Arthur Hayes:2023会和2022一样糟糕吗?

原文作者:Arthur Hayes

原文编译:GaryMa 吴说区块链

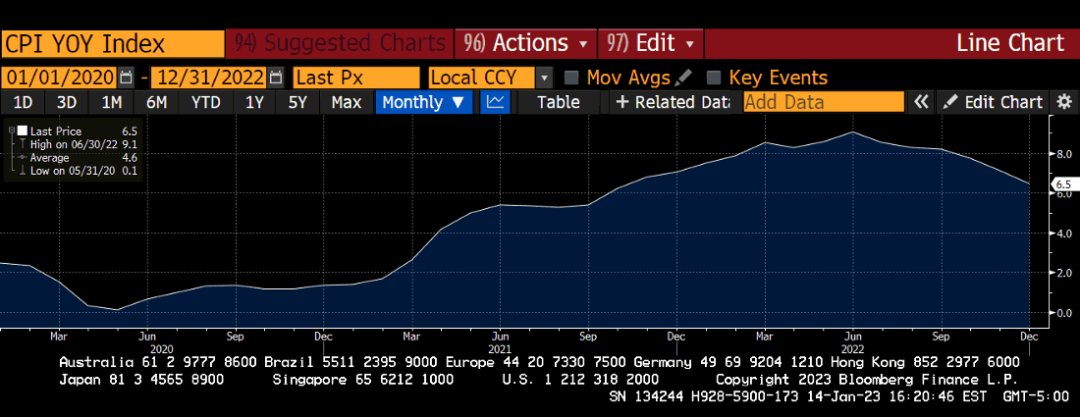

US CPI 同比指数

从上图中可以看出,由美国劳工统计局发布的(有缺陷和误导性的)消费者价格指数(CPI)系列衡量的通货膨胀率在 2022 年年中达到 9% 左右的峰值,现在正朝着至关重要的 2% 水平急速下降。

有很多人认为 CPI 最近的稳步下降趋势只意味着一件事:鲍威尔准备重新放水,像 2020 年 3 月一样。随着美国甚至可能还有全世界处于衰退的边缘,那些预言者会说,鲍威尔正在寻找一切机会,从他目前的量化紧缩(QT)政策转向,如果我们进入经济衰退,该政策将承担很大一部分责任。随着 CPI 的下降,他现在可以指着下跌说,他杀死通胀这头猛兽的正义运动已经成功,现在可以放心地重新打开水龙头了。

我不太确定这些预测是正确的,但等下我们会有更多讨论。现在,让我们假设市场认为这是最有可能的前进道路,那么,我们能期望比特币如何反应?为了准确地建模,我们必须记住关于比特币的两件重要事情。

首先,比特币和更广泛的加密资本市场是唯一真正不受央行行长和大型全球金融机构操纵的市场。你可能会问:“但 3AC、FTX、Genesis、Celsius 等破产公司所谓的不正当行为呢?” 这是一个公平的问题,但我的回答是,随着加密市场价格的调整,这些公司倒闭了,市场很快就找到了一个低得多的清算价格,在这个价格上,杠杆被淘汰出了系统。如果同样鲁莽的行为发生在 TradFi 系统中,当局就会试图通过支持濒临破产的实体(他们一直都是这样做的)来推迟市场的清算,并在这个过程中破坏了他们本应保护的经济,但加密货币领域面临着严峻的挑战,并迅速清理了经营不善、商业模式有缺陷的企业,为迅速而健康的反弹奠定了基础。

