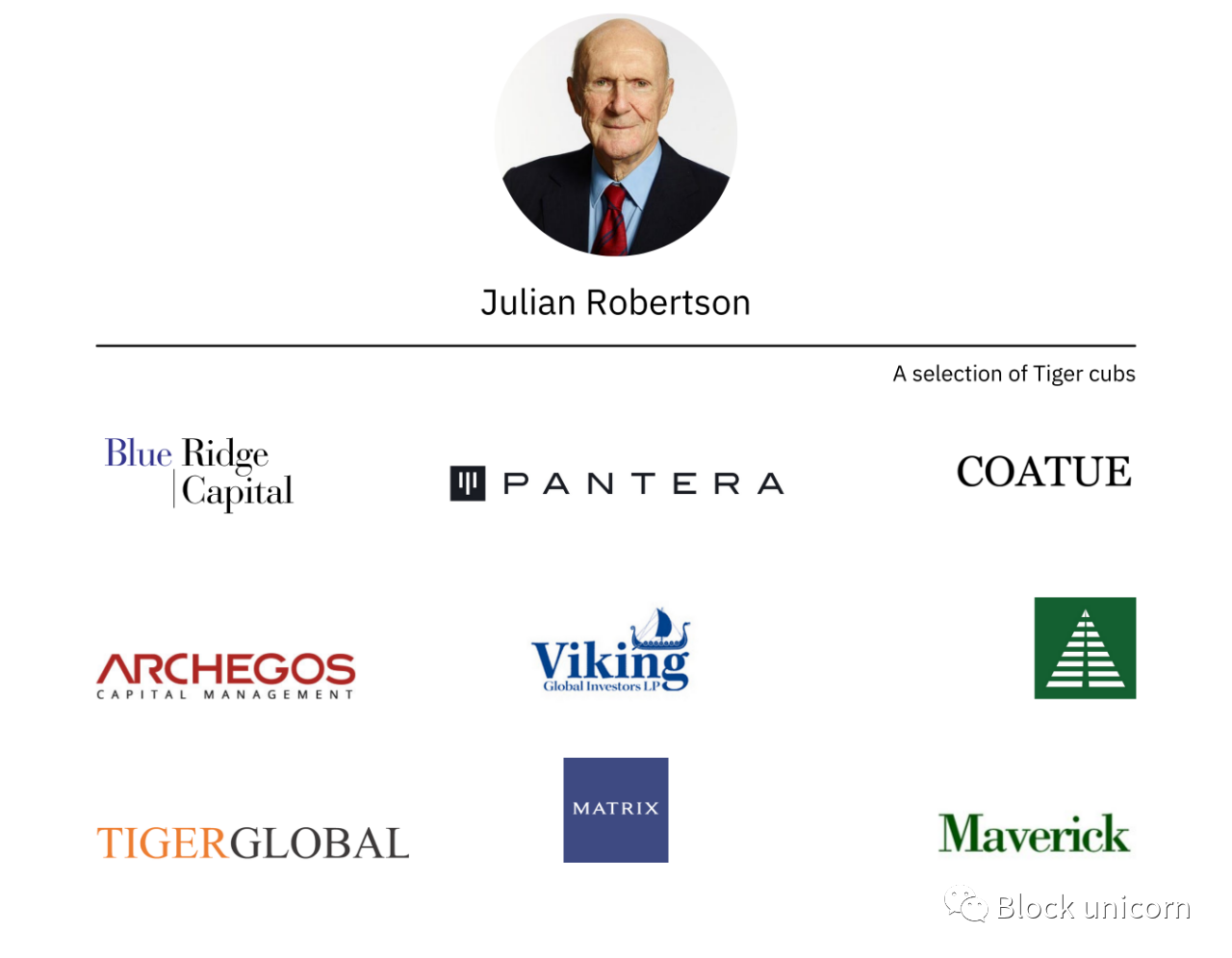

Robertson's preface

To understand Tiger Global, you must first understand its predecessor, Tiger Management. To understand Tiger Management, we must start with its founder, Julian Robertson.

text

At the very beginning...

Time for something new, Robertson thought. Over the past 20 years, the North Carolina native built a fine but unspectacular career on Wall Street as a stockbroker. He made handsome money at Kidder, Peabody & Co., but not enough to elevate him to the upper echelons of New York's financial world.

Still, he was promoted to head the firm's asset management division, an achievement that would surprise many of his fellow college professors. While Robertson has always had an eye for numbers, he's been an average, unenthusiastic student at Chapel Hill.

At 47, it's time for a break. Robertson left New York for New Zealand, relocating his wife and two young children in the process. He later recalled the choice as a somewhat odd one:

I went downstairs as soon as I got up... I shouldn't be so stupid. We can't afford it or anything.

During his antipodal sabbatical, Robertson wrote a novel. Its plot will be familiar to anyone who knew him: a young Southerner moves to Manhattan to make his fortune and secure his future.

Life requires free narrative liberties that even the bravest of authors cannot afford, which is to say that whatever glittering triumphs Robertson contemplates for his protagonists, they certainly pale in comparison to what happens.

Although the year in New Zealand taught Robertson to be "not by any stretch of the imagination a novelist", it gave him the time and space to plot his next act.

In 1980, he returned to New York City and opened the doors of Tiger Management. He started with a simple plan: run a long-short hedge fund driven by fundamentals. Robertson's style was later succinctly described as simply buying the best companies and shorting the worst.Over the next two decades, Robertson increased Tiger's assets under management to a high of $21 billion, an increase of 259,000%. Tiger has beaten the market in 14 of its 20 years, delivering an average annual return (net of fees) of 25% to its limited partners (LPs).

To understand how this continued brilliance came about, we must first outline Robertson's particular genius.

first level title

Robertson's Genius Investing Skills

While researching this article, I had the opportunity to speak with several investors and founders who have interacted with Tiger Management and its affiliated organizations. Among them was Erez Khalil. Kalir previously worked at Tiger Management under Robertson's direction, founded the "Tiger Cub" - Sabretooth Capital Management, and served as CIO and CEO of Stansberry Asset Management. During our chat, Kalir laid out some of the factors that make Robertson a great fund manager. include:

The Gift of Spotting Talent

meritocracy

excellent pattern recognition

Flexible Investment Authorization

Robertson found that the skills of the genius investor likely defined his legacy. As Khalil puts it, "Julian has a reputation for hiring young talent."

It seemed like a natural gift for Robertson, though his intuition was woven into a rigid recruiting structure as Tiger grew up. Beginning in the 1990s, Tiger required applicants to complete a 450-question test that took more than three hours to complete. It is designed to assess ability as well as desirable character traits, including competitiveness, intellectual openness, teamwork and integrity. A former employee recalled a question from the test:

Is it more important to get along with your team or challenge them? Would you rather be intellectually right and lose money, or be intellectually wrong and save the deal?

