数据复盘USDC危机:是什么导致了脱锚?有哪些连带影响?

原文作者:Kaiko

原文编译:Peng SUN,Foresight News

3 月 11 日,在硅谷银行倒闭后的几个小时内,稳定币 USDC 发行方 Circle 宣称 33 亿美元的储备存放在硅谷银行,引发市场恐慌,中心化与去中心化市场均陷入大规模混乱。13 日上午,Circle 首席执行官 Jeremy Allaire 宣布 USDC 储备 100% 安全,美联储等机构也表示储户可以提取硅谷银行内所有现金,市场恐慌情绪渐渐消逝。

像是又一次坐了过山车,加密市场在一夜之间陷入极端恐慌,一夜之间又恢复如常。那么,USDC 到底发生了什么?究竟是什么导致了 USDC 脱锚,产生了哪些连带影响,危机期间加密市场流动性情况如何,市场又是如何复苏的?这篇文章对此次 USDC 危机做了一次复盘,用数据告诉你当时到底发生了什么。

一、引发大规模市场混乱的 USDC 脱锚

(一)CEX 的巨大影响

USDC 主要用于 DeFi 生态系统中,因此在 CEX 上的流动性相对较低。截至上周,USDC 占 CEX 总交易量不到 0.5% 。然而,CEX 在引爆上周末的市场混乱中影响巨大。

这是因为在未知情况下,交易员只会想一件事:在哪里清算自己持有的 USDC。

今天,CEX 上只有 8 个 USDC-USD 活跃交易对,它们有效成为 USDC 兑换成美元的实时汇率。上周末,在 Circle 和 Coinbase 暂停 USDC 与美元转换的情况下,这些交易对是唯一的出金渠道。

但问题是,这些 USD 交易对的流动性相对较差:在 3 月第一周,日均交易量仅为 2000-4000 万美元。上周六,这些货币对的交易量达到历史新高的 6 亿美元,其中以 Kraken 为主,它提供了流动性最好的 USDC-USD 交易对。

果不其然,订单簿无法支持大量的卖单,导致 USDC 汇率暴跌。在 USDC 脱锚前,USDC-USD 订单簿上只有 2000 万不到的出价,而这无法支持数以亿计的卖单量。

虽然 USDC-USD 交易对出现前所未有的交易量,但大多数加密市场活动实际上并未通过美元进行的。大多数交易者使用离岸交易所,这些交易所不为 USDC 提供直接的美元转换,但是提供 USDC-USDT 交易对。这里的问题是,世界上最大的交易所 Binance 早在去年 9 月就下架了所有的 USDC 交易对。

到周六中午,Binance 终于重新上架 USDC-USDT 交易对,但那时 USDC 已经在流动性较差的 CEX 上以大幅折价交易。此后不久,USDC-USDT 交易对的交易量达到 99 亿美元,创下历史新高,因为交易者以脱锚价轮流卖出或买入 USDC。

总的来说,卖盘多于买盘,导致 Tether 对美元和 USDC 的交易溢价很高。

随着 Binance 重新上架大量 USDC 交易对,衍生品交易所也试图利用这种波动性。直到本周末,交易者只能在交易活动较低的 Bybit 上交易。上周末,未平仓合约飙升至 2.56 亿美元的历史高位。资金利率仍然处于波动状态,在 -0.13% 到 1.08% 之间震荡,因为交易者同时做空做多,但截至 13 日上午已经恢复到了正常水平。

其他几个衍生品交易所在周末相继推出 USDC 永续合约,其杠杆率从 Bitmex 的 10 倍、OKX 的 20 倍到 Binance 的 30 倍不等。

那么,如果这些交易所并不经常使用 USDC,为什么 CEX 上的交易活动在更广泛的市场动荡中产生如此巨大的影响?最直接的原因在于稳定币的 DeFi 喂价不能提供真实的美元汇率,因为你无法在 DEX 上交易法币。这就是为什么许多协议使用去中心化价格预言机来决定清算水平,而数据通常直接来自于 CEX。

原因还在于 CoinGecko、Coinmarketcap 等网站是计算其喂价的方式,它们在很大程度上依赖中心化市场。值得注意的是,尽管 Curve 是流动性最好的市场之一,但并未在 CoinGecko 或 CMC 的 USDC 市场页面上列出。