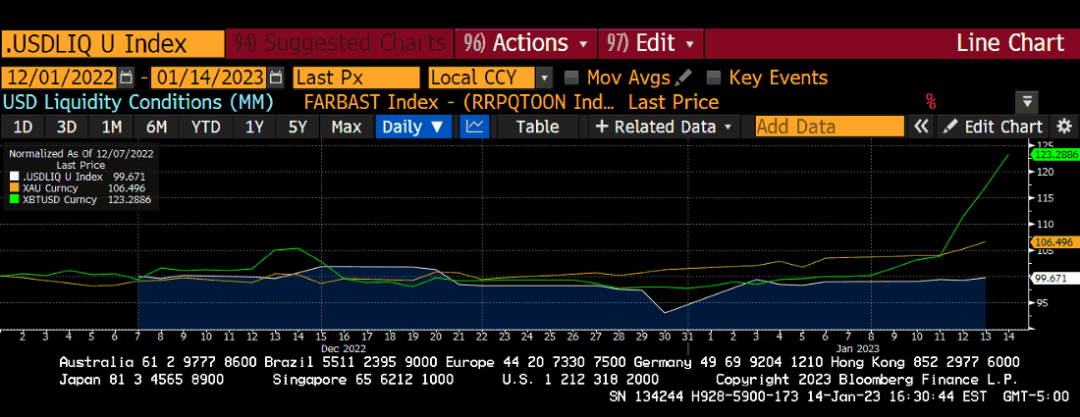

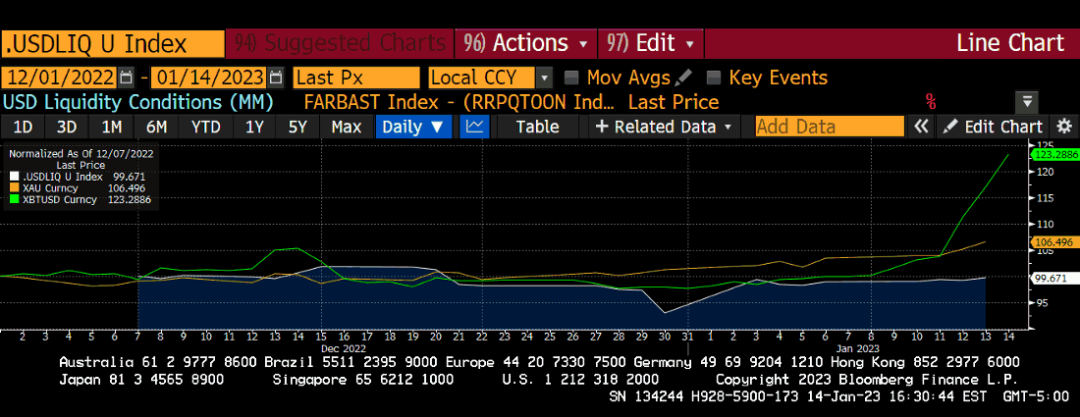

关于比特币要记住的第二件事是,因为它是对世界全球法定货币体系挥霍的一种反应,它的价格在很大程度上依赖于美元全球流动性的未来路径(由于美元作为全球储备货币)。我在最近的文章中详细地谈到了这个概念和我的美元流动性指数。为此,在过去两个月里,比特币的表现超过了持平的美元流动性指数。在我看来,这表明市场认为美联储的转向已经来临。

黄金(黄色),比特币(绿色),美元流动性指数(白色),指数为 100

看看比特币的价格走势,它目前从一个低位开始拉升。从这里,我们可以根据实际推动反弹的因素确定几种不同的潜在前进路径:

反弹催化剂情景 1 :比特币只是从低于 1.6 万美元的本地低点经历了自然反弹。

● 如果这次反弹真的只是局部低点的自然反弹,我预计比特币随后将找到一个新的平台,并横盘移动,直到美元流动性状况改善。

反弹催化剂情景 2 :比特币上涨是因为市场领先于美联储恢复印钞。如果是这样的话,我认为可能会出现两种情况:

● 情景 2 A:如果美联储没有实施转向,或者多位美联储官员在 CPI 数据 “良好” 之后也不太看好转向的预期,比特币可能会跌回之前的低点。

● 情景 2B:如果美联储真的实施了转向政策,比特币将继续保持强劲表现,这次反弹将成为长期牛市的开始。

显然,我们都愿意相信我们正在走向情景 2B。也就是说,我认为我们实际上将面临情景 1 和 2 A 的某种组合,这让我那发痒的 “买入” 手指有点犹豫。

虽然我相信美联储将会转向,但我不认为它会仅仅因为 CPI 趋于下降而发生。鲍威尔宣称,他更关注工资增长(美国时薪)与核心个人消费支出(核心 PCE)之间的相互作用,而不是依赖 CPI 作为衡量通胀的指标。说句题外话,我认为 CPI 和核心 CPE 都不是衡量通胀的好指标。核心个人消费支出尤其虚伪,因为它不包括食品和能源。平民们不会因为平板电视的价格上涨而闹事,而是因为面包的价格上涨 100% 而闹事。但不管我怎么想,对我们的预测工作来说,重要的是鲍威尔已发出电报,表示他打算将有关潜在政策转向的任何决定,不仅基于 CPI,还基于美国工资增长与核心个人消费支出的对比。

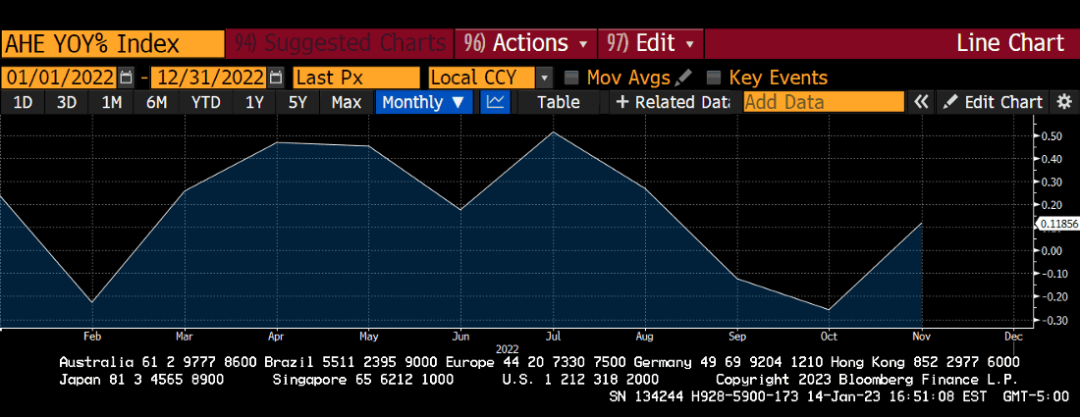

美国每小时收入的变化减去核心 PCE 的变化,均为同比增长百分比

从上图中可以看出,美国的平均工资增长速度与通货膨胀速度相同。这意味着,虽然商品越来越贵,但由于工资的增长,人们购买这些商品的能力实际上也在以类似的速度增长。因此,人们购买力的增强可能会进一步推动商品通胀。换句话说,商品生产商可能会意识到,他们的买家现在比以前赚了更多的钱,并进一步提高价格,以更多地吸收买家最近的工资增长,所有这些都不用担心会扼杀对他们产品的需求。因此,鲍威尔实际上有理由继续提高利率(即抑制消费需求,阻止商品价格进一步上涨)。而且他很可能会使用它,因为他已经表示,他正在寻求确保整个美国国债曲线的收益率高于通货膨胀率(目前还没有)。