Influenced in the design of the test was Dr. Aaron Stern, a psychoanalyst who was Robertson's advisor. Stern also served as chief operating officer at some point in Tiger's life.

(The now-deceased, The Good Doctor appeared to be an interesting and complex character—the author of "I: The Narcissistic American" and former head of the Hollywood ratings agency, where he famously edited scripts and carefully cut Notorious for pornographic scenes.)

Although unorthodox, especially at the time, Stern's presence speaks to the importance Robertson places on talent assessment and his desire to go beyond resume requirements.Tiger's success in this regard is obvious. As we'll discuss later, Robertson later seeded many of his former employees to work as fund managers. The outstanding performance of so many people shows what a strong team the "Wizards of Wall Street" has assembled.Robertson's trick with

Create a truly elite environment

strong desire combined. When discussing this quality, Khalil pointed to the relationship of the famous University of North Carolina (UNC) college basketball coach Dean Smith with Michael Jordan.

He singled out the 1982 NCAA championship game. UNC trails by one in a tight battle with Patrick Ewing's Georgetown. With 32 seconds left in the game, Smith drafted a play that put the ball in Michael Jordan's hands. He was just a freshman at the time.

As Jordan recalled in ESPN's documentary "The Last Dance," Smith said, "If you can shoot the ball, shoot it." He got the shot and made it.

Robertson, who happens to be a UNC alumnus, adheres to similar principles. While the rest of Wall Street operates in an almost militaristic hierarchy, Robertson gives geniuses the chance to score, no matter their age or experience. From Kalil:

He doesn't care how old you are, he doesn't care if you paid your dues, he doesn't care how long you've been working for him...he throws the ball at you.

Those with hot hands are also handsomely rewarded. If you are capable of producing these goods, Robertson will pay you without hesitation. "If they put points on the board, he'd pay eight-figure money in the twenties," Khalil said.

None of this would matter if Robertson and those around him weren't shrewd analysts, good at pattern matching. Decades in business honed Tiger's founder's instincts to such an extent that he can assess the macroeconomic environment and the specifics of a particular business better than almost anyone else. In particular, Robertson appears to have near-knowledge on the financials of each investment and its impact on company performance.

A controversial article in BusinessWeek — where Robertson filed a $1 billion defamation suit before the publisher admitted a settlement without wrongdoing — sheds light on this ability:

This used to happen every day until 1993, when Robertson moved from the trading desk to his own office. On the screen are the prices of the stocks in Tiger's portfolio -- all 100 stocks. Just the price, and how each stock changes. A tiger might own a million shares, another one 2 million. But it's not on screen. There are only tickers, their prices, and changes during the day.

Robertson would call out a figure. He has mentally calculated the total change for the entire stock portfolio, accurate to zero. Inevitably, he was right.

One Tiger employee said of Robertson: "He can look at a long string of numbers in a financial statement that he's never seen before and say, 'That number is wrong.' And he's right." This acuity comes naturally, but can only flourish with experience.Although it originated in Robertson, rapid pattern recognition became the hallmark of the entire Tiger organization. A keen understanding of business fundamentals appears to have contributed to Tiger's flexibility as an investor. During the fund's epic run, Robertson has made big bets on stocks, commodities and currency exchanges. He adapted to the market environment and found new ways to win.”

Julian makes money in a variety of different ways.

Given this agnosticism, it may be surprising that the tiger's ultimate demise stems from recalcitrance. In 2000, Tiger closed its doors.

first level title

pass the torch

Three months into the new millennium, Tiger released a letter announcing its closure. Although not signed, the explanation is pure Robertson:As you've heard me say on numerous occasions, the key to Tiger's success over the years has been an unwavering commitment to buying the best stocks and shorting the worst. In a rational environment, this strategy works well. But in an irrational market where yield and price considerations take a backseat to mouse clicks and momentum, that logic doesn't matter as we've learned.

The current tech, internet and telecommunications boom, fueled by the desire for performance from investors, fund managers and even financial buyers, is unknowingly creating a Ponzi pyramid doomed to collapse. The tragedy, however, is that the only way to generate short-term performance in the current environment is to buy these stocks. This makes the process self-perpetuating until the pyramid eventually collapses from its own excess.

Tiger's performance suffered the first two years as he refused to adjust to hyperventilated valuations in the tech sector. In the end, it turned out that Robertson was right. Just three days after Tiger's farewell words, Microsoft was found guilty of monopolistic conduct, sending its stock price down 15 percent and truly heralding the start of the dot-com bubble. Within seven months, Pets.com was out of business and the technology sector was down 75%.

By then the tiger was too late, and even if it had happened a year earlier, it might not have mattered. A lot of money has flowed out of the fund, and Robertson, now 69, is much older. This is the right time for something new to emerge.

While Robertson has earned his legacy, arguably his most enduring legacy came after he stopped managing the Tigers. With his team effectively out of work, Robertson secured the seed money for the best talent to start his own fund.

Tiger seed lists are now a vital part of hedge fund knowledge. Many of the most influential companies of the past 20 years can be traced back to Tiger and Robertson. (Note that some refer to funds that receive funding as "tiger seeds" to distinguish them from funds run by corporate alumni who do not receive mentor funding.)

first level title

a new tiger

text

What's in the name?

If America had aristocrats, Chase Coleman III was undoubtedly one of them. Coleman, a descendant of New York Director-General Peter Stuyvesant, was born wealthy during his tenure as a Dutch colony. On the North Shore of Long Island, Coleman befriended Spencer Robertson, the son of the famous Tigers manager.

After captaining the lacrosse team at Williams College in 1997, Coleman joined Pat Robertson's company. Over the next four years -- Coleman managed Robertson's personal capital for a year after Tiger Management closed -- the economics and Spanish graduate impressed as a partner.