总的来说,流动性差的中心化现货市场、多个 USDC 衍生品合约的出现以及迅速传播的币价与汇率网站截图加剧了脱锚事件。就像银行挤兑一样,叙事成为现实,湮没 DeFi 生态系统。

(二)DeFi 承受了 USDC 脱锚的主要冲击

DeFi 实际上是建立在 USDC 上的。该稳定币为借贷协议提供了至关重要的稳定性,占去中心化稳定币(如 DAI)储备的很大一部分。许多 DeFi 协议都是在 USDC 永远不会脱锚的假设下构建的。

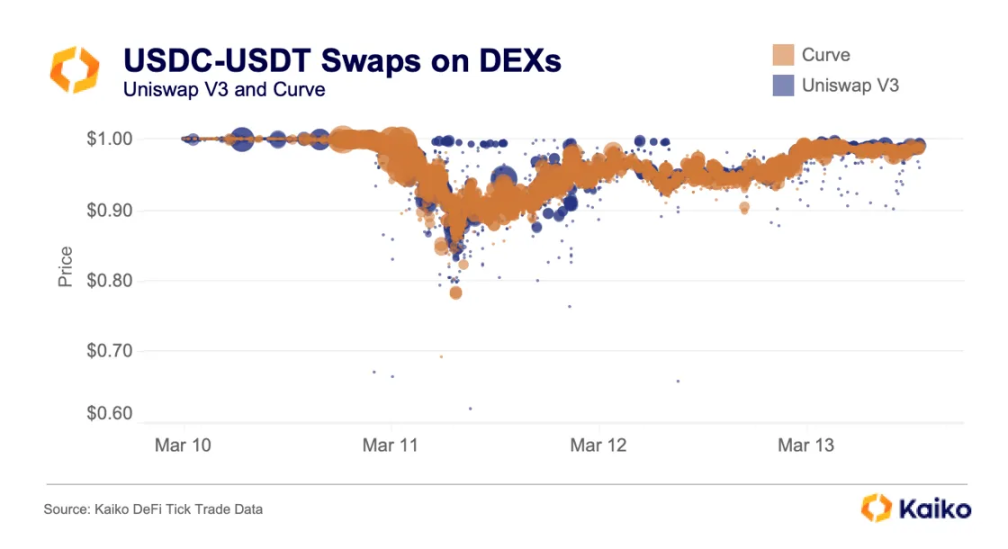

上周末,Uniswap 与 Curve 创造了历史最高的交易量,因为交易者将 USDC 兑换成 ETH 或 USDT 等稳定币。自 3 月 10 日以来,Curve 与 Uniswap V3 上的 USDC-USDT 交易量几近相同,分别为 59.1 亿美元与 59.6 亿美元。在 Uniswap V3 上,USDC-USDT 汇率达到 0.6188: 1 低点;在 Curve 上则达到 0.6911: 1 。

兑换 USDC 热潮使 Curve 3 pool 严重失衡,USDT 在池中的占比达到 2% 左右低点。3 月 13 日, 3 pool 总价值不到 4 亿美元,其中近 95% 是 USDC 和 DAI,再次反映了市场对 USDT 的强烈需求。