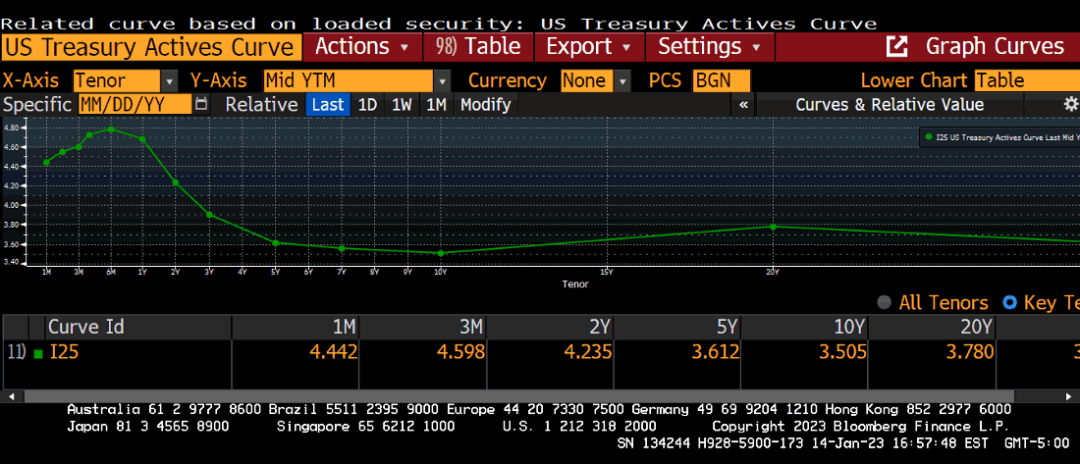

美国国债活跃度曲线

2022 年 12 月核心个人消费支出同比增长 4.7% 。从上面的曲线可以看出,目前只有 6 个月期国库券的收益率高于 4.7% 。因此,鲍威尔有很大的回旋余地继续加息。更重要的是,继续缩减美联储的资产负债表,进一步收紧货币环境,使其达到他希望的水平。

这最后几张图表和一些言论的意义只是表明,不断下降的 CPI 数字毫无意义,因为它与鲍威尔用来判断美联储是否成功遏制通胀的实际指标不一致。CPI 的下降可能意味着什么,但我不认为它会以任何有意义的方式来预测美联储最终转向的时间。

也就是说,我确实相信,如果鲍威尔无视 CPI 数据,继续通过 QT 收缩美联储的资产负债表,这将导致信贷市场严重混乱,并迫使他们积极转向。

自 2022 年 4 月 13 日达到 8.965 万亿美元的高点以来,截至 2023 年 1 月 4 日,美联储的资产负债表已经减少了 4580 亿美元。美联储本应在 2022 年将资产负债表总额缩减 5230 亿美元,因此他们已经实现了 88% 的目标。目前的 QT 利率表明,资产负债表每月将再减少 1000 亿美元, 2023 财政年度将再减少 1.2 万亿美元。如果在 2022 年抽走 5000 亿美元导致了几百年来最差的债券和股票表现,想象一下,如果在 2023 年取消一倍的金额会发生什么。

市场在注入和撤出资金时的反应是不对称的。因此,我预计意外后果定律将在美联储继续收回流动性时咬着它的屁股。我也相信鲍威尔本能地理解这一点,因为尽管他的 QT 非常激进,但按照目前的速度,需要很多年才能完全扭转新冠疫情开始后印钞的数量。从 2020 年 3 月中旬到 2022 年 4 月中旬,美联储印了 4.653 万亿美元。按每月削减 1000 亿美元计算,大约需要 4 年时间才能完全恢复到疫情前的美联储资产负债表水平。

如果美联储真的想要扭转货币增长,它应该直接出售 MBS 和美国国债,而不是仅仅停止对到期债券进行再投资。鲍威尔本可以加快步伐,但他没有,这表明他知道市场无法承受美联储抛售其资产。但我仍然认为,他高估了市场应对美联储继续被动参与的能力。MBS 和国债市场需要美联储的流动性,如果 QT 继续以同样的速度增长,这些市场以及所有其他从这些基准获得估值和定价的固定收益市场很快就会陷入痛苦的世界。

美联储转向情景分析

在我看来,有两件事可能会促使美联储转向:

1. 鲍威尔认为 CPI 指标的下降证实了美联储已经做得足够多,可以在不久的某个时候暂停加息,如果 23 年下半年出现温和衰退,可能会停止 QT 并降息。货币政策通常有 12 到 24 个月的滞后,因此鲍威尔看到 CPI 呈下降趋势,可以相信根据过去一年发生的情况,通胀将在不久的将来继续回到 2% 的圣杯。正如我上面所概述的,我认为这种情况不太可能发生,因为我不认为鲍威尔使用 CPI 作为通货膨胀的衡量标准,但这也不是不可能。

2. 美国信贷市场的某些部分崩溃,导致涉及广泛金融资产的金融崩溃。作为与 2020 年 3 月类似的反应,美联储召开紧急新闻发布会,停止 QT,大幅降息,并通过再次购买债券重新启动量化宽松。

在情景 1 中,我预计风险资产价格将缓慢上行。我们不会再回到 2022 年的低点,对基金经理来说,这将是一个令人愉快的环境。只要坐下来,看着 CPI 的基础效应发挥作用,机械地降低整体数据。美国经济会发现自己处于一个一般的位置,但不会发生非常糟糕的事情。即使出现轻微衰退,也不会像我们在 2020 年 3 月至 4 月期间或 2008 年全球金融危机期间所看到的那样。在这两种情况中,这是首选的一种,因为这意味着你可以在经济向好通胀持低之前,现在就开始买入。

在情景 2 中,风险资产价格暴跌。随着以美元为基础的全球金融体系的粘合剂溶解,债券、股票和太阳下的每一种加密货币都会被熏黑。想象一下,美国 10 年期国债收益率从 3.5% 迅速翻倍至 7% ,标准普尔 500 指数跌破 3000 点,纳斯达克 100 指数跌破 8000 点,比特币以 1.5 万或更低的价格交易。就像一头被车灯照到的鹿一样,我期待鲍威尔爵士会骑上马,带领印钞大军前来救援。这种情况不太理想,因为这意味着现在购买风险资产的每个人都将面临业绩大幅下滑。在美联储转向之前, 2023 年可能和 2022 年一样糟糕。

我的猜想是情景 2 。

黄金为何涨?

黄金(黄色),比特币(绿色),美元流动性指数(白色),指数为 100

对我的情景 2 基本假设最合理的反驳是,黄金也随着比特币一起上涨。黄金是一种流动性更强、更值得信赖的抗脆弱资产,它也有类似的目的,即它也是一种对冲法定货币体系的工具。因此,乍一看,你可能会合理地推测,黄金最近的上涨进一步证明了市场相信美联储将在不久的将来调整政策。这是一个合理的推断,但我怀疑黄金的上涨完全是出于另一个原因。因此,重要的是不要把黄金和比特币的上涨混为一谈,认为这是美联储即将转向的共同证实。让我解释一下。

黄金是主权货币,因为在一天结束的时候,民族国家总是可以用黄金来结算货物和能源贸易。这就是为什么每个中央银行的资产负债表上都有一定数量的黄金。

由于每个央行都持有一定数量的黄金,当一国货币必须贬值以保持全球竞争力时,央行总是诉诸于对黄金贬值。最近的一个例子是,美国在 1933 年和 1971 年让美元对黄金贬值。这就是为什么我在投资组合中配置了大量的实物黄金和金矿商。与央行并肩投资总是比与央行作对要好。

我(和其他许多人)已经写了大量关于在最近几个关键的地缘政治事件(如美国冻结俄罗斯在西方金融体系中持有的“资产”)之后,未来几年世界去美元化将如何加速的文章。我预计,世界上廉价劳动力和自然资源的生产者迟早会意识到,如果他们惹怒了美国众国,他们可能面临与俄罗斯同样的命运,那么把财富储存在美国国债上是没有意义的。这使得黄金成为最明显、最具吸引力的投资目的地。