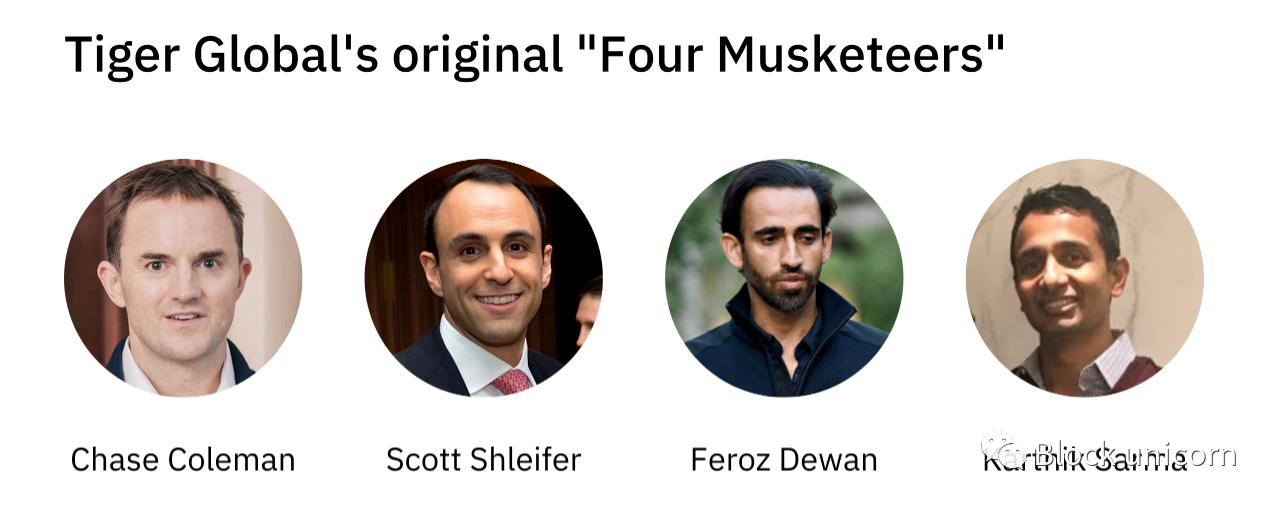

When it was time to move on, Robertson provided the money. Coleman, with $25 million under management, founded Tiger Tech. He was only 25 years old at the time.

Stylistically, Tiger Tech was both a continuation and a negation of Robertson's approach. The new tool is reminiscent of Tiger as a long-short hedge fund, focused on fundamentals. But while his mentors were known to reject tech stocks, Coleman embraced them. The entire purpose of the fund is to invest in emerging fields.While Coleman seeks returns in different areas, his philosophy is typical Robertson. According to Kalil, "In many ways, Chase was Julian's most successful standard-bearer."

Chief among these similarities is a keen sense of talent.

The first investors Coleman hired in the new fund were Scott Shleifer, Feroz Dewan and Karthik Sarma. All three have gone on to have very successful careers in the years since. Shleifer leads Tiger's private equity team, reportedly worth $5 billion. Dewan spent 15 years at Tiger, taking over day-to-day management for a while before launching his own fund, Arena Holdings. Sarma left after five years to start SRS Investment Management; just last week, the Financial Times reported that the fund had unrealized gains of as much as $5 billion thanks to a well-timed bet on Avis.

"There's no 'FK you, I'm Chase, I'm the one,'" Khalil points out. "He's signaling to these people, 'If you stick with me, we're all going to be billionaires.'"

That seems to be confirmed, though it will require flexibility, which would do Robertson proud. Coleman's fund appears to have undergone three separate mandate changes since its debut.

first level title

Shift 1: Going Global

When Tiger Tech was established, it was limited to listed technology companies in the United States. That didn't last long. Tasked with finding long-short opportunities in the telecommunications industry, Dewan quickly identified opportunities outside the US. In particular, he recognized the potential of Orascom Telecom (now known as Global Telecom Holding).

To accommodate the stakes, Tiger changed its approach. It won't be limited to the US, but will work globally. Eventually, when "Tiger Tech" becomes "Tiger Global," its name will reflect this broader vision.

Dewan is right. According to Kalir, Orascom's bet was a "grand slam home run," with a return of about 25 times. From its inception, Tiger recognized the potential of technology to create big winners globally and would build a strong reputation for supporting companies in China, India, Latin America and elsewhere.

first level title

Shift 2: The Potential of the Private Sector

Just as Dewan's research would change Tiger's geographic strategy, Shleifer's work opens a different front.

Like Robertson's fund, Coleman is a pattern-matching specialist. According to Kalir, Tiger Global has a knack for identifying businesses with a favorable set of characteristics. Once they've done that, grasping the shape of related entities, they look for companies with a similar complexion in different markets.

Dewan's work in telecommunications informed the companies Tiger was looking for in the tech space. But when Shleifer started digging into the space, he found that many of the most exciting businesses had yet to hit the public markets.

Tiger Global made a second adjustment. Coleman raised a new fund to go after the private market, with Shleifer at the helm.

Like Dewan, Wharton alumni are also attracted to businesses outside the United States. Not only are valuations more reasonable, but competition is significantly less. Those early bets included Yandex.

In 2000, Shleifer led a $5.3 million Series A round for the Russian search engine and made additional capital injections throughout the company's life. Yandex went public in 2011 at a valuation of more than $11 billion; today, it has a market capitalization of $30 billion.

Yandex was followed by acquisitions of Mail.Ru (acquired), Maktoob (acquired), Dangdang (valued at $1 billion in IPO), eLong (post-IPO merged with Tongcheng), Mercado Libre (listed, now $78 billion valuation) and Despegar (IPO, now valued at $850 million).

It's been an incredible run that deserves comparisons to any venture fund boom. Over the next decade, by 2010, Tiger would have managed to pick out a host of other winners, including Zynga (Series B), LinkedIn (via Secondary), Flipkart (Series B), Facebook (via Secondary) and Trendyol (via Secondary). B series).

The performance of this venture is enhanced by tidy picks in the public markets. Shleifer is credited with Tiger's investment in China's "Yahoo" -- the likes of NetEase and Sina saw big gains in 2002-2003.

In hindsight, Tiger was right to pay above market price. Of course, technology company valuations can only go up.

Khalil recalls one particular anecdote where Tiger outbid Yahoo by 2-3x to seal the deal. To many at the time, this might have seemed ridiculous. But in just a few years, Yahoo bought Tiger's shares at a premium of 20 times. Shleifer and the rest of the private-markets team may have struck deals that look rich but often turn out to be shrewd.

first level titleShift 3: Top 10% Indexed

We are going through Tiger's third mission shift.