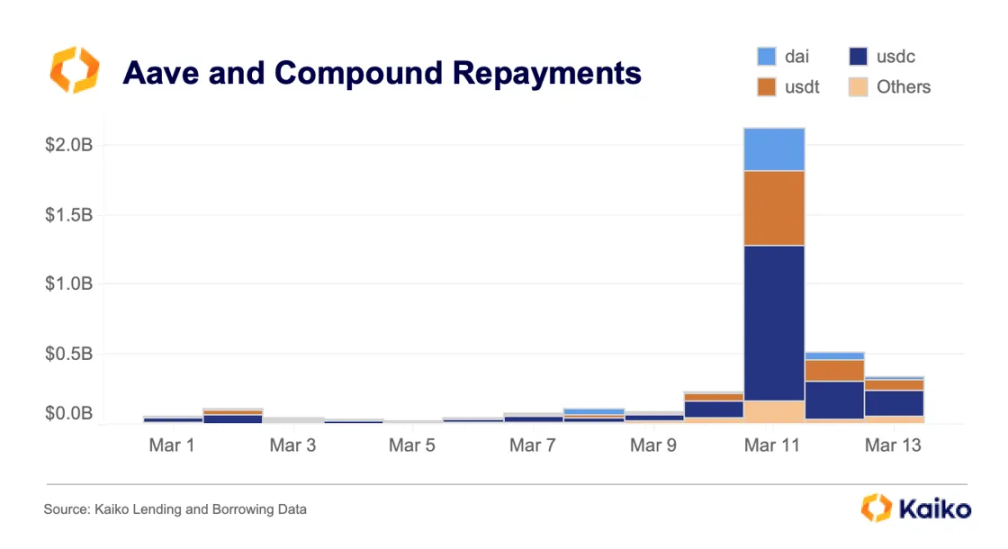

借贷池也受到影响。3 月 11 日,Aave 和 Compound 收到超过 20 亿美元的还款,其中大部分是 USDC,因为借款人能够因其脱锚而以低价偿还贷款。

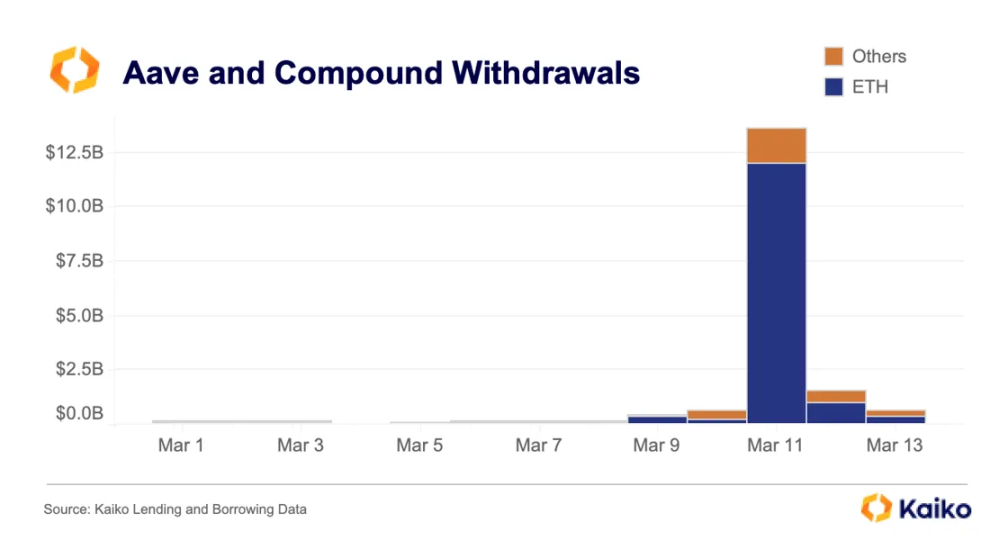

从 Compound 撤出 4 亿美元,从 Aave 撤出 131 亿美元,其中 119 亿美元是 ETH。请注意,这并不意味着 TVL 下降了 131 亿美元;那天 Aave 上有 136 亿美元存款,因为机器人在该协议上特别活跃。