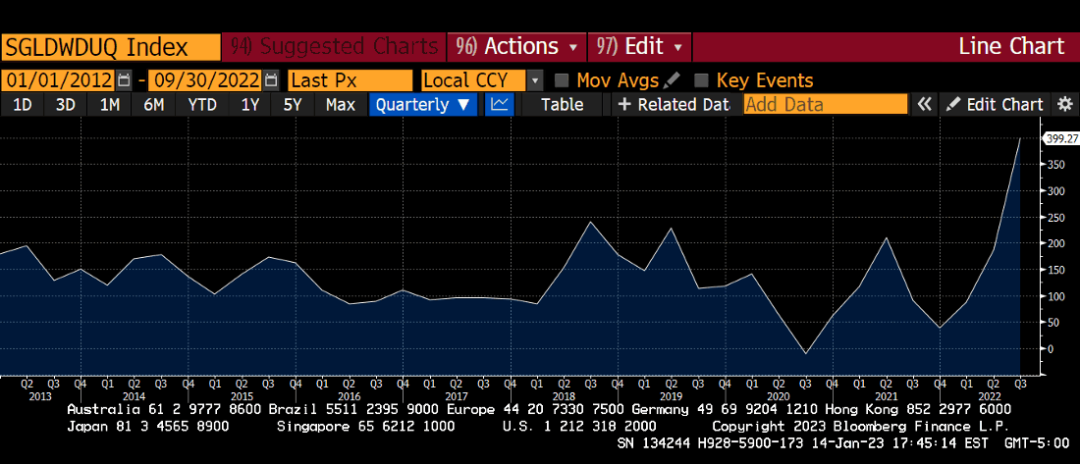

这些数据支持了这样一种观点,即各国政府正转向以历史悠久的主权储备货币,黄金来储存财富。下图追溯至 10 年前,描绘了各国央行的黄金净购买量。正如你所看到的,我们在 2022 年第三季度创下了历史新高。

中央银行的黄金净购买量(公吨)