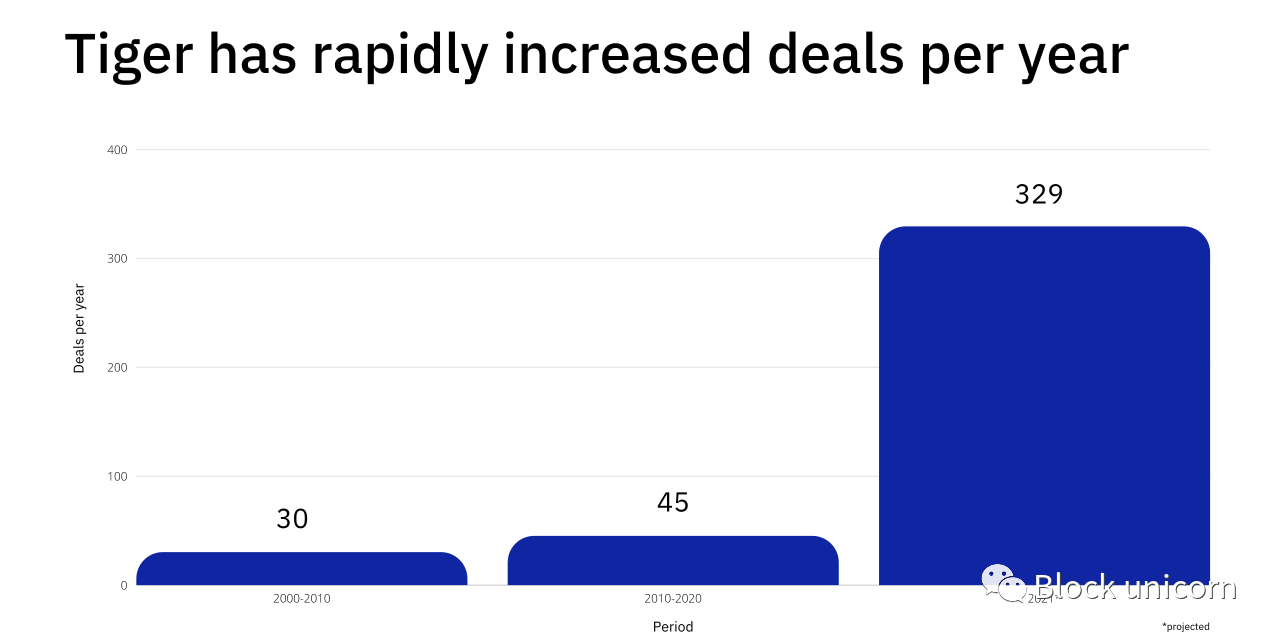

For most of its history in the early private markets, Tiger's actions have been relatively conservative. For example, between 2000 and 2010, the company participated in only 30 venture financings, an average of 3 per year. The data comes from Crunchbase and includes secondary purchases and multiple investments in the same entity.

Over the next decade, Tiger accelerated its deployment: The number of people involved in funding events skyrocketed to 449, or roughly 45 per year.

Over the next decade, Tiger accelerated its deployment: The number of people involved in funding events skyrocketed to 449, or roughly 45 per year.

While that represents a rather slow pace, Tiger's 2021 makes it look pretty lethargic. So far this year, the company has invested in 286 rounds. At the current pace, the company should easily clear 300 by the end of the year.

Crunchbase data

So, what has changed? How do we explain Tiger's 100x growth in the first decade and 6.6x growth in the next decade?

The fund's adjustments appear to be less anecdotal and more systematic. To some extent, this may also be related to personnel changes.

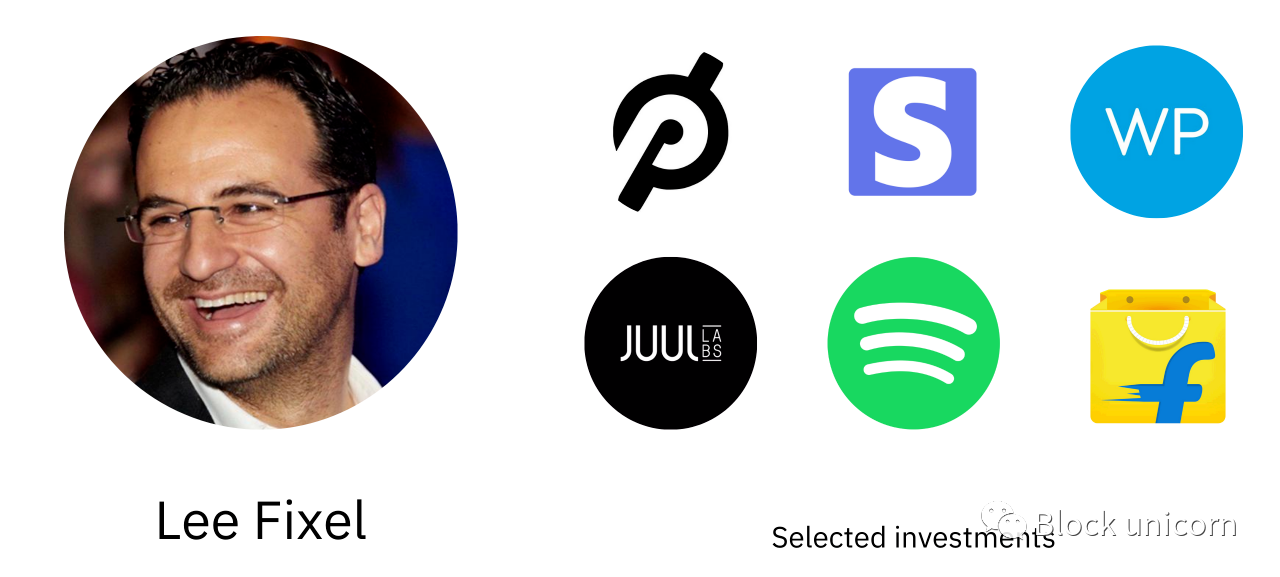

Lee Fixel joined Tiger in 2006 as a young economics graduate from Washington University in St. Louis. Over thirteen years, he has achieved near-legendary venture capitalist status, being named to the Midas Touch eight times.

As part of the Shleifer team, Fixel supports Peloton, Stripe, Spotify, Warby Parker, and Juul. He has also built a particularly stellar reputation in the Indian market, backing Flipkart, Ola, Myntra, Quikr, and more.

Flipkart's CEO spoke of Tiger Investor's impact on the ecosystem, describing him as "the pioneer who single-handedly pushed the Indian startup scene onto the global map".

While Fixel has moved quickly, he seems to prefer a more secretive, low-key approach to investing. A manager at a leading venture fund described Fixel's approach as "shady and surgical"; you won't hear his moves, just see his name on the hat table.

Fixel's departure in 2019 appears to coincide with a shift in approach. Rather than attacking stealthily and selectively, Tiger is starting to carve out a place in the market.

The manager mentioned above recalls hearing that Tiger was interested in a software company when Fixel left. He was taken aback; it was a solid business, but not an obvious breakout performance. When he asked another investor what Tiger thought of the company, his peers responded that Tiger told them they had a "software thesis" and believed that "the value of the software asset class [was] mispriced."

This sentence is very prosaic, but very instructive. While the venture capital ecosystem had long seen the potential in software and pitched the industry's potential to outside parties, Tiger effectively said to these investors: Your idea is still too small. We're earlier than you realize, and the winner will be orders of magnitude larger than we currently think.

This seems to be the most fundamental reason behind Tiger's latest update. Despite being bullish on the tech sector, Coleman and Shleifer appear to have adjusted upwards in line with their forecasts. It's only natural, especially given the size of Tiger's assets under management (AUM), that such a revision would lead to higher prices and greater activity.

As we mentioned before, Tiger has grown from 30 to 300 deals per year. Inevitably, when this transition occurs, relative quality standards must drop. The VC managers I spoke to said that Tiger seems to have gone from investing in the top 2% of tech companies to the top 10%.