总的来说,DeFi 市场经历了两天巨大的价格错位,整个生态系统产生了无数的套利机会,并凸显了 USDC 的重要性。

二、市场流动性情况

现在,让我们把视野打开,看看这几家银行倒闭对市场究竟造成了多大的冲击。

美元支付渠道的中断意味着美国的做市商一直在从交易所中撤出流动性,因为他们决定如何能够安全地恢复在加密市场提供流动性。

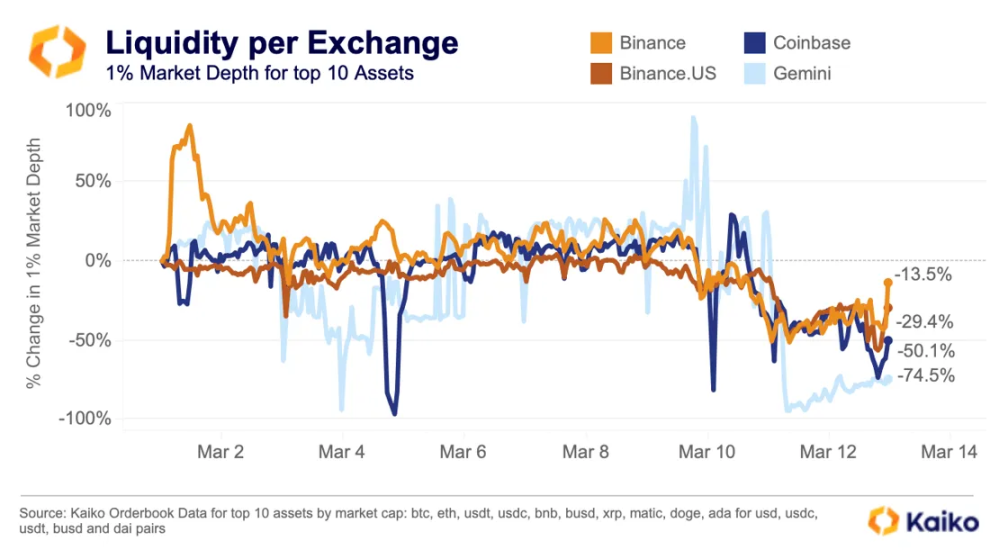

因此,美国交易所在流动性方面受到的打击最大,Gemini 市场深度在 3 月下降 74% ,Coinbase 下降 50% ,Binance.US 下降 29% 。另一方面,得益于其更多的全球市场风险敞口,本月迄今为止,币安的流动性仅下降 13% 。

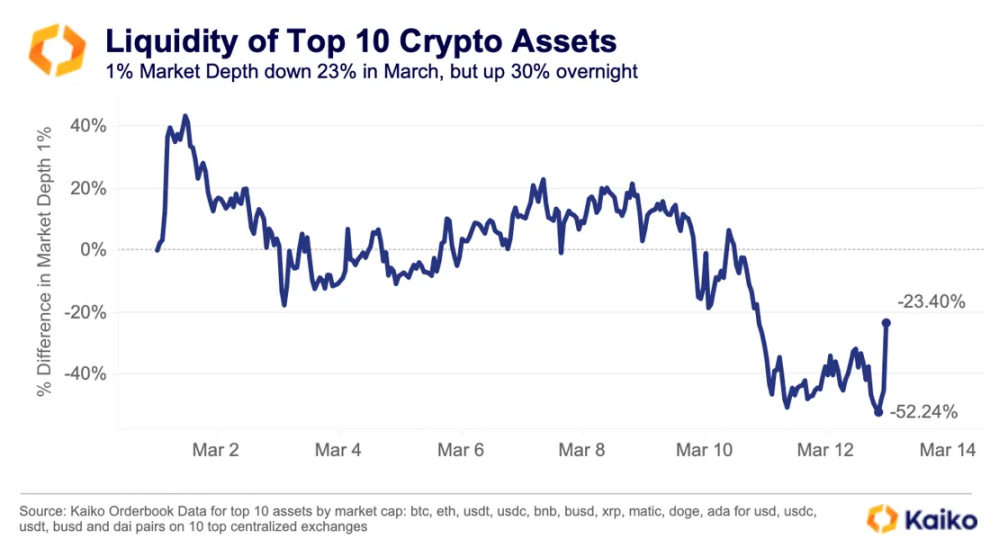

当流动性全面下降时,我们可以看到价格的剧烈波动,缺乏流动性无疑在对救助消息的反应中产生影响。在市值前十的加密资产中, 3 月迄今至硅谷银行储户将得到补偿的消息传出之前,加密市场的流动性下降 52% ,加剧了紧随其后的价格波动。