廉价能源的峰值已经来临,许多国家的首脑都认识到了这一点。他们本能地知道,就像大多数人一样,黄金在能源方面(原油)的购买力比美元等货币要好。

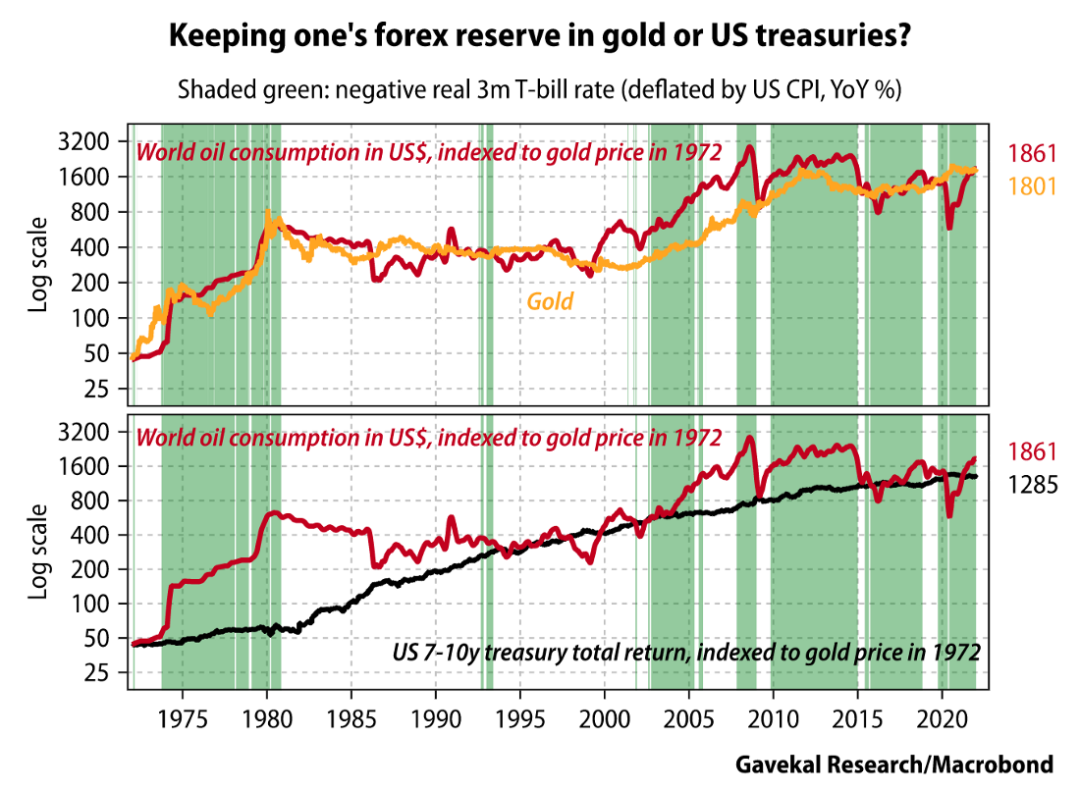

这张来自 Gavekal Research 的优秀图表清楚地表明,黄金是比美国国债更好的能源储存方式。

在我看来,这些数据表明,金价上涨更多是因为真实的实物需求,而不是因为世界各国央行认为美联储将转向。当然,至少有一部分是由于预期美联储的货币政策可能会在不久的将来放松,但我不认为这些预期是背后的驱动力。

交易筹备

如果我错了,经济好通胀低的情景 1 发生了怎么办?

这意味着我已经错过了从底部反弹的时机,比特币不太可能回头,因为它正无情地朝着历史新高前进。如果这是真的,加息可能会分两个阶段进行。在第一阶段,精明的投机者将走在美联储政策实际转变的前面。在这一阶段,比特币很容易交易到 3 万至 4 万美元,因为目前价格受到 FTX 后看跌情绪的严重打压。下一阶段将使我们达到 6.9 万美元或更高,但只有在大量美元注入加密资本市场后才能开始。这样的注入至少需要暂停加息和 QT。

如果我错了,我很乐意错过从底部反弹的最初机会。我已经做多了,所以无论如何我都会受益。但是,我以短期国库券形式持有的美元会突然表现不佳,我需要将这些资金重新配置到比特币上,以最大化我的投资回报。不过,在我放弃以 5% 收益率购买的债券之前,我希望有高度的信心,牛市已经回来了。5% 显然低于通货膨胀率,但这比下跌 20% 要好,因为我没有把握好市场时机,在下一个周期过早购买了风险资产。

当他们真的决定转向时,美联储将事先明确传达他们将放弃紧缩货币政策。美联储在 2021 年底告诉我们,他们将转向通过限制货币供应和加息来对抗通胀。他们坚持到底,并于 2022 年 3 月开始这样做,任何不相信他们的人都被屠杀了。因此,同样的事情很可能在另一个方向发生,也就是说,美联储会告诉我们什么时候结束,如果你不相信他们,你就会错过随后的猛涨。

由于美联储尚未发出转向的信号,我可以等待。我认为第一是保本,第二是增长。我宁愿买入一个在美联储传达转向之后已经从低点反弹 100% + 的市场,也不愿买入一个从低点反弹 100% + 的市场,因为转向没有发生,然后由于糟糕的宏观基本面而遭受 50% + 的回调。

如果我是对的,灾难性的情景 2 发生了(即全球金融崩溃),那么我就有再一次抄底机会。我将知道市场可能已经触底,因为当系统暂时崩溃时发生的崩溃要么保持之前的 15800 美元低点,要么就不会。向下最终达到什么水平并不重要,因为我知道美联储随后将采取行动印钞,避免另一场金融崩溃,这反过来将标志着所有风险资产的底部。然后我得到了另一个类似于 2020 年 3 月的场景,加紧购买加密货币。