While this explains what Tiger is doing, it doesn't tell us how the fund is doing it. Even with tens of billions under management, how is it possible for a team of 200 to invest in a company almost every day?

Time to dig into Tiger's playbook.

first level title

script

When broken down into its component parts, venture capital is an easy game. The Fund has four main responsibilities:

1. Purchasing Transactions. If you can't see any transactions, you can't invest. To start deploying capital effectively, you need to find ways to attract opportunity. These may come directly from entrepreneurs or other investors.

2. Assess the business. Every investor—even Tiger—sees more deals than they could possibly invest in. To make an informed choice, you need to do your due diligence and assess the potential of your business.

3. Win the deal. The best startups are often able to choose from multiple capital partners. If you want to invest, you need to prove your worth and outbid or outbid your competitors.

4. Support the company. Once you're done investing, you can start working to help your portfolio. Your goal is to improve your company's chances of success and build a solid reputation.

(You could argue that there is a fifth — exit investing. While some VCs may be active in this, either as matchmakers or SPACs, many are not. This topic also fits very well with the concept of “backing.” ")

The conventional wisdom is that to be a great VC, you need to be great at all of them, and to be good at one or more.

For example, Benchmark has earned a reputation for doing well on step 2. Although they undoubtedly excelled at each task, they were known as superior evaluators, better than almost anyone else at determining the winner.

Compare it to Andreessen Horowitz (A16z). Also, while talented in this stack, a16z's rise has come from domination of the company (responsibility #4 above). Fund founders Marc Andreessen and Ben Horowitz were happy to accept lower salaries to build a Portfolio Services team that could help with marketing, product, finance, and just about everything else Founders provide support.

Of course, every task is tied to the others, but it helps to stand out at certain things to be considered special.

While other funds may be better sources, evaluators or supporters, no one wants to work as hard as Shleifer and his team when it comes to getting the ball over the free throw line.

Tiger's unique skill set here doesn't just come down to a good sprint, though that might work. It's a product of funds doing things differently at each step of the VC process. The ability to win starts with a clear mission.

first level title

Mission: lower the bar

While not part of the four key functions outlined, we should start with Tiger's mission. The fund's strategy works because it seeks a fundamentally different return profile than traditional venture funds.

As we mentioned above, Tiger's current practice is to invest in the top tenth of tech startups. If the tech sector continues to grow and the fund picks reasonably well, Tiger's returns should be strong -- but it's unlikely to drive the extreme outlier performance that traditional venture funds look for.

Traditional VCs typically look for a 30% internal rate of return (IRR) on their investment; a Tiger might want closer to 20%. The prospectus for Tiger XV, which is about to launch a private equity fund worth $10 billion, shows that the fund has performed above that threshold. The internal rate of return for the 14 private entities was 34%, or 27% net of fees.

In his book "Playing Different Games," Everett Randall articulates the difference in approach:

General Fund: I'm going to deploy this fund I raised over the next 3 years or so because that's what a fund is supposed to do and that's what I tell my LPs we're going to do. During these 3 years, I will try to do the best deal I can and maximize the MoM (multiple of money) / IRR.

Tiger: I will deploy as much capital as possible at the 18% IRR threshold rate.

Essentially, traditional venture capitalists want the best returns within a certain time frame. Meanwhile, Tiger is looking to invest as much money as possible with a reasonable IRR.

Why would any limited partner (LP) want to invest in Tiger if other VC firms offer the opportunity to earn higher IRR?

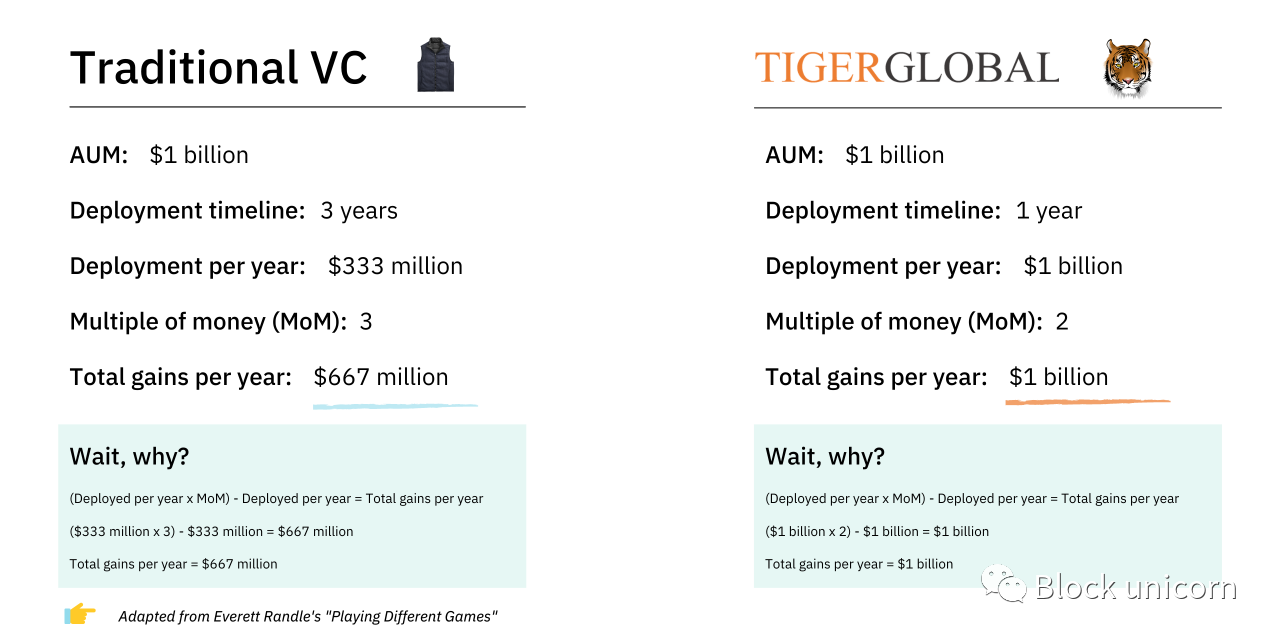

Again, Randall's work is excellent here. He outlined a scenario in which traditional VCs and Tiger each receive $1 billion in funding. Traditional VC deployment over three years and generating a 3x return or multiple on money (MoM). Tiger deployed for over a year and generated 2x the MoM.

The Valley of Dunning-Kreuger

Here's what it means in terms of net gain, adapted from Randle:

image description

While traditional VCs may get bigger month-over-month, Tiger spits out more cash each year. This is especially beneficial for large LPs - think large endowments and sovereign wealth, as they can continue to reinvest, putting more and more of their capital to work.

For example, let's say you're the head of the Duke Foundation. For higher returns, you'd need to invest $1 billion in a traditional venture fund. Since it's been deployed for over three years, you're effectively putting $333 million a year into venture capital.

Now, if you put $1 billion into Tiger, it gets deployed in 12 months. Since Tiger wants to keep investing, that means you have an opportunity to deploy another $1 billion next year and the year after, and so on.

Ten years from now, you might only be able to allocate $3.3 billion to the risky asset class with traditional funds, versus $10 billion with Tiger.

The real numbers are crazier than that. The aforementioned prospectus states that Tiger plans to deploy the entire $10 billion of the XV Fund within 12-18 months.

Now, reasonably, you might say, well, why not put more money into traditional venture funds?

Usually, the answer is that it is impossible to do so. While venture funds have grown, the way they handle procurement, due diligence and support (discussed later) means there is a cap on the amount of money they can put to work.

While emerging managers may have difficulty building a limited partner base, established firms have had to turn down many institutions or drastically reduce the amount of capital they can accept.

In a discussion about Tiger, an investor described how his firm was often approached by potential LPs, especially sovereign wealth funds. Because of their size, these parties hope to put hundreds of millions of people to work. While appealing in the abstract, the manager pointed out that this was impossible - the fund could not efficiently commit so much additional capital to operate, and doing so would distort the composition of its LP base.

These are exactly the types of customers Tiger can serve. Want to drop $200 million into tech jobs? no problem.

Tiger has a total of $83 billion in AUM, not including the $10 billion raised through August 2021. It is likely to be closer to $100 billion. You might not get Sequoia-level returns, but there are bigger benefits than putting your cash into bonds or Treasuries.

While it's almost always impossible to find a complete list of a fund's limited partners, we get a sense of Tiger's basics. It's exactly the kind of list you'd expect, with charitable entities, university endowments, and retirement funds.

This LP base is very stable. According to the prospectus, 85% of external funding comes from investors who have worked with Tiger for more than 5 years. In Tiger's last fund, 89% came from existing limited partners.

This solidity is further reinforced by the fact that Tiger's largest LP is its own employees. Not only does this mean Tiger has real skin in the game, but a significant portion of its money comes from people who bought into the fund's strategy a priori.

first level title

Sourcing: Buying Leads

Like other high-profile funds, Tiger has benefited from huge demand. One founder I interviewed outlined how he targeted tigers in a seed round, learning about their deep pockets and hands-off approach—an attractive combination for seasoned founders.

In addition to reputation-driven inbound, Tiger took two concrete steps to strengthen its sourcing:

Seed other funds.

Hire a consultant.

To secure more deals, Tiger tapped its seed funding. Shleifer's team typically looks to invest about $25 million in emerging early-stage funds, explained an investor familiar with the practice. The goal here is to be the largest LP with the new manager and to give Tiger visibility into future funding rounds for the portfolio companies.

Sources I spoke to noted that Tiger was essentially asking these managers, "How can we be your only partner in bringing series As?"

Besides the money, Tiger has plenty of perks to lure managers, offering private jet travel and lavish tickets to the hottest sporting events.

It's unclear how many times the strategy has been executed, but given Tiger's size, the fund certainly has the clout and money to roll out the strategy at a reasonable scale.

Tiger's friendliness extends to Series A funds. One investor following that stage said that while Tiger did not make an investment proposal, a partner expressed hope to boost their entire portfolio in future rounds.

As you might expect, Tiger seems less interested in cultivating relationships with his growth-stage colleagues. After all, these are competitors looking to maximize distribution in hot rounds. A manager at a prominent fund said of John Curtius, one of Shriver's most prominent lieutenants, "John made no effort to build a relationship with me ... Neither did anyone at Tiger."

In addition to seed funding, Tiger identifies opportunities through research and outreach. While other funds do this internally, relying on analysts and colleagues, Tiger takes a different approach.

As we'll discuss later, much of the Tiger model relies on the work of consultants. Tiger is Bain's largest client, though the fund also relies on the work of Ernst & Young and possibly others.

The task of these consulting shops is to research specific markets and find prospects. Tiger's history of pattern-matching excellence plays a crucial role here—once Shleifer's team has developed a belief in a field and approach, they invest in multiple players across geographies.

For example, looking at Tiger's bets, it's clear that grocery delivery is one of the priorities. The fund supports businesses across the stack, including Getir, Jokr, Nuro, Favo, Grofers, Wolt, and Telio.

Another obvious area of interest is the "democratization of investing" in traditional stocks and cryptocurrencies. Tiger's has invested in Groww, FTX, Public, CoinSwitch, Coinbase, Falcon X, and Robinhood.

It's easy to pull other themes from the portfolio - digital business banking, restaurant tech and SMB operations all stand out. If these areas of focus sound a little bland and general, well, that's the point. While companies like Union Square Ventures (USV) have always been surgical in defining and executing a well-thought-out detailed thesis, Tiger is happy to say "tech = good" and work with it. The fact that it works vindicates Tiger's understanding of the macro environment, and perhaps suggests that in times like these, risk taking can simply be taken.

first level title

Evaluation: "Cloud" Diligence

Tiger's use of consultants came to a head when evaluating companies. Let's briefly review Tiger's approach:

It bets on private technology as an asset class.

It will deploy as much as $10 billion per year into this market.

It will participate at any stage, from seed to pre-IPO (and beyond).

How do other funds do this? In a highly complex, rapidly changing industry, how do you realistically evaluate companies across dozens of complex, ever-changing geographies?

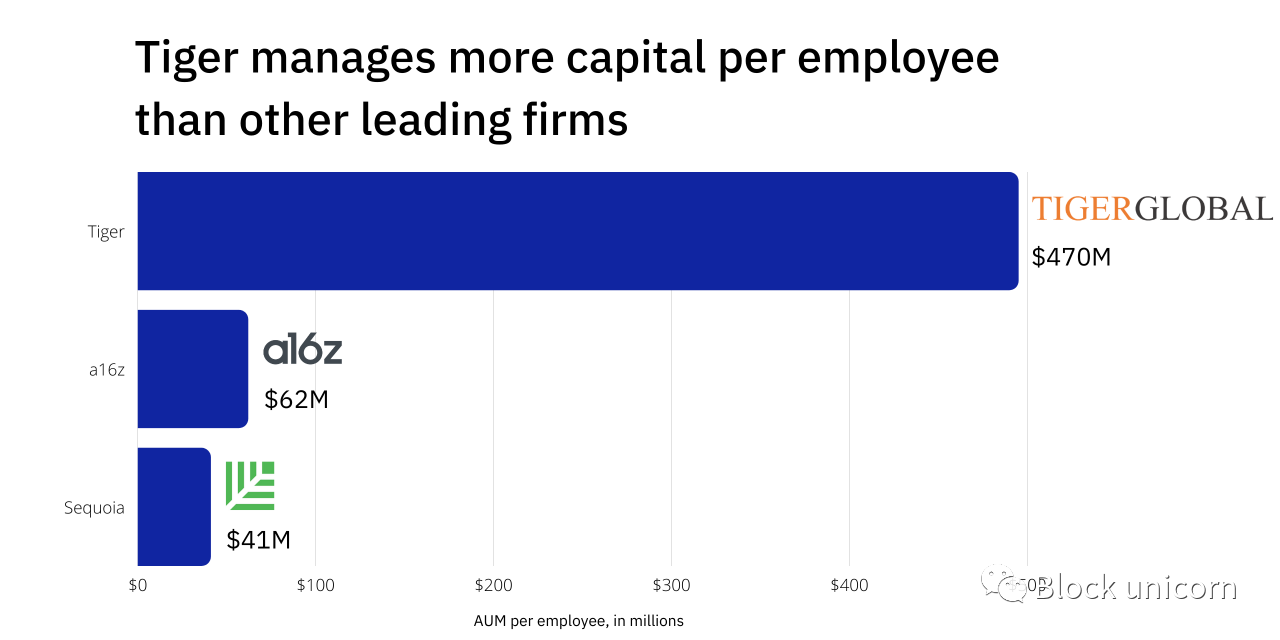

How do you staff this strategy? How many people do you need to run it? If you just look at the number of Tigers, you'd assume the answer is about 200 people. LinkedIn tells us that the fund has 188 people and effectively manages $93 billion. This equates to nearly $500 million in assets per employee. No other leading venture fund can come close to this efficiency:

image description

LinkedIn data, fundraising messages

As one investor described it, "[Tiger] is the most leveraged business model ever." So what's the secret? Is every Tiger investor more magical and faster than their counterparts at Sequoia or A16z? No, of course not.

The difference is that traditional funds conduct their due diligence in-house, while Tiger outsources it. The fund reportedly spends hundreds of millions of dollars a year on Bain's services, much of it for company valuations. Given Tiger's annual management fee income of between $1.5 billion and $2 billion, the fund can certainly afford it.

There are other benefits to this approach. Specifically, Tiger can add new coverage as needed, unlike startups that spin up new servers through AWS. Let's say Shleifer suddenly decides he wants to fund a startup in Pakistan's food delivery market. He doesn't need to set up a dedicated local office or hire an expert in the industry—he can call someone at Bain. With offices around the world and diverse talent, the consultancy can staff teams overnight.The same goes for working on aggressive trades. If Tiger were looking for a merchant-banking startup in Egypt, it wouldn't need to put investors through rigorous investigations and back-channels; it could have Bain do it dozens of times and report the results.

Tiger effectively turns a fixed cost (employee salaries) into a variable cost (consulting as needed).

Venture investors have seen this approach in action. One manager recalled how a Tiger investor showed up to a portfolio company with hundreds of pages of client calls apparently crafted by a consulting firm. Amazingly, Tiger paid for all of this research before the company raised money. This pre-emptive approach is part of what makes Tiger such a winning machine for venture capital.

first level title

Winning: Act Faster, Pay More

Tiger's genius zone is the space between spotting an opportunity and agreeing to a term sheet. This is a fund that thrives on competition and will do whatever it takes to win.

The main lever Shleifer pulls is price. Tiger is willing to pay more than anyone to seal a deal.

There are many? It depends on who you ask. Some of my sources estimate Tiger's premium to be around 25-50%, while others say the fund is willing to pay competitors with multiples.

One investor described a situation in which Tiger approached several other Tier 1 funds for a company that offered a valuation 25% above the table offer. When the company CEO said they had to think about it, Tiger countered, asking how much it would cost to close the process. When the CEO said another $100 million, Tiger agreed immediately. The deal is theirs.

One source summed up Tiger's valuation methodology, "Honestly, in many cases, I think [they pay] what they need to do the job."

Does this mean Tiger overpaid for his trade? Possibly, while this is also doable, venture capitalists have simply undervalued private tech companies over the past few decades. In either case, it probably doesn't matter; Tiger's differential return profile means it can afford to pay for the winners.

Relatedly, entrepreneurs know that Tiger will continue to deploy more people to their companies over time. One entrepreneur noted that it was almost a "responsibility" to ask for more money from the fund. He was sold to work with them in part because he saw Tiger stick with the business round after round, often under difficult circumstances. "I watched [ed] the consistency of their participation, round after round, in ups and downs," he said.

The tiger has other arrows in the quiver outside the deep pocket. Arguably the biggest is its willingness to make decisions within the time that most companies schedule an introductory call. Entrepreneurs I spoke with explained that Tiger's process closed in a matter of days, while other VCs took weeks to make a decision.

A founder who later received funding from Tiger commented on the speed, saying that once you start the process with the fund, you know it's only a matter of days and you'll receive a definitive decision . "It was such a fucking pleasure," he added.

It's a godsend for entrepreneurs focused on moving fast. Rather than allocating months to fundraising, they could simply work with Tiger and shorten the process, allowing them to return to business building.

Again, Tiger is only able to do this because of its model. It can make more frequent investments with lower return thresholds, and is often subject to outsourced investigations before the process officially begins. The entrepreneur said that in his first call with Tiger's team, they were "very clear about what they wanted."

Sometimes, that speed can be a mirage. While Tiger is usually happy to wire funds for small checks within a few days, larger investments can take a longer process. Tiger gets around this by committing to deals quickly and then investing based on further effort. Studies of this lag are typically conducted by EY. On at least one occasion, Tiger reportedly backed out of a deal after a verbal commitment.

Shleifer needs to be careful here; nothing damages a VC's reputation like breaking a deal. The tiger's final weapon of victory is a cultural weapon: aggression. Because of its origins, Tiger feels more like a hedge fund than a venture capital firm -- it's a place that expects and values extreme hustle, quantitative flexibility, and fierce competition.

While still pugnacious, venture capital has the etiquette of a gentleman's boxing match; the world of hedge funds is a naked brawl.

For some founders, this ethos is attractive. Given the intensity of running a startup, many entrepreneurs seem to find Tiger's ruthlessness similar. VCs typically come to work at 10 a.m. for a couple of coffee meetings before bouncing around in the early afternoon, and tigers are seen as places that require grit and stamina. This is fueled by teams willing to bid whatever it takes to get a deal done or jump on a flight to turn around a failed career.

Part of the reason the Tigers won was their willingness to go the extra mile.

Support: by network

Over the past decade, the venture capital market has been reacting to a16z's game, defined by its commitment to portfolio support.

To catch up, other funds have expanded their teams and the services they offer. The idea here is that by being the most "founder-friendly", "hands-on" and "value-add" company, they should be able to win the most competitive deals.

The fact that these phrases require citation at all illustrates the skepticism most of these claims arouse. While some VCs can meaningfully change a company's trajectory through their participation, many VCs offer nothing more than a Rolodex and the occasional meaningless phone call. Because of this perception of overpromising and underdelivering, many entrepreneurs are skeptical of these promises.

Tiger capitalized on this zeitgeist, swinging in the opposite direction. Instead of trying to prove its sincerity as a SuperNiceCapitalistHelper, it explicitly advertises a lack of engagement. Tiger Woods' partner also doesn't want to be the first number on your speed dial or the person you cycle through to your team's two-day outing. They don't want to be on your board, although they occasionally do. They're money—smart money, yes, but money nonetheless.

This approach can have a negative impact on a company if not executed properly. One investor who served on the board with Tiger Partners noted that during the meeting, the investor "didn't really pay attention. I don't know why he was there ... he was just looking at his phone and messing around. "

While this type of behavior can be repulsive to founders, this lack of engagement can be attractive if managed thoughtfully. One seasoned founder explains Tiger's unobtrusive allure, "I know what I need to do, and I don't need a babysitter."

Now, that's not to say that Tiger doesn't add any value after investing, it's just that, again, it's dependent on others for support. Perks come in the form of spending points and access to elite networks.

Once you become part of the Tiger portfolio, you receive free Bain consulting services. One founder jokingly calls them “tiger coupons,” and you can use them at your own discretion.

Another highlighted how valuable it was to him, especially when it came to major decisions, like choosing the company's next market. "It's a $10 million decision ... the fact that you have access to this resource [Bain] ... is crazy."

Although less discussed, elite recruiting firm Heidrick & Struggles has a similar arrangement. When it comes time to search for their next executive, portfolio companies have the option to search companies for free.

The final bonus is Tiger's network. While most established funds offer significant access, Tiger's is very different from most venture capital firms. Specifically, Shleifer's team can connect entrepreneurs with public market investors who have deep expertise in related industries.

This can be very valuable. One founder I spoke with noted that he learned a lot from talking to hedge fund managers who covered his industry. Not only did he gain a better understanding of his market, but he also gained insight into what late-stage investors might be looking for:

Surrounded by very financially savvy investors...you can get a good sense of how the public market views your company.

I can't speak highly enough of these guys. I'd love to work with hedge fund investors for the rest of the day...you get sharper.

Tigers are not afraid to do things differently. In every core function of venture capital, the fund makes unusual choices, all to improve its odds of winning.

first level title

move and counter move

One of the most interesting parts of Tiger's strategy is that it is extremely difficult for traditional venture funds to emulate. Tiger effectively sacrifices precision by increasing game speed. It accepts higher error rates to deploy more funds faster.

Copy Tiger breaks with traditional venture funds. If they choose to move faster, they increase the error rate; if they try to outbid the competition, they reduce the return. Tiger aims to absorb these influences - the mission dictates this approach, and the size of AUM makes it feasible. But traditional venture funds have a different, finely balanced risk and return profile, not to mention a culture that tends to be unwieldy.

Still, good competitors can always find ways to adapt new strategies. Tiger isn't the endgame for the venture capital market, though it does feel like the logical conclusion to the blitz strategy.

Others argue that Tiger has sparked a divide in the venture capital market between established conservatives and fast-moving insurgents. In his article, Randall suggests that we are heading towards a world where "luxury retailers" like Sequoia and Benchmark compete with "low-cost providers" like Tiger.

A veteran VC I spoke to made a similar inference, arguing that some founders prefer traditional, hands-on companies, while others gravitate towards Tiger's lighthearted and laissez-faire ethos:

Ultimately, if the founders were to decide between the two of us [Tiger and the personal company], one of us might be in the wrong room.While brand and reputation always carry weight, it seems like a misjudgment to classify the Tiger as something entirely different and implicitly lower-end. None of the founders I spoke to seemed to feel that Tiger had a negative brand name; instead, they seemed proud of their affiliation with the company. Again, all were exceptionally enthusiastic, more enthusiastic than many of the founders I interviewed about raising money from traditional funds. While Tiger explicitly didn't intervene, the firm appears to be adding meaningful, tangible value to its portfolio founders, while also offering them favorable valuations and exempting them from the arduous fundraising process.

Do founders wait for Tier 1 traditionalists when Tiger offers better and faster terms?

Sometimes, but probably not as often as one might think. To ensure they win competitive deals, traditional companies will have to speed up their decision-making process, but somehow not fundamentally increase their error rate. They also need to make their unique advantages much more tangible. Casual browsing of VC sites is drowning in a sea of platitudes about believing, helping, thought partner, caring, loving, understanding, supporting, awe, being inspired, serving, seeing the future, moving the world forward, and whatever Other well-meaning platitudes. Only a few have really shed light on how those promises were delivered and the difference they made. Broadly speaking, VCs need to do a better job of demonstrating their true expertise and turning that into impact for founders during the fundraising process.

Choices may also not be binary. We may increasingly see founders picking both Tiger and a legacy company. In many ways, this is the best of both worlds. Since Tiger's structural advantages almost always allow it to move faster, founders can use the fund as leverage to force traditional companies to step up and pay the price. The company has unlocked access to a vast network of “tiger tickets” and funds, while also gaining attention from traditional investors who have articulated and demonstrated the tangible value they can bring.

Of course, if the market shifts to the Tiger+1 default, competition for companion slots will intensify, forcing traditional funds to manipulate each other more directly.

While Tiger has the tools to dominate the current market, there is always a risk of failure. While the company's reputation seems solid for now, that could change. Tiger needs to be careful about avoiding verbal agreements or publicly investing in competitors. It must also ensure that its aggressive capitalization strategy does not lead to the high-profile outbursts of the likes of SoftBank that WeWork has endured. Any of these could tarnish Tiger's understated charm. Likewise, if Tiger's hands-off approach encourages poor outcomes and startups don't get enough advice and governance, founders may resent it. Some venture capitalists have sounded the alarm on this front, arguing that too many companies operate without oversight and strategic planning.

Of course, for many, this is a motivating position; believing anything else leads to cognitive dissonance. That doesn't mean the debate is without merit. Of course, there will be some startups that suffer from lack of governance just as others suffer from poor governance. Tiger needs to make sure it doesn't become a poster child for the first kind of failure.

The biggest risk to Tiger is macroeconomic. Now, the fund is happy to pay a premium, knowing that public market investors are interested in tech. If the industry sees a sharp decline, Tiger could see its portfolio shrink significantly. Because of its broader strategy, it likely has more losing bets than traditional selective companies.

Likewise, a tech winter could reduce the number of startups, making it harder for funds to effectively allocate the huge sums under management.

Of course, Tiger would be well aware of these risks. If the past is any indication, they'll be ready to adapt to changes in their environment.

Bobby Fischer once said, "Blitz kills your ideas." For Fischer, the speed of the game hinders one's ability to generate complex, novel strategies.

It’s tempting to think along the same lines about today’s venture capital market and the role of tigers in it. Now it's a spray and pray business and the line of thinking is that Tiger has the biggest hose.