然而,由于价格效应促进了交易所 USD 流动性的恢复,市场深度一夜之间增加了超过 1.25 亿美元,占比 30% 。

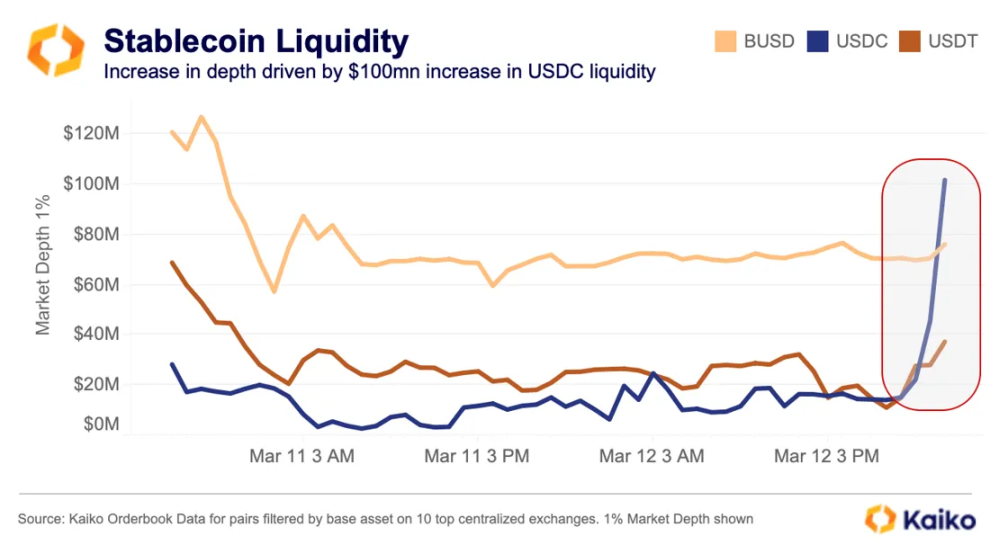

虽然价格会影响交易所 USD 流动性数据,但仔细看看交易对层面的流动性,会发现很大一部分增长实际上来自于 USDC 流动性的恢复。很明显,Circle 将于周一上午获得其在硅谷银行中的 33 亿美元,USDC 会更接近于锚定汇率,做市商很乐意再次开始为 USDC 对提供流动性。

以 USDC 为基础资产,一夜之间提供的额外流动性超过 1 亿美元,其中超过 6000 万美元属于 Binance 上重新上架的 USDC-USDT 交易对,而 Kraken 上的 USDC-USD 交易对也注入了 2000 万美元的流动性。

三、牛市反转:币安行业复苏基金

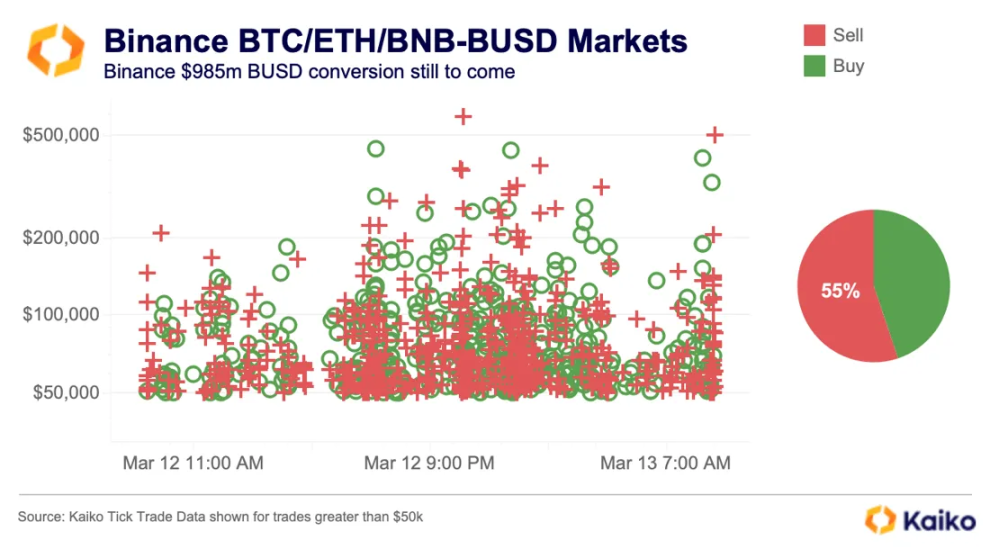

与此同时,币安宣布将把其 10 亿美元行业复苏基金的剩余资产从 BUSD 兑换为 BTC、ETH 与 BNB。该公告是在稳定币波动之后发布的,其中 BUSD 受到牵连,因为其 2.5 亿美元的储备存放在已关闭的 Signature Bank 中。虽然美国政府官员表示所有储户将得到补偿,但从波动性和流动性的角度来看,币安显然认为 BTC、ETH 与 BNB 是更安全的短期选择。

尽管在硅谷银行储户将得到补偿的消息传出后市场出现反弹,但 BTC、ETH 与 BNB 可能会流入更多积极的资金,因为币安似乎尚未将 BUSD 兑换成上述资产。我们的交易数据显示,在过去 24 小时内,交易所 BUSD 对的卖单仍然超过了买单,没有超额的买单。

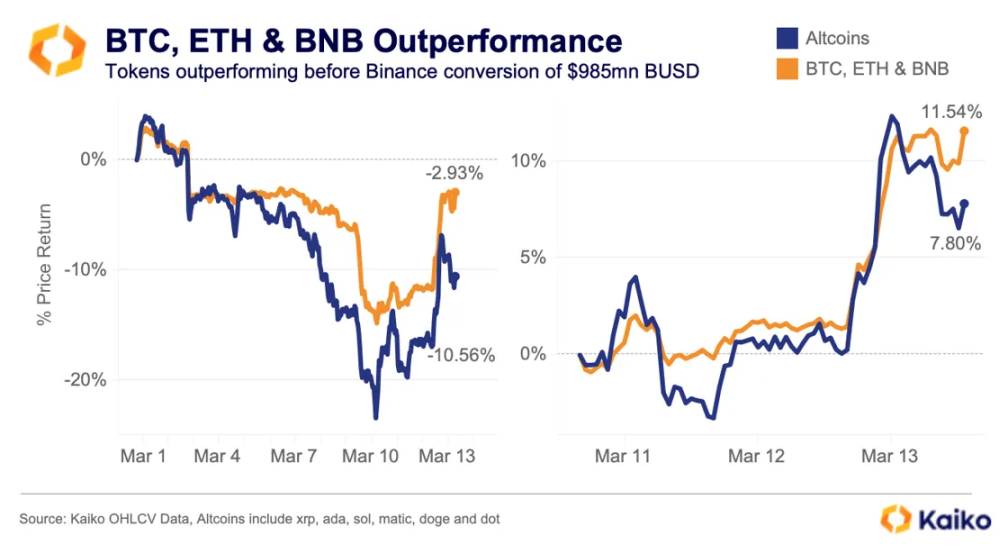

考虑到这一兑换还没完成,BTC、ETH 与 BNB 将有可能在短期内跑赢大盘。本月以来,这三种加密货币的表现优于一篮子山寨币 7.5% ,尽管受到最近市场波动的影响,但仅下跌了 2.9% 。自 3 月 11 日市场触底以来,这三种加密货币上涨 11.5% ,而山寨币的回报率为 7.8% 。

四、后果

虽然 Silvergate 与 Signature 倒闭的全部后果尚未可知,但我想到了以下几个潜在后果:

首先,对市场流动性的影响将是广泛的。随着 Silvergate 与 Signature 的关闭,加密市场基础设施已经倒退,因为加密行业与传统银行系统的关系更加割裂。诸如 Silvergate 交易网络(SEN)、SigNet 等实时支付网络对于管理隔夜和周末的流动性至关重要——促进 OTC 交易、交易所之间的套利以及正常开放时间之外的稳定币兑现。随着这些解决方案的消失,并且暂时没有替代方案,法币入金可能会恶化,更有可能导致价格波动。

尽管美联储通过新设立的银行定期融资计划(BTFP)改善了市场流动性,但货币政策的不确定性已经上升,可能会进一步助长机构交易者的避险情绪。根据美国利率期货,市场对美联储终端利率的预期从上周的近 6% 降至周一上午的 5% 左右。根据 CME FedWatch 工具,对下周美联储会议上加息 50 bps 的预期在几天内从 40% 降至零。

总的来说,加密行业再次度过一次重大的市场危机,截至周一上午,市场已处于比较稳定的状